WALCL — Fed Balance Sheet, Monetary Signal and Systemic Liquidity Indicator

Since 2008, the Federal Reserve’s balance sheet aggregated in the WALCL ticker has become the Fed’s effective monetary footprint, complementing the Fed Funds rate. Reading it correctly conditions any analysis of financial conditions and of the 2022-2026 QT runoff now approaching its terminus.

TL;DR

Since 2008 the Fed's balance sheet, aggregated in WALCL, carries what the Fed Funds rate cannot: the duration and credit risk pulled from the market, read through three doctrinal regimes.

- Published every Thursday by FRED from the H.4.1 release, WALCL aggregates only Fed assets (Treasuries, MBS, repos); reserves, ON RRP and the TGA sit on the excluded liability side.

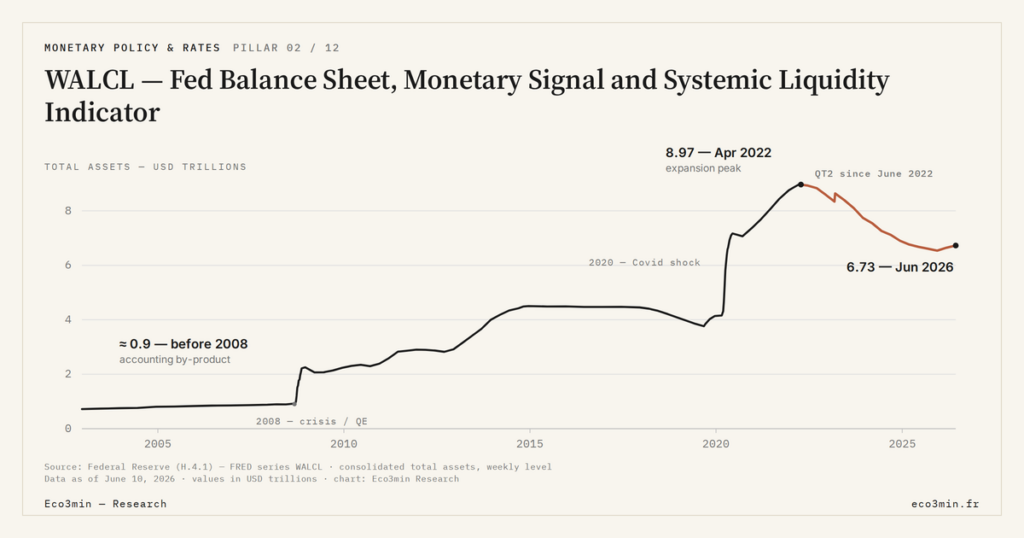

- Four QE waves multiplied the balance sheet ninefold over fourteen years, from $900 billion to $8.97 trillion, before QT2 removed close to three trillion from June 2022 on.

- The QT2 runoff cap started at -$95 billion a month, then dropped to -$60 billion in May 2024 as the Fed neared the 'ample reserves' level it formally adopted in January 2019.

- Over 2022-2024 WALCL fell by more than two trillion with no visible liquidity crisis, because the ON RRP absorbed nearly the entire shock while M2 slipped only about 4.5%.

Reading WALCL today requires distinguishing three doctrinal regimes, two complementary variables — level and composition — and a critical frontier with market liquidity.

WALCL — Total Assets of the Federal Reserve, published every Thursday by FRED at the St. Louis Fed from the Board of Governors’ H.4.1 release — aggregates every asset carried on the Federal Reserve’s consolidated balance sheet: Treasuries, agency Mortgage-Backed Securities (MBS), repos, primary credit, emergency support facilities. Before 2008, the series sat near $900 billion and held the attention of a narrow academic readership. Three episodes turned it into a core macro indicator: the successive QE programs from November 2008 to October 2014, the March 2020 monetary response to the Covid shock that drove WALCL to an absolute peak of $8.97 trillion in April 2022 (FRED WALCL, week ending April 13, 2022), and the Quantitative Tightening initiated in June 2022 and still ongoing by late 2025.

Reading WALCL today is no longer tracking a ledger entry. It is observing the Fed’s effective monetary footprint on global financial conditions — the imprint that, for fifteen years, the Fed Funds rate decision alone has no longer been sufficient to summarize. This article sets the frame: why WALCL became central, what it measures and what it does not, the three doctrinal regimes that structure its use, and how to read the current QT phase as the Fed approaches its terminal balance sheet.

Why WALCL became central after 2008

For the four decades that preceded the 2008 financial crisis, US monetary policy reduced, for both analysts and markets, to a single variable: the Federal Funds rate. The Federal Reserve’s balance sheet was not a policy instrument but an accounting by-product of routine banking system plumbing. According to Federal Reserve data, this balance sheet oscillated between $700 and $900 billion from the late 1990s through August 2008, made up mostly of Treasuries held against currency in circulation. For context: Liquidity and Financial Conditions: Monetary Plumbing, QT Cycles, and Market Impact.

Lehman Brothers’ collapse in September 2008 changed that equation. The Fed cut its policy rate to the effective lower bound of 0-0.25% in December 2008, hitting what economists call the zero lower bound. The traditional channel — affecting the cost of capital via the policy rate — was neutralized. To keep acting on financial conditions, the Fed had only one option left: actively use the size and composition of its balance sheet. This is the contemporary invention of Quantitative Easing, formalized on November 25, 2008 when the FOMC announced the purchase of $500 billion of agency MBS. Worth reading alongside: the myths surrounding the Fed and monetary policy.

Since then, WALCL has gone through four major expansions and two orderly contractions. The QE1 (2008-2010), QE2 (2010-2011), QE3 (2012-2014) and QE Covid (2020-2022) expansions multiplied the balance sheet ninefold over fourteen years, from $900 billion to $8.97 trillion. The QT1 (October 2017 – July 2019, interrupted by the September 2019 repo crisis) and QT2 (June 2022 – ongoing) contractions have removed close to three trillion dollars cumulatively. How Fed balance-sheet doctrine evolved across these regimes is itself an analytical object distinct from the simple chronology of dollar amounts.

What makes WALCL irreplaceable for the contemporary analyst is that it records a dimension of monetary policy that the Fed Funds rate cannot capture. The policy rate acts on the marginal price of interbank credit; WALCL measures the quantity of duration and credit risk the central bank has removed from the market. Two distinct variables, two distinct transmission channels, two different imprints on financial conditions. The FRED WALCL ticker has become, over fifteen years, the most direct quantitative indicator of this second dimension. For the mechanics of liquidity transmission to financial conditions, the balance sheet today is as structurally important as the rate.

The central-bank academic literature, since 2012, has documented this duality. Work by the Federal Reserve Board staff on the portfolio rebalancing channel and the signaling channel of QE has established that variations in the balance sheet affect term premia on the Treasury curve independently of expectations about the Fed Funds rate. It is this analytical distinction that justifies monitoring WALCL with the same attention given to FOMC rate decisions.

The shift from the Federal Funds rate as the dominant variable to a dual rate-plus-balance-sheet toolkit corresponds to a deep conceptual mutation, documented notably in the December 2008 FOMC minutes and the 2009 annual report of the Board of Governors. Before that date, the Fed’s monetary communication spoke almost exclusively of a rate target; since then, every FOMC Statement dedicates a specific section to asset purchases, balance sheet composition, then to runoff pace. The institutional embedding of the balance sheet as a policy variable also shows up in statistical production: the WALCL series itself, technically available since 2002 on FRED, only became a routine analytical object after 2010, when QE2 purchases forced analysts to quantify monetary effort beyond the rate.

This mutation also has practical consequences for macro-financial reading. The Fed Funds rate acts first on the short end of the curve; WALCL acts rather on the long end via the portfolio rebalancing channel. When the Fed combines the two tools in the same direction (rate hikes plus balance-sheet reduction over 2022-2024), the effect on financial conditions compounds. When it dissociates them (hypothetical case of rate cuts during an ongoing QT), the net effect becomes ambiguous and requires composite reading. This is precisely what makes WALCL inseparable from the Fed Funds rate in contemporary analysis: they are two complementary variables of the same global monetary stance, not an instrument and its substitute. A related read: our reading of monetary plumbing and QT.

The analysis of FOMC decisions in the dedicated pillar on monetary regimes and rate cycles deepens this duality by situating it within the long history of developed central banks. The US specificity lies in the fact that the Fed was the first major central bank to assume this doctrinal duality; the ECB and BoJ followed with a lag, in different structural contexts.

What the ticker actually measures — and what it does not

Despite its sometimes ambiguous treatment in general media, WALCL does not aggregate “the Fed balance sheet” in the full accounting sense. It precisely measures the total assets held by the consolidated Federal Reserve System, as reported every Thursday by the Board of Governors’ H.4.1 release. The liability side of the balance sheet — bank reserves, ON RRP, Treasury General Account (TGA), currency in circulation, foreign and institutional accounts — sits outside WALCL. This asymmetry matters analytically: what WALCL precisely measures requires acknowledging that liability movements can neutralize or amplify the effect of an asset move at constant total size.

Three analytical conflations come up repeatedly and deserve to be disposed of from the start. The first equates WALCL with M2, the broad monetary aggregate also published by the Fed. M2 measures liquid holdings of the non-bank private sector (deposits, money market funds, savings accounts); WALCL measures the stock of financial assets held by the central bank. The two can diverge sharply: over 2022-2024, M2 contracted by roughly 4.5% in nominal terms according to the Fed’s M2SL series, while WALCL fell by about 25%. The rotation between the two variables is not mechanical.

The second conflation identifies WALCL with the monetary base. The monetary base stricto sensu consists of the Fed’s monetary liabilities: currency in circulation plus bank reserves. It is smaller than WALCL by roughly two trillion dollars by the end of 2025, mainly because of the ON RRP and TGA, which sit on the liability side but do not constitute the monetary base in the classical monetarist sense. The distinction is explicit in the Fed’s own statistical publications, which separates H.4.1 (balance sheet) from H.3 (reserves and monetary base). In depth: our sub-pillar on liquidity and financial conditions.

The third conflation, and probably the most damaging for market analysis practice, identifies WALCL with the financial system’s liquidity. Research published notably by NY Fed staff on the reserves regime since 2018 has established that the effective liquidity available to market participants depends on liability-side variables — bank reserves and ON RRP in particular — far more than on the aggregate asset size. This is precisely the object of the deeper analysis covered in the signal limits of WALCL versus market liquidity.

This analytical separation between WALCL and monetary aggregates has a practical consequence often missed in market commentary. The quantity of money in actual circulation depends primarily on commercial banks’ credit decisions, which mobilize their reserves as raw material but are not mechanically constrained by reserve levels in the contemporary ample-reserves regime. A WALCL variation is therefore not a direct signal of monetary creation; it is a signal about upstream conditions (interbank rates, term premia, collateral availability) that then orient credit decisions.

This dissociation is made explicit in the post-2008 literature on creditless recovery: during the 2010-2014 phase, WALCL tripled without M2 or bank credit to the private sector following at the same pace. Conversely, phases of rapid private credit expansion (2003-2006 for example) occurred with a flat WALCL. The transmission belt between the Fed balance sheet and money creation passes through relays that can be coupled or decoupled depending on the regime in place.

The contemporary Fed itself acknowledges this distinction in its communication: when Chair Powell speaks of monetary stance, he uses both the Fed Funds rate and the balance-sheet posture as joint variables; when he speaks of money in circulation or inflation transmission, he refers instead to M2, bank credit, and household savings dynamics. The conceptual separation is institutionalized.

This regime-dependent reading is what distinguishes a working analytical use of WALCL from a static, level-only interpretation. The ticker remains the same; what it informs about changes with the surrounding monetary and operational regime.

Reading a WALCL decline as automatically equivalent to a systemic liquidity contraction is the most widespread analytical error. Over 2022-2024, WALCL fell by more than two trillion dollars without a visible liquidity crisis, because the ON RRP absorbed nearly the entire shock. The relevant reading requires cross-checking the asset (WALCL) with liability components.

Three doctrinal regimes structure use across 2008-2026

Granular historical analysis of WALCL reveals not a continuous trajectory but a succession of three distinct doctrinal regimes, each characterized by a different function the Fed assigns to its balance sheet. This typology is not a mere taxonomic exercise: it conditions what reading the ticker can mean at any moment in the cycle.

The first regime, running from November 2008 to October 2014, established the balance sheet as a prolonged emergency tool. Three successive QE programs (QE1 announced November 2008, QE2 decided November 2010, QE3 launched September 2012) drove WALCL from ~$900 billion to ~$4.5 trillion over six years, in a context where the zero lower bound rendered the rate channel inoperative. The official doctrine, as developed in the FOMC Statements of the period, presented the balance sheet as a temporary substitute for the policy rate. The explicit objective was flattening the Treasury curve via the portfolio rebalancing channel, and supporting financial conditions by compressing term premia. Also relevant: our explainer on steepening versus flattening.

The second regime, much shorter but more intense, runs from March 2020 to March 2022. It repositioned the balance sheet as a rapid-response weapon. Facing the Covid shock, the Fed practically doubled WALCL in three months: from ~$4.2 trillion in early March 2020 to ~$7.2 trillion by late June 2020. This expansion simultaneously covered four distinct objectives — stabilizing the Treasury market, supporting agency MBS, opening credit facilities for corporates and municipalities, and providing international dollars via swap lines. The absolute peak of $8.97 trillion was reached in April 2022 according to FRED WALCL data, marking the end of the expansion. On the same question: our explainer on swap lines.

The third regime opened in June 2022 with the start of Quantitative Tightening 2 (QT2) and redefines the balance sheet as a permanent, dosage-variable lever. The Fed no longer envisages returning to the pre-2008 size, but rather reaching a terminal balance sheet consistent with the ample reserves regime it formally adopted in January 2019. The initial runoff cap was set at -$95 billion per month (with -$60 billion on Treasuries and -$35 billion on MBS); it was lowered to -$60 billion per month in May 2024, primarily through a reduction of the Treasury cap to -$25 billion. This coordinated slowdown signals that the Fed is approaching the level of bank reserves considered “ample” without being excessive. Understanding the current QT runoff trajectory requires integrating this variable-dosage logic.

These three regimes differ less in WALCL size than in the function the Fed assigns to it within its toolkit. Emergency tool at the ZLB, then systemic response weapon against an exogenous shock, then controlled normalization instrument — each transition changes the grammar of how the ticker should be read. This doctrinal analysis is complementary to but distinct from the history of operational tools (BTFP, SRF, ON RRP, primary dealer facilities) that the Fed invented to manage its balance sheet during each crisis, a reading developed in dedicated work on the three episodes that required new operational tools between 2002 and 2026.

Closer examination of each regime reveals internal inflections that a summary chronology hides. The first regime in fact breaks down into three sub-phases. QE1 (November 2008 – March 2010) aimed at stabilizing the MBS market after Lehman’s collapse, with $1.25 trillion of MBS purchases, $175 billion of agency debt and $300 billion of Treasuries according to the program’s final figures. QE2 (November 2010 – June 2011) inaugurated a pure quantitative-target logic with $600 billion of Treasury purchases over eight months. QE3 (September 2012 – October 2014) introduced the major novelty of open-ended purchases calibrated on labor-market conditions, with a variable pace of $40 then $85 then $65 billion monthly. Directly related: every Fed pause since 1971.

The second regime has a rarely highlighted singularity: it simultaneously combines classic QE (Treasury and MBS purchases) and exceptional support facilities (Primary Market Corporate Credit Facility, Municipal Liquidity Facility, Main Street Lending Program) that did not exist in the pre-2020 toolkit. This operational innovation took the Fed into non-conventional territories beyond pure asset purchases: it became, temporarily, a direct credit actor to the non-bank private sector. Most of these facilities were closed in late 2020 or early 2021, but the doctrinal precedent matters for future regimes.

The third regime is distinguished by a unique feature: it is the first QT planned as a full-cycle phase, not as an emergency correction. The QT1 precedent (October 2017 – July 2019) had been prematurely interrupted by the September 2019 repo crisis. The current QT2 incorporates this learning: higher initial cap but with programmed slowdown anticipating the floor, explicit FOMC communication on the ample reserves regime, and an available SRF backstop. This transition toward a QT planned as a full-cycle tool, rather than a temporary aberration, constitutes the doctrinal signature of regime 3.

Composition and the GDP ratio: two complementary reading keys

Tracking the WALCL level alone provides incomplete information. Two derived variables — instrument-level composition and the balance-sheet-to-GDP ratio — add analytical dimensions the raw ticker does not carry, and which change the practical interpretation.

Current composition, by late 2025, breaks down into ~$4.3 trillion of Treasuries, ~$2.3 trillion of agency MBS, and a residual of ~$200 billion across repos, primary credit and various facilities (FRED data for the week ending November 26, 2025). This structure differs radically from the pre-2008 composition, which was almost entirely Treasuries. The introduction of MBS into the Fed’s balance sheet dates back to QE1 (purchases launched in January 2009) and constitutes a doctrinal rupture that no other G7 central bank has truly replicated at this scale. The instrument-by-instrument breakdown of Fed assets reveals very different absorption dynamics between Treasuries and MBS, especially during the current QT phase.

This MBS specificity practically conditions what QT can do. Unlike Treasuries, which the Fed can let mature on a known schedule, MBS leave the balance sheet via prepayments that themselves depend on mortgage rates. In a regime with 30-year rates at ~7%, US households retain their existing loans and prepayments collapse. The -$35 billion monthly MBS cap authorized since June 2022 has almost never been hit in practice — actual MBS runoff has hovered between -$15 and -$20 billion per month according to NY Fed SOMA reports. The 2022-2026 QT is therefore structurally lopsided: it shrinks the balance sheet mainly via Treasuries, gradually shifting relative composition toward MBS.

The other complementary reading key is the WALCL-to-GDP ratio. Comparing the raw WALCL level to that of other central banks carries no economic information: $6.8 trillion does not mean the same thing in an economy with $27 trillion of GDP as in one with $6 trillion. For the Fed, this ratio went from ~6% in 2008 to ~38% at the March 2022 Covid peak, before retreating toward ~24% by late 2025 according to combined Fed and BEA data. Over the same period, the ECB peaked at roughly 70% of euro-area GDP at the height of the PEPP in 2022, and the Bank of Japan has held between 100% and 130% of Japanese GDP for the past decade.

These gaps are not statistical noise: they reflect three distinct monetary doctrines, three different structural constraints (public debt, banking-system size, reserve-currency status), and three asymmetric tightening windows. To position the Fed within this landscape, WALCL-to-GDP compared with ECB and BoJ benchmarks provides the relevant reading frame. Normalization by GDP eliminates the size effect and reveals that the Fed’s balance-sheet posture is, by late 2025, relatively moderate compared with its developed-market peers. The canonical FRED dataset itself, the official Fed balance sheet time series, allows full historical reconstruction of these dynamics.

The Treasuries/MBS asymmetry in the current QT phase produces a rarely explicit composition effect. If Treasuries leave the balance sheet faster than MBS (the case observed since June 2022 due to collapsed prepayments), the relative MBS share in WALCL rises structurally. According to estimates derived from SOMA data, the MBS share in WALCL went from roughly 30% at the April 2022 peak to roughly 34% by late 2025, despite a nominal reduction in the overall balance sheet. This drift modifies the Fed balance sheet’s effective sensitivity to mortgage rates: a 30-year rate move now acts on a wider fraction of the asset.

The maturity composition of held Treasuries is another rarely scrutinized key. According to SOMA reports published quarterly by the NY Fed, the maturity distribution by end-September 2025 shows roughly $280 billion of Bills (under one year), $2,300 billion of Notes (1 to 10 years), $1,100 billion of Bonds (over 10 years), and roughly $360 billion of TIPS and indexed securities. This breakdown conditions the effective runoff calendar: a large outstanding of 2-3 year Notes maturing in 2026-2027 provides the raw material for Treasury runoff in the current phase.

The interplay between maturity composition and runoff calendar is therefore a key second-order variable that strategists track when assessing Fed liquidity withdrawal pace.

WALCL must always be read at three parallel scales: absolute level (balance-sheet size), relative composition (Treasuries vs MBS vs residual), and maturity composition (which determines runoff mechanics). An analysis that mobilizes only one of these three scales produces analytical misreadings during transition phases.

The current phase: 2022-2026 QT runoff and landing

Since June 2022, WALCL has been contracting continuously. The Fed has cut its balance sheet from ~$8.97 trillion at the April 2022 peak to ~$6.8 trillion by late 2025, a drawdown of $2.2 trillion over three and a half years, according to weekly FRED WALCL data. The instrument is passive runoff: the Fed lets maturing securities roll off the balance sheet without reinvestment, within a fixed monthly cap. Securities exceeding the cap are reinvested (rolled); those within the cap effectively leave the balance sheet.

The initial cap, in force between June 2022 and May 2024, was set at -$95 billion per month: -$60 billion on Treasuries and -$35 billion on MBS. On May 1, 2024, the FOMC announced a reduction of the cap to -$60 billion per month, primarily by lowering the Treasury cap to -$25 billion. The MBS cap remained unchanged at -$35 billion, but as noted earlier, this cap is not binding: actual prepayments are markedly lower.

This modulation matters analytically. It signals that the Fed is approaching the floor level it targets for its balance sheet — the terminal balance sheet consistent with the ample reserves regime. Analyst consensus at the major houses (Goldman Sachs, JPMorgan, Morgan Stanley, BNP Paribas) converges on a zone of $6.0 to $6.5 trillion, without an official figure communicated by the Fed. Chair Powell indicated in May 2024 that the end of runoff would be announced “well before” bank reserves reached too low a level, without specifying a quantified target.

One critical variable conditions the landing: the Overnight Reverse Repo Program (ON RRP). This facility allows money market funds and other eligible counterparties to place cash at the Fed overnight at an administered rate. At the program’s peak, in December 2022, the ON RRP reached roughly $2.55 trillion according to the FRED RRPONTSYD series. By late September 2025, the same indicator had fallen to roughly $50 billion. This progressive collapse is not incidental: during most of the 2022-2024 QT, it is the ON RRP drawdown that absorbed the balance-sheet reduction, allowing bank reserves to stay nearly stable. The dedicated FAQ on QT market impact and the ON RRP / QT offset dataset document this absorption mechanism in detail.

When the ON RRP cushion is exhausted, as is the case in 2025, QT hits bank reserves directly. This is exactly the mechanic that led, in September 2019, to the repo crisis — a brief but severe episode during which overnight repo rates spiked by 200 to 600 basis points in hours, forcing the Fed to halt QT1 and resume purchases. Several structural differences distinguish today’s situation from September 2019: the Standing Repo Facility, created in July 2021, provides a permanent backstop against repo stress; bank reserves remain higher than in 2019; and the Fed has better-calibrated communication tools. Empirical observation of actual runoff pace, ON RRP level, and repo spreads forms the operational reading grid for this phase.

At the pace observed since the May 2024 adjustment (~$40-45 billion of actual monthly runoff), WALCL would reach the $6.0-6.5 trillion consensus range between the end of the first half of 2026 and early 2027. This projection is conditional on three variables: maintenance of the current cap, stability of MBS prepayments, and absence of a stress event forcing an interruption.

Comparison with the 2017-2019 QT1 provides the most instructive reading grid for the current phase. QT1 reduced the balance sheet from ~$4.5T to ~$3.8T between October 2017 and September 2019, roughly $700 billion over two years — an effective pace of ~$30 billion per month well below the cap authorized at the time. The episode ended abruptly on September 17, 2019, when overnight repo rates hit an intra-day peak of 10% while the effective Fed Funds rate sat at 2.30%, breaching the top of the Fed’s target corridor for the first time since the crisis. The Fed had to inject emergency liquidity via overnight and term repos, then resumed Treasury purchases in October 2019 under the “not QE” framing per official communication of the time.

Three structural differences distinguish today’s situation from September 2019. The first is the very existence of the Standing Repo Facility, created in July 2021 to provide a permanent cushion against stress. The second is the size of bank reserves themselves: ~$3.2 trillion by late 2025 vs ~$1.5 trillion in September 2019. The current cushion is more than twice as thick. The third, more subtle, lies in communicational learning: the FOMC now explicitly documents the expected end of runoff in its minutes and speeches, whereas in 2019 the official end was presented as a reactive response to repo tensions.

These differences do not guarantee an incident-free ending, but they modify the risk profile. A repeated repo crisis scenario as soon as ON RRP hits zero is not the central scenario for 2026; alternative scenarios include a pre-announced end of runoff, or a voluntary blocking of ON RRP at a positive floor as a preserved cushion. Empirical observation of the repo spread (SOFR vs IORB), deposits at the Fed, and Treasury Bill rates constitute the next early-warning indicators to monitor.

The terminal balance sheet question itself has not received a definitive answer from the Fed, only successive iterations. The May 2024 FOMC minutes were the first to articulate explicitly that the cap reduction served as an anticipation tool toward the end of runoff, not as a deceleration in response to immediate stress. Subsequent FOMC communication through 2024 and 2025 has refined the framework around three operational concepts: the floor of “ample” reserves (estimated but not officially quantified), the role of permanent facilities (SRF, IORB rate) as cushions, and the trade-off between balance-sheet size and balance-sheet composition flexibility. None of these concepts maps directly onto a target dollar figure; each constrains the trajectory differently.

What WALCL does not say: the frontier with market liquidity

Rigorous reading of WALCL requires precisely tracing what the ticker does not say. Conflating the Fed’s balance-sheet size with the effective liquidity available to market participants is one of the most structural analytical errors. The ticker measures the stock of assets held by the central bank; market liquidity measures the actual availability of cash circulating across the financial system. Three distinct mechanisms decouple them.

The first mechanism is the Treasury General Account (TGA). The US Treasury holds its operational liquidity on the liability side of the Fed’s balance sheet, in an account whose balance can vary by several hundred billion in a few weeks. When the TGA rises (the Treasury accumulates cash via debt issuance), it drains liquidity from the banking system toward the Fed without any WALCL movement. When the TGA falls (during a debt-ceiling episode for example), it returns that liquidity to the system, also without WALCL moving. Over 2023, the TGA rose by roughly $500 billion after the June 2023 debt-ceiling resolution, partially neutralizing the expansionary effect a stable WALCL would otherwise have produced. For the broader picture: the record of Fed easing into highs.

The second mechanism is the Overnight Reverse Repo. As described earlier, ON RRP drains several hundred billion dollars from the banking system toward the Fed’s liability side whenever money market funds judge that the administered rate offers better returns than market alternatives. The aggregate balance sheet does not move, but effective cash circulation contracts. The reverse holds during a drawdown phase.

The third mechanism stems from the very structure of MBS held by the Fed. A substantial fraction of these securities is held to maturity rather than actively managed at the margin. An accounting movement in their value does not translate an ongoing monetary policy intervention — it reflects structural prepayments that depend on independent variables (mortgage rates, refinancings, residential mobility).

Practical consequence: a stable WALCL can coexist with contracted system liquidity (rising TGA + full ON RRP), just as a falling WALCL can coexist with stable liquidity (the 2022-2024 QT absorbed by ON RRP drainage). This differentiated reading is the object of the Net Liquidity index = WALCL – TGA – ON RRP proposed by several analytical strands, whose in-depth examination is conducted in the long-form critique of WALCL as a liquidity proxy. For a synthetic introduction to the reading limits, what WALCL does not tell us enumerates the three critical mechanisms in a more condensed form.

The practical analysis of the WALCL/market-liquidity decoupling over the 2022-2025 period provides the most convincing empirical material. While WALCL dropped by over 25% in nominal value, financing conditions on repo markets (triparty repo, SOFR) remained relatively stable, with the SOFR-IORB spread compressed below 5 basis points most of the time. This stability rests entirely on the progressive ON RRP drawdown, which released collateral and liquidity back to the banking system at exactly the pace needed to offset runoff. A reading of WALCL alone would have predicted a liquidity crisis; effective financing indicators disproved that prediction.

This operational lesson changes how WALCL variations should be read in the post-2025 phase: the disappearance of the ON RRP cushion means that the same nominal WALCL variation will potentially have a more direct effect on financing conditions. WALCL’s explanatory power for predicting effective liquidity conditions mechanically increases as the cushion empties.

This dynamic feedback loop is itself relatively recent in the analytical practice of macro-finance professionals. It became fully visible only after the 2023 episodes when the partial decoupling between bank reserves and effective liquidity was empirically validated by the absence of repo stress despite continued QT. The lesson is that WALCL’s informational content is regime-dependent: in regimes with full ON RRP buffer, it overstates the contractionary effect; in regimes with depleted buffer, it understates it.

A practical implication for analysts entering this period is that the validity window of a WALCL-based reading shortens as the buffer thins. Before 2023, weekly WALCL changes could be treated as proxies for monetary impulse over multi-month horizons. From mid-2025 onward, the same weekly variations carry direct same-week implications for funding markets, demanding a higher monitoring frequency and a tighter cross-check with the H.3 series and the daily SOFR-IORB spread.

Reading WALCL in isolation is like trying to assess a hydraulic flow by measuring only the upstream pressure while ignoring the downstream valves.

Variables to watch and competing readings

Analytical use of WALCL in the current phase can be structured around three complementary variables to be tracked within a single reading grid, none of which is sufficient on its own.

The first variable is the actual runoff pace. The official cap (-$60 billion per month since May 2024) is not the quantity actually removed from the balance sheet: Treasury runoff depends on the effective maturity calendar, and MBS runoff depends on prepayments. The actual pace observed in 2025 has oscillated between $35 and $50 billion per month depending on the week, markedly below the theoretical cap. An acceleration toward the cap would signal a decline in mortgage rates (favoring MBS prepayments) or a heavier Treasury calendar.

The second variable is the ON RRP level. At $50 billion in September 2025 according to FRED RRPONTSYD data, ON RRP has practically exhausted its absorption capacity. A return toward zero or a durable block at this floor would signal that QT is now hitting bank reserves directly. This transition is the critical pivot point of the current phase. The Standing Repo Facility plays a preventive role here that it did not have in 2019.

The third variable is the level of bank reserves themselves, published weekly by the Fed in the H.3 series. The ample reserves regime concept assumes a minimum floor below which money-market conditions become volatile. Estimates of this floor range from $2.5 to $3.0 trillion depending on the analysis, but none are precise. The reserves’ proximity to this estimated threshold constitutes an operational alert signal.

Three competing readings can be made from these data. The first, dominant in macro strategy notes, treats WALCL as a monetary-stance indicator: balance-sheet size vs projected terminal size, convergence speed, signal on FOMC orientation. The second, carried notably by global liquidity analyses, makes Net Liquidity (WALCL – TGA – ON RRP) the relevant metric for anticipating marginal funding conditions. The third, more controversial but widely diffused in general media, establishes a direct correlation between WALCL and equity-market performance — a correlation discussed in dedicated analyses on the link between Fed balance sheet and equity markets and which deserves to be strongly qualified.

These three readings are not mutually exclusive, but they apply to different questions. Conflating the effective monetary stance with effective liquidity or with the equity-market signal produces durable analytical misreadings. WALCL is a necessary but insufficient ticker: at any moment, one must know what one is making it say. Companion analysis: how solvency and liquidity compare.

The debate open for 2026 and beyond bears on two distinct but intertwined questions: will the Fed manage to end its QT without a repo stress event, and what will the balance-sheet doctrine look like in a durable post-QT regime? The answers are not predetermined. Several trajectories remain open depending on the actual runoff pace, mortgage-rate evolution, and money-market reaction to the exhaustion of the ON RRP cushion.

Several counter-arguments dispute the very relevance of WALCL as a central indicator, and deserve to be heard. The first, carried notably by academic work on the fiscal theory of the price level, argues that the Fed’s balance sheet only has an impact jointly with fiscal policy; in a fiscal-dominance regime, WALCL becomes endogenous to Treasury behavior and loses its quality as an autonomous indicator. This critique is analytically important, especially when one observes the TGA variations described earlier, which blur the boundary between US monetary and fiscal policy.

The second counter-argument bears on balance sheet endogeneity in a high-reserve-floor regime: if the Fed commits to not letting reserves fall below an estimated threshold (~$2.5 to $3T), then the end of QT is not a discretionary decision but a mechanical consequence of liability-side evolution. Terminal balance-sheet size does not reflect monetary intent, but a plumbing constraint. This reading, if correct, weakens WALCL’s usage as an indicator of the monetary stance during landing phases.

The third counter-argument observes that the correlation between WALCL and equity performance, on which part of the media-readings rests, is unstable: strong over 2020-2022, weak or even negative over 2023-2024. A variable whose correlation with the tracked underlying is unstable is not a good proxy for that variable. This critique applies mostly to the third competing reading identified above, and less to the first two which do not claim to predict equity markets directly.

A useful framing for the period ahead is to read WALCL not as a target variable but as a constraint variable. The Fed does not optimize the size of its balance sheet for its own sake; it adjusts the balance sheet to maintain operational consistency with its rate corridor and its ample-reserves commitment. From this angle, WALCL becomes more informative when read jointly with the H.3 reserves series, the IORB-SOFR spread, and Treasury auction dynamics than when read as a standalone target. This integrated reading grid is what distinguishes professional analysis from the more reductive treatment WALCL receives in general media.

Rigorous analytical practice of WALCL therefore requires three disciplines: a definitional discipline (knowing what the ticker measures and what it does not), a contextual discipline (situating the current level within the relevant doctrinal regime), and a triangulation discipline (cross-checking with liability components and marginal financing indicators). None of these disciplines is trivial, and their absence probably explains the frequency of analytical misreadings on this subject in non-specialist commentary.

Looking forward, the most interesting analytical question is not whether the Fed will end its current QT, but what shape the balance sheet will take in the durable post-QT regime. A $6.0-6.5 trillion terminal would still leave WALCL at roughly 21-23% of US GDP, far above the 6% baseline that prevailed pre-2008. This durable expansion of the central-bank footprint relative to the economy carries doctrinal and institutional consequences that the analyst community has only begun to digest. The next decade will likely refine the reading grid established here, but the core proposition — that WALCL is a necessary but insufficient indicator, demanding triangulation — should remain valid across regime transitions.

- WALCL aggregates total assets held by the consolidated Federal Reserve System; it contains neither the liability side (reserves, ON RRP, TGA), nor the M2 or monetary-base aggregates, nor market liquidity.

- Three doctrinal regimes structure balance-sheet use since 2008: prolonged emergency tool (2008-2014 QE), rapid-response weapon (2020-2022 Covid QE), permanent variable-dosage lever (2022-2026 QT).

- The Fed WALCL-to-GDP ratio moved from 6% to 38% then 24% between 2008 and late 2025; international comparison requires this normalization rather than raw level.

- The current QT phase is approaching its consensus terminal balance sheet ($6.0-6.5T); ON RRP exhaustion (~$50 billion in September 2025) signals the transition to a QT that hits bank reserves directly.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…

Inverted Yield Curve: Reading a Regime Signal Without Immediate Effect

The inverted yield curve operates as a regime signal, not a timing tool. Its lagged effects are constitutive…