T10Y3M Recession Signal: The 10y / 3m Treasury Spread Explained

The T10Y3M spread, the gap between the 10-year Treasury yield and the 3-month Treasury bill, has stood for three decades as the empirical reference variable for estimating U.S. recession probability, validated each month by the Federal Reserve Bank of New York.

The T10Y3M spread — the gap between the 10-year Treasury yield and the 3-month Treasury bill — has stood for three decades as the empirical reference variable for estimating U.S. recession probability, a choice formalized by Estrella and Mishkin and validated each month by the Federal Reserve Bank of New York.

TL;DR

An inverted T10Y3M curve compresses bank net interest margins, tightening lending two to four quarters later, the documented channel that turns the yield-curve signal into recession.

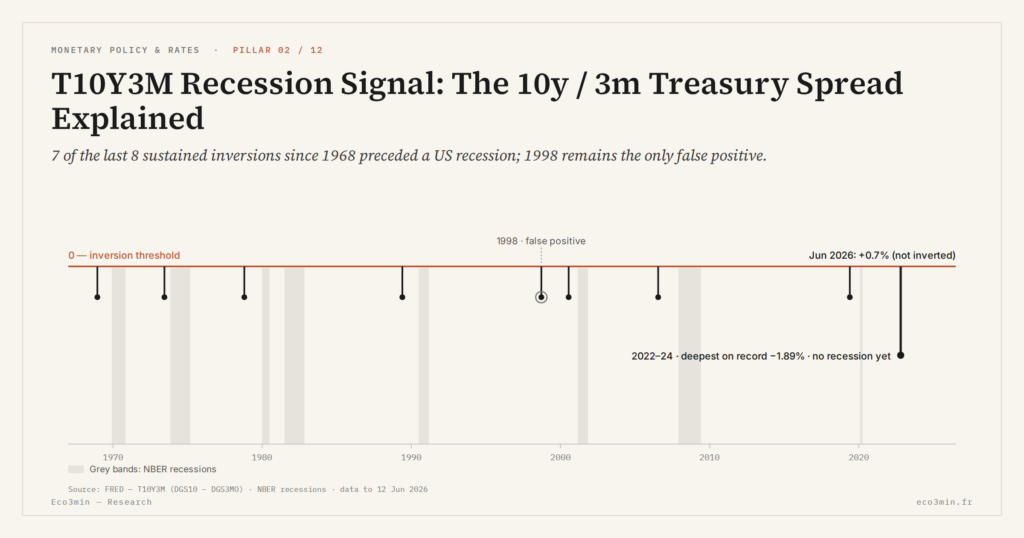

- Across eight inversions since 1968, seven preceded an NBER recession, an 87.5% true-positive rate, with a median lag of twelve months but a range of five to seventeen; the 2022-2024 episode (trough -189 bps, 626 trading days) shows none NBER-dated 35 months on.

- Estrella and Mishkin formalized the 10y/3m pair in 1996 (NBER Working Paper 5379); adding real-activity controls such as industrial production did not improve out-of-sample fit and in several specifications worsened it, leaving the single-variable model preferred.

- The New York Fed publishes a monthly 12-month recession probability from a univariate probit, Φ(α + β × T10Y3M_t-12), estimated by maximum likelihood; historically the figure exceeded 30% ahead of each of the seven recessions.

Reading this signal requires understanding why this specific maturity combination, what it captures that others do not, and how to interpret it within the post-QE regime that began in 2022.

Why this maturity pair rather than another

The 10-year / 3-month combination is not an inherited convention but the result of a formal empirical selection published by Arturo Estrella and Frederic Mishkin in a National Bureau of Economic Research working paper in 1996 (NBER Working Paper 5379, later published in the Review of Economics and Statistics in 1998). The authors systematically tested several candidate yield curve spreads — the 1-year / 10-year, 2-year / 10-year, Fed Funds / 10-year, as well as variants incorporating equity indices, industrial production, or Conference Board leading indicators — over the 1959-1995 sample, and measured their out-of-sample predictive power against NBER-dated recessions. The T10Y3M spread emerged as the top performer on nearly every test: best likelihood ratio, best pseudo-R-squared, and most importantly best performance on out-of-sample evaluation windows, which guard against overfitting.

This empirical result reflects distinct analytical properties of the two selected maturities. The precise meaning of T10Y3M requires returning to what each leg of the spread measures in isolation.

Three months as a direct proxy for the policy rate

The 3-month Treasury bill secondary market yield (FRED series DGS3MO and the complementary DTB3 series) tracks the Fed Funds effective rate with a spread typically oscillating between five and fifteen basis points. This proximity reflects a direct arbitrage mechanism: 3-month T-bills are near-perfect substitutes for collateralized interbank operations backed by Treasury securities, and their yield mechanically aligns with the very short-term funding cost set by the Federal Open Market Committee. When the Fed raises rates, the 3-month yield follows within roughly two weeks of the FOMC decision — the full absorption delay never exceeds a month.

This property makes the 3-month yield a superior indicator of the effective policy rate compared with the 2-year yield, which already embeds partial expectations about the future path of monetary policy. For recession reading, the relevant quantity is the gap between current monetary policy and long-run expectations — not the gap between two distinct sets of expectations at different horizons. The 3-month is, on this score, the cleanest mirror of current monetary tightening.

Ten years as the mirror of long-run expectations

At the other end, the 10-year Treasury yield (FRED series DGS10) embeds three theoretically decomposable components: the expected path of the Fed Funds rate over ten years, the term premium demanded by long-duration holders, and a residual structural demand component for duration (foreign central banks, pension funds, life insurers with long liabilities). On this clock, ten years is long enough to smooth out cyclical noise from the monetary path — an investor holding a 10-year bond integrates several possible Fed cycles over the holding period. Our term-premium record sets out how the indicator is built.

The 30-year alternative, occasionally suggested, is empirically rejected for two reasons. First, the term premium becomes the dominant factor there and blurs the expectations component. Second, the 30-year Treasury market is less liquid and more sensitive to idiosyncratic flows (pension fund rebalancing, insurer duration adjustments), which introduces noise unrelated to macroeconomic reading. The 10-year maturity sits at the equilibrium point where market depth (over two trillion dollars of weekly volume in 2024) ensures a clean signal while remaining long enough to ignore cyclical noise.

The empirical selection: Estrella, Hardouvelis, and the NY Fed formalization

The first systematic work on the predictive power of the yield curve dates back to Estrella and Hardouvelis (1991), published in the Journal of Finance. The authors established that the slope of the curve precedes turning points in U.S. economic activity with a one- to two-year horizon, and that this property is robust over the 1955-1988 sample. The paper does not yet definitively rank slope variants, but it establishes the methodological foundation — probit regression on NBER-dated binary recession indicators, with coefficients calibrated by maximum likelihood.

Earlier work by Robert Laurent (1988, Federal Reserve Bank of Chicago Economic Perspectives) and Frederic Mishkin (1990, Journal of Monetary Economics) had already documented that yield curve slope contained information about future real activity, but without formalizing the recession-probability framework. James Stock and Mark Watson (1989, NBER Macroeconomics Annual) tested yield-curve variables within broader leading-indicator combinations, finding them robust but not isolating them as a standalone signal. Estrella-Hardouvelis 1991 represents the convergence point where these strands met and produced the first explicit recession-prediction framework.

It was in 1996 that the T10Y3M selection became explicit. Estrella, then an economist at the Federal Reserve Bank of New York, and Mishkin, then at Columbia, published the formal out-of-sample comparison at the NBER. Their key result: T10Y3M dominated not only the other yield curve spreads tested, but also richer models incorporating real variables such as industrial production or leading indicators. The parsimony of the model — a single variable — became an additional argument in favor of out-of-sample robustness. The standard objection to univariate models — that they ignore valuable conditioning information — was empirically refuted: adding real-activity controls to the probit specification did not improve out-of-sample fit, and in several specifications worsened it, a result attributed to the curse of dimensionality on a sample with relatively few recession events (eight episodes over the testing window).

The Federal Reserve Bank of New York then adopted the model as an internal tool, and has since 2006 published on a dedicated page the 12-month recession probability it generates, updated at each monthly close of Treasury series. This publication installed T10Y3M as the canonical variable in the monetary research ecosystem and among market economists. The T10Y3M vs T10Y2Y comparison across the eight historical inversions confirms this empirical dominance, despite the broader media coverage given to the 2-year / 10-year spread.

A recent review by Michael Bauer and Thomas Mertens at the Federal Reserve Bank of San Francisco (Economic Letter 2018-07) reexamined the signal’s robustness following the expansion of the Fed balance sheet and quantitative easing policies. Their conclusion: T10Y3M retains statistically significant predictive power over the expanded 1959-2018 sample, and the credit-channel transmission mechanism remains operative despite term-premium distortions introduced by QE. The QE-effect debate is addressed later in this analysis, but this robustness finding explains why the NY Fed has not reformulated its model after the 2008-2009 crisis. A 2023 update by the same authors (Economic Letter 2023-14) extended the analysis through the 2022 inversion onset, confirming numerical stability of the coefficients and absence of structural break in the predictive relationship.

The transmission mechanism — how inversion becomes recession

The predictive power of T10Y3M does not rest on a statistical coincidence but on a documented causal channel: yield curve inversion alters the profitability structure of the banking system, which alters its lending behavior, which ultimately slows investment and consumption. The detail of this causal mechanism through the credit channel deserves laying out to understand why a six- to eighteen-month lag typically separates inversion from the actual decline in GDP.

The bank credit channel — net interest margins

U.S. commercial banks by construction operate a maturity transformation: they fund themselves short-term (demand deposits remunerated at money-market rates, three-month certificates of deposit, overnight repo) and lend long-term (thirty-year residential mortgages, five- to ten-year commercial loans, lines of credit indexed on compounded rates). Their net interest margin — the difference between the average asset yield and the average funding cost — depends mechanically on the slope of the yield curve.

When T10Y3M is positive and wide, maturity transformation is profitable. Banks are incentivized to extend their balance sheets, to apply mild credit standards, to offer competitive rates on long-term loans. When T10Y3M inverts, the profitability structure inverts as well: lending at ten years at a rate below the three-month funding cost becomes a negative-margin operation — at least on an accounting basis, subject to the bank’s capacity to hedge duration via swap or other coverage.

The operational consequence is visible in the Senior Loan Officer Opinion Survey (SLOOS), the quarterly Federal Reserve survey of roughly one hundred major commercial banks. Historically, the net share of banks tightening Commercial and Industrial loan standards rises in the two to four quarters following a T10Y3M inversion, reaching levels above 30 percent during the 2001, 2008, and 2020 recessions. During the 2022-2024 inversion, SLOOS showed tightening from the second quarter of 2023 onward, that is, two quarters after T10Y3M crossed into negative territory on October 25, 2022.

Net interest margins and lending incentives

Transmission of the credit supply tightening to the real economy operates through three measurable channels. First, the volume of commercial and industrial loans (Fed series TOTLL and BUSLOANS) slows and then contracts typically six to twelve months after SLOOS tightening. Second, non-bank financing conditions tighten in parallel: investment-grade and high-yield corporate credit spreads widen, the leveraged loan market contracts, and the private credit conditions indices tracked by the Chicago Fed enter restrictive territory. Third, the housing market reacts with an additional lag: building permits, new home sales, and then construction employment peak and then decline.

This transmission chain explains why T10Y3M inversion precedes NBER recession with a median lag of twelve months and an observed range of six to eighteen months across the eight inversions documented since 1968. The lag is neither a coincidence nor a miraculous regularity: it corresponds to the time required for the change in bank behavior to propagate through borrowing firms’ balance sheets, then through their hiring and investment decisions, then through household income, then through aggregate demand.

Empirical lags — why not instantaneous

A mechanical reading of the curve — “inversion triggers recession in X months” — misses the operational nuance. The lag depends on three factors: the depth of inversion (the deeper the trough, the more compressed the bank margin), its duration (one month in negative territory does not produce the same balance-sheet effect as eighteen months), and the initial state of bank balance sheets (capital level, duration risk exposure, dependence on market funding versus deposits). For the 1998 inversion — examined as an edge case later in this analysis through the 1998 T10Y3M false positive and its lessons — the combination of low depth (29 basis points trough) and short duration (eight trading days) prevented the transmission from initiating.

For the 2022-2024 inversion, by contrast, the depth (189 basis points trough in May 2023) and the duration (626 trading days) created the conditions for maximum transmission — which was indeed reflected in the SLOOS tightening mentioned, but without leading to an NBER-dated recession at the date of this analysis. The debate on this apparent anomaly is addressed in the final section.

Eight T10Y3M inversions since 1968 — historical table

The T10Y3M series (DGS10 minus DTB3) is published by the Federal Reserve Bank of St. Louis on a daily frequency from January 1962 onward. Across the sixty-two years covered, eight episodes of sustained inversion (lasting more than ten consecutive trading days in negative territory) are documented. Seven of these eight inversions were followed by an NBER-dated recession, with a median lag of twelve months between the inversion trough and the economic activity peak. The table below summarizes the essential characteristics of each episode.

| Inversion | Start | End | Duration (trading days) | Max depth (basis points) | NBER recession | Lag to recession |

|---|---|---|---|---|---|---|

| 1968-1969 | Dec 1968 | Jan 1970 | ≈ 250 | -115 | Dec 1969 – Nov 1970 | 12 months |

| 1973 | Jun 1973 | Jan 1975 | ≈ 320 | -218 | Nov 1973 – Mar 1975 | 5 months |

| 1978-1980 | Oct 1978 | Aug 1980 | ≈ 460 | -460 | Jan 1980 – Jul 1980, then Jul 1981 – Nov 1982 | 15 months |

| 1989 | May 1989 | Oct 1989 | ≈ 105 | -49 | Jul 1990 – Mar 1991 | 14 months |

| 1998 (false positive) | Sep 1998 | Oct 1998 | 8 | -29 | None within 24 months | n.a. |

| 2000 | Jul 2000 | Jan 2001 | ≈ 130 | -95 | Mar 2001 – Nov 2001 | 8 months |

| 2006-2007 | Jul 2006 | Aug 2007 | ≈ 260 | -66 | Dec 2007 – Jun 2009 | 17 months |

| 2019 | May 2019 | Oct 2019 | ≈ 90 | -52 | Feb 2020 – Apr 2020 | 9 months |

| 2022-2024 | Oct 2022 | Dec 2024 | 626 | -189 | None NBER-dated as of May 16, 2026 | pending |

This table invites several complementary readings.

First observation: the consistency of the signal across fifty years. Seven inversions out of eight were followed by an NBER recession, a true positive rate of 87.5 percent — a remarkable score for an economic indicator. No other single-variable recession signal achieves this precision over a comparable sample. The Conference Board leading indicators, Fed regional activity indices (Philly Fed, Empire State, KC Fed), or ISM surveys do not match this robustness over a five-decade horizon.

Second observation: the dispersion of lags. The lag between inversion and recession ranges from five to seventeen months across episodes. This empirical dispersion invalidates any mechanical reading of the type “inversion plus twelve months equals recession.” The twelve-month median is useful as an approximate clock, but the distribution has wide tails: the lower quartile is at eight months, the upper quartile at fifteen. For the 2022-2024 inversion, the lag since the May 2023 depth trough reaches thirty-five months at the date of this analysis — well beyond the historical envelope.

Third observation: the calibration of the probit model.The probit formalization of the T10Y3M signal by the NY Fed uses precisely this panel of eight inversions to calibrate its coefficients. The recession probability the model generates depends on the average depth of the inversion over the trailing twelve-month window — a parametrization that reproduces the historical peaks ahead of the actual recessions (1969, 1973, 1980, 1990, 2001, 2008, 2020).

The 1998 inversion — the exception that clarifies the signal

The September-October 1998 inversion occupies a distinct place in the literature because it constitutes the only sustained false positive in the series. Over eight trading days, T10Y3M crossed into negative territory at a trough of -29 basis points, in the context of the Long-Term Capital Management (LTCM) hedge fund crisis and the Russian sovereign defaults of August 1998. The Federal Reserve, under Alan Greenspan, responded with three consecutive emergency Fed Funds cuts (September 29, October 15, November 17, 1998), totaling 75 basis points.

This rapid monetary response re-steepened the curve within two months and prevented credit-system transmission from producing its contractionary effects. The U.S. economy entered an expansion phase that lasted another twenty-eight months before the official March 2001 recession — which is attributable to the technology cycle reversal (Nasdaq correction beginning March 2000) and not to a delayed effect of the 1998 inversion. This isolated case reinforces the causal reading a contrario: without sustained transmission through banking contraction, inversion does not precipitate recession.

The NY Fed probit model as quantitative formalization

The Federal Reserve Bank of New York publishes each month, on its Recession Probability page, a 12-month U.S. recession probability computed from a univariate probit model whose only explanatory variable is the monthly average of T10Y3M. The functional form is Φ(α + β × T10Y3M_t-12), where Φ denotes the cumulative distribution function of the standard normal and the twelve-month lag reflects the forecasting horizon retained. The coefficients are estimated by maximum likelihood over the 1959-present history and updated as data accumulates.

The model output is directly interpretable as a conditional probability: given the current value of T10Y3M, what is the probability that the U.S. economy enters a recession (NBER definition) within the next twelve months. Historically, this probability exceeds 30 percent ahead of each of the seven actual recessions, and 50 percent for the 1973, 1980-1982, 1990, 2008, and 2020 recessions. The 1998 probability reached 27 percent, just below the 30 percent empirical alert threshold commonly retained.

For the 2022-2024 inversion, the probability peaked at 71 percent in June 2023, a level consistent with the historical peaks ahead of the 1980 and 2008 recessions. As of May 2026, this probability has receded to about 8 percent following the December 2024 un-inversion, but the retrospective analysis of the sequence is still in progress: no recession has been NBER-dated at this stage, even though the model spent sixteen consecutive months above 50 percent. The detailed replication of the model by Eco3min economists documents the numerical stability of the coefficients and the absence of structural drift in predictive power over the post-1990 period.

The 2022-2024 episode — the longest inversion since Volcker

On October 25, 2022, the T10Y3M spread crossed the negative boundary at one basis point below zero for the first time. It exited on December 13, 2024, after 626 consecutive trading days in negative territory — the longest uninterrupted sequence documented since the October 1978 to August 1980 inversion under the Volcker chairmanship, which had totaled roughly 460 trading days. No other inversion in the T10Y3M series has exceeded 320 days.

The trigger of the 2022 inversion is mechanically attributable to the most rapid monetary tightening cycle since 1980. Between March 2022 and July 2023, the Federal Open Market Committee raised the Fed Funds target range from 0.25-0.50 percent to 5.25-5.50 percent, a cumulative 500 basis points over sixteen months. During this sequence, the 3-month yield rose from 0.12 percent to 5.55 percent, faithfully tracking the Fed Funds effective rate. Meanwhile, the 10-year yield rose only from 1.73 percent to a peak of 4.98 percent in October 2023, reflecting a collective anticipation of return to a lower long-run equilibrium rate. The 2022-2024 T10Y3M inversion, the longest since 1980, is documented month by month in the dedicated article, with precise daily depth values.

Maximum depth was reached on May 4, 2023, at -189 basis points — the deepest trough since 1981. On that date, the 3-month yielded 5.12 percent and the 10-year yielded 3.23 percent. This extreme configuration matched the market consensus anticipating an imminent recession from monetary tightening — an anticipation that economist surveys (Philadelphia Fed Survey of Professional Forecasters, Bloomberg consensus, Blue Chip Economic Indicators) placed predominantly in Q4 2023 or Q1 2024.

That recession did not materialize on schedule. U.S. GDP instead accelerated by 2.1 percent annualized in 2023, supported by household consumption (disposable incomes lifted by pandemic-era savings and by post-tight-labor-market wage adjustments), by non-residential investment (notably through Inflation Reduction Act and CHIPS Act incentive programs), and by a federal deficit that remained above 6 percent of GDP. The probit recession probability peaked at 71 percent in June 2023, but no cyclical trigger converted this high probability into an actual recession.

The December 2024 un-inversion marks the formal end of the episode. The August to December 2024 T10Y3M un-inversion operated primarily through the short leg: the 3-month yield collapsed from 5.38 percent on July 31, 2024 to 4.30 percent on December 31, 2024, a direct consequence of the three Fed Funds cuts of September (50 basis points), November (25 basis points), and December 2024 (25 basis points). The 10-year yield, by contrast, remained contained within a 4.15-4.55 percent band over the same period. This un-inversion mechanic — short-rate collapse faster than long-rate decline — historically corresponds to the un-inversion profile observed ahead of the 2001, 2008, and 2020 recessions.

Direct comparison with the Volcker 1978-1980 episode

The only T10Y3M inversion longer in history is that of October 1978 to August 1980, under Paul Volcker’s Federal Reserve chairmanship. This inversion lasted roughly 460 consecutive trading days and reached a maximum depth of -460 basis points in March 1980 — that is, 2.4 times deeper than the 2022-2024 trough at -189 basis points. This historical magnitude reflects the exceptional monetary shock Volcker imposed to break inflation at 14.8 percent at the March 1980 peak: the Fed Funds rate was raised to 19-20 percent in March-April 1980 and again to 19 percent in May-June 1981 — levels never matched since in the modern history of the Federal Reserve.

Three structural differences between Volcker 1978-80 and 2022-2024 deserve note for calibrating the comparison. First, pre-tightening inflation: 14.8 percent peak in 1980 versus 9.1 percent in June 2022. Volcker faced a more entrenched inflationary regime that required a deeper inversion trough to produce the necessary contraction. Second, cyclical composition: 1978-80 produced two distinct recessions (January-July 1980 then July 1981-November 1982), separated by a brief recovery — a sequence sometimes labeled “double-dip” by cycle historians. 2022-2024 produced no recession dated in the inversion’s wake. Third, fiscal policy regime: 1978-80 unfolded under relative fiscal discipline (federal deficit below 3 percent of GDP on average), whereas 2022-2024 unfolded under continuous fiscal expansion (deficit above 5 percent of GDP). This third difference potentially explains part of the outcome asymmetry — 2022-2024 monetary contraction was offset by fiscal support absent in 1978-80. Our map of historical market crises gathers these episodes.

This comparison highlights that depth alone does not determine recessionary outcome: the combination of depth, duration, and fiscal context determines effective transmission. The 2022-2024 episode is longer than Volcker in duration but shallower in magnitude, and it unfolded within a strong fiscal counterweight. The macroeconomic resultant — no recession dated at the end of the inversion — is consistent with that parameter combination, without invalidating T10Y3M as a measure of intentional monetary tightening by the FOMC.

Reading T10Y3M inversion mechanically as a fixed-lag clock — “inversion in October 2022, therefore recession in autumn 2023” — confuses an empirical median regularity with a deterministic law. The historical lag dispersion (five to seventeen months) and the unique 1998 false positive impose a probabilistic reading: T10Y3M adjusts the conditional probability of recession, it does not fix the date. The NY Fed probit calibration translates that nuance — a 70 percent probability still leaves 30 percent of scenarios where recession does not materialize within the projected window.

Sources, methodology, and the ecosystem of alternative spreads

The T10Y3M series as used by the Federal Reserve Bank of New York and by virtually all academic literature is calculated from two primary series distributed by the Federal Reserve Bank of St. Louis on its FRED platform. The first, DGS10, measures the 10-year Treasury constant maturity yield, daily-interpolated by the Treasury Department from the active issuance curve. The second, DTB3, measures the secondary market yield of the 3-month Treasury bill, also constant maturity, calibrated on same-day secondary transactions. The difference between the two is published directly by FRED under the T10Y3M ticker, in percentage points to two decimals, available daily since January 1962.

A technical nuance deserves note: two conventions exist for calculating the “three months.” The constant-maturity convention (DTB3) smooths gaps between thirteen-week newly issued T-bills and older T-bills in portfolio by interpolating the active issuance curve. The pure secondary-market convention (DGS3MO) takes the current yield of a residual 3-month T-bill — often slightly different from DTB3. The NY Fed uses DGS10 minus DGS3MO in its probit model, while FRED publishes T10Y3M from DGS10 minus DTB3. The gap between conventions typically oscillates between five and ten basis points and does not affect signal reading, but it explains small numerical divergences between distinct publications.

The NY Fed Recession Probability page publishes the resulting 12-month recession probability monthly, with a delay of approximately two weeks after month-end. The coefficients are re-estimated annually, and their temporal stability is one of the arguments in favor of model robustness: since 1996, the published α and β coefficients have varied by less than 10 percent of their central value, suggesting an absence of structural drift in predictive power. T10Y3M raw data downloads are accessible from the Eco3min dataset that aggregates the FRED series with NBER recession bands and probit probability values, in CSV format.

The ecosystem of alternative spreads and their place in the literature

T10Y3M coexists with half a dozen candidate yield curve spreads that have been tested against it in the literature and that circulate in practitioner use. Four deserve mention for situating the NY Fed choice within its intellectual ecosystem.

The Fed Funds / 10-year spread (FF-10Y) was advocated by Jonathan Wright in a Federal Reserve Board paper in 2006 (Finance and Economics Discussion Series 2006-07), which showed a slight superiority of this spread over T10Y3M in certain specifications. The argument rests on direct use of the Fed Funds rate as the proxy for current monetary tightening, without going through the 3-month bill as intermediary. The counter-argument offered by Estrella and Trubin (NY Fed Current Issues 2006) is that the Fed Funds rate is administered by monetary policy and not by the market, which can introduce discontinuities at FOMC decision dates. T10Y3M thus retains the advantage of market purity.

The near-term forward spread, proposed by Eric Engstrom and Steven Sharpe at the Federal Reserve Board in 2018 (Finance and Economics Discussion Series 2018-055), measures the gap between the eighteen-month forward yield implied by the curve and the current 3-month yield. The authors show that this spread, shorter in horizon than T10Y3M, has predictive power comparable or superior over the 1973-2017 window. This proposal reignited a debate on the share of the “far slope” in the signal — a debate that has not yet converged. The NY Fed maintains T10Y3M as the principal variable but has also published the near-term forward spread on its Recession Indicator page since 2020 as a complementary indicator.

Credit spreads — notably the Gilchrist-Zakrajsek excess bond premium (American Economic Review 2012) — capture a dimension orthogonal to T10Y3M: the perceived default risk on corporate debt, independent of term structure. In recent inversions, the GZ spread has provided useful confirmatory signal, but its precocity as a leading indicator is inferior to T10Y3M. It remains used as a complement in Fed-style macroeconomic models. Related research: the case for 2-year or 10-year.

Finally, aggregate financial conditions indices (Chicago Fed National Financial Conditions Index, Bloomberg Financial Conditions Index, Goldman Sachs Financial Conditions Index) embed T10Y3M as one of many components, alongside credit spreads, implied volatilities, equity indices, and bank funding spreads. These indices do not dominate T10Y3M in recession prediction, but they offer a useful multidimensional reading for decomposing the sources of ongoing financial stress. The Chicago Fed NFCI series documents this measure in detail.

Institutional use by foreign central banks

The use of T10Y3M as a reference signal is not limited to the Federal Reserve. The Bank of England explicitly tracks T10Y3M in its financial stability publications as a U.S. recession risk indicator — relevant for its own stress scenarios, given that a U.S. recession affects global demand and sterling funding conditions. The European Central Bank publishes its own analogs on the Bund curve (German 10-year minus 3-month Euribor) in the Financial Stability Review, explicitly noting their calibration on the Estrella-Mishkin methodology. The Bank of Japan, whose domestic curve was altered by Yield Curve Control between 2016 and 2024, tracks T10Y3M as an external proxy for the global monetary cycle.

This broad institutional adoption is a secondary but notable argument in favor of the NY Fed choice: T10Y3M is the only recession spread to have traversed three decades of academic discussion without being dethroned by an empirical challenger, and its use by several independent central banks validates its intellectual robustness beyond the U.S. perimeter. The model’s position within the broader toolkit for reading central-bank policy and rate-cycle transmission makes it, in practice, the default barometer consulted by market-economics desks and by financial risk-management units.

Reading the signal today — limits and nuances

The 2022-2024 episode has reopened the academic and operational debate on the reliability of the T10Y3M signal in a structurally modified environment following post-2008 quantitative easing policies. This discussion sits within a broader reading of monetary regimes and interest rate cycles, where the interaction between conventional instruments (Fed Funds) and unconventional ones (asset purchases, forward guidance) alters the propagation of FOMC decisions to the full curve. Three questions deserve resolution to calibrate signal reading in 2026.

The 1998 false positive and the possibility of a 2022-2024 false positive

With the December 2024 un-inversion and no NBER-dated recession as of the date of this analysis, the 2022-2024 inversion empirically becomes the second sustained T10Y3M inversion without a following recession — subject to future retrospective dating by the NBER Business Cycle Dating Committee, which can occur with a delay of two to three years. The 1998 precedent does not provide a direct parallel: the 1998 inversion lasted eight days and was interrupted by an emergency Fed intervention. The 2022-2024 inversion lasted 626 days without offsetting intervention, and the probit probability spent sixteen months above 50 percent.

Two explanations coexist in recent literature. The first, advanced by Bauer and Mertens (SF Fed Economic Letter 2018-07 then 2023-14), considers that the signal remains valid but that credit-channel transmission was offset by other forces: post-pandemic excess savings, federal fiscal expansion, acceleration of industrial investment spending tied to sectoral subsidy policies. The recession would be simply delayed beyond the historical eighteen-month window, not canceled. The second, advanced notably by Marco Del Negro et al. at the NY Fed (Liberty Street Economics, 2024), explores the hypothesis of a structural term-premium distortion caused by massive Fed purchases of long Treasuries post-2020, which would reduce the expectations component in the 10-year yield and bias the spread downward.

The distortion argument relies on a technical decomposition of the 10-year yield into two components: the average expected short rate over ten years (the “expected short rates” component), and the term premium. Affine term-structure models, including the Adrian-Crump-Moench (ACM) estimation maintained by the NY Fed, suggest that the 10-year term premium remained markedly negative across 2022-2024 (between -50 and -100 basis points depending on period), whereas it was positive at comparable levels during pre-2008 inversions.

If the term premium is artificially compressed, the 10-year yield understates the true expectations component — which makes the T10Y3M spread more negative than it would be under a normalized term-premium regime. The corollary: a given inversion in 2022-2024 would be less “signal-heavy” than an inversion of the same magnitude in 1989 or 2006. This argument is not universally accepted; it remains empirically contested because ACM models themselves produce estimates surrounded by wide uncertainty bands. But it provides an interpretive grid that helps reconcile the persistence of the probit signal with the absence of an actual recession.

The T10Y3M vs T10Y2Y question

In the financial press, the 2-year / 10-year spread (T10Y2Y) is more frequently cited than T10Y3M. This media preference rests on two properties: T10Y2Y inverts on average two to four months earlier than T10Y3M (the 2-year yield already embeds Fed hike expectations), and it is tracked by the bond market as a tactical indicator. But this earliness comes at the cost of lower robustness: T10Y2Y produces more marginal ambiguous signals (brief and shallow inversions), and its academic alignment with the bank credit channel is less direct — a commercial bank’s net interest margin depends on very short-term funding cost, better captured by the 3-month than by the 2-year.

For rigorous predictive use, the NY Fed retains T10Y3M. For tactical use in bond markets, T10Y2Y retains its utility. The two signals are complementary: their divergence is itself an indicator, signaling a dissociation between very-short-term and medium-term expectations. Over 2022-2024, T10Y2Y inverted in July 2022 — three months before T10Y3M — and turned positive again in September 2024 — also three months before T10Y3M.

Implications of the 2024 un-inversion for 2025-2026 reading

The exit from negative territory in December 2024 does not close the debate on signal reading, but shifts it. Historically, un-inversion — the moment when the spread returns to positive — precedes actual recession with a median lag of nine months, and this turning-point signal is even considered in part of the literature as more predictive than the initial inversion. The mechanism: un-inversion occurs when the Fed begins cutting policy rates, which materializes FOMC recognition of an ongoing deterioration. In the 2001, 2008, and 2020 inversions, un-inversion occurred respectively nine, twelve, and one month before the NBER-dated activity peak. Adjacent reading: Fed versus ECB, by the data.

For 2025-2026, this logic would imply heightened vigilance through approximately September 2025 — nine months after the December 2024 un-inversion. As of May 2026, this window has largely passed without a dated recession, which constitutes a progressive disarming signal if one adheres to the historical envelope. But the NBER Business Cycle Dating Committee operates with a twelve- to twenty-four-month lag on retrospective dating: a recession initiated in late 2025 might not be confirmed until 2027. The conservative reading therefore consists of maintaining non-trivial conditional recession probability until positive confirmation of sustained growth over 2026-2027.

Three confirmation indicators deserve tracking in parallel with T10Y3M to calibrate this conditional reading. The first is the unemployment rate: Claudia Sahm’s rule (Sahm rule), based on the three-month moving average of the unemployment rate minus its prior twelve-month minimum, triggers a recession signal when the gap exceeds 0.5 percentage points. As of May 2026, the U.S. unemployment rate oscillates around 4.1 percent with a three-month moving average near its local minimum — the Sahm rule is not active. The second is real quarterly GDP growth and its acceleration/deceleration, measured by the Bureau of Economic Analysis. The third is the Conference Board Leading Economic Index, historically in negative territory over six consecutive months before each NBER recession. Related dataset: our Sahm-rule data.

The convergence of these three indicators with T10Y3M constitutes the prudent multifactor reading. Over 2022-2024, T10Y3M and the LEI signaled an imminent recession, but neither the Sahm rule nor GDP deceleration materialized. Over the second half of 2025 and the first half of 2026, the divergence persists: recession signal extinguished on T10Y3M (positive turn), Sahm rule inactive, LEI in timid recovery since the late-2023 trough. This configuration suggests that the 2022-2024 episode probably constituted an anomaly without complete transmission to the economic cycle, rather than a recession delayed by more than thirty months.

Causal explanation hypotheses for the 2022-2024 anomaly

Three families of hypotheses circulate in research to explain why the 2022-2024 inversion did not produce recession at the expected date. Each carries different operational implications for future signal reading.

The first family, “offsetting fiscal expansion,” attributes the non-recession to the exceptional scale of the U.S. federal deficit. The primary federal deficit remained between 5 percent and 7 percent of GDP over 2022-2024, a level historically associated with wartime or deep-recession periods. The fiscal multiplier estimated for this episode by Brookings Institution and Peterson Institute economists oscillates between 0.7 and 1.2, suggesting that this fiscal expansion added three to six cumulative percentage points to growth over the period — enough to offset the monetary braking transmitted by T10Y3M.

The second family, “post-pandemic excess savings,” attributes resilience to a savings stock accumulated during the pandemic through fiscal transfers (stimulus checks, enhanced unemployment allowances) and forced reduction in consumption. This stock, estimated at between 2,100 and 2,400 billion dollars at the 2021 peak, gradually eroded over 2022-2024 and would have been exhausted by mid-2024 according to Federal Reserve Bank of San Francisco estimates. This erosion could explain a delayed effect of monetary transmission, materializing from 2025 onward — a hypothesis compatible with the conservative reading mentioned above.

The third family, “sectoral subsidy policy,” identifies the Inflation Reduction Act (2022), CHIPS and Science Act (2022), and Infrastructure Investment and Jobs Act (2021) programs as structural stimulus to non-residential investment. Private equipment spending on industrial construction (Bureau of Economic Analysis series on Private Nonresidential Fixed Investment, Manufacturing Structures) doubled in nominal terms between 2021 and 2024, reaching historically high levels. This sectoral dynamic would have supported industrial employment and capital goods demand, partly bypassing the monetary braking transmitted through bank credit conditions.

These three hypotheses are not mutually exclusive — they can coexist and accumulate. Their common implication: T10Y3M remains a valid signal of intentional monetary braking, but its translation into actual recession depends on the coexistence of offsetting fiscal and structural stabilizers. In a regime of prolonged expansionary fiscal policies, transmission lag can lengthen significantly beyond the historical eighteen-month envelope — without invalidating the monetary signal reading.

The absence of a 2023-2025 recession does not disqualify T10Y3M as a signal — it redefines the admissible lag and requires integrating term premium into the quantitative reading of the spread.

- T10Y3M has preceded seven of the eight U.S. recessions since 1968, with a single sustained false positive (1998, interrupted by an emergency Fed intervention).

- The 10-year / 3-month choice results from formal empirical selection (Estrella-Mishkin 1996), confirmed by post-QE reviews (Bauer-Mertens 2018, 2023).

- The causal channel runs through bank net interest margins, observable via the Senior Loan Officer Opinion Survey with a typical lag of two to four quarters after inversion.

- The 2022-2024 inversion (626 days, depth -189 basis points) is the longest since Volcker; its final un-inversion in December 2024 marks the episode’s end without an NBER-dated recession as of May 2026.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…

Inverted Yield Curve: Reading a Regime Signal Without Immediate Effect

The inverted yield curve operates as a regime signal, not a timing tool. Its lagged effects are constitutive…