T10YIE Meaning: What Breakeven Inflation Is and How It Is Calculated

T10YIE is the FRED ticker for a daily subtraction between two Treasury yields. Understanding what that subtraction actually measures — and what it does not — is the prerequisite to any macro reading of the figure.

TL;DR

Bond arbitrage between nominal Treasuries and TIPS sets the equilibrium inflation that T10YIE reports, an estimate two premia push 30 to 60 basis points away from pure expectations.

- The liquidity premium runs 10 to 30 basis points; the inflation risk premium, extracted by the New York Fed's ACM model, ranged 25 to 60 basis points over 2003-2025.

- A 2.3% breakeven means different things in 2014 and 2024, which is why central-bank staff report the model-extracted expectations component alongside the raw figure.

This article sets the strict technical definition: series origin, formula, two parasitic premia, and the distinction between breakeven and realized inflation. For the full macro reading, see T10YIE as the reference measure.

1. The FRED T10YIE series: origin, publication, temporal scope

T10YIE is the ticker of the FRED “10-Year Breakeven Inflation Rate” series, published daily by the Federal Reserve Bank of St. Louis. This articulation appears in the mechanics of the inflation breakeven. The first observation dates from January 2, 2003, which means the series now covers more than 23 years of continuous daily-frequency history. Publication occurs with one business day of lag: values available on the morning of day D reflect yields observed at close of day D-1, after the Treasury Department’s par yield curve calculation.

The series carries an official name — 10-Year Breakeven Inflation Rate — and a ticker name — T10YIE. Both designations refer strictly to the same quantity: the yield gap between nominal Treasury and TIPS at 10-year residual maturity. Before 2003, no equivalent series existed, because the TIPS market — launched in January 1997 — remained too illiquid to generate stable pricing. The Federal Reserve waited nearly six years before officially publishing the series, the time needed for traded volumes to reach a threshold of methodological reliability. Source data: the breakeven inflation series.

The temporal scope of the series matters for its interpretation. Covering 2003-2026 includes two decades marked by major macroeconomic shocks: the 2008 financial crisis, the 2014-2015 European deflation, the 2014 oil shock, the 2020 pandemic, the 2021-2024 post-COVID inflation cycle. This breadth makes the series analytically rich, but it does not exempt from comparing with retrospective estimates over longer periods — those that the Cleveland Fed publishes going back to the 1960s from structural models.

FRED publication is systematically updated at end of New York session, making it the reference indicator not only for US markets but for all global macro desks that depend on the dollar as the anchor currency. European, Asian, and emerging-market central bankers track T10YIE as an input to their own reading of global financial conditions, which amplifies its reach well beyond the Fed framework alone.

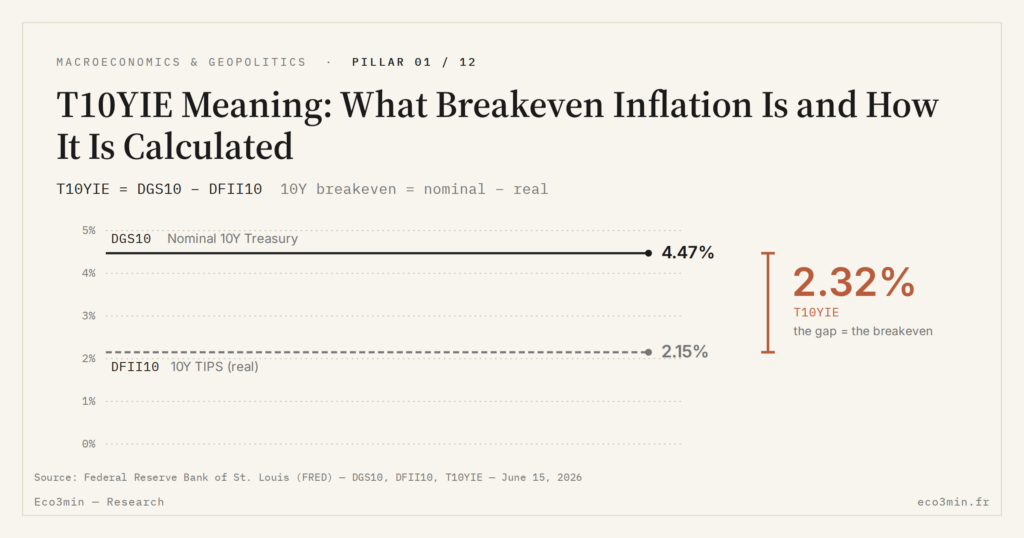

2. The calculation formula: DGS10 minus DFII10 and its assumptions

Mathematically, T10YIE = DGS10 − DFII10. DGS10 is the constant-maturity yield of the 10-year nominal Treasury, a series also published by FRED from the Treasury’s par yield curves. DFII10 is the constant-maturity yield of the 10-year TIPS, calculated under the same methodology. This construction guarantees that the two subtracted yields correspond to the same calculation date and exactly the same residual maturity, which is not the case if individual bonds are taken with their own maturity dates. Related reading: the copper-gold signal mapped against bond yields.

The economic logic of this subtraction rests on a no-arbitrage condition. A nominal investor buys DGS10 and earns a certain nominal yield. A TIPS investor buys DFII10 plus realized CPI inflation over the decade. In equilibrium, the average inflation expected by markets must be such that the two instruments offer the same expected nominal yield — otherwise arbitrage would shift prices until equality is restored. It is this equilibrium average inflation that is referred to as T10YIE and labeled breakeven.

The calculation assumes three conditions that are not always rigorously satisfied. First, the indexation of TIPS to the non-seasonally-adjusted CPI-U — not any other price index. Second, the absence of significant liquidity gap between the two segments — a condition relaxed in practice, as the next section will clarify. Third, the absence of an inflation risk premium that arbitrageurs would demand to bear the risk of divergence between realized and expected inflation. These three assumptions rarely holding simultaneously, T10YIE is an approximation of expectations, not their pure measure.

The weighted average reflected by T10YIE is not an arithmetic average of expected annual inflations. It is technically a geometric average weighted by the effective duration of the two instruments, which implies that the early years carry more weight than the later ones in the figure. For a fine decomposition of the 5Y vs 10Y expectation slope, see the nominal versus TIPS yield decomposition; the present article stays on the reading of the single T10YIE figure.

3. The two parasitic premia: liquidity and inflation risk

The raw breakeven does not exactly equal inflation expectations. Two parasitic components are constantly blended in, generally of small magnitude but sometimes significant.

The first component is the TIPS liquidity premium. The nominal Treasury market is the most liquid in the world, with an average daily volume above 600 billion dollars according to the Treasury Bulletin (Q4 2025). The TIPS market, despite a 2.2 trillion dollar outstanding amount at the same date, remains significantly less liquid — its average daily volume runs around 25 billion dollars. This difference translates into a TIPS yield slightly higher than it should be in theory, hence a mechanically underestimated breakeven. The liquidity premium typically oscillates between 10 and 30 basis points in normal regime and can widen to 50 basis points during stress episodes.

The second component is the inflation risk premium. Holding a nominal Treasury exposes to inflation surprise risk that erodes real yield; arbitrageurs demand compensation for that risk, which adds to expectations themselves. This premium is harder to isolate because it does not appear separately in any quoted market — it must be extracted by factor models. According to the ACM decomposition published by the New York Fed (Adrian, Crump, Moench, 2024), this premium has oscillated between 25 and 60 basis points over 2003-2025, with phases close to zero (2009-2015) and phases above 50 basis points (2022-2024).

The direction of the two premia can offset or accumulate. In a TIPS-liquidity-stress regime, T10YIE is biased downward by the liquidity premium but simultaneously biased upward by the inflation risk premium. When the two premia move in the same direction — typically coming out of a crisis — the total bias can reach 50 to 80 basis points. For daily reading, these nuances do not matter; for structural macro reading that calibrates monetary policy, they are decisive. For a shorter primer with worked examples, see also a shorter primer on breakeven rates.

A practical consequence for the analyst: any T10YIE reading at a single point in time should be qualified by the regime under which it is observed. The same 2.3% breakeven in early 2014 — high TIPS liquidity premium, low inflation risk premium — does not carry the same informational content as 2.3% in late 2024, where the premium structure has shifted materially. Treating the figure as if it were regime-invariant is the single most common error in non-specialist commentary, and it is the analytical reason why central-bank staff routinely report not just the raw breakeven but the model-extracted pure expectations component alongside.

4. What T10YIE is not: the confusion with an inflation forecast

The main confusion surrounds the epistemic status of the figure. T10YIE is not an inflation forecast in the sense an economist would publish a forecast: it is an implicit projection resulting from bond arbitrage among thousands of market participants. This difference in nature has two practical consequences.

First, T10YIE has no vocation to be right in the statistical sense. The 10-year breakeven observed in April 2022 indicated an average anticipated inflation of 2.99% over the following decade. Saying whether that number will be realized or not in terms of cumulative CPI 2022-2032 has little analytical interest: T10YIE measures what the market thought at a given moment, and what changes or does not change afterwards will reflect the evolution of the information flow, shocks, and monetary policies. The relevance of a breakeven is not in its match with future realized inflation but in the gap to the Fed target and in the regime reading. Further reading: the macro-financial implications of inflation.

Second, T10YIE says nothing directly about current realized inflation. The CPI inflation published by the Bureau of Labor Statistics each month measures the present and the recent past; T10YIE measures an average anticipated over the next ten years. These two quantities can diverge considerably and it is precisely this divergence that produces the macro signal. For an analysis of this divergence, see reading the T10YIE signal in practice. The present article stays on the definition.

This distinction is moreover at the heart of the very function of the sub-pillar beyond published CPI: understanding that inflation expectations, measured by T10YIE and other indicators, are a macro quantity distinct from the inflation published monthly, and that they deserve their own monitoring. The breakeven is in some way the forward counterpart of CPI: one looks backward, the other projects forward, and the gap between the two is not an anomaly but information.

Treating T10YIE as a 10-year market inflation forecast. This is inaccurate on two counts: it is an implicit projection rather than an asserted forecast, and the raw figure embeds an inflation risk premium and is netted of a TIPS liquidity premium — together 30 to 60 basis points of gap from pure expectations depending on the regime. For rigorous reading, systematically cross-check T10YIE with SPF and Michigan surveys and the inflation swap spread.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Monetary Tightening: How Central Banks Are Reshaping Financial Markets

After more than a decade of ultra-accommodative policy, monetary tightening has reintroduced the real cost of capital as…

Hidden Unemployment: Reading the Real Labor Market in 2026

Headline unemployment is stabilizing while broad underemployment still runs above pre-2020 levels. Reading the gap between official rates…

2026 Economic Outlook: Key Trade-Offs After the End of Cheap Money

2026 ushers in a more constrained macro regime where real rates stay positive, fiscal space narrows and geoeconomic…