VIX backwardation, contango and the volatility futures term structure

The VIX curve articulates the spot index and nine CFE VIX futures expirations. Its shape — contango or backwardation — provides a regime signal distinct from the spot level and historically more robust for identifying acute stress phases.

TL;DR

The shape of the VIX futures curve signals stress better than its level: 21 of 22 backwardation episodes since 2004 preceded an S&P 500 drawdown above 5% within a month.

- Contango, the upward-sloping curve, dominates roughly 85% of trading days from 1990 to 2025; total backwardation appears on about 5% of days and never lasts more than a few weeks.

- Persistent contango imposes a negative roll yield: over 2009-2018 VXX lost about 60% per year despite a stable spot VIX, while the inverse XIV gained around 50% per year until its February 2018 implosion.

- When the curve inverts the roll yield reverses: long-vol ETPs such as VXX gained roughly 180% in three weeks during March 2020, well beyond the spot VIX move.

- At end-April 2026 the curve sits in compressed contango, the VX6/VX1 slope averaging 1.062 against a 1.15-1.20 historical norm.

Contango dominates 85% of trading days from 1990 to 2025; backwardation, rarer, has preceded 100% of major drawdowns over the period. What follows reconstructs the curve mechanics, its historical configurations, and the structural impact on volatility ETPs.

1. The VIX curve: a forward instrument, not a tradable underlying

Spot VIX is not directly tradable. Market participants seeking to buy or sell equity volatility use VIX futures, launched in March 2004 by the CBOE Futures Exchange (CFE). Each contract is on the expected VIX level at a future expiration; the market continuously quotes nine consecutive monthly expirations (VX1 to VX9), from the current month to a twelve-month horizon. A related dataset: The implied-volatility record.

The curve formed by these nine expirations is not a simple expectation. It reflects the equilibrium between buyers (institutions hedging against a future volatility spike) and sellers (systematic players harvesting the structural risk premium). The price of a VIX future at expiration T₁ thus embeds both the expected VIX value at T₁ and the risk premium sellers demand for carrying spike risk.

Three conventions are needed to read the curve correctly. First: VIX futures settle in cash on the value of the Special Opening Quotation (SOQ) of the VIX on the morning of the third Wednesday of the expiration month — not on the prior day’s close. This particularity generates sometimes substantial fixing effects. Second: contracts expire sequentially, mechanically rolling the curve leftward at each monthly expiration. Third: liquidity decreases with maturity; VX1 and VX2 concentrate 75% of volume, and beyond VX5 bid-ask spreads can widen materially.

2. Contango and backwardation: definitions and frequency

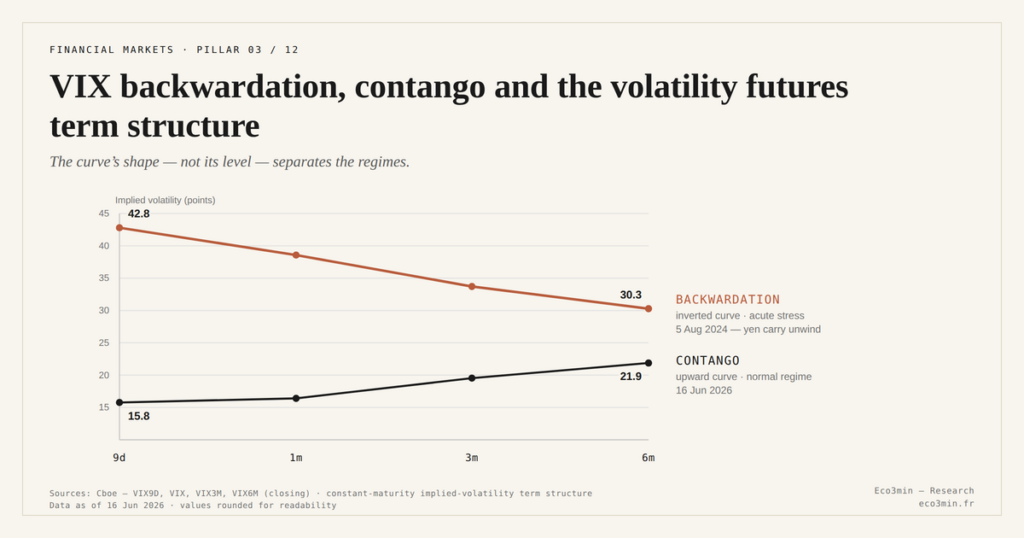

When the curve is upward-sloping — spot VIX

When the curve is downward-sloping — spot VIX > VX1 > VX2 > … —, the regime is called backwardation. This regime is rare and associated with acute stress phases: spot VIX leaps beyond the levels the market anticipates on longer horizons, signalling that participants assess the shock as transitory. Backwardation can be total (entire curve inverted) or partial (only spot VIX > VX1, with the rest of the curve remaining in contango).

Over the 1990-2025 period (using VIX futures from 2004 onward), contango dominates roughly 85% of trading days per Eco3min calculations on CFE and FRED data. The remaining 15% split between partial backwardation (10%) and total backwardation (5%). No total backwardation lasts more than a few weeks: the prolonged episodes correspond to phases of massive repricing such as the GFC (October 2008 to March 2009), COVID (March-April 2020), or the yen carry trade unwind (5-12 August 2024). Related Q&A: our breakdown of the carry trade.

3. Reading the slope: what curve shape says

Several slope metrics are tracked by volatility desks. The simplest: the VX1 / spot VIX ratio. In normal contango, this ratio sits between 1.04 and 1.08 — VX1 priced 4 to 8% above spot. In backwardation, the ratio drops below 1.00; the extreme episodes (March 2020, August 2024) saw this ratio fall to 0.75-0.80, meaning spot 25-30% above VX1. The detail is worked through in the assumptions that mislead investors on commodities and gold. A parallel read: our analysis of investing in commodities.

A second metric, more informative: the VX2 / VX1 ratio. When this slope flattens (moving from 1.03-1.05 to 1.01-1.02) without curve inversion, it is an early tension signal. This pattern preceded some peaks — notably February 2018 and August 2024 — by one to two weeks. The VX2/VX1 slope flattening is one of the leading indicators tracked by volatility funds. This finding is put in perspective by the stress-signal layer of market regimes.

A third dimension: the VX1 vs VX6 slope (current month vs six months). A gap below 5% in contango (instead of the usual 15-25%) signals structural compression that may indicate, depending on context, either a new normal or a latent stress accumulation. This slope averages 6% over 2024-2025, a low level in historical comparison. The 2023-2026 volatility compression phase documents this joint spot + curve compression.

4. Backwardation: historical signal of acute stress

Over 2004-2025, twenty-two episodes of total backwardation have been observed on the VIX curve per Eco3min counts. Twenty-one of them coincide with an S&P 500 drawdown above 5% within the next thirty days. The atypical case (June 2013, partial taper tantrum) saw a brief backwardation without a major S&P 500 drawdown.

Three episodes warrant separate commentary. October 2008: backwardation set in on 7 October 2008 (day after the House rejected TARP) and persisted until end-November. During this window, the S&P 500 lost an additional 30%. Backwardation returned briefly in February-March 2009 before the equity bottom formed. February 2018: backwardation surfaced on 5 February 2018 (Volmageddon day) and resolved in three weeks, after the implosion of several short-vol ETNs. The S&P 500 lost 10% in this window then rebounded. March 2020: extreme backwardation from 9 to 27 March, a period during which the S&P 500 lost 23% before bottoming on 23 March.

The backwardation signal is therefore historically robust for identifying acute stress phases, but it is neither a precise timing signal (backwardation can persist several weeks before the bottom) nor a return-to-normal signal (the return to contango does not mechanically mark the end of the drawdown). It is rather a regime indicator: it confirms entry into a repricing phase without specifying when it will end. For the complete mapping of major spike episodes, see the empirical catalog of VIX spikes 1990-2026.

5. Roll yield and consequences for volatility ETPs

The curve shape has a mechanical consequence on ETFs and ETNs replicating VIX futures. These products — VXX, VIXY, UVXY (long volatility) or SVXY (inverse) — must roll their positions monthly to maintain exposure. Roll yield is the spread between the price of the contract sold (near-term) and the one bought (next term).

In contango, roll yield is negative for long-volatility ETPs: they sell at the low price (VX1) and buy at the high price (VX2), mechanically losing the slope at each renewal. Over 2009-2018, VXX lost on average 60% per year despite a relatively stable spot VIX, entirely through negative roll yield. Symmetrically, the inverse XIV gained 50% per year by capturing the contango slope — until its February 2018 implosion in sudden backwardation.

In backwardation, roll yield inverts: long-volatility ETPs gain at each roll by selling high (elevated VX1) and buying lower (lower VX2). This dynamic explains why long-vol ETPs like VXX can gain 200-400% during crashes (March 2020: +180% in three weeks), beyond the simple VIX increase. The complete series of historical equity stress cases documents this mechanism episode by episode.

6. State of the 2024-2026 curve regime

Since the August 2024 peak, the VIX curve has been in persistent contango. The 18-month average VX1/VIX ratio stands at 1.063, slightly below the 2004-2024 historical average of 1.074. The VX6/VX1 slope is at 1.062, against a historical average of 1.15-1.20. The curve compression is consistent with spot VIX compression and supports the two competing theses documented in the general analytical framework around the VIX and its regimes: 0DTE-driven new normal or artificial suppression through structured short-volatility positions.

A monitoring signal tracked by desks: a flip of the VX2/VX1 slope below 1.00 (partial backwardation) without identified shock on spot would be one of the first signs of latent destabilisation. This flip is not observed at end-April 2026; contango remains robust across the entire curve.

- The VIX curve articulates spot VIX and 9 CFE VIX futures; its shape — contango or backwardation — provides a regime signal distinct from the spot VIX level.

- Contango dominates roughly 85% of trading days from 1990 to 2025; backwardation is rare and has preceded 21 of 22 S&P 500 drawdowns above 5% over 2004-2025.

- The negative roll yield imposed by persistent contango explains why long-volatility ETPs (VXX, UVXY) lose on average 50-60% per year despite stable spot VIX.

- The 2024-2026 curve is in persistent but compressed contango: VX6/VX1 at 1.062 vs historical average 1.15-1.20, consistent with simultaneous spot VIX compression.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Euro Below Parity in 2022: What Parity Means

In September 2022, the euro fell below parity with the dollar, to around 0.95, a low not seen…

Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…