NFCI: What the 105 Sub-Variables Actually Measure (Risk, Credit, Leverage)

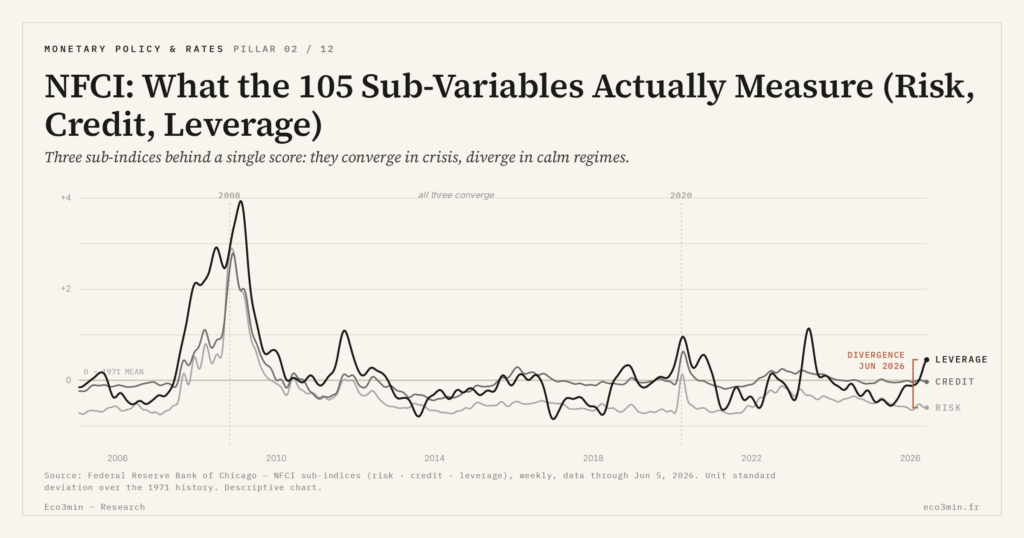

The aggregate NFCI masks its internal machinery. Beneath the composite score, the Chicago Fed publishes three sub-indices in parallel — risk, credit, leverage — each built from a subset of 105 weekly series.

TL;DR

A zero NFCI can mean two opposite things: all three sub-indices calm, or some tightening while others ease and cancel out, hiding a fragility the aggregate score never shows.

- The risk sub-index (NFCIRISK) tracks money-market and volatility stress: the TED spread ran from 30 bps in June 2007 to a record 460 bps in October 2008; typical weight 25-35%.

- The credit sub-index (NFCICREDIT) dominates the current regime: in May 2026 IG spreads sit near 85 bps and HY near 280 bps, historically tight against 1996-2024 averages of about 145 and 520 bps; weight 30-55%.

- The leverage sub-index (NFCILEVERAGE) reads intermediary balance sheets: margin debit, hedge-fund flows (equity long-short shed $27bn in March 2020) and primary-dealer inventories; a cross-sub-index standard deviation above 0.30, as in May 2026, marks structural divergence.

Reading the sub-index decomposition changes the analytical grammar. Inter-market divergence is often more informative than the aggregate value itself.

1. Why decompose the aggregate: analytical stakes

The weekly NFCI published by the Chicago Fed since 1971 is a composite measure. Read at its aggregate value alone, it discards the internal stress structure — which is often more informative than the composite score. When the aggregate index sits at zero, two radically different configurations are possible: the three sub-indices are simultaneously at zero (generalized equilibrium), or some sub-indices are positive while others are negative and offset on average (unstable equilibrium masking fragility). Without decomposition, these two regimes are not distinguishable.

The Chicago Fed publishes every Friday at 8:30 AM Chicago time, alongside the aggregate, the three sub-indices NFCIRISK, NFCICREDIT, and NFCILEVERAGE. Each is built from a subset of the 105 observed series, aggregated by the same dynamic factor model (DFM) and normalized following the same conventions (zero mean, unit standard deviation over the 1971-2026 history). The technical construction detail is treated in the article on how the aggregate is computed. For ongoing weekly access to all three series, the FRED NFCI dataset for the raw series provides direct download.

This decomposition is a financial conditions transmission structured by channel: risk, credit, leverage are three distinct propagation channels between the financial system and the real economy. Each channel mobilizes different actors, markets, and timescales. The purpose of this article is to map the real content of each of the three sub-indices and to provide a coherence-or-divergence reading grid, which analytically extends the reading of the aggregate index as meta-measure without replacing it.

2. The risk sub-index: money markets, volatility, short-term funding

The risk sub-index (NFCIRISK) measures tensions on money markets and financial volatility indicators. Its main components fall into four families: short-term funding spreads, gaps between market rates and risk-free rates, implied volatility indices, and certain market liquidity measures.

Short-term funding spreads include the commercial paper spread (gap between financial CP three-month rate and Treasury 3-month rate), repo spreads (general collateral repo rate versus Fed Funds), and the Eurodollar-OIS gap. These measures capture the ease or difficulty for financial institutions to refinance on wholesale markets. In normal times, the commercial paper spread oscillates between 10 and 30 basis points; in stress periods (August-September 2007, March 2020), it can jump to 200-400 basis points within weeks.

Gaps between market rates and risk-free rates historically include the TED spread (3-month LIBOR minus 3-month Treasury, through LIBOR cessation in June 2023), then OIS-SOFR spread since 2018, and the swap spread (gap between fixed leg of an interest rate swap and Treasury yield at matching maturity). These spreads capture the counterparty risk premium on interbank and derivatives markets. The TED spread went from 30 basis points in June 2007 to 460 basis points in October 2008, a record level that on its own summarizes the market-credit signature of the GFC.

Implied volatility indices include the VIX (30-day implied volatility on S&P 500, CBOE) and the MOVE (bond market implied volatility computed by Merrill Lynch since 1988 from options on Treasuries). Our VIX history series compiles the full historical series. These two measures give the ex-ante risk premium embedded in options. The VIX historical average is around 19; peaks exceed 80 (November 2008, March 2020). The MOVE historical average is around 90 basis points; peaks exceed 200 (March 2020, March 2023).

The risk sub-index weight in the aggregate typically varies between 25 and 35%, with excursions above 40% during purely volatility-markets shocks (October 1987, August 2011 during the European crisis).

3. The credit sub-index: corporate spreads, bank lending, non-bank financing

The credit sub-index (NFCICREDIT) measures the ease or difficulty of obtaining debt financing in the U.S. economy, through the three main channels: commercial bank credit, market-based corporate credit, non-bank financing. It is the densest sub-index in terms of underlying series, and the one that dominates in adaptive weighting during pure credit stress episodes.

Commercial bank lending conditions are measured by the Senior Loan Officer Opinion Survey (SLOOS), a quarterly Fed survey addressed to roughly 80 domestic banks and 24 foreign bank branches. SLOOS asks credit officers whether they have tightened or loosened their lending standards over the quarter, and the net fraction of banks having tightened enters the sub-index. A positive net fraction (more banks tightening than loosening) pulls the sub-index up. The Q4 2008 SLOOS recorded net tightening from 84% of banks on large enterprise loans — a record. In Q1 2023, the net fraction reached 46%, a historically elevated level that nonetheless did not push the aggregate above 0.5.

Market-based corporate spreads are measured through ICE BofA indices: US Corporate Master OAS for investment grade, US High Yield Master OAS for high yield. These daily series are averaged weekly to enter the sub-index. The historical 1996-2024 IG average is around 145 basis points; the HY average around 520 basis points. Peaks exceed 600 bps (IG) and 1,800 bps (HY) in November 2008. In May 2026, levels are respectively at 85 bps and 280 bps, historically tight levels.

Non-bank financing includes non-financial commercial paper (rate and volume), ABCP (asset-backed commercial paper, whose market collapsed between August 2007 and 2010 and never recovered its pre-crisis volume), some leveraged loan secondary rates, and the NACM Credit Manager Index published monthly by the National Association of Credit Management. NACM measures the ease of inter-business commercial credit on a sample of 1,000 credit managers.

The credit sub-index weight typically varies between 30 and 55%, and dominates in the 2007-2008 episodes and in the 2024-2026 accommodative regime.

4. The leverage sub-index: margin, hedge funds, dealers, investment banks

The leverage sub-index (NFCILEVERAGE) measures leverage and balance sheet conditions at financial intermediaries and leveraged investors. It is the hardest sub-index to interpret without knowing the balance sheet mechanics of market intermediaries, but it is also the one that captures the most systemically dangerous stress episodes (LTCM 1998, GFC 2008, March 2020). Directly related: the mechanics of liquidity and QT.

Main components include broker net margin debit (margin debit published monthly by FINRA since 2010, and previously by the Federal Reserve), which measures the total amount of retail and institutional positions purchased with borrowed funds at their brokers. Net margin debit peaked at 935 billion dollars in October 2021 (absolute record) before declining to around 700 billion by May 2026.

Hedge fund flows are captured via the TASS and HFR databases. Net monthly hedge fund outflows pull the sub-index up (signal of disengagement and liquidity pressure). Equity long-short hedge funds recorded net outflows of 21 billion in September 2008 and 27 billion in March 2020. Macro and CTA funds have inverse profiles: massive inflows during stress periods (hedge role). Divergent in flow, these vehicles run on the same financing plumbing — and that plumbing is what sets the transmission role of leveraged funds in market stress.

Primary dealer positions, published weekly by the New York Fed, measure the net inventory of the 24 primary dealers in Treasuries, MBS, and corporate bonds. In stress periods, dealers reduce inventory synchronously, creating dislocations on underlying markets — precisely what happened in March 2020 on the Treasury market and triggered the massive Fed intervention.

Investment bank leverage ratios come from quarterly Y-9C call reports (Federal Reserve regulation on bank holding companies). This less frequent source is integrated by weekly interpolation in the sub-index.

The leverage sub-index weight is typically 20-30%, but can exceed 45% in balance sheet crises (October 2008 record at 45%).

5. Reading coherence or divergence among the three sub-indices

The main analytical value of decomposition lies in coherence-or-divergence reading. When the three sub-indices move in the same direction with comparable magnitudes, the aggregate summarizes without distorting the signal — typical of major systemic shocks (October 2008, March 2020). When one or two sub-indices diverge durably, the aggregate masks structural information — the May 2026 case, where the credit sub-index is at around −0.7 (very accommodative) while leverage is at +0.1 (marginally restrictive).

This reading grid justifies systematically looking at the three sub-indices alongside the aggregate, and computing their instantaneous dispersion. A three-sub-index standard deviation below 0.15 indicates a robust signal where the aggregate suffices; above 0.30 indicates structural divergence where decomposition becomes primary information.

This reading grid complements without replacing the comparison with VIX and HY OAS, which examines the relationship between aggregate NFCI and other external indicators of U.S. financial stress.

- The aggregate NFCI masks three distinct sub-indices (risk, credit, leverage) published in parallel by the Chicago Fed every Friday under FRED codes NFCIRISK, NFCICREDIT, NFCILEVERAGE.

- The risk sub-index weights money markets, short-term funding gaps, VIX and MOVE; typical weight 25-35%.

- The credit sub-index aggregates SLOOS, IG and HY ICE BofA spreads, non-bank financing; typical weight 30-55%, dominant in credit stress.

- The leverage sub-index captures net margin debit, hedge fund flows, primary dealer positions, and investment bank balance sheet ratios; typical weight 20-30%, up to 45% in balance sheet crises.

- Coherence or divergence among sub-indices is often more informative than the aggregate value itself; a three-sub-index standard deviation above 0.30 signals structural divergence.

Last updated — 23 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…