T10Y3M 1998: The LTCM False Signal, Unique Exception Since 1968

The September 1998 T10Y3M inversion is the single documented false positive for the signal since 1968: a brief inversion triggered by the Russian crisis and LTCM, neutralized by three Fed cuts in eight weeks.

The September 1998 T10Y3M inversion is the single “false positive” documented for the signal since 1968: a brief inversion, triggered by the Russian crisis and the near-failure of the LTCM hedge fund, that was followed by no U.S. recession thanks to an emergency Fed response — three rate cuts totaling 75 basis points in under eight weeks.

TL;DR

Three Greenspan cuts in eight weeks neutralized the September 1998 T10Y3M inversion before it could transmit: the signal's only false positive since 1968, born of Russia's default and LTCM's collapse.

- Russia's August 17, 1998 GKO default sent investors fleeing into Treasuries; LTCM, levered 25x to 30x, lost $4.6 billion in six weeks and was recapitalized September 23 by a fourteen-bank consortium for $3.6 billion.

- The inversion stayed shallow (-25 to -30 bp) for just 8-12 trading days and never showed on the monthly average, so the NY Fed probit peaked near 22%, below its 30% threshold; recent work (Bauer-Mertens) calls it an unconfirmed daily alert rather than a strict false positive.

Examining this exceptional episode illuminates both the empirical frontier of the T10Y3M recession signal and the conditions under which a sufficiently rapid monetary response can neutralize inversion before transmission to the cycle.

The August-September 1998 context — Russian defaults and LTCM destabilization

The September 1998 T10Y3M inversion does not fit the classical pattern of a monetary-tightening cycle followed by inversion. At the time of the crossing, the Fed was not in an active hiking phase — the Fed Funds target rate had last been raised in March 1997 to 5.50 percent and had remained stable there. The 1998 inversion is therefore attributable to a specific exogenous shock: the combination of the Russian financial crisis and the near-collapse of Long-Term Capital Management.

The event sequence begins on August 17, 1998, when Russia announces the suspension of ruble-denominated GKO domestic debt repayment and the devaluation of the ruble. This partial sovereign default — unprecedented for a major economy since 1917 — triggers a massive flight to risk-free assets across global markets. Institutional investors liquidate positions on emerging-market debt and high-yield bonds to buy U.S. Treasuries, producing a sharp drop in the 10-year yield.

This flight to quality is amplified by the destabilization of Long-Term Capital Management in the following weeks. LTCM, the fund managed by John Meriwether with two Nobel economics laureates (Myron Scholes and Robert Merton) on the board, had built positions with extreme leverage (approximately 25x to 30x equity) on bond-spread convergence strategies. The Russian defaults invalidated all its bets, and cumulative fund losses reached $4.6 billion over six weeks. On September 23, 1998, the Federal Reserve Bank of New York organizes a consortium of fourteen major banks to recapitalize LTCM by $3.6 billion, to avert a disorderly liquidation that would have propagated systemic crisis. This is unpacked carefully in our study of the 1998 Russia/LTCM crisis.

The brief September 1998 T10Y3M inversion

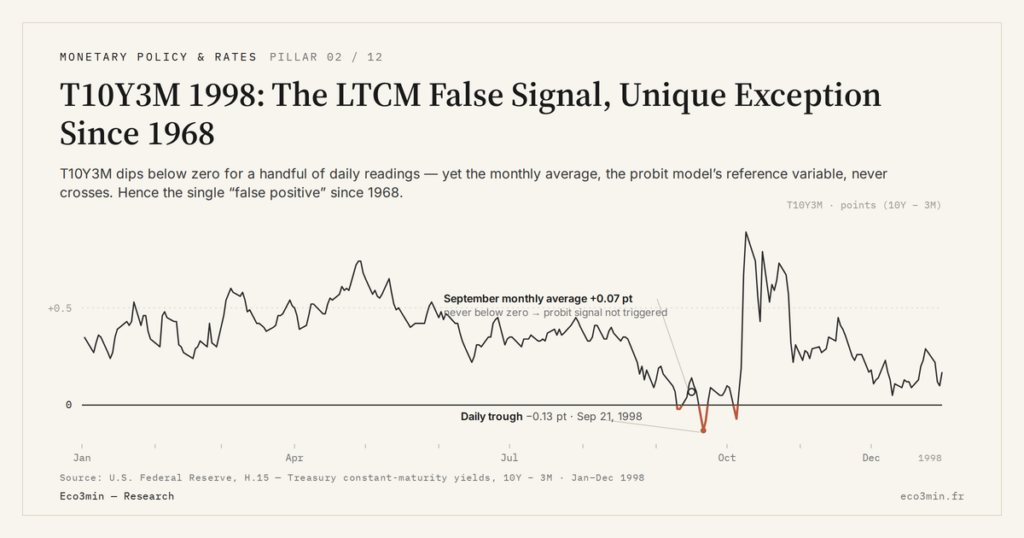

T10Y3M crosses the negative boundary in early September 1998, against a backdrop of a falling 10-year (from 5.50 percent in early August to roughly 4.40 percent in mid-September) combined with a 3-month yield stable around 4.80-5.00 percent, a consequence of the unchanged Fed Funds target rate. The depth of the inversion remains modest — the episode is documented with a trough of order -25 to -30 basis points, eight to ten times shallower than the inversions of 1973, 1980, 2000, or 2023 (all beyond -180 basis points at trough).

The duration of the inversion is also limited. Daily T10Y3M values remain in negative territory for roughly eight to twelve trading days — a short window contrasting with the 626 days of the 2022-2024 inversion or the 460 days of 1978-1980. The crossing was never confirmed on the monthly average, which is the reference variable of the NY Fed probit model: the monthly average for September 1998 stayed marginally positive, around +5 to +10 basis points depending on aggregation conventions. This daily-vs-monthly distinction is essential for qualifying what is here called “false positive.”

The NY Fed probit signal therefore did not exceed the 30 percent conditional-probability threshold over this window — it peaked around 20-22 percent in October-November 1998, a level interpreted as “moderate alert” by Fed economists and contemporary literature, but not triggering a strict-sense recession signal of the model. This is precisely why some recent academic work (Bauer-Mertens 2018, 2023) does not classify 1998 as a false positive of the monthly signal but as an “unconfirmed alert” of the daily signal.

The Fed emergency response — three cuts in under eight weeks

The Federal Reserve under Chairman Alan Greenspan responded to the destabilization with a rapid cutting cycle, unprecedented outside characterized recessionary phases. The first cut occurs on September 29, 1998, six days after the NY Fed-organized LTCM rescue, taking the Fed Funds target rate from 5.50 to 5.25 percent. The second cut, exceptional because decided at an inter-meeting (between two scheduled FOMCs), occurs on October 15, 1998, taking the rate to 5.00 percent. The third cut comes at the scheduled November 17, 1998 FOMC, taking the rate to 4.75 percent.

The cumulative three cuts total 75 basis points over fifty calendar days, a response pace three times faster than a standard cutting cycle (typically 25 bp per FOMC, i.e., five to six weeks). The acceleration is attributed by monetary literature (Greenspan 2007 memoirs; Reinhart-Reinhart 2008) to perceived acute systemic risk linked to the possible propagation of the LTCM crisis through interconnected financial institutions.

This rapid response has two direct effects on T10Y3M. First effect: the 3-month yield immediately follows the Fed cuts — moving from 4.95 percent in late September to 4.50 percent in early December 1998, a 45-basis-point drop aligned with Fed Funds. Second effect: the 10-year rebounds gradually from its trough at 4.16 percent on October 5, 1998 toward 4.65 percent in late December 1998, as recession expectations dissipate. The combination of the two movements produces a complete un-inversion in less than three weeks after the first cut.

Why 1998 is called an exception, not a signal failure

The majority academic literature does not treat 1998 as a failure of the T10Y3M signal but as a boundary case illuminating the validity conditions of the probit model. Three arguments structure this reading.

First argument, the signal threshold was not triggered. As noted above, the monthly average of T10Y3M in September 1998 stayed marginally positive, and the probit probability did not exceed 22 percent conditional probability. The “strict” NY Fed model signal — conventionally defined by a sustained crossing of the monthly boundary and a 30 percent threshold exceedance — was not activated. This distinction between daily signal (briefly crossed) and monthly/probit signal (not crossed) is central to the academic qualification of the episode.

Second argument, the 1998 inversion is not mechanically the product of a classical tightening cycle. The other seven documented T10Y3M inversions since 1968 all came on the heels of a Fed hiking cycle (typically 12 to 18 months into a tightening cycle). The 1998 inversion came in a context of stable Fed Funds for eighteen months — the inversion was the product of an exogenous shock on the long leg (flight to quality), not of an ongoing monetary tightening. This generational difference invalidates direct application of the interpretive model that assumes a transmission channel through post-tightening bank-credit contraction. The complete analysis of why the yield curve inverts precisely distinguishes these two generations.

Third argument, the rapid Fed response effectively neutralized transmission. Counterfactual analyses published by the Fed and the monetary literature (Carlson 2007 FEDS WP, Mishkin 2010) estimate that absence of fall-1998 Fed cuts would likely have produced a recession in H1 1999, through propagation of the LTCM crisis to exposed financial institutions and contraction of interbank credit. This counterfactual estimate, non-verifiable by nature, does not invalidate the signal — it suggests the signal extinguished because its underlying cause (tightening of financial conditions) was corrected by monetary action.

Implications for reading the probit model in atypical regimes

The 1998 episode teaches two operational readings for atypical economic regimes where the T10Y3M signal must be interpreted with additional uncertainty margin. This nuance enriches the reading framework available through common mistakes in interest-rate analysis by flagging the conditional validity of the signal.

First reading, distinguish daily signal from monthly signal. A brief daily inversion does not automatically activate the probit signal. The NY Fed model is calibrated on the monthly average, and a crossing of a few trading days may never propagate to the monthly statistic. The “false positive” 1998 is actually a false positive of the daily signal, not of the official probit signal. This terminological distinction matters for correctly qualifying future episodes where daily would briefly cross without persistence.

Second reading, identify the generation of the inversion. An inversion produced by an exogenous shock on the long leg (flight to quality, foreign financial crisis, massive institutional repositioning) does not have the same cyclical implication as an inversion produced by an ongoing monetary tightening cycle. The former is typically reversible by rapid monetary action; the latter signals effective tightening of credit conditions that transmits with standard 12-to-18-month lag. The distinction is not always trivial in real time — it requires mapping the spread decomposition between 3-month movement (Fed proxy) and 10-year movement (expectations + term premium + exogenous shock).

Over the 2022-2024 period, no serious reading attempted to classify the T10Y3M inversion as “1998 type” — the record depth (-189 bp), record duration (626 days), concurrence with a 525-basis-point Fed hiking cycle, and absence of an equivalent exogenous shock made the “classical cycle” qualification undisputable. Comparative detail is documented in the 2022-2024 T10Y3M inversion, the longest since 1980. But the memory of 1998 informs caution on future brief or shallow inversions, requiring their generation to be identified before applying the standard interpretive grid. This nuance is integrated into the central-bank policy and rate-cycle transmission framework retained by Eco3min for monetary-signal reading.

- The September 1998 T10Y3M inversion is the single documented “false positive” since 1968: a brief inversion (8 to 12 days), shallow (-25 to -30 bp), followed by no recession.

- The episode was generated by an exogenous shock (August 1998 Russian crisis, September 1998 LTCM near-failure), not by a Fed tightening cycle — key structural distinction.

- Greenspan’s Fed responded with three cuts in eight weeks (Sept 29, Oct 15, Nov 17, 1998), totaling 75 bp, with complete un-inversion in under three weeks.

- The NY Fed monthly probit signal did not exceed 22 percent conditional probability; some recent work (Bauer-Mertens) does not classify 1998 as a strict false positive but as an unconfirmed alert of the daily signal.

Last updated — 20 June 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…