NFCI Explained: Meaning, Calculation, and Analytical Reading

Before debating empirical thresholds or the current regime, the NFCI must be defined precisely and its construction mechanics laid bare. Three methodological properties structure any rigorous reading of the index.

TL;DR

Each weekly NFCI value comes from a single-factor model re-estimated monthly over 105 series, normalized so zero marks the 1971-2026 average and one unit equals one standard deviation.

- When the Chicago Fed adds or drops a series, it propagates the change backward, so a January 1980 reading is computed in the same framework as a May 2026 one, keeping decade-long comparisons clean.

- Beyond the level, the four-week change matters: a 0.3 rise over four weeks signals more than the same move spread over six months, with weekly autocorrelation above 0.95 favoring four-to-eight-week windows.

The Chicago Fed has published the index since 1971 following a methodology codified in 2010 and updated in 2014. This article isolates definition and computation, deferring thresholds and decomposition.

1. What NFCI measures: operational definition

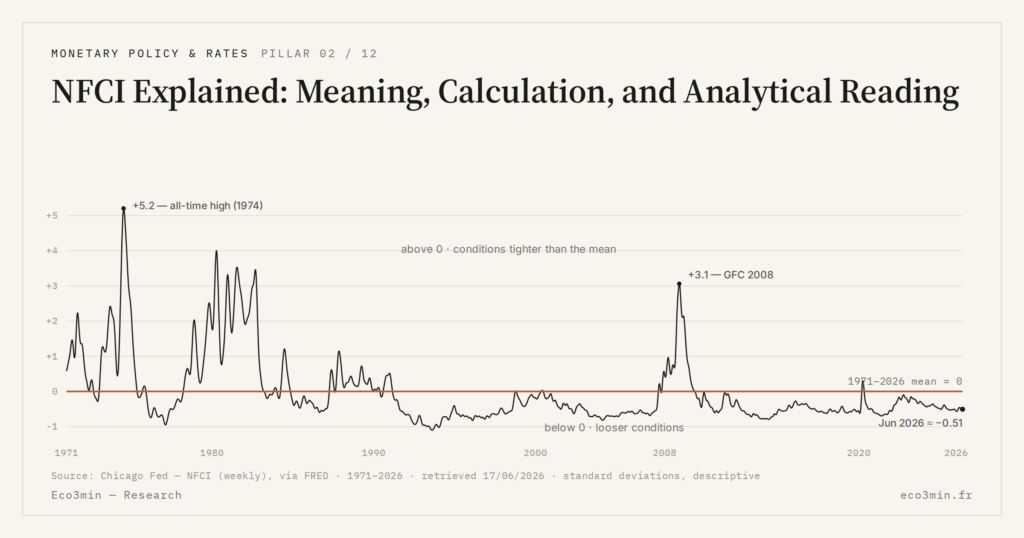

NFCI measures the position of U.S. financial conditions at a given moment relative to their historical mean since 1971. See our NFCI data for the underlying data. It is a cyclical position indicator, not an absolute level indicator. The raw datum is a weekly value expressed in standard deviations around a mean fixed at zero with unit standard deviation, published every Friday at 8:30 AM Chicago time by the Federal Reserve Bank of Chicago.

The term financial conditions covers a broad perimeter: the costs and availability of financing across all observable channels — money markets, commercial bank credit, market-based corporate credit, wholesale funding, market intermediary balance sheets. NFCI aggregates 105 weekly series spanning these channels. A score at zero indicates conditions exactly in line with the 1971-2026 mean. A positive score indicates conditions tighter than the mean (financing more expensive or harder to obtain). A negative score indicates conditions more accommodative than the mean.

The score’s magnitude, expressed in standard deviations, gives severity. NFCI at +0.5 indicates conditions meaningfully tighter than the mean — this is the empirical threshold above which the index has historically preceded every NBER-defined U.S. recession. NFCI at +2.0 indicates major historical stress, a level reached only six times since 1971 (Volcker 1980-1982, October 1987 briefly, GFC 2008-2009, March 2020 briefly). Conversely, NFCI at −0.5 or −0.8 indicates accommodative compression, a level reached in November 2021 (−0.82 historical record) or in May 2026 (−0.55).

NFCI fits within the broader framework of financial conditions in macro-finance, which constitute a primary transmission belt between Fed monetary policy and the real economy. This is why NFCI as a meta-indicator of financial conditions has structured much of U.S. macro-financial analysis for twenty-five years.

2. How the Chicago Fed computes it technically

The construction methodology is documented in Chicago Fed Working Paper 2010-02 (Brave and Butters, “Diagnosing the Financial System: Financial Conditions and the Financial Crisis”), with a 2014 technical update published in the Chicago Fed’s Economic Perspectives journal. The core principle: extract a weighted common factor from 105 heterogeneous weekly series via a Dynamic Factor Model (DFM).

The DFM assumes that a single latent factor (financial conditions) explains most of the joint variance observed in the 105 series. The relative weight of each series is estimated by maximum likelihood and varies over time as a function of the instantaneous covariance among series. This adaptive weighting property is central: it lets the aggregate automatically pick up credit stress episodes (where spreads dominate), leverage stress episodes (where intermediary flows dominate), or mixed episodes, without requiring the analyst to choose a priori which signal to watch.

Concretely, the model estimated by the Chicago Fed is a single-factor DFM with AR(1) dynamics on the latent factor and idiosyncratic error structure by series. Estimation frequency is monthly (the model is re-estimated each month including the most recent observations), but the resulting weights are applied weekly to the index update. The main sources of time variation in weights come from both instantaneous covariance among series (adaptive weighting effect) and from the progressive extension of the variable set (coverage effect). The methodology is publicly documented, which allows external researchers to replicate the index and audit its statistical properties over the full historical series. The sub-index decomposition details how these weights translate into the three families risk, credit, and leverage.

The extraction output is normalized to have zero mean and unit standard deviation over the entire history since 1971. Normalization is computed on the complete series and each new release marginally recalibrates parameters — this property means that the value attributed to a given week may very slightly move when new observations are added to the history, but the magnitude of these adjustments is small (typically below 0.02 standard deviations on observations more than five years old).

A variant of the index, the ANFCI (Adjusted NFCI), removes the portion of financial conditions explained by current economic conditions (GDP, employment, inflation). The ANFCI addresses a legitimate methodological critique: an accommodative NFCI may simply reflect underlying healthy economic conditions, and conversely a restrictive NFCI may reflect a recession already underway. The ANFCI isolates the financial conditions component not explained by the real cycle — this is the measure used in some monetary policy rules and by the Fed’s internal stress tests. Standard NFCI remains the reference indicator for analytical reading of cyclical position, with ANFCI serving as a complement when the analyst wants to isolate the purely financial component. Also relevant: the structuring role of market liquidity.

Data is released every Friday morning at 8:30 AM Chicago time (2:30 PM Paris time during European summer time), covers the week ending the previous Friday, and is publicly available on the St. Louis Fed FRED platform under codes NFCI and ANFCI. Free CSV download, free API, complete archives since January 1971.

One additional methodological point deserves emphasis: the NFCI series is internally consistent over the full historical period. When the Chicago Fed adds new variables or removes discontinued ones, the historical revision propagates the change backward so that an observation from January 1980 is computed with the same methodological framework as an observation from May 2026. This property is not trivial — most financial conditions indices published by private institutions break methodologically every few years, making long-run comparisons noisy. The NFCI’s commitment to backward-consistent revisions is one reason it remains the canonical reference for cyclical position analysis over multiple decades, despite its relative complexity compared to simpler weighted-average approaches.

3. Reading a positive or negative score without falling into binary interpretation

The most common reading error treats NFCI as a binary signal: positive means stress, negative means no stress. This grammar discards the index’s primary information, which is its magnitude in standard deviations. NFCI at +0.1 and NFCI at +1.8 both indicate conditions tighter than the mean, but at analytically incomparable intensities.

Correct interpretation runs through position in the historical distribution. Over 55 years of data, roughly 16% of the time NFCI sits above +0.5 and roughly 18% of the time below −0.5. Readings above +1.0 represent 5% of history. Readings above +2.0 represent less than 1%. Symmetrically, levels below −0.8 represent 4% of history. These fractions immediately calibrate what a level means: a score at −0.55 is not exceptional but it places conditions in the most accommodative quintile; a score at +0.5 enters the upper restrictive quintile.

Beyond magnitude, temporal dynamics matter. NFCI moves slowly by construction (weekly autocorrelation above 0.95), which justifies reading the index by rolling windows of four to eight weeks rather than week by week. A 0.3 rise over four weeks is analytically more significant than a 0.3 climb spread over six months. This persistence property explains why an isolated weekly move, even apparently significant, may reflect a measurement edge from a source publication rather than a regime break.

A complementary reading lens consists of separating the index value into level and trend components. A high level with a flat trend (NFCI stabilized at +0.8 for several weeks) signals an entrenched tight regime; a moderate level with a sharply rising trend (NFCI at +0.3 climbing 0.15 per week) may be more informative about imminent stress than a higher static level. Brave and Butters (2014) document this property explicitly, showing that the four-week first difference of the index is itself a useful signal independent of the level. This dual reading by level and trend constitutes a more analytically robust framework than the single binary comparison to the 0.5 threshold.

The empirical 0.5 threshold rule, which circulates widely in market notes, deserves precise analytical reading — origin, mechanism, documented empirical limits — addressed separately in the article dedicated to the empirical reading of the 0.5 threshold.

4. What this article does not address

Three topics fall to dedicated articles. The fine decomposition of the 105 sub-variables into three sub-indices (risk, credit, leverage) and the inter-sub-index coherence reading are not developed here. The analytical interpretation of the empirical 0.5 threshold, its academic origin, and its documented limits (false positives and false negatives since 1971) are treated in a specific article. The confrontation of NFCI with other U.S. financial stress indicators (VIX, HY OAS, STLFSI) is mapped separately.

The present article deliberately isolates pure definition and computation mechanics, because these two elements are prerequisites for any subsequent rigorous reading and they deserve systematic treatment without interference from interpretive debates.

- NFCI measures the position of U.S. financial conditions relative to their historical mean since January 1971, in standard deviations.

- The methodology relies on a Dynamic Factor Model that extracts a latent factor from 105 weekly series with adaptive weights — Brave and Butters 2010, 2014 update.

- A positive score indicates conditions tighter than the mean; a negative score indicates more accommodative conditions; magnitude conveys severity.

- ANFCI is a variant isolating the financial conditions component not explained by the real economic cycle; it complements rather than replaces standard NFCI.

- Any rigorous reading runs through position in the historical distribution and four- to eight-week rolling windows, not through sign alone.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…