NFCI: The Chicago Fed Meta-Indicator of U.S. Financial Conditions Since 1971

Every Friday the Chicago Fed publishes the NFCI, a weekly index aggregating 105 financial variables since 1971. Reading it by standard deviation rather than by binary threshold reveals where the current regime sits within 55 years of U.S. macro-financial history.

TL;DR

The Chicago Fed's NFCI compresses 105 financial variables into one weekly figure available since 1971, the longest continuous record of U.S. financial conditions at weekly frequency.

- Its weekly series starts in January 1971 and runs about 2,880 observations through May 2026; the St. Louis (1993), Goldman Sachs (1990), Bloomberg (1991) and Kansas City (1990) alternatives all start at least two decades later.

- Roughly 60% of U.S. non-financial corporate financing flows through capital markets and 40% through banks, a ratio reversed in the euro area, which is why the index weighs both SLOOS bank surveys and market spreads.

- May 2026 prints -0.55, an accommodative reading in which the credit sub-index carries roughly 50% of the aggregate's weight, against about 30% risk and 20% leverage.

- Above +0.5 about 16% of the time and above +2.0 less than 1% (six episodes since 1971), the index has preceded every NBER recession with a 6-to-12-month median lead when it holds above 0.5.

May 2026: the index prints at −0.55, an accommodative level rarely observed after a tightening cycle. The ongoing compression challenges the canonical reading of Fed-to-financial-conditions transmission.

1. NFCI within the U.S. financial stress indicator ecosystem

The National Financial Conditions Index is released every Friday morning at 8:30 AM Chicago time by the Federal Reserve Bank of Chicago. The series starts the week of January 8, 1971 and counts roughly 2,880 weekly observations through May 2026. No other U.S. financial conditions indicator spans such a long period at such high frequency: the St. Louis Fed Financial Stress Index goes back to 1993 only, the Goldman Sachs Financial Conditions Index to 1990, the Bloomberg US Financial Conditions Index to 1991, the Kansas City Fed Financial Stress Index to 1990, and most proprietary bank indices (Citi, Deutsche Bank, JPMorgan) to less than 25 years. A related read: How tightening conditions reach markets.

This historical depth is not a technical detail. It means the NFCI has spanned Bretton Woods, the 1970s stagflation, the 1973 and 1979 oil shocks, the Volcker chairmanship, the Savings and Loans crisis from 1986 onward, October 1987’s Black Monday, the Drexel Burnham Lambert collapse in February 1990, the 1997 Asian crisis, the Russian default and Long-Term Capital Management collapse in September 1998, the dot-com bust, the 2007-2009 Global Financial Crisis, the European sovereign debt crisis, the 2020 pandemic, and the post-COVID inflation episode. The historical mean fixed at zero is computed over the entire series since 1971, and each new release marginally recalibrates that mean — a property documented by the Chicago Fed in its 2010 methodological working paper (Brave and Butters) and its 2014 update.

Positioning the NFCI relative to other U.S. stress indicators is essential to understand what it measures. The VIX, computed by the CBOE since 1990, captures the 30-day implied volatility of the S&P 500: a narrow indicator derived from a single market, at intraday frequency. The ICE BofA HY OAS, published since 1996, measures the option-adjusted spread of high-yield bonds over Treasuries: a sub-investment-grade corporate credit risk indicator at daily frequency. The St. Louis Fed STLFSI combines 18 weekly series since 1993, methodologically close to NFCI but with fewer variables and two decades less history. The Kansas City KCFSI uses 11 monthly series since 1990. The NFCI stands out both for its historical depth and its scope: it includes equity volatility and credit spread components among its 105 variables, but adds shadow banking, intermediary leverage, surveyed bank lending conditions through the Fed’s Senior Loan Officer Opinion Survey, wholesale money market flows, and primary dealer balance sheet composition. A NFCI confronted with VIX and HY OAS reveals what each indicator captures and what it ignores.

The consequence is that NFCI does not measure financial stress in the narrow sense. It measures financial conditions broadly: how easy or difficult it is to obtain financing in the U.S. economy at a given moment, across all sources. The term stress enters through the upper end of the distribution. When the index moves significantly into positive territory, conditions become tighter than average. When it moves into negative territory, they are more accommodative than the historical mean. The NFCI’s function is therefore less about flagging point-in-time crises than about providing a stationary measure of the cyclical position of financial conditions over time.

This broad scope has a direct consequence on the index’s temporal profile. VIX can spike from 15 to 40 in a single trading session and fall back within weeks: it is a short-term panic indicator. This dynamic is quantified in the VIX dataset. NFCI moves more slowly because it incorporates series with varying underlying frequencies (some surveys are monthly, some balance sheet data quarterly). In return, its movements are more informative about cyclical positioning. A VIX at 35 may signal an isolated equity shock; an NFCI at +1.0 sustained over eight weeks signals a systemic tightening of financing conditions that alters credit behavior in the real economy.

Another NFCI specificity is its joint coverage of bank financing and market financing. In the United States, roughly 60% of non-financial corporate financing flows through capital markets (corporate bonds, commercial paper, leveraged loans securitized into CLOs, private credit) and 40% through traditional bank credit — a ratio reversed compared to the euro area where bank financing dominates. This structure justifies an aggregate indicator that explicitly weighs both channels. The 105 NFCI series include both SLOOS surveys at commercial banks and market financing spreads, allowing the index to capture episodes where the two channels converge (GFC, COVID) and those where they diverge (for example the mid-2023 bank tightening alongside a concomitant reopening of the HY market). For ongoing access to the underlying series, the FRED NFCI raw dataset page provides direct download.

The topic sits within the monetary regimes and rates pillar, whose dedicated branch addresses specifically liquidity and financial conditions as the transmission belt between the Fed and the real economy. NFCI is one of three or four central indicators in that transmission, alongside the Fed balance sheet measured by WALCL, the Treasury 10-year minus 3-month spread, and corporate credit spreads.

2. How the index is built: 105 variables, three sub-indices, a weighted regression

The NFCI construction methodology is published in the Chicago Fed Working Paper “Diagnosing the Financial System: Financial Conditions and the Financial Crisis” (Brave and Butters, 2010), with a 2014 technical update in the Economic Perspectives journal. The core principle: extract a weighted common factor from 105 heterogeneous weekly series using a dynamic regression that updates continuously, then normalize the output so that it has zero mean and unit standard deviation over the entire history since 1971.

The 105 sub-variables are organized into three families: risk, credit, leverage. The risk sub-index weights money markets (commercial paper spread, repo, Eurodollar and LIBOR before its cessation in June 2023, SOFR since 2018), short-term funding spreads (TED spread, OIS-LIBOR then OIS-SOFR), and volatility measures (VIX, MOVE for bond market volatility computed by Merrill Lynch since 1988, swap spreads). The credit sub-index aggregates bank lending conditions from the Fed’s Senior Loan Officer Opinion Survey (a quarterly survey distributed to roughly 80 domestic banks and 24 foreign bank branches), ICE BofA investment grade and high yield corporate spreads, non-bank corporate financing conditions (financial and non-financial commercial paper, ABCP, structured conduits), and the NACM Credit Manager Index published monthly by the National Association of Credit Management. The leverage sub-index incorporates broker margin debit (Federal Reserve, FINRA since 2010), hedge fund flows (TASS, HFR), intermediary balance sheet composition (NY Fed primary dealer positions in Treasuries, MBS, and corporate bonds), and certain investment bank leverage ratios from quarterly Y-9C call reports. A map of the three sub-indices and their 105 variables is developed in a dedicated article.

The aggregate index calculation is not a simple average of the three sub-indices. The Chicago Fed uses a dynamic factor model (DFM) in which weights vary over time as a function of the instantaneous covariance among series. Technically, the model estimates a single latent factor from the 105 observable series, assuming this common factor explains most of the joint variance of financial conditions. The relative weights of the three sub-indices in the aggregate are therefore a model output, not an input. In practice, during a credit stress episode the credit sub-index receives more than 50% weight in the aggregate because joint variance is dominated by spread movements. During a leverage stress episode (typical of balance sheet crises like 2008 or March 2020) the leverage sub-index becomes dominant. This adaptive weighting is a major methodological feature: it lets the aggregate capture the shifting nature of stress episodes without requiring the analyst to choose a priori which signal to watch.

This methodology has a subtle implication: today’s NFCI does not measure exactly the same thing as the NFCI in 1985 or in 2008. Weights adapt, and the set of 105 variables has evolved over time. Some series have been added (for example ETF flows from the 2000s, post-Dodd-Frank OTC derivatives funding indicators), others have disappeared (LIBOR replaced by SOFR, certain Eurodollar funding series discontinued). The Chicago Fed publishes each year a limited historical revision that backcasts methodological changes across the entire series, so the current series is internally consistent over the full 1971-2026 period.

For concrete intuition on adaptive weights, two extreme documented configurations are worth citing. In October 2008, the leverage sub-index explained roughly 45% of the aggregate’s instantaneous variance, against 30% for risk and 25% for credit — methodological priority shifted to the leverage channel because that is where the largest and fastest moves were happening. In May 2026 by contrast, estimated weights are approximately 50% credit, 30% risk, 20% leverage, with the credit sub-index dominating because it carries most of the current regime’s signature. This weight information is not published directly by the Chicago Fed but can be inferred from statistical decomposition of the three series available on FRED.

A variant exists, the ANFCI (Adjusted NFCI), which removes the portion of financial conditions explained by current economic conditions (GDP, employment, inflation). The ANFCI addresses a legitimate methodological critique: an accommodative NFCI may simply reflect a healthy economy, and conversely a restrictive NFCI may reflect a recession already underway. The ANFCI isolates the financial conditions component not explained by the real cycle, and this is the measure used in some monetary policy rules and by the Fed’s internal stress tests. The full definition and how the NFCI is computed, including the NFCI versus ANFCI distinction, is detailed in a dedicated article.

Publication takes place every Friday morning at 8:30 AM Chicago time, covering the week ending the previous Friday. The lag is minimal: the most recent data incorporated dates from the Tuesday of publication week, so the freshest data is three to four days old. No major revision is applied to past observations in the standard routine; the Chicago Fed however publishes annually a limited historical revision incorporating source series corrections and the possible inclusion of new variables. Data is publicly available on the St. Louis Fed FRED platform under code NFCI (and ANFCI for the adjusted version), with free CSV download and free API access.

Methodologically, NFCI sits in a family of indicators that has evolved substantially since the GFC. Before 2008, the dominant approach to measuring financial conditions used Taylor-rule-style weighted averages of a handful of variables (short rate, long rate, equity returns, dollar). The DFM approach pioneered by Brave and Butters and used by the Chicago Fed produces an indicator that adapts both to the changing nature of stress and to the changing structure of financial markets. Subsequent academic work has explored extensions: time-varying loadings (Aramonte, Lee, and Stebunovs 2015), regime-switching factor models (Hatzius et al. 2010), and machine-learning-based aggregators (more recent literature post-2020). The Chicago Fed has so far retained its 2010 framework with incremental refinements, on the rationale that methodological stability is itself a value for a long-running historical series.

3. Reading NFCI by standard deviation, not by binary threshold

The most common reading error treats NFCI as a binary signal: positive means stress, negative means no stress. This impoverished reading discards the index’s primary information, which is its magnitude in standard deviations. An NFCI of +0.1 and an NFCI of +1.8 both indicate tighter-than-average conditions, but at intensities that are not remotely comparable. Correct interpretation grammar runs through position in the historical distribution.

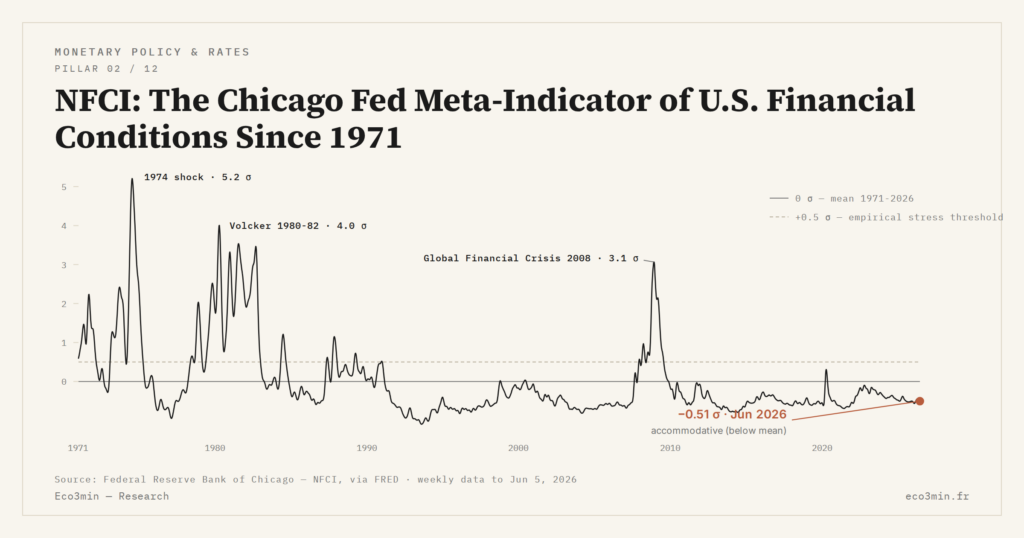

Over the 1971-2026 period, the empirical distribution of weekly NFCI is slightly right-skewed. Restrictive episodes last less long but reach more extreme levels than accommodative episodes. Roughly 16% of the time, the index sits above +0.5; roughly 5% of the time, it exceeds +1.0; readings above +2.0 represent less than 1% of history and correspond to only six episodes (Volcker 1980-1982, briefly the 1987 crash, GFC 2008-2009, briefly COVID March 2020). Symmetrically, roughly 18% of the time the index is below −0.5, and roughly 4% of the time below −0.8. The all-time low is reached in November 2021 at −0.82, in the context of massive post-COVID liquidity and policy rates still at zero. These fractions immediately calibrate what a level means: an NFCI at −0.55 is not exceptional, but it places conditions in the most accommodative quintile of the historical record.

The empirical 0.5 threshold rule — an NFCI sustainably above +0.5 signals financial stress sharp enough to precede a recession — was not declared by the Chicago Fed. It emerged from subsequent studies (Federal Reserve Bank of Chicago Economic Perspectives, several academic works between 2012 and 2018) showing that every NBER-defined U.S. recession since 1971 has been preceded by a sustained move above 0.5, with a median lead time of 6 to 12 months. The threshold is arbitrary in its number — a rule-of-thumb standard deviation — but the underlying mechanism is not: crossing 0.5 standard deviations above the mean signals a financial conditions tightening sharp enough to alter credit and investment behavior. The reading the empirical 0.5 stress threshold is treated in a dedicated article, which details the rule’s false positives (2011, where the index touched 0.6 without a recession following) and false negatives (2022, where the +0.4 peak did not precede an officially declared recession but where a technical recession remains debated).

A less common but analytically richer interpretive key consists of reading NFCI not by absolute value but by coherence or divergence among its three sub-indices. When the three sub-indices (risk, credit, leverage) move in the same direction with comparable magnitudes, the aggregate signal is robust: typically the March 2020 case, where risk, credit, and leverage tighten simultaneously and the aggregate jumps in two weeks from −0.3 to +1.5. When one sub-index diverges durably from the other two, the aggregate masks information: this is the case in May 2026, where the credit sub-index is markedly accommodative (around −0.7) while the risk sub-index is neutral (around −0.1) and the leverage sub-index marginally restrictive (around +0.1). This inter-market coherence reading grid structures the Eco3min editorial position on the index, developed in section 6.

The pace of variation is also informative. A 0.3 increase in NFCI over four weeks is analytically more significant than a 0.3 climb spread over six months. Brave and Butters (2014) show that the index’s variation speed (measured as the four-week first difference) is itself a predictor of imminent stress. This property explains why the most striking episodes in NFCI history (October 2008, March 2020) are characterized as much by the level reached as by the slope of the ascent.

One last statistical property deserves mention: the index has high temporal persistence. The one-week autocorrelation exceeds 0.95, and at 12 weeks it remains around 0.75. This justifies reading NFCI over four- to eight-week windows rather than week by week. An isolated weekly move, even of apparently significant magnitude (say +0.25), may reflect a measurement edge from a source publication rather than a regime break. Conversely, a trend sustained over eight weeks, even of modest magnitude, constitutes a robust signal. This rolling-window reading grammar is not explicitly documented by the Chicago Fed but emerges from the statistical properties of the series, and it is implicitly used by most experienced analysts.

4. 55 years of episodes: what NFCI captured and what it missed

The history of NFCI since 1971 reads as a chronicle of major U.S. financial ruptures. The Volcker period (1980-1982) constitutes the first historical peak: the index reaches +2.3 in July 1982, a level never reached again outside the GFC. The Federal Funds Rate hike to 19% in June 1981, combined with the industrial recession and the nascent Savings and Loans crisis, massively tightens financing conditions. NFCI stays above +1.0 for 47 consecutive weeks, the longest documented stress sequence outside the GFC. Exit from the episode is gradual: the index dips back below zero only at end-1983, eighteen months after the peak.

The 1984-1986 period sees a structurally neutral to mildly accommodative NFCI, despite the rising federal budget deficit and the dollar’s massive appreciation through the September 1985 Plaza Accord. The Savings and Loans crisis crystallizing from 1986 produces a moderate move in the credit sub-index (Thrifts are not in NFCI’s core perimeter as defined in 1971, and their collapse remains geographically and sectorally contained), explaining why the aggregate records no major episode between 1983 and 1987.

The July 1990-March 1991 recession, triggered by the oil shock following the Kuwait invasion and amplified by the S&L crisis peaking in 1989-1990, translates into NFCI as a moderate peak at +0.8 in October 1990. The index falls back below +0.5 by spring 1991, several months before the official NBER recession end. This episode illustrates a recurring property of the index: stress exit regularly precedes recession exit, because financial conditions ease in anticipation of Fed action (rate cuts began in July 1990 and cumulated 175 basis points over the year).

The February-November 1994 bond bear market, triggered by Greenspan’s seven successive Fed Funds hikes (from 3% to 6% in less than a year), produces a very modest move in aggregate NFCI (peak at +0.3) but a meaningful signature in the risk sub-index. The shock is strictly fixed-income and shows no major transmission to credit conditions or intermediary leverage, an illustration that fast rate hikes do not mechanically translate into broad financial conditions tightening, absent stress on bank balance sheets or market intermediary balance sheets. This episode is analytically instructive for understanding 2022 (another fast hiking cycle without full NFCI transmission). A closely related framework: Liquidity and Financial Conditions: Monetary Plumbing, QT Cycles, and Market Impact.

October 19, 1987’s Black Monday produces a +1.1 peak, but brief: three weeks above +0.5 then rapid return to neutral. The Fed (Greenspan in place since August 1987) intervenes immediately through liquidity injections and the famous October 20 communiqué announcing the availability of lending facilities. The episode’s purely equity dimension (no major credit stress, no durable intermediary leverage stress) limits propagation to the rest of the index. The episode is methodologically instructive: it validates NFCI’s capacity to distinguish an intense but narrow equity shock from a systemic crisis.

The 1997 Asian crisis and the September 1998 Long-Term Capital Management collapse produce a double peak reaching +1.2 in October 1998, with a leverage component dominant (the forced liquidation of LTCM’s portfolio crystallizes balance sheet stress on primary dealers). The bailout organized by the New York Fed on September 23, 1998 and the three successive rate cuts between September and November 1998 bring the index back below zero in less than twelve weeks. The cost-benefit ratio of this episode has become a textbook case: 3.6 billion dollars of private capital mobilized by 14 financial institutions averted a systemic unwind that would likely have cost several hundred billion.

The 2001-2002 dot-com crisis peaks more modestly at +0.9 in September 2002: a stretched-out episode of limited financial intensity, because the correction primarily concerns equity valuation and venture financing, two components weakly weighted in NFCI. The March-November 2001 NBER recession was preceded by a move above 0.5 from September 2000, but the index stayed contained below 1.0 throughout, confirmation that the dot-com bust was primarily an equity crisis and only secondarily a broad financial conditions crisis.

The Global Financial Crisis produces the all-time record: +4.2 in October 2008, following Lehman Brothers’ bankruptcy on September 15. The index had begun rising as early as August 2007 with the ABCP market freeze, exceeded +1.0 in September 2007, then +2.0 in March 2008 during the Bear Stearns rescue by JPMorgan organized by the New York Fed. The post-Lehman peak corresponds to total alignment of the three sub-indices: maximum risk stress (financial commercial paper collapse, repo frozen, money market funds breaking the buck), extreme credit stress (IG spreads at 600 bps, HY at 1,800 bps in November 2008), historic leverage stress (primary dealers trying to shrink balance sheets synchronously, creating dislocations on Treasuries and tri-party repo). No other episode has produced such inter-sub-index coherence at such magnitude. GFC exit is slow: the index returns below +0.5 only mid-2009, below zero only in 2010.

The 2010-2012 European sovereign debt crisis has a moderate effect on U.S. NFCI: a +0.6 peak in October 2011, corresponding to the acute phase of the Greek program and tensions on Italy and Spain. Transmission to the U.S. system passes through U.S. money market fund exposure to European financials, picked up notably by the risk sub-index. The absence of U.S. recession following this move above 0.5 constitutes the reference false positive of the empirical rule.

The March 2020 pandemic produces a +1.5 peak, reached in two weeks after March 9. The profile is singular: extremely fast climb, then return below zero in eight weeks thanks to massive Fed interventions (broadened liquidity facilities, Primary Dealer Credit Facility, Money Market Mutual Fund Liquidity Facility, Commercial Paper Funding Facility, Term Asset-Backed Securities Loan Facility, international swap lines restored on March 15, unlimited Treasury and MBS purchases announced on March 23, direct corporate credit support via the Primary and Secondary Market Corporate Credit Facilities). The COVID episode shows NFCI’s capacity to capture a global liquidity shock and record its extinction by central bank intervention, almost in real time. The speed of return to accommodative territory (the index drops below −0.4 by August 2020) is unique in the series’ history. Related explainer: Our walkthrough of swap lines.

The 2022 episode constitutes the index’s most debated test. Facing a cumulative Federal Funds Rate increase of 525 basis points between March 2022 and July 2023, the fastest since Volcker, and an inflation cycle reaching 9.1% in June 2022 (CPI), NFCI only peaked at +0.4 (October 2022), never crossing the empirical 0.5 threshold. This absence of signal triggered substantial analytical debate: has the index become insensitive to the current monetary regime, or is Fed-to-financial-conditions transmission structurally weaker than in the last century? A complete chronology of the stress episodes from 1971 to 2026, with peak levels and pre-recession lead time, is developed in a dedicated article.

5. The current regime: accommodative compression despite QT

May 2026: weekly NFCI prints around −0.55 over the past eight weeks, placing financial conditions in the most accommodative quintile of the historical record. This compression is analytically surprising given the monetary configuration in place. The Federal Funds Rate peaked at 5.25-5.50% between July 2023 and September 2024, before a cutting cycle cumulating 150 basis points between September 2024 and May 2026, bringing the rate to the current 3.75-4.00% range. In parallel, the Fed balance sheet measured by WALCL has shrunk by roughly 2.2 trillion dollars from its April 2022 peak of 8.97 trillion, consequence of quantitative tightening engaged in June 2022 (initial cap of 47.5 billion per month, raised to 95 billion in September 2022) and slowed in May 2024 (cap reduced to 60 billion then 40 billion from April 2025). The series: Our Fed balance-sheet record.

The traditional monetary transmission logic, observed historically over 1971-2010, would lead to expect NFCI close to zero or in mildly restrictive territory in this configuration. The index does the opposite: it has fallen continuously from the October 2022 peak, crossing the neutral zone late 2023 and settling in accommodative territory from mid-2024. The divergence between monetary policy and the aggregate index poses a structural question that has occupied macro strategist notes for eighteen months.

Three competing readings circulate in strategist notes and recent academic publications. The first reading is one of internal decomposition: the aggregate NFCI masks a specific compression of the credit sub-index (investment grade spreads at 85 bps in May 2026 against a 2010-2024 average of 130 bps, high yield at 280 bps against a 2010-2024 average of 450 bps, bank lending conditions less restrictive than the late-2022 SLOOS suggested), while the risk sub-index is neutral and the leverage sub-index marginally restrictive. The aggregate result is pulled by the credit component, which dominates through adaptive weighting in a context of a late-cycle economy without imminent rupture.

The second reading is structural: the post-2020 regime has modified monetary transmission itself. The ample reserves system installed since 2008 and confirmed since 2020, combined with the post-Dodd-Frank robustness of bank balance sheets, has structurally reduced the pass-through from policy rates to effective financial conditions. Corporations and households having locked in a significant portion of their financing at fixed rates during 2020-2021 (the U.S. average outstanding 30-year mortgage rate stayed around 3.8% through mid-2024 despite a marginal rate at 7%) are less sensitive to short rate hikes. The share of S&P 500 companies with average debt cost below 4% remains around 60% in 2026 according to S&P Capital IQ data, against less than 30% before 2020. In this framework, the accommodative NFCI is not an anomaly but the reflection of a structurally different regime where monetary transmission operates with reduced lag and amplitude.

The lock-in mechanism deserves quantification. According to Freddie Mac data, the average rate on outstanding U.S. residential mortgages (the effective rate paid by households, not the marginal rate available on new loans) was 3.99% in mid-2024 and 4.21% in early 2026, against a market 30-year rate that has fluctuated between 6.5% and 7.9% over the same period. This 250 to 350 basis point gap between average and marginal rates is unprecedented in U.S. mortgage history. On the corporate side, the average maturity of S&P 500 debt outstanding lengthened from 7.8 years pre-2020 to 10.2 years end-2025 (S&P Global data), reflecting the historic 2020-2021 wave of long-duration issuance at near-zero rates. These two structural features together imply that the marginal financing rate increase signaled by the Fed Funds Rate transmits to the average effective rate paid by the private sector only with a multi-year lag — a property that did not characterize previous tightening cycles.

The third reading is cyclical but pessimistic: the compression is analogous to 2006-2007, when NFCI settled around −0.4 to −0.6 despite a Fed hiking cycle complete since June 2006. Passage into strongly restrictive territory occurred only from August 2007 with the ABCP market freeze, 14 months after the end of the hiking cycle. This reading frames the current compression as dangerous complacency that will not survive the first systemic shock. Defenders of this reading point to the extreme compression of HY spreads (below 300 bps despite a structurally higher default environment), the strength of leveraged loan and private credit issuance (record 2024-2025 cumulative volumes), and the historic weakness of implied equity risk premium. The accommodative compression of 2024-2026 and the three competing readings are the subject of a specific article that lays out the debate without adjudicating it. In depth: the macro-analysis tools hub.

None of the three readings is falsifiable in the short term. The decomposition reading is validated by the data but does not explain why the credit sub-index is compressed. The structural reading is consistent with lock-in observation but will be testable only in case of a major shock to the system. The pessimistic reading draws the 2006-2007 analogy but the analogy is partial: credit market structure, banking regulation, and the Fed’s mandate have substantially changed since 2008.

Beyond credit spreads, several micro market functioning indicators confirm the accommodative reading. Bid-ask spreads on 10-year Treasuries are at levels comparable to 2019 (around 0.5 cent per 100 dollars of face value on average over 2025), suggesting normal market liquidity. The SOFR-OIS spread, a measure of very short-term funding stress, oscillates around 1 to 3 basis points since late 2024, against a historical average of 5 to 8 basis points. Repo stress indicators (notably the spread between general collateral rate and OBFR) are also compressed. Conversely, some intermediary leverage indicators are beginning to show marginal tensions: primary dealer positioning growth in corporate credit has slowed since Q4 2025, and hedge fund long-short positions on cash-versus-future Treasuries reached in early 2026 levels comparable to March 2020, which the New York Fed explicitly flagged in its February 2026 Liberty Street Economics post.

Reading NFCI as a binary signal — positive means crisis, negative means no risk — discards the index’s primary information, which is its magnitude in standard deviations. An NFCI at −0.55 does not say that everything is fine; it says conditions are more accommodative than the 1971-2026 mean in a sample that includes Volcker and the GFC. The useful question is not the index’s sign but its position in the historical distribution and the coherence among its three sub-indices.

6. Eco3min position: NFCI as a measure of inter-market coherence

NFCI is treated in most market notes as a unified gauge of financial conditions, read at its aggregate value. The Eco3min angle shifts one notch: NFCI is useful primarily as a measure of coherence or divergence among the three sub-indices, and only secondarily through its aggregate value. This position is not an editorial eccentricity; it is consistent with the adaptive weighting methodology documented by the Chicago Fed itself.

When the three sub-indices move together (typical of major shocks: 1987, 2008, March 2020), the aggregate is the useful information and the signal is robust. In these configurations, the aggregate value summarizes without distorting the stress structure. When one or two sub-indices diverge durably (the 2022 case where risk tightens but credit stays neutral; the May 2026 case where credit is accommodative while leverage is marginally restrictive), the aggregate value masks primary information. In these configurations, reading the composite alone amounts to losing signal structure and reproducing the binary reading error critiqued above.

This inter-market coherence reading grid produces two practical consequences for macro-financial analysis. First, it invites systematically publishing the three-sub-index decomposition alongside the aggregate — which the Chicago Fed does but which market commentary rarely picks up. The weekly data published on FRED contains the three series (NFCIRISK, NFCICREDIT, NFCILEVERAGE) freely accessible and usable to visually reconstruct divergence or convergence. Second, it suggests that the most analytically instructive episodes are not the index’s absolute peaks (where everything converges) but the periods of sustained divergence (where aggregate NFCI is silent but internal structure tells a story). The 2006-2007 and 2024-2026 phases share this characteristic of durable divergence, which warrants attention even when the composite index sends no stress signal.

This editorial stance carries an analytical cost: it complicates the communication work on the index. It is easier to write “NFCI at −0.55, accommodative conditions” than to write “the aggregate NFCI is accommodative but its internal coherence is weak, with credit markedly compressed against marginally restrictive leverage, which makes the index less informative than usual”. The first words pass through a wire; the second do not. The Eco3min bet is that a fraction of readers (macro analysts, risk managers, specialist journalists) find more value in the second formulation, and that this fraction justifies the additional editorial effort.

Operationalizing this inter-market coherence reading does not require sophisticated technical tools. A simple procedure consists of publishing weekly, alongside aggregate NFCI, two derived indicators: the instantaneous standard deviation across the three sub-indices (a divergence measure) and the sign of each of the three sub-indices taken separately. When the three-sub-index standard deviation is below 0.15, all three move in concert and the aggregate suffices; when this standard deviation exceeds 0.30, the aggregate masks heterogeneous internal structure and decomposition becomes the primary information. Over March-May 2026, this standard deviation oscillates around 0.42, a level that places the composite index in a zone of reduced informativeness.

A second implication concerns empirical thresholds. The 0.5 threshold on the aggregate is itself conditional: it was calibrated on episodes where the three sub-indices converged. When the aggregate is pulled primarily by a single sub-index, the 0.5 threshold loses part of its predictive value. This property partially explains the 2022 false negative (the aggregate did not cross 0.5 because inter-sub-index divergence dampened the composite signal). The use of empirical thresholds therefore benefits from conditioning on internal coherence — a point that does not appear in the standard literature on NFCI but that structures the Eco3min reading.

The aggregate NFCI hides as much as it reveals; durable divergence among its three sub-indices is more informative than its composite value.

- NFCI is published weekly by the Chicago Fed since January 1971 and aggregates 105 financial variables through an adaptive-weights regression.

- Its correct reading runs through standard-deviation magnitude, not sign: NFCI at −0.55 places conditions in the most accommodative quintile over 55 years.

- The empirical 0.5 threshold rule preceded every NBER-defined U.S. recession since 1971 with a 6 to 12 months lead time, but failed in 2022 (false negative).

- The May 2026 regime shows accommodative compression (−0.55) despite a Federal Funds Rate at 3.75-4.00% and cumulative QT of 2.2 trillion; three competing readings coexist (internal decomposition, structurally weaker transmission, 2006-2007 analogy).

- The richest analytical angle reads NFCI through inter-sub-index coherence (risk, credit, leverage) rather than through its aggregate value alone.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…

Inverted Yield Curve: Reading a Regime Signal Without Immediate Effect

The inverted yield curve operates as a regime signal, not a timing tool. Its lagged effects are constitutive…