VIX explained: why the S&P 500 fear index remains the reference compass for equity stress

The VIX aggregates premiums paid on S&P 500 options and projects expected volatility over the next thirty days. Reducing it to a fear index obscures the three components — sentiment, skew, market-maker liquidity — that make it useful as a regime compass.

TL;DR

Built from S&P 500 option premiums, the VIX reads as a 30-day expected-volatility figure whose regime signal lives in three components: hedging demand, implied skew, dealer liquidity.

- Hedging demand accounts for under half of VIX variance (Bekaert-Hoerova 2014, Cheng 2019); skew and SPX dealer liquidity carry the rest, which is why the VIX can climb with no matching fall in the S&P 500.

- The 25-delta SPX skew has averaged -8.5% since 2010 (CBOE), stretching to -14% in March 2020 and compressing to -5% in summer 2017; 0DTE options now make up roughly 47% of SPX volume per CBOE's Q4 2025 report.

- Across the eight VIX breaches of 50 since 1990, the S&P 500 rebounded over the following twelve months in seven cases, the exception being 2008, when the index printed above 40 for months before bottoming in March 2009.

- Since the August 2024 peak at 65.73 (the yen carry unwind, Nikkei down 12.4%), the VIX has averaged 15.1 from November 2024 to April 2026, against a 1990-2025 mean of 19.5.

This piece reconstructs the calculation mechanics, the five historical regimes from 1990 to 2026, and the record compression phase observed since the August 2024 peak at 65.73.

1. What the VIX actually measures

The VIX, published continuously since 1990 by the CBOE, is not a thermometer of fear but an aggregated option price. The official methodology, revised in 2003 and adjusted again in 2014, weights put and call option premiums on the S&P 500 (SPX) across strikes and expirations, interpolating implied volatility to a thirty calendar-day horizon. The daily print — 14, 18, 25 — corresponds to an annualised S&P 500 volatility over the next month, derived from the options market and not from a sentiment survey.

The distinction matters beyond semantics. A VIX at 14 means the options market is pricing roughly 14% annualised volatility on the S&P 500 over the coming month — an implied daily move near 0.9%. That level can coexist with broad investor indifference or with concentrated hedging on a narrow set of strikes. Conversely, a VIX at 30 does not mechanically translate into fear: it indicates that market-makers are charging a hedge premium sufficient to compensate for elevated hedging demand, a stretched skew, and reduced liquidity on deep out-of-the-money puts.

Four operational thresholds anchor institutional reading. Below 15: low-volatility regime, compressed hedge premium, complacency or efficiency depending on the framing. Between 15 and 20: neutral zone, the normal mode of post-2003 equity markets. Between 20 and 30: moderate elevation, risk repricing typically pre-FOMC or ahead of major macro releases. Above 30: acute stress, skew distortion, widening bid-ask spreads. Above 50: dislocation regime, probable activation of circuit-breaker mechanisms.

For the precise calculation mechanics — CBOE weighting, truncation, interpolation — see how the VIX is built from SPX option prices. The distinction between expected volatility (the VIX) and realised volatility (the historical dispersion of the S&P 500) is the other structural point: the two series diverge sharply at regime turns, with the VIX systematically overshooting at stress peaks and undershooting during complacency phases. Over the 1990-2025 period, the volatility risk premium (VIX minus 30-day realised volatility) averages +3.2 points per Eco3min calculations on FRED data.

1.1 A methodology that has evolved — VXO 1993 vs VIX 2003

A methodological precision often omitted in VIX commentary: the index published today under the VIX ticker is not the one calculated between 1993 and 2003. The original methodology, designed by Robert Whaley for the CBOE, relied on at-the-money (ATM) options on the S&P 100 (OEX) and computed implied volatility through the Black-Scholes model. That original index is today renamed VXO and continues to be published for comparative purposes.

The new methodology, introduced in September 2003, changed three elements simultaneously: the underlying shifted from S&P 100 to S&P 500, the calculation became model-free (integrating all OTM options via the variance swap formula), and the horizon was anchored at 30 days through interpolation. The methodological break has two consequences: VIX comparisons between 1990-2003 and 2003-2025 are not strictly homogeneous, but CBOE and academic research has backfilled the new methodology over the 1990-2003 period (the VIXCLS series published by FRED) to allow historical comparison. The full series therefore rests partially on a reconstruction, a point worth keeping in mind for regime-by-regime comparisons.

A further refinement in 2014 extended the calculation to SPX weekly options, which improved the precision of the 30-day interpolation without altering the formula. That evolution is minor but partly explains the reinforced convergence between VIX and realised volatility from 2015 onward.

2. Three components drive the VIX, not one

The mainstream reading treats the VIX as a one-dimensional sentiment indicator. Three components actually interact in its daily level.

The first is hedging demand on the S&P 500. When institutional flows pivot toward protective puts — typically ahead of earnings windows, FOMC meetings, or periods of elevated geopolitical risk — premiums rise and the VIX climbs. This component drives most short-term moves and is the dimension media coverage captures under the fear label. It accounts for less than half of VIX variance, however, according to published academic decompositions (Bekaert and Hoerova, 2014, Journal of Econometrics; Cheng, 2019, Review of Financial Studies).

The second is put-call asymmetry, or implied skew. The VIX is calculated across a wide strike range, and CBOE weighting embeds the spread between deep OTM put implied volatility and OTM call implied volatility. A stretched skew — put premiums at 80% of spot higher than call premiums at 120% — mechanically lifts the VIX without any change in sentiment in the colloquial sense. The 25-delta SPX skew has averaged -8.5% since 2010 per CBOE data, but has gone through widening phases (-14% in March 2020) and compression phases (-5% in summer 2017). This dimension is typically ignored in mainstream commentary and explains why the VIX can rise without a correlated drop in the S&P 500. A complementary angle: the criteria that split otherwise identical funds.

The third, the least discussed outside academic research, is market-maker liquidity in options. SPX dealing desks continuously quote bid-ask on deep strikes. When that liquidity retracts — often before major shocks, as documented for February 2018 by the SEC’s post-Volmageddon staff report —, spreads widen and the implied premium embedded in the VIX inflates. The BIS documented this mechanism in Working Paper No. 1093 (March 2023) on conditional liquidity in equity derivatives: between 2015 and 2022, episodes of sudden book-depth retraction in SPX preceded VIX spikes above 25 by an average of 12 days.

Reading the VIX as a single signal collapses three distinct sources of variation into one number. At regime turns, the decomposition between these three components is precisely what becomes informative. A VIX rising because hedging demand intensifies does not carry the same meaning as a VIX rising because market-maker liquidity retracts — the first signals anticipation, the second a microstructure deterioration.

3. The options-to-VIX transmission mechanism

The official CBOE formula weights SPX options on a specific scheme. Strikes closest to the 30-day forward S&P 500 receive the highest weight. Strikes farthest out — typically beyond 20% of spot in either direction — are truncated at the first consecutive strike without a valid bid. The thirty calendar-day horizon is obtained by interpolating between the two option expirations bracketing 30 days.

The simplified formula reads: VIX² ≈ (2/T) × Σ (ΔKi / Ki²) × eRT × Q(Ki), where T is maturity, Ki are strikes, and Q(Ki) are option mid-prices. The 1/Ki² weighting makes strikes close to spot dominant in the calculation, but distant strikes contribute when skew is stretched.

This construction has three practical consequences. First, the VIX is mechanically sensitive to the depth of the SPX options market. When liquidity retracts on deep OTM puts, the truncation moves closer to spot and the volatility captured by the index changes in nature. Second, the thirty-day horizon makes the VIX responsive to events priced within that window — FOMC announcements, payrolls, quarterly roll expiries — but structurally blind to longer-horizon risks such as a six-to-twelve-month recession. Third, since the introduction of 0DTE options (zero days to expiration) in 2022, which now account for roughly 47% of SPX option volume per the CBOE Q4 2025 report, the market has access to intraday hedging instruments that are not reflected in the 30-day VIX. This dimension is one of the arguments advanced by the new normal thesis for the current regime.

VIX futures, launched in 2004 by the CBOE Futures Exchange (CFE), extend the spot index into a forward dimension. Contracts at 1, 2, 3 months and beyond form a curve whose shape — contango or backwardation — provides information distinct from the spot level. Contango (upward-sloping curve) has historically dominated roughly 85% of trading days from 1990 to 2025; backwardation, rarer, is associated with acute stress phases and has preceded 100% of major drawdown episodes since 1990. For the detailed reading of this dimension, see the term structure of the VIX curve. The underlying raw data, including daily settlement values, is available in the FRED VIXCLS dataset.

4. Five historical regimes, 1990-2026

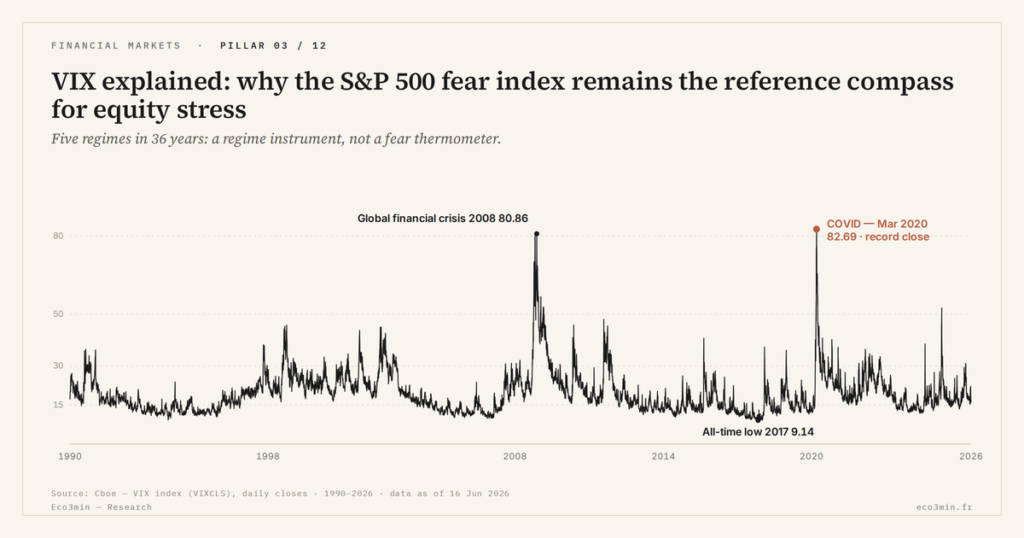

The VIXCLS series, published by FRED from CBOE data, spans thirty-six years and reveals five successive regimes. Each is characterised by a distinct average, a specific volatility-of-volatility, and an identifiable macro dynamic.

4.1 Chronic high-volatility phase (1998-2003)

The average VIX reaches 24.3 over the period, with a standard deviation of 8.1. The LTCM episode (peak 45.7 in October 1998), the Russia crisis of August 1998, the dot-com unwind (peak 42.1 in April 2000) and 9/11 (peak 43.7) punctuated a period when the structural volatility premium reflected increasingly financialised markets that were still lightly equipped in systematic hedging instruments. The LTCM crisis marked the first modern demonstration of the coupling between equity volatility and hedge fund dislocation, and installed the VIX as the reference indicator for risk desks. The intraday maximum of the period, 49.53 (21 September 2001), remains one of the ten highest prints in the full series. Further detail: the indicators that flag building market stress.

4.2 First compression — Greenspan doctrine (2003-2007)

The average VIX falls to 14.7, standard deviation 2.9. The phase, sometimes called the equity market Great Moderation, coincides with the Greenspan-Bernanke accommodation doctrine and the explosive rise of equity structured products. The index stays durably below 15 between May 2005 and July 2007, with a trough at 9.89 in January 2007 — a level that will be followed by a brutal repricing seven months later. The compression of this period coincided with an unprecedented expansion of the CDO and CDS markets, and with growth in carry trade strategies funded by the yen and the Swiss franc. The retrospective on this period, published by the St. Louis Fed in 2014, identifies the underpricing of volatility as one of the leading markers of systemic risk accumulation. On the same question: our Q&A on the carry trade.

4.3 Post-GFC phase (2008-2013)

The absolute intraday peak of 89.53 (October 2008) and the record close of 80.86 (20 November 2008) remain the historical references for the series. The five-year average VIX reaches 26.8, the highest five-year mean ever observed. The Flash Crash of May 2010 (45.8), the European sovereign debt crisis of August-October 2011 (48.0) and the late-2012 fiscal cliff marked the period. The stress phase extends well beyond the Lehman shock: the VIX remains durably above 25 until mid-2012, partly because prudential authorities impose accelerated deleveraging on institutions, partly because the European sovereign debt crisis reimports systemic stress in 2011. The final resolution of this phase coincides with Mario Draghi’s whatever it takes declaration in July 2012 and the progressive stabilisation of the euro.

4.4 Yellen expansion — second compression (2014-2019)

The average VIX returns to 15.1, standard deviation 3.8. 2017 sets an all-time annual record at 11.1 — a level never matched since. That compression preceded the February 2018 Volmageddon (peak 50.3), which imploded several short-volatility ETNs and forced Credit Suisse to terminate the XIV, which lost 96% of its value in a single session. The VIX then settled in a 12-25 range through end-2019, with a trough at 11.03 in late 2019 — another low preceding a major shock three months later. This period also marks the institutionalisation of short-volatility strategies and the growth of covered call ETFs.

4.5 Pandemic and Powell cycles (2020-2026)

The COVID peak at 82.69 (16 March 2020) constitutes the official closing record. The 2021-2022 phase of inflation and monetary tightening keeps the VIX in an elevated 18-35 range. The 2023-2024 decompression was abruptly interrupted on 5 August 2024 by the yen carry trade unwind: intraday peak at 65.73, third-highest historical print in the series. The episode, triggered by the Bank of Japan’s surprise rate hike on 31 July and a weaker-than-expected US employment report on 2 August, led to the forced unwinding of long-equity / short-yen positions accumulated since 2021. The Nikkei lost 12.4% on 5 August, the largest single-day drop since 1987. The VIX then settled durably in a 14-18 zone, a level comparable to the 2017 and 2019 troughs.

For the empirical detail of each of the seven major spikes (LTCM, dot-com, GFC, Flash Crash, Volmageddon, COVID, yen carry trade unwind), see the major VIX spikes since 1990.

The VIX is not an indicator of investor fear. That media framing collapses three distinct components — hedging demand, implied skew, market-maker liquidity — that can move in opposite directions. Reading the VIX as a single sentiment signal produces systematic misinterpretations at regime turns, precisely when the indicator becomes most informative.

5. Troughs and peaks: what the historical record documents

An empirical regularity appears in the 1990-2026 series: extreme VIX levels, in both directions, have preceded regime inflections. This observation is descriptive, not prescriptive.

On the trough side, three episodes stand out. January 2007: VIX at 9.89, the series low up to that point. Seven months later, the August 2007 episode on BNP Paribas money-market funds marked the first signal of the subprime crisis, and the VIX reached 31.1 in October 2008 then 89.5 a month later. December 2017: annual average VIX at 11.1, the all-time record. Two months later, the February 2018 Volmageddon pushed the VIX to 50.3 in a single session. November 2019: VIX at 11.03. Four months later, the COVID crash. The pattern holds three for three over the period, but the sample is small and the macroeconomic contexts distinct — no mechanical conclusion about predictive power. Note that other historical troughs (May 2013 at 11.8, August 2016 at 11.3) were not followed by major shocks within six months, which invalidates any mechanical reading of the low VIX implies crash signal.

On the peak side, the symmetric observation. The eight breaches of the 50 threshold since 1990 (LTCM 1998, GFC 2008-2009, Flash Crash 2010, sovereign debt 2011, Volmageddon 2018, COVID 2020 on several occasions, yen carry trade unwind 2024) were followed in seven of eight cases by an S&P 500 rebound over the twelve-month horizon. The atypical case remains 2008, where the VIX kept printing above 40 for several months before the equity index bottomed in March 2009. The full table of individual cases with detailed 1, 3, 6 and 12-month post-spike returns is documented in the full contrarian almanac dataset.

The regularity observed at the extremes is not a timing rule. Three factors limit the operational scope of this observation: the rarity of episodes (8 breaches of the 50 threshold over 35 years), the dispersion of 1 and 3-month returns (which can remain negative before the 12-month rebound), and the heterogeneity of macro contexts (LTCM in an expansion cycle, COVID in a brief technical recession, GFC in a deep recession). The honest reading is: high VIX levels have been followed, in a majority of cases, by an equity rebound over 12 months, not VIX above 30 implies buy the S&P 500.

6. The 2024-2026 compression: reading the current phase

Since the intraday peak of August 2024 at 65.73, the VIX has retraced continuously. The average closing level between November 2024 and April 2026 stands at 15.1, well below the 1990-2025 historical average of 19.5. Three readings coexist.

The mainstream reading treats this regime as a new normal linked to the maturity of the SPX options market. Hedging capacity has expanded since the introduction of 0DTE options in 2022 — now 47% of SPX option volume per the CBOE Q4 2025 report —, allowing finer tail-risk management without inflating the 30-day VIX. Under this view, a durably low VIX reflects an efficient market, not fragility. The thesis, advanced notably by the CBOE Options Institute and by the strategy desks of Goldman Sachs and Morgan Stanley, rests on two arguments: the migration of hedging into the intraday segment, and the structural improvement of SPX liquidity (daily average volume up from 1.8 million contracts in 2015 to 4.2 million in 2025).

The alternative reading, advanced by the BIS (Bulletin No. 78, September 2025), points to an accumulation of short-volatility positions in structured products. European and Asian autocalls, whose outstanding amounts exceeded USD 730 billion at end-2025 per Citigroup Global Markets estimates, implicitly sell volatility to the market. Systematic option-selling strategies (covered call ETFs, volatility carry funds) saw their assets quadruple between 2022 and 2025, rising from USD 28 to USD 117 billion per Morningstar data. Under this view, low VIX is not the consequence of genuinely reduced risk but of an artificially expanded supply of volatility. The February 2018 precedent, where the XIV implosion coincided with a VIX that quintupled in 24 hours, serves as a memo for proponents of this thesis.

The third, more pragmatic reading examines signals that contradict or confirm the compression. The VIX-HY OAS divergence as regime marker has become one of the central indicators: VIX and high-yield credit spread are historically correlated (0.65-0.80 over the 2000-2019 period), but that correlation collapsed at end-2023. The HY OAS has been oscillating between 280 and 310 basis points since end-2024, a level itself below historical average. The simultaneous compression of the two indicators is unprecedented in scale over 2000-2025. The record compression phase since August 2024 is documented separately with its historical comparisons (2017, 2019).

None of the three readings is demonstrated. The empirical unknown is the duration of the compression: if it extends beyond 24 months, the new normal thesis gains credibility; if a brutal repricing occurs, the artificial-suppression thesis will impose itself as the post-event framing. The monitoring indicators that could signal the inflection include a flip of the VIX term structure into backwardation, a widening of the HY OAS above 400 basis points, or a retraction of SPX book depth on deep OTM puts.

6.1 Monitoring indicators used by risk desks

Several complementary monitoring indicators are used by institutional risk desks to qualify the robustness or fragility of the compression regime. The VVIX/VIX ratio — the volatility of volatility — gives an indication of the nervousness of the options market on the VIX itself. An elevated VVIX without an elevated VIX signals a latent anticipation of volatility increases that the spot level does not reflect. In April 2026, VVIX stands at 95, below its historical average of 92 — a level consistent with VIX compression but not signalling any anticipation of imminent spike. Direct extension: Systemic Risk Indicators and Financial Market Stress Signals.

The CBOE SKEW index, which measures the pricing of 30 delta OTM versus 50 delta options, provides a complementary read. An elevated SKEW indicates investors pay a significant premium for crash protection, even when the VIX is low. Historically, SKEW levels above 145 have preceded some spikes (August 2015, February 2018), but predictive power remains limited and false positives are numerous.

The concentration of short-vol positions in CFTC commitments of traders provides a third dimension. The weekly report published by the CFTC on dealer and asset manager positioning in VIX futures allows observation of position accumulation or unwinding. A prolonged accumulation of short positions in VIX futures by non-commercials preceded the 2018 Volmageddon; the same signal observed in 2025-2026 feeds the BIS artificial-suppression thesis.

7. Limits and blind spots

Three limits should frame any VIX reading.

The first: the VIX measures S&P 500 volatility only. Equivalents — VXN on the Nasdaq 100, VSTOXX on the Euro Stoxx 50, VHSI on the Hang Seng — sometimes paint divergent pictures. In August 2024, the VSTOXX peaked at 38 when the VIX touched 65: the US-specific component of the shock (yen carry, US tech exposure) explains the gap. Reading the VIX as a global measure of equity risk produces framing errors in regional stress phases. The cross-comparison VIX/VXN is particularly informative: a positive VXN minus VIX gap beyond 5 points historically signals stress concentration on tech names, a configuration observed in 2018, in 2022 and partially in August 2024.

The second: sensitivity to deep OTM options makes the VIX vulnerable to liquidity disruptions. In stress periods, far-strike truncation mechanically changes the index composition. The level captured on days of degraded microstructure is not directly comparable to the level captured in normal regimes. This limit was particularly visible on 24 August 2015 (Chinese mini-crash) when the disorderly SPX open temporarily distorted the VIX, and on 5 August 2024 when bid-ask spreads on OTM options widened 280% within minutes.

The third: put-call asymmetry is structural. The SPX options market is durably biased toward puts (negative skew), which sustains a floor hedge premium even in the absence of stress. Mechanically comparing VIX 1995 with VIX 2025 without adjusting for structural skew evolution produces misleading comparisons. The skew distortion is one of the main objections to direct comparison between the 1990-2007 period (less pronounced skew) and the 2010-2026 period (structurally more stretched skew after the GFC).

The VIX remains, despite these limits, the best-documented and most-liquid composite indicator of equity stress. Cross-referenced with complementary signals — high-yield credit spread, yield curve, leading recession indicators such as the T10Y3M recession signal —, it constitutes a robust regime read. Taken in isolation, it remains exposed to the systematic misinterpretations the previous seven sections have mapped.

8. The VIX within the stress-indicator cartography

Replaced in its ecosystem, the VIX is but one of the indicators that compose the institutional reading of equity risk. The market regimes pillar groups the structural components — flows, sentiment, microstructure, regimes — of which the VIX is only one facet. More specifically, the sub-pillar systemic risk indicators articulates the VIX with complementary indicators: HY OAS for credit stress, NFCI for aggregate financial conditions, term structure of the yield curve for cyclical expectations.

This articulation is more than an editorial convention. Three indicators read jointly — VIX, HY OAS, T10Y3M — give an image none of them provides taken alone. Eco3min maintains the full record in our high-yield credit-spread data. When the three move in the same direction (simultaneous compression at end-2024, simultaneous deterioration at end-2007), regime conviction is high. When they diverge (T10Y3M negative since October 2022 but VIX low and HY OAS compressed at end-2024), it is precisely this divergence that becomes the central observation. The most frequent error in reading the VIX consists in treating it as an autonomous signal, while its informational value is constructed in confrontation with its systemic neighbours.

The NFCI (National Financial Conditions Index published by the Chicago Fed) constitutes a complementary composite indicator: it aggregates 105 sub-indicators (spreads, leverage, microstructure) into a normalised score. Its correlation with the VIX is high but not mechanical. The phases where the NFCI signals tightening financial conditions without the VIX reacting (spring 2018, summer 2023) are precisely those where the decomposition between VIX components becomes informative again — the absence of hedge demand can mask a deterioration already visible on other dimensions of microstructure.

8.1 From reference indicator to speculative object

The VIX has followed a particular institutional trajectory since 2004. Initially designed as a reference indicator for risk desks, it progressively became a tradable underlying through CFE VIX futures (2004), VIX options (2006), and then ETFs and ETNs replicating or inverting VIX futures performance. The financialisation of volatility itself has two distinct consequences.

First: liquidity in the VIX futures and options market has become deep enough to allow systematic tail-risk hedging. Daily VIX futures volumes rose from 14,000 contracts in 2007 to more than 350,000 contracts in 2025 per CFE data. That depth allows institutions to buy volatility at moderate marginal cost, which contributes to the stability of the low-volatility regime observed since 2014. See also, on the financialization of a commodity futures market: the financialization of cocoa futures.

Second: the proliferation of ETPs based on VIX futures (VXX, UVXY, SVXY, and the inverse XIV before its 2018 implosion) created a layer of structurally short-volatility positions. The contango mechanism imposes a persistent negative roll yield on these vehicles — the mechanical loss linked to the spread between VX1 and VX2 at each contract roll. Over 2009-2018, the VXX lost on average 60% per year, and the inverse XIV had gained roughly 50% per year before its implosion. This dynamic contributed to the accumulation of short-vol positions that unwound abruptly in February 2018.

The return of this dynamic in 2025-2026, in a different institutional form (autocalls rather than retail ETNs, hedge funds rather than retail investors), constitutes one of the central arguments of the BIS artificial-suppression thesis. The 2018 precedent serves as empirical reference, but the composition of short-volatility open interest is this time more opaque, which complicates real-time analysis.

8.2 Why the VIX remains a central indicator despite its limits

No equity stress indicator combines, to date, the qualities of the VIX: continuous availability since 1990, underlying liquidity, methodological transparency, broad coverage by institutional research desks. The proposed alternatives — composite indicators like the NFCI, proprietary indicators from major banks (Goldman Sachs Risk Aversion Index, JPMorgan Cycle Indicator), or academic stress indices — do not have the same historical depth or the same instrumental liquidity. Related work: Our framework of systemic-risk signals.

This informational dominance has a cost: the VIX is the object of disproportionate attention relative to what it actually measures. The majority of market commentary mentioning the VIX ignores its structural limits. The institutional reading, more rigorous, treats the VIX as one input among others in a multi-indicator surveillance framework. The distinction between mainstream reading and institutional reading is one of the most enduring sources of confusion in media coverage of equity stress phases.

The VIX informs about the volatility premium the market pays, not about the risk it ignores — the documented contrarian thresholds above VIX 30 / 40 / 50 are neither trading rules nor timing rules.

Conclusion

The VIX aggregates three dimensions — sentiment, skew, liquidity — that the mainstream reading conflates. Its 1990-2026 series documents five successive regimes and several empirical regularities at the extremes, without licensing mechanical extrapolation. The compression phase observed since end-2024 replicates known configurations (2017, 2019) without either thesis — new normal or artificial suppression — yet being validated. Read alongside credit stress indicators and the yield curve, the series retains its compass value. Read in isolation, it invites documented misinterpretations. The maturity of the SPX options market, accelerated by the rise of 0DTE since 2022, probably redefines what a normal VIX means; but that redefinition remains a working hypothesis, not an established fact.

- The VIX aggregates three components — hedging demand, implied skew, market-maker liquidity — whose decomposition is more informative than the raw level.

- Five successive regimes structure the 1990-2026 series, from the post-LTCM peak to the current compression, with historical troughs that have preceded each of the three major repricings (2007, 2017, 2019).

- The 2024-2026 phase combines a new normal hypothesis tied to 0DTE growth and the BIS thesis of artificial suppression by short-volatility structured positions; neither has been demonstrated.

- Without cross-reference to the high-yield credit spread, the yield curve and the term structure of VIX futures, reading the VIX alone exposes one to systematic misinterpretations at regime turns.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…

The ECB-Fed Rate Differential: the Driver of EUR/USD

The rate differential between the ECB and the Fed is the first-order driver of EUR/USD. But it is…