Public Debt Sustainability: Why Real Rates Are the Key

Sovereign debt sustainability rests on the gap between real rates and growth, not on the debt-to-GDP level. The shift from a deeply negative r – g gap to a near-zero gap restores a fiscal constraint that had been dormant for a decade.

The burden of sovereign debt is not measured by the headline nominal rate, but by the gap between the real rate paid and the real growth of the economy. This differential governs the trajectory of the debt-to-GDP ratio.

TL;DR

France's public debt near 112% of GDP carries a 2026 interest bill above €55 billion; its trajectory is set by the differential between the real rate paid and real growth.

- The r-g condition is the mechanism: when the real rate paid sits below real growth, the debt ratio stabilizes without a primary surplus, which let Italy, France and Japan carry heavy debt through the 2012-2021 negative-rate decade.

- The gap has closed: per the IMF (Fiscal Monitor, October 2025), the average implicit real rate on advanced-economy debt moved from ≈-1.5% in 2021 to ≈+0.8% in early 2026, pushing r-g toward zero against eurozone growth near 1%.

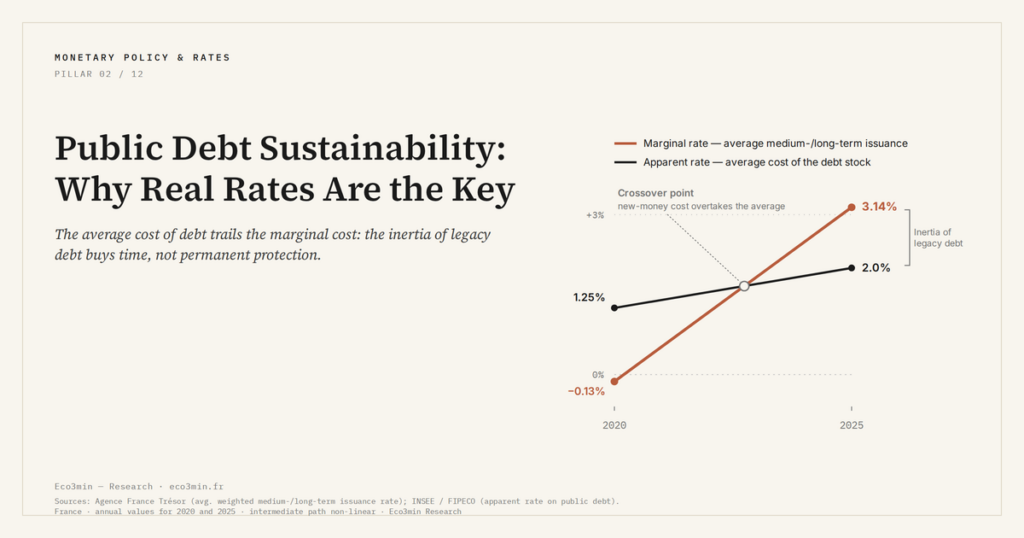

- Legacy debt buys time, not safety: France's average debt maturity is ≈8.5 years (Agence France Trésor), but the Cour des Comptes projects the interest burden could reach ≈€70bn by 2028, roughly double, if real rates hold.

The reversal of real rates since 2022 calls into question fiscal equilibria that seemed settled during the decade of negative rates.

Public debt sustainability rests on the gap between real rates and growth. Analysis of the debt-to-GDP dynamic and its fragilities. A parallel read: the fiscal dominance macro regime atlas.

French public debt reached ≈112% of GDP at end-2025, according to INSEE data. The interest burden in the 2026 budget exceeds €55 billion — an amount that rivals the budget of France’s national education ministry. Yet these nominal figures are not enough to assess debt sustainability. What determines whether debt feeds on itself or stabilizes is the differential between the real rate paid on debt and the real growth rate of the economy — the condition economists summarize as the r – g gap. Read alongside: monetary metal anchored to public-finance sustainability.

The r – g Condition: The Core Mechanism

When the real rate paid on debt (r) sits below real growth (g), the debt-to-GDP ratio stabilizes or declines spontaneously — even without a primary surplus. Striking a balance before interest and striking one after are two different operations, and that is exactly what the arithmetic rests on — the subject of the gap between primary and total deficits. This mechanism explains why heavily indebted countries like Italy, France or Japan could coexist with apparently sustainable public finances between 2012 and 2021: negative real rates made the r – g condition systematically favorable. Related series: our US total public debt dataset (1966–2026).

According to IMF estimates (Fiscal Monitor, October 2025), the average implicit real rate on advanced-economy debt has moved from ≈-1.5% in 2021 to ≈+0.8% in early 2026. With real growth oscillating around 1% in the eurozone, the r – g condition approaches zero — a neutral zone that only stabilizes debt provided the primary balance stays close to equilibrium. Understanding the centrality of real rates in macro dynamics is indispensable to assessing these fiscal trajectories.

The Protective Inertia of Legacy Debt

An element often overlooked in analysis: the rise in real rates does not transmit instantly to the average cost of outstanding debt. This transmission is explained in the mechanism by which markets detach from the yield curve signal. Sovereigns issue bonds at long maturities — the average maturity of French debt stands at ≈8.5 years according to Agence France Trésor. The stock of debt contracted at historically low rates between 2015 and 2021 continues to weigh favorably on the average cost, even as new issuance proceeds at significantly higher rates.

This inertia offers a temporal reprieve, not permanent protection. According to projections from the Cour des Comptes (Annual Report 2025), France’s interest burden could reach ≈€70 billion by 2028 if real rates hold at their current level — a doubling in five years. The channel through which monetary decisions transmit to the cost of debt runs directly through monetary transmission to the real cost of debt, with a lag that depends on the maturity structure.

Assessing debt sustainability from the debt-to-GDP ratio alone ignores the determining factor: the r – g differential. A country with 120% debt-to-GDP and a negative r – g gap sits in a more comfortable position than one at 60% debt-to-GDP whose real rates exceed growth. The debt level matters less than its dynamic, which is conditioned by real rates. A companion piece: our deep dive into the transmission of monetary policy to company results.

What Real Rate Normalization Changes

The shift from a deeply negative r – g gap to a near-zero gap — the early-2026 configuration for most advanced economies — restores a fiscal constraint that had disappeared for a decade. Fiscal room narrows: every point of primary deficit now weighs directly on the debt-to-GDP trajectory, whereas negative rates partially absorbed it. Narrowing room does not by itself close the gap, whose sources are structural — savings surpluses, reserve-currency demand, ageing — and are the substance of the question of why wealthy states run permanent deficits.

For sovereign bond markets, this reconfiguration alters risk pricing. The dispersion of eurozone sovereign spreads — ≈70 basis points between Germany and France, ≈130 for Italy in early 2026 according to market data — reflects fiscal trajectory differences in an environment where real rates no longer act as an automatic shock absorber. This dynamic sits within the monetary conditions that determine these equilibria at the eurozone level.

Friction Points to Keep in Mind

- Debt sustainability depends on the r – g differential, not on the debt-to-GDP ratio in level — a gap that flips positive calls established equilibria into question.

- The inertia of low-rate legacy debt temporarily shields public budgets, but each new issuance at a positive real rate progressively raises the burden.

- The widening dispersion of eurozone sovereign spreads reflects the end of the negative real rate regime that artificially uniformized financing conditions.

Last updated — 22 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…