WALCL-to-GDP: Fed Balance Sheet Ratio, International Comparison with ECB, BoJ, BoE

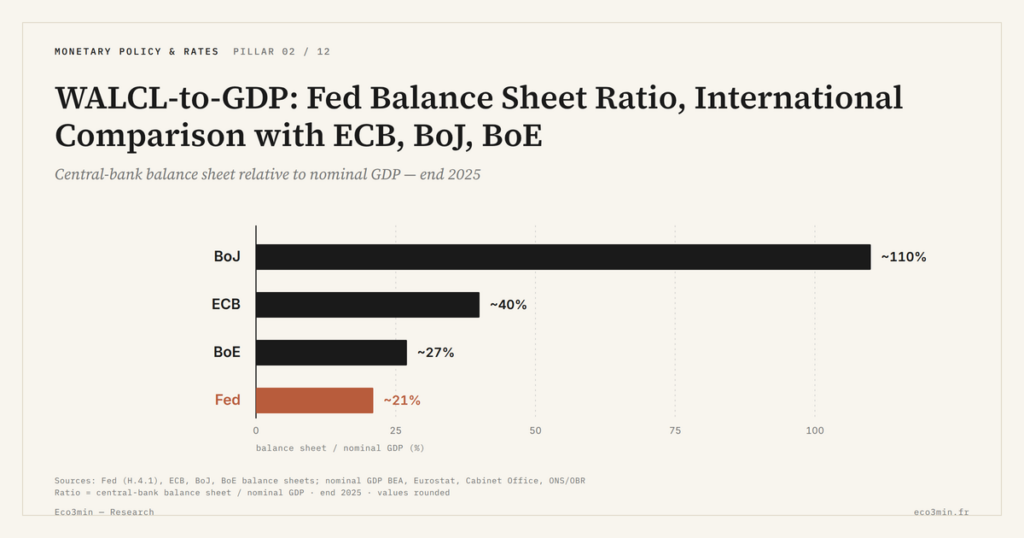

The Fed’s WALCL-to-GDP ratio moved from 6% in 2008 to 38% at the March 2022 Covid peak, before retreating toward 24% by late 2025. Compared to the ECB (50%), the BoJ (120%) and the BoE (24%), it positions the Fed in a median spot.

TL;DR

A significant share of the Fed's balance-sheet normalization since 2022 came from US nominal GDP rising about 7%, alongside WALCL itself shrinking by -$2.2 trillion.

- WALCL records foreign central banks' dollar swap-line drawings on the Fed's asset side; during the March 2020 episode that usage peaked near $450 billion, adding directly to the series.

- Across 2022-2025 the Fed and BoE each cut roughly 4 percentage points of GDP per year, the ECB at half that pace, while the BoJ stabilizes between 100% and 130%.

- An identical ratio carries different meaning by context: Japanese debt held over 90% domestically, US public debt around 123% of GDP (CBO), euro-area near 88% (Eurostat) in 2025.

Reading WALCL in raw value without GDP normalization says nothing. Comparing the Fed to the three other major developed central banks requires the balance-sheet-to-GDP ratio and attention to divergent structural constraints. This dynamic is quantified in the Fed balance-sheet dataset.

Comparing $6.8 trillion of Fed assets to ~€5 trillion of ECB balance sheet or ~¥700 trillion of BoJ balance sheet in raw nominal values carries no actionable economic information. The three economies have different sizes, different financial structures, and distinct monetary regimes. The metric that makes comparisons interpretable is the balance-sheet-to-GDP ratio, which neutralizes the size effect and allows homogeneous relative reading. This normalization is the cornerstone of any serious comparative analysis of developed-market central bank balance sheets, and conditions the reading of the integrated read of Fed stance through the balance sheet.

Why the WALCL-to-GDP ratio is the relevant metric

For the Fed, this ratio moved from ~6% in 2008 to ~38% at the March 2022 Covid peak, before retreating toward ~24% by late 2025 according to combined Fed (WALCL) and BEA (US Nominal GDP, trailing year) data. This trajectory encapsulates three distinct elements that the dollar level alone does not show: the progressive Fed balance-sheet expansion over fifteen years, the denominator effect of nominal US economic growth (US nominal GDP nearly doubled between 2008 and 2025), and the ongoing QT phase that combines WALCL decline and continued denominator growth.

Ratio construction matters analytically. The Fed publishes WALCL weekly; the BEA publishes nominal GDP quarterly, with frequent historical revisions. For an instantaneous reading, one generally takes the weekly WALCL divided by the annualized nominal GDP of the latest available quarter — introducing a minor but systematic temporal lag. International comparisons apply the same convention with the corresponding national sources: Eurostat for the euro area, the Japanese Cabinet Office for Japan, the Office for National Statistics for the United Kingdom.

The denominator effect deserves specific attention. Over 2022-2025, the Fed’s WALCL-to-GDP ratio fell not only because WALCL was declining (-$2.2 trillion), but also because nominal GDP rose by roughly 7% cumulative in current value over the period. A significant share of the “normalization” of the Fed balance sheet measured by the ratio therefore comes not from QT but from underlying economic expansion. This distinction is rarely made explicit in market commentary.

The four trajectories: Fed, ECB, BoJ, BoE

The Fed, over 2008-2025, saw its ratio move from 6% to 38% then 24%. The 38% Covid peak is historically elevated for the Fed, but remains moderate in international context. The current normalization phase brings the ratio back into a range comparable to the post-QE3 peak of 2014 (~25%), well above the pre-2008 baseline.

The ECB followed a different trajectory. According to ECB and Eurostat data, its balance-sheet-to-euro-area-GDP ratio moved from roughly 20% in 2008 to roughly 70% at the height of the Pandemic Emergency Purchase Programme (PEPP) in 2022. The post-2022 normalization has been slower than the Fed’s: APP reinvestments were halted in July 2023 and PEPP reinvestments fully stopped in late 2024 per official ECB communication. The ECB-to-GDP ratio stands at roughly ~50% by late 2025, twice the Fed’s ratio in an economy comparable in aggregate size.

The Bank of Japan occupies a structurally different position. Its balance-sheet-to-Japanese-GDP ratio moved from roughly 20% in 2008 to a structurally elevated 100-130% since 2015 according to BoJ and Japanese Cabinet Office data. This considerable relative size reflects three factors: the Quantitative and Qualitative Easing launched in April 2013, the Yield Curve Control policy active from October 2016 to March 2024, and a substantial holding of exchange-traded funds purchased by the BoJ that no other developed-market central bank has ever acquired. The March 2024 dismantling of YCC did not lead to aggressive balance-sheet reduction: the BoJ has reduced its JGB purchase pace without engaging in discretionary QT comparable to the Fed or BoE. The Japanese context is documented in the thirty years of Japanese deflationary trap which illuminate the specific structural constraints.

The Bank of England occupies an intermediate position. Its balance-sheet-to-UK-GDP ratio moved from roughly 4% in 2008 to a peak of ~40% in 2022 according to BoE and ONS data, before falling back toward ~24% by late 2025. The BoE distinguishes itself from the other three by its QT methodology: it conducts active sales of gilts (~£100 billion per year decided since September 2022), in addition to passive runoff. This methodological asymmetry changes how the BoE ratio reads: the BoE reduces its balance sheet faster than the Fed as a percentage of GDP, but at the cost of more active intervention in the secondary gilts market.

The cumulative observation of all four trajectories over the 2022-2025 window reveals another often-omitted element: the pace of relative normalization differs strongly across the four central banks, even when the direction of variation is shared. The Fed and BoE reduce their ratios at a comparable rate (roughly 4 percentage points per year over 2022-2025), the ECB reduces at half that pace, the BoJ stabilizes. This pace differentiation, not only the level differentiation, is the structural data point of the contemporary phase.

One additional structural feature deserves explicit treatment: the role of swap lines. The Fed maintains permanent swap-line agreements with five major foreign central banks (ECB, BoJ, BoE, BoC, SNB) plus temporary lines with several others. These arrangements allow foreign central banks to access dollars during stress without holding them on their own balance sheet. WALCL records the dollar value of swap-line drawings on the Fed asset side when activated. During the March 2020 episode, swap-line usage peaked at roughly $450 billion, adding directly to WALCL. This international plumbing dimension does not appear in raw cross-country comparisons but matters for understanding why the dollar’s reserve-currency status structurally enlarges the Fed’s effective footprint relative to GDP. The wider context: how liquidity flows through to assets.

Comparing the Fed to the BoJ and concluding that the BoJ has a “four times more expansive” balance sheet relies on comparison without contextual normalization. Structural constraints — public debt, reserve currency status, banking structure, depth of the domestic bond market — radically modify what an identical ratio means in two economies. The raw compared figure is correct; reading it as an indicator of “relative posture” is misleading.

Three readings of the post-2022 divergence

The first reading integrates structural constraints. Japan displays the highest balance-sheet-to-GDP ratio in the developed-market panel for the past decade, but operates with public debt held primarily domestically (>90% by Japanese residents per BoJ data), an economy with weak or declining nominal growth, and a yen that does not function as a dominant reserve currency. The ECB operates with twenty different economies, no common Treasury, and an average public-debt ratio around 88% of euro-area GDP in 2025 per Eurostat. The Fed operates with the dollar as the international reserve currency and US public debt reaching ~123% of GDP in 2025 per CBO data. These contexts are not comparable without caveat.

The second reading concerns the forward trajectory. Over 2022-2025, the Fed and BoE reduce their ratios, the ECB progressively stabilizes its own, the BoJ continues its very gradual normalization policy. These choices reflect different constraints: the Fed has policy space tied to its high ON RRP liquidity that cushions QT, the ECB must manage potential sovereign-spread fragmentation between members, the BoJ keeps an elevated ratio as a structuring tool of post-YCC monetary policy. The doctrinal shift behind the current ratio partly explains this divergence. For full historical reconstruction, the WALCL-to-GDP dataset for full time series provides the underlying data.

The third reading poses the implicit normative question that raw-value comparisons wrongly treat as settled: is there a “good” balance-sheet-to-GDP ratio? No modern monetary theory provides a universal optimal threshold. The 120%-of-GDP Japanese ratio has not generated a major monetary crisis in a decade; the historical 6% Fed ratio was not associated with particular monetary sterility. Comparisons must be read as relative positionings in a spectrum, not as ratings on an absolute scale. This methodological neutrality is crucial for liquidity conditions across the monetary system whose determination depends on each national context.

Concretely, by late 2025, the Fed at ~24% sits in a median position within the developed-market panel. For the analyst seeking to position the Fed’s monetary stance in its international context, the message is sober: the Fed is neither the most expansive central bank in the panel (the BoJ is, structurally), nor the most restrictive (the BoE accelerates its reduction via active sales). The current Fed ratio sits in an intermediate range that does not, in itself, carry a verdict on effective monetary stance. The verdict, if there is one, comes from integrated reading with the Fed Funds rate, liability components, and marginal financing indicators. Cross-country benchmarking informs context; it does not replace the integrated reading exercise, nor does it provide a normative anchor for monetary stance assessment in the absence of explicit structural caveats.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…