Nominal vs Real Rates: Why the Distinction Matters

When nominal rates stabilize, real rates can keep rising if inflation slows more slowly. This distinction conditions the actual degree of monetary restriction and often explains the gap between central bank discourse and economic reality.

When rates appear to stabilize or recede, the real cost of capital can still continue to rise. The distinction between nominal and real rates remains one of the major blind spots in reading monetary policy and its effects on the economy.

TL;DR

When inflation recedes more slowly than policy rates, the real cost of capital can keep climbing even as posted rates look stable, a tightening that headline numbers hide.

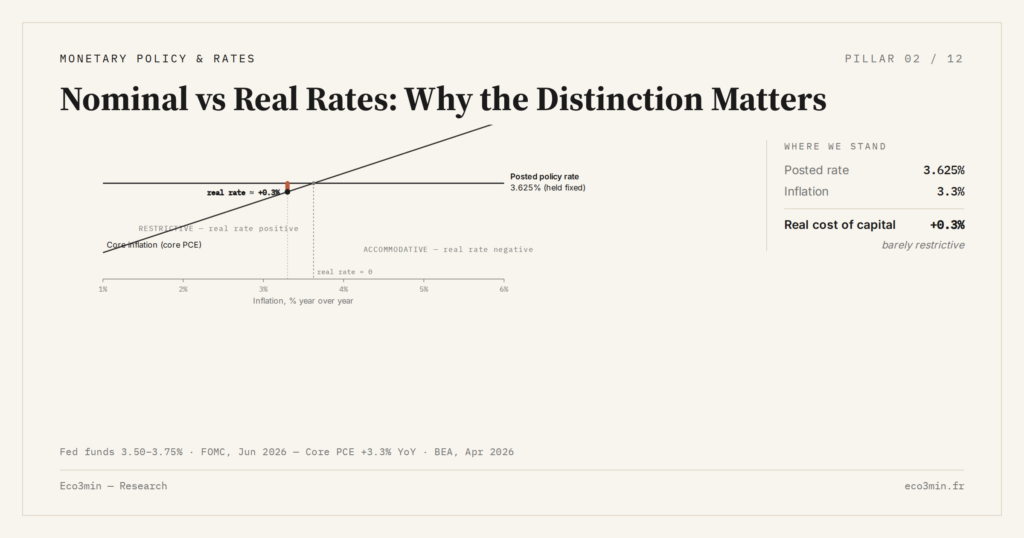

- In late 2025 nominal rates stabilised while core inflation held near ≈3% in several advanced economies, leaving the ex post real rate slightly positive and higher than a year earlier.

- Capital-intensive and long-cycle sectors such as real estate and infrastructure feel rising real rates first, through longer profitability thresholds and deferred projects, even with no further nominal hikes.

The mechanism is discreet but central. Central banks steer nominal rates, while the real economy responds to inflation-adjusted rates. As long as inflation moves faster than policy rates, the perceived monetary impulse can differ radically from the stated intent.

This gap fits within the broader monetary transmission framework detailed in our reference analysis on how monetary policy operates and its effects on the real economy. The angle here is deliberately narrower: understanding why reading rates in nominal terms can become misleading when inflation slows without disappearing.

The friction point between monetary decisions and real economic cost

This distinction between nominal and real rates fits within the broader framework of monetary policy and interest rates, whose impact on the economy cannot be assessed solely from announced decisions but from the financial conditions actually transmitted to economic agents.

A 4% policy rate does not carry the same meaning whether inflation is at 2%, 3% or 5%. In late 2025, in several advanced economies, nominal rates stabilized while core inflation remained around ≈3%. The ex post real rate thus stayed slightly positive, even rising relative to the prior year.

For corporates, this differential translates into a more constraining cost of capital than official communication suggests. For households, credit remains expensive in real terms, even when posted rates stop rising.

Dominant consensus and analytical blind spot

This perception gap is all the more pronounced when one considers the difference between policy rates, market rates and real rates, which explains why a seemingly stable monetary environment can continue to produce restrictive effects in the real economy.

The central scenario adopted by many market participants still relies heavily on nominal rates as the primary indicator of monetary restriction. This reading explains why markets can rise despite an inverted yield curve, once participants price in a forthcoming normalization. Stabilization, or even the anticipation of cuts, is often interpreted as a signal that financial conditions are easing.

Our analysis diverges on this specific point. As long as inflation does not return durably to target, monetary policy can remain restrictive in real terms, even without further policy rate hikes. The issue is not the movement of nominal rates, but their relative position against price dynamics. A related read: the Eco3min study of the way tighter policy reaches the income statement.

Why the distinction matters more now

After the 2022–2023 inflation peak, the disinflation observed in 2024–2025 shifted the dominant reading. In early 2026, several indicators show stickier inflation in services and wages, while policy rates have reached a plateau. This configuration mechanically raises real rates, without any further explicit decision.

This drift is rarely perceived as tightening, although it produces some of its effects: stricter investment trade-offs, increased pressure on leveraged balance sheets, slowing of long-horizon projects.

Differentiated impacts across economic agents

For capital-intensive businesses, rising real rates lengthen profitability thresholds and delay certain investments. Long-cycle sectors such as real estate and infrastructure are particularly sensitive to this parameter.

For households, the effect is more diffuse but persistent. Even without further nominal hikes, the purchasing power of credit remains constrained if nominal incomes do not grow faster than inflation.

In financial markets, this distinction explains certain apparent disconnects: valuations that fail to ease despite stable nominal rates, or flows that remain cautious despite less aggressive monetary rhetoric.

What readers are really looking for

Behind the question of nominal versus real rates lies a simpler concern: is monetary policy genuinely easing, or only slowing the pace of tightening? The real question is not the next stated decision, but the level of economic constraint actually felt.

Concrete indicators for tracking real constraint

- Ex post real rate: difference between policy rates and observed 12-month inflation.

- Implicit real rate on credit: applied rates minus inflation expectations of agents.

- Evolution of productive investment: leading signal of how the cost of capital is perceived.

What could invalidate this reading

This analysis rests on the assumption of inflation durably above targets without further acceleration. A more pronounced slowdown in inflation, or a rapid drop in price expectations, would mechanically reduce real rates without further action. Conversely, an exogenous inflation shock would make real constraint even tighter at unchanged nominal policy.

Reading perspective

The distinction between nominal and real rates is not a theoretical refinement. It conditions the understanding of the actual degree of monetary restriction and explains why some decisions appear ineffective or excessive depending on the period. It is not always the central scenario put forward, but it is often where the gap between monetary discourse and economic reality lies.

What this mechanism really reveals

- A stabilization of nominal rates can mask real tightening if inflation slows more slowly.

- The cost of capital relevant to the economy is the real rate, not the posted rate.

- A large share of current economic adjustments reflects this differential more than visible decisions.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…