NFCI Compressed in 2024-2026: Post-GFC Anomaly or New Regime?

May 2026: NFCI at −0.55, a compression rarely observed after a monetary tightening phase. Fed-to-financial-conditions transmission appears to operate differently than in previous cycles.

TL;DR

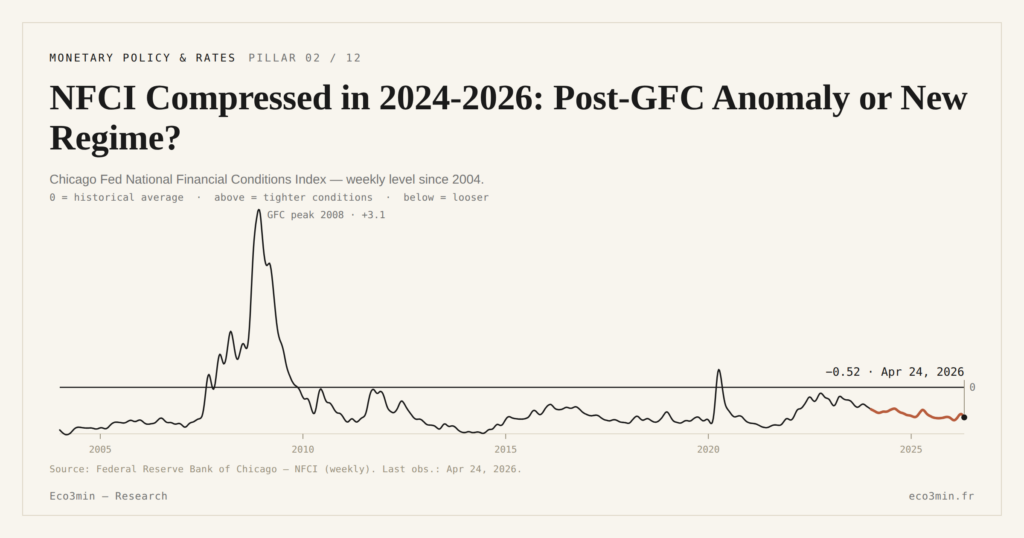

Two years into a rate-cutting cycle, with QT still running, the NFCI reads -0.55 in May 2026; three competing readings explain why financial conditions sit this loose, none falsifiable yet.

- Internal decomposition: the credit sub-index near -0.7 pulls the aggregate through the Chicago Fed's adaptive weighting (estimated ~50% weight), with IG spreads at 85 bps and HY at 280 bps versus 2010-2024 averages of 130 and 450.

- Weakened transmission: fixed-rate lock-in from 2020-2021 (outstanding 30-year mortgages near 3.8% against 6.5-7.9% marginal) and G-SIB CET1 ratios above 13% blunt the pass-through of policy tightening.

- Cyclical analogy: 2006-2007, when the NFCI held -0.4 to -0.6 for fourteen months before reaching +4.2, read as late-cycle complacency, though private credit now sits at 2.4 trillion against near zero then.

Three competing readings circulate in strategist notes and recent academic literature. This article lays out the three without adjudicating.

1. The observation: compression sustained despite ZIRP end and QT

May 2026, weekly NFCI measurement: −0.55. The level has settled around this value over the past eight weeks, after a slow drift from the October 2022 peak at +0.4. Crossing the neutral zone occurred late 2023; settlement in accommodative territory dates from mid-2024.

The monetary configuration in place makes this compression analytically surprising. The Federal Funds Rate peaks at 5.25-5.50% between July 2023 and September 2024 — a range held for 14 months. The cutting cycle that follows cumulates 150 basis points between September 2024 and May 2026, bringing the rate to the current 3.75-4.00% range. In parallel, the Fed balance sheet measured by WALCL has shrunk by roughly 2.2 trillion dollars from its April 2022 peak of 8.97 trillion, consequence of quantitative tightening engaged in June 2022 (initial cap 47.5 billion per month, raised to 95 billion in September 2022, slowed to 60 billion in May 2024, then 40 billion since April 2025).

Traditional monetary transmission logic, as observed over 1971-2010, would lead to expect NFCI near zero or weakly restrictive in this configuration. Over the same historical period, after a hiking cycle peak of roughly +500 bps in two years, the index typically stays above +0.3 for 18 to 24 months. The index does the opposite: it has fallen continuously and settled in markedly negative territory. This divergence between monetary policy and the aggregate index is the object of the ongoing analytical debate, and cannot be addressed without the reading of NFCI definition and analytical reading developed in the cluster MAJEUR.

2. Reading 1: internal decomposition — credit pulls the aggregate

The first reading, most mechanical, examines what is happening inside the aggregate via the sub-index decomposition. The finding is sharp: the credit sub-index (NFCICREDIT) is at roughly −0.7 in May 2026, a historically tight compression level. The risk sub-index (NFCIRISK) is at roughly −0.1, near neutrality. The leverage sub-index (NFCILEVERAGE) is at roughly +0.1, marginally restrictive. The aggregate result is pulled by the credit component.

This credit sub-index compression reflects several measurable empirical facts. ICE BofA US Investment Grade Master OAS spreads are at 85 basis points in May 2026, against a 2010-2024 average of 130 bps. HY OAS is at 280 bps against a 2010-2024 average of 450 bps. Bank lending conditions measured by the Senior Loan Officer Opinion Survey are markedly less restrictive than the late-2022 SLOOS (net tightening from 45% of banks) suggested: the latest quarterly survey indicates a net easing of 3% on average on large enterprise loans, a return to normal post-COVID conditions.

The DFM adaptive weighting mechanism used by the Chicago Fed amplifies the effect. In a late-cycle context without imminent rupture, instantaneous covariance among credit series dominates the variance-covariance matrix, and the credit sub-index receives an estimated weight around 50% in the aggregate. Mechanically, credit at −0.7 with a 50% weight pulls the aggregate negative, only partially offset by the other sub-indices near zero.

This reading is descriptive: it explains the how without explaining the why. It validates that aggregate NFCI is consistent with its components, but says nothing about why the credit sub-index is itself compressed. It is a first-level reading, which sets up the second and third readings.

3. Reading 2: structurally weakened transmission — the lock-in effect

The second reading postulates that the post-2020 regime has modified monetary transmission itself, and that accommodative NFCI reflects this structural change rather than a cyclical anomaly. Two main mechanisms are mobilized.

First mechanism: lock-in of fixed-rate financing during 2020-2021. The U.S. average outstanding 30-year mortgage rate stayed around 3.8% through mid-2024 according to Freddie Mac data, while the marginal rate on new loans oscillated between 6.5% and 7.9% over the same period. This 250 to 350 basis point gap between average effective and marginal rate of residential financing is unprecedented in U.S. mortgage history. On the corporate side, the average maturity of S&P 500 outstanding debt rose from 7.8 years pre-2020 to 10.2 years end-2025 according to S&P Global, reflecting the historic 2020-2021 wave of long-duration issuance at near-zero rates. The share of S&P 500 companies whose average debt cost remains below 4% is around 60% in 2026 according to S&P Capital IQ, against less than 30% before 2020. These two structural features together imply that the marginal rate increase signaled by the Fed transmits to the average effective rate paid by the private sector with a multi-year lag.

Second mechanism: the ample reserves system installed since 2008 and confirmed since 2020, combined with the post-Dodd-Frank robustness of bank balance sheets. Common equity tier 1 capital ratios of large U.S. banks (G-SIBs) exceed 13% in 2026, against a regulatory requirement around 11% and pre-GFC levels of 6-7%. Eco3min’s analysis of the 2008 crisis traces this episode. This balance sheet robustness limits transmission of policy rate tightening to bank lending conditions — banks can absorb moderate tightening without passing it on to borrowers.

In this framework, accommodative NFCI is not an anomaly but the reflection of a structurally different regime where monetary transmission operates with reduced lag and amplitude. The structural reading is consistent with empirical lock-in and bank robustness observation, but stays partially non-testable: it will only be verifiable in case of a major shock to the system that would reveal the real elasticity of transmission. This reading fits within financial conditions as monetary transmission across cycle, whose very nature is in post-2020 mutation.

4. Reading 3: the 2006-2007 analogy — dangerous late-cycle complacency

The third reading is cyclical and pessimistic: current compression is analogous to 2006-2007, when NFCI settled around −0.4 to −0.6 despite a Fed hiking cycle complete since June 2006. This analogy frames May 2026 compression as dangerous complacency that will not survive the first systemic shock.

The chronological reminder of 2006-2007 is instructive. The 2004-2006 hiking cycle cumulated 425 basis points (from 1.00% to 5.25%), concluded in June 2006. NFCI settled around −0.4 to −0.6 between July 2006 and July 2007 — a phase of apparent accommodative normality. On August 9, 2007, BNP Paribas suspended three money market funds with subprime exposure; the ABCP market froze within weeks. NFCI crossed zero in late August 2007, +0.5 in September 2007, and would reach +4.2 fourteen months later. The transition from accommodative regime to systemic crisis took 14 months — a window during which the composite index sent no signal of imminent rupture.

Defenders of this reading for 2024-2026 point to several parallels. The extreme compression of HY spreads (280 bps in May 2026 against 500 bps historical average) despite a structurally higher default environment than 2006 (U.S. HY default rate 2020-2025 average of 3.8% against 2.4% in 2003-2006). The vigor of leveraged loan and private credit issuance, with cumulative 2024-2025 volume reaching an all-time record of 1.8 trillion (Pitchbook LCD), suggestive of a credit risk demand reminiscent of 2006-2007. The historic weakness of implied equity risk premium, measured by the inverse of the Shiller-adjusted PER, at roughly 2.8% in May 2026 against a 1970-2024 average of 4.3%.

The pessimistic reading nonetheless has its limits. The 2006-2007 analogy is partial: credit market structure has substantially changed (private credit outside the banking perimeter now represents 2.4 trillion against virtually nothing in 2006), banking regulation is significantly tighter (Dodd-Frank, Basel III), the Fed’s mandate now explicitly includes financial stability, and Treasury market depth is sufficiently maintained by SRF and FIMA facilities to limit risks of systemic dislocation seen in March 2020. A rigorous historical comparison refers to the major financial ruptures documented since 1971, which show that each cyclical analogy has its limits.

5. The three readings are not falsifiable in the short term

None of the three readings is falsifiable in the immediate horizon. The decomposition reading (reading 1) is validated by the data but does not explain why the credit sub-index is compressed — it is descriptive without being explanatory. The structural reading (reading 2) is consistent with the lock-in observation but will only be testable in case of a major shock revealing the real elasticity of monetary transmission. The pessimistic reading (reading 3) draws the 2006-2007 analogy but the analogy is partial and market conditions have materially changed.

The absence of immediate falsifiability is not an analytical defect: it is inherent to the nature of late-cycle phases. The test will come from the next quarters. Three indicators deserve surveillance in this perspective. First, the NFCI inter-sub-index dispersion: if it narrows (the three sub-indices converge toward a common value), the aggregate signal becomes readable again and reading 1 loses relevance. If it stays elevated, the aggregate continues to mask internal structure and the other readings retain value. A sub-index reading grid remains indispensable for tracking this dispersion. The underlying weekly data needed to monitor the three sub-indices is freely available via the live FRED NFCI weekly data.

Second, the evolution of the leverage sub-index: it is at +0.1 in May 2026 after having been markedly negative in 2024. A gradual rise above +0.3 over 12 rolling weeks would be consistent with a late-cycle scenario following the 2006-2007 pattern (the leverage sub-index began to tighten from mid-2007, several months before the aggregate rupture). Third, market functioning indicators (Treasury bid-ask, SOFR-OIS spread, primary dealer positioning): their gradual degradation would constitute an early warning signal, independent of aggregate NFCI.

The Eco3min analysis does not adjudicate among the three readings because adjudication would not be analysis but forecasting. The editorial position consists in laying out the three readings with their respective implications, signaling the surveillance indicators that will discriminate among them as quarters pass, and letting the reader form their own informed judgment.

- NFCI May 2026 at −0.55, an accommodative compression level installed since mid-2024 despite Federal Funds Rate at 3.75-4.00% and cumulative QT of 2.2 trillion.

- Reading 1 (internal decomposition): credit sub-index at −0.7 pulls the aggregate via adaptive weighting; descriptive without being explanatory.

- Reading 2 (structurally weakened transmission): lock-in effect of 2020-2021 fixed-rate financing and post-Dodd-Frank bank robustness; non-testable absent shock.

- Reading 3 (2006-2007 analogy): dangerous late-cycle complacency; analogy partial, market conditions materially different.

- Surveillance indicators to discriminate: inter-sub-index dispersion, leverage sub-index drift, market functioning indicators (Treasury bid-ask, SOFR-OIS, dealer positioning).

Last updated — 20 June 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…