VIX meaning, VIXCLS ticker, calculation from S&P 500 options and CBOE publication

The VIX is calculated from a basket of SPX options through a variance swap formula published by the CBOE in 2003. The precise mechanics — inverse-square weighting of strikes, truncation, 30-day interpolation — explain why the VIX behaves the way it does.

TL;DR

The VIX is the price of a 30-day implied variance swap on 1/K²-weighted SPX options, recomputed every 15 seconds; its daily close is the VIXCLS series, backfilled to 1990.

- Because it reflects expectations rather than past returns, the VIX can move while the S&P 500 stays flat, on shifting option premiums alone ahead of an FOMC or a geopolitical shock.

- A structural risk premium keeps it averaging 3.2 points above the subsequent 30-day realised volatility over 1990-2025: option sellers earn more than the risk actually anticipated.

- Stopping the calculation at the first two strikes without a bid makes the index sensitive to options-market depth: a liquidity retraction on far OTM puts can compress the VIX.

The official methodology is documented but rarely discussed in detail. What follows reconstructs the four calculation steps, their practical consequences for daily reading of the VIXCLS ticker, and the minor differences between the intraday index and the FRED series.

1. The principle: an implied variance swap, not historical volatility

The VIX 2003 methodology, designed by the CBOE in collaboration with Goldman Sachs, rests on a precise theoretical result: the expected future variance of an underlying can be replicated by a static portfolio of put and call options at different strikes, weighted by 1/K². The formula comes from the variance swap literature (Demeterfi et al., 1999) and applies to any underlying with a sufficiently liquid OTM options market.

Concretely, the VIX does not measure past S&P 500 volatility (which is realised volatility, computed directly from daily returns), but the volatility the options market anticipates over the next 30 days. The distinction is central: the VIX is a price derived from an active OTC market, not an indicator computed on historical series. Its value at any moment reflects the equilibrium between buyers and sellers of SPX options, not a statistical calculation on the past of the S&P 500. Related material: how tracking and cost differ across S&P 500 ETFs.

This property explains two characteristic behaviours of the VIX. First: it can move without any change in the S&P 500. Expectations shift (an upcoming FOMC release, a geopolitical event), option premiums adjust, the VIX reacts. Second: it embeds a structural risk premium — option sellers demand compensation beyond the anticipated real risk — which explains why the VIX has averaged 3.2 points above the subsequent 30-day realised volatility over 1990-2025.

2. The official CBOE formula in four steps

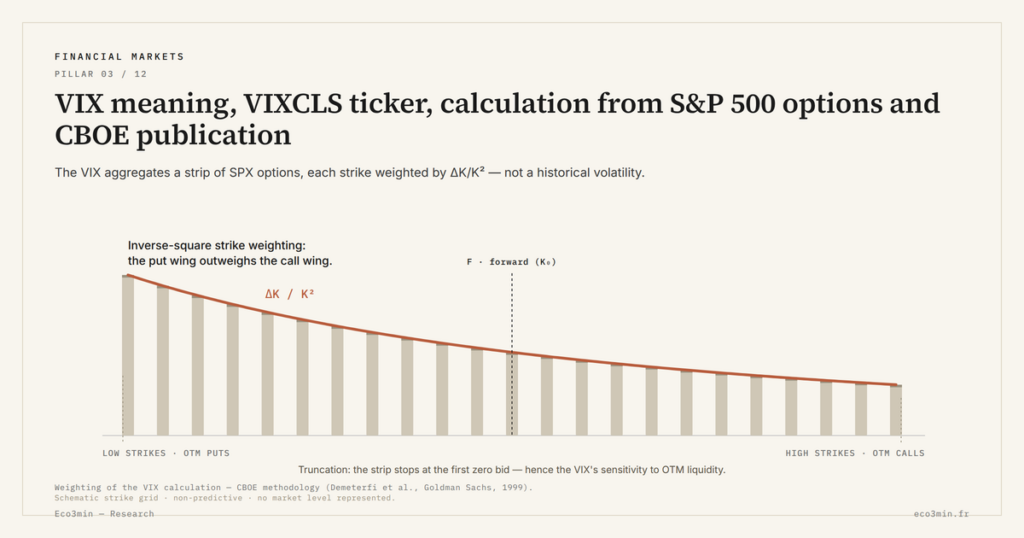

The complete formula, as published in the CBOE VIX White Paper, reads: σ² = (2/T) × Σ (ΔKᵢ / Kᵢ²) × e^(R·T) × Q(Kᵢ) − (1/T) × (F/K₀ − 1)², where T is maturity in years, Kᵢ are strikes, ΔKᵢ the spacing between consecutive strikes, R the risk-free rate, Q(Kᵢ) the option mid-price at strike Kᵢ, F the implied forward, and K₀ the strike just below F.

Four steps structure this calculation. The first identifies the two SPX option expirations bracketing the 30-day horizon: a near-term expiration (T₁) of more than 7 days and a next-term expiration (T₂) of less than 35 days. The second selects eligible strikes for each expiration: all OTM options are retained (puts below the forward F, calls above), stopping as soon as two consecutive strikes have a zero bid. The third computes the implied variance σ₁² and σ₂² for each expiration via the formula above. The fourth linearly interpolates between σ₁² and σ₂² to obtain a variance at exactly 30 days, whose annualised square root gives the VIX.

The published result, multiplied by 100 and displayed to two decimals, is the number read under the VIX ticker. This mechanism runs continuously during SPX market hours, recomputed every fifteen seconds by the CBOE from the most recent bid-ask quotes on the underlying options.

3. The inputs: which options enter the calculation

The CBOE uses standard SPX options expiring monthly (third Friday of the month) and weekly options (SPXW). Since 2014, adding SPXW improved 30-day interpolation precision by narrowing the gap between the two bracket expirations. Before 2014, the two monthly expirations used could be far apart (sometimes 25 and 55 days), making interpolation less precise.

The weight of each strike in the calculation follows the ΔKᵢ / Kᵢ² formula. This 1/K² weighting makes strikes near spot largely dominate the calculation, while distant strikes contribute marginally — yet their contribution is not zero, especially when put skew is stretched. A strike at -20% of spot can contribute significantly to the VIX during stress periods, while its contribution is near zero in normal regimes.

Truncation is the most delicate step. The calculation stops on the put side as soon as two consecutive strikes below have a zero bid, and symmetrically on the call side. This stopping rule makes the VIX mechanically sensitive to the depth of the options market: when liquidity retracts on deep OTM puts, truncation moves closer to spot, and the VIX can underestimate the volatility actors would have been willing to pay on distant strikes had a quoted market existed.

4. The 30-day interpolation and daily slide

Interpolation between the two expirations is linear in variance, not in volatility. The formula is σ²(30d) = w₁ × σ₁² + w₂ × σ₂², where weights w₁ and w₂ are calibrated to land exactly on 30 calendar days (not 30 trading days). The annualised square root then gives the published VIX.

A minor but real consequence: the VIX slides daily not only as a function of option prices, but also as a function of time passing. Each day, T₁ approaches, and when T₁ drops below 7 days, the CBOE rolls to the next expiration. These rolls introduce very slight discontinuities, but the mechanism is robust enough in practice not to disrupt daily reading.

This construction also has a structural side effect: the VIX is blind to risks beyond 30 days. To capture expectations at 90 days, 180 days or one year, the CBOE publishes complementary indices (VIX9D for 9 days, VIX3M for 90 days, VIX6M for 180 days), and CFE VIX futures allow tracing a full forward curve. For detailed reading of this curve, see the forward dimension via CFE VIX futures.

5. The VIX variants published by the CBOE

The family of VIX indices published by the CBOE includes several variants that mainstream commentary sometimes conflates with the main VIX. Knowing they exist helps locate VIXCLS within its ecosystem.

On the time horizon side, four indices coexist. VIX9D applies exactly the same 2003 methodology but on a 9 calendar-day horizon: it captures very short-term expectations, especially around imminent macro or FOMC releases. VIX3M (90 days) and VIX6M (180 days) extend the horizon to the quarter and the semester, allowing a forward read of equity volatility. CFE VIX futures, tradable on 9 consecutive monthly expirations, complete the picture by tracing an implied volatility curve out to one year.

On the neighbouring indicator side, three are particularly useful. VXO, the original Whaley 1993 index, remains published for comparative purposes and helps evaluate the impact of the 2003 methodological break on historical levels. VVIX (volatility of volatility) measures the implied volatility of options on the VIX itself: it signals expectations of a spike on the VIX and is one of the leading indicators tracked by vol arbitrage desks. The SKEW index (published since 2010) measures the relative pricing of deep OTM puts — the put-call asymmetry of the SPX options market: an elevated SKEW indicates investors pay heavily for crash protection regardless of VIX level.

These indicators are not redundant. A low VIX with an elevated VVIX signals a complacent market that is nervous about its own volatility — a configuration observed several times since 2024. A low VIX with an elevated SKEW indicates investors are not paying for 30-day coverage but are paying for crash protection — a configuration documented in 2017 before Volmageddon. A related perspective: our mapping of systemic risk metrics.

6. From intraday index to the VIXCLS series

The VIXCLS ticker published by FRED is the close version of the VIX: daily value at session close, 4:05 PM ET, as fixed by the CBOE. The series covers from 2 January 1990, with backfilling of the 2003 methodology over the 1990-2002 period performed by the CBOE and published for historical comparison. The full daily history is available through the VIXCLS series page on Eco3min for empirical work and regime analysis.

Three precisions on VIXCLS. First: the published value slightly differs from the last observed intraday print, because the official close is calculated on the most recent bid-ask before 4:00 PM, while intraday uses continuous prices. The gap is usually a few hundredths of a point. Second: VIXCLS does not reflect the extended session (after-hours), even though some platforms publish an intraday VIX that may move after 4:00 PM. Third: the VIXCLS series is occasionally revised by the CBOE to correct quote errors, but these revisions are rare and limited to isolated days.

To understand what each daily print actually measures, the complete analysis of the VIX as an equity stress indicator places the calculation mechanics in their interpretive context: three components, five historical regimes, institutional reading. This article deliberately confines itself to mechanics. The VIXCLS series also serves as reference for cyclical analyses and regime-by-regime comparisons documented within Eco3min’s full mapping of market regimes and financial dynamics.

- The VIX is an implied variance swap calculated on a basket of SPX options at different strikes, weighted by 1/K², not a historical S&P 500 volatility.

- The 2003 methodology (revised in 2014) selects OTM options from the two bracket expirations around 30 days and linearly interpolates in variance to anchor a 30 calendar-day horizon.

- Truncation at the first two strikes without a bid makes the calculation mechanically sensitive to options market depth; a retraction of OTM liquidity can artificially compress the VIX.

- VIXCLS (FRED) is the daily close version, backfilled to 1990 using the new methodology to allow cross-regime historical comparison.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Euro Below Parity in 2022: What Parity Means

In September 2022, the euro fell below parity with the dollar, to around 0.95, a low not seen…

Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…