Dividends and Buybacks: Why Total Shareholder Yield Changes the Comparison

Dividend yield alone underestimates what equity holders actually receive. Adding net buybacks reshuffles the comparison between US and European firms, and exposes companies that distribute through one channel while diluting through the other.

Dividend yield alone underestimates what equity holders actually receive. Adding net buybacks reshuffles the comparison between US and European firms, and exposes companies that distribute through one channel while diluting through the other.

TL;DR

Total shareholder yield — dividends plus net buybacks — reshuffles equity comparisons both ways: it surfaces tech firms returning cash through share retirement and exposes buybacks erased by stock-based dilution.

- A firm yielding 1% in dividends but retiring 4% of its float each year delivers a 5% total shareholder yield, matching a utility paying a 5% dividend, and the headline ranking inverts.

- Per S&P Global, S&P 500 buybacks have run above dividends in recent quarters, in the low hundreds of billions each quarter; the inversion has been structural since the early 2000s while Europe stays dividend-led.

- Buybacks are procyclical: activity peaked in the quarters before the 2007-2009 and Q1 2020 drawdowns, and debt-financed buybacks amplify pressure when the rate cycle turns.

- Sustainability is what headline yield hides: a 7% yield in a pressured sector often precedes a cut, and the diagnosis runs through payout ratio, dividend-to-free-cash-flow and net debt, not the apparent yield.

Reading time: 6 minutes

Cash returned to equity holders flows through two channels: dividends and share buybacks. Treating them separately, or ignoring buybacks because they are less visible than a quarterly dividend, distorts any comparison between firms and between geographies. According to S&P Dow Jones Indices, the long-run contribution of reinvested distributions to total S&P 500 returns is decisive once the horizon stretches beyond a decade — substantially more than price appreciation alone over multi-decade windows. Understanding how the two channels interact, and how the cycle distorts both, refines equity analysis without converting it into investment advice. Related coverage: our analysis of dividend-stock selection.

The Dividend: Recurring Income and Confidence Signal

A dividend is the slice of profit a board chooses to distribute rather than reinvest. The decision encodes a trade-off the firm makes explicit: does management believe internal capital allocation will return more than what shareholders could redeploy themselves? When the answer is no, distribution becomes the rational option.

For shareholders, the dividend delivers cash that is independent of price action. It also functions as a signal. Initiating or raising a dividend communicates confidence in the durability of earnings; cutting one almost always reads as an admission of stress. Academic and central-bank work on signaling theory (Lintner’s seminal model and its successors) has long documented that markets react asymmetrically and that cuts tend to be punished sharply in the days following the announcement. The wider context: how buybacks and dividends compare.

This signaling function explains why management resists cutting dividends, even when earnings have weakened. Executives often prefer to maintain a stable distribution by drawing on cash reserves or adding debt rather than send a negative signal to the market. The result is a temporal disconnect: distributed flows lag real earnings, smoothing the visible cash return over cycles where underlying profitability is far more volatile.

Dividend Yield: Interpretation and Limits

The dividend yield divides the annual dividend by the share price. A 4% yield means an equity holder receives four euros in cash for every hundred invested at the current price. The ratio enables comparison across stocks, sectors, and asset classes — including the implicit yield of long-dated bonds. A complementary angle: whether dividend stocks protect against inflation.

The metric breaks down in two opposite directions. A high yield can be the optical consequence of a falling share price anticipating a cut — the classic yield trap. Sectors facing structural headwinds (utilities saddled with stranded assets, tobacco names under regulatory pressure, banks during balance-sheet repair) routinely display yields that look attractive precisely because the market doubts their sustainability. A low yield, conversely, can reflect superior internal compounding: US tech megacaps spent two decades returning very little in cash while building dominant franchises that delivered the bulk of equity returns through buybacks and price appreciation.

Ranking stocks by headline dividend yield. A 7% yield in a sector under structural pressure often signals an impending cut rather than a bargain. The relevant sustainability check combines the payout ratio, the dividend-to-free-cash-flow ratio, and the trajectory of net debt — not the apparent yield level.

A share buyback is the other major channel of capital return. The firm uses cash to repurchase its own shares on the open market and then retires them. The operation reduces the share count, mechanically lifting earnings per share and each remaining shareholder’s claim on the underlying business. Nothing about the operating business changes; the residual claim concentrates.

Buybacks offer two practical advantages over dividends. They are flexible: a firm can throttle or pause its repurchase program without sending the same negative signal that a dividend cut triggers. They also benefit from tax treatment that is, in most jurisdictions, more favorable to long-term holders, since capital gains are typically taxed only on realization and often at lower rates than dividend income.

According to S&P Global, S&P 500 firms have routinely deployed more cash into buybacks than into dividends in recent quarters, with quarterly buybacks running in the low hundreds of billions of dollars. The historical inversion took shape in the early 2000s and has since become structural. To grasp how these flows shape equity returns and interact with the cycle, the broader picture of how distribution policies move through expansion and contraction provides the complementary framing.

Buybacks attract growing criticism, and the arguments deserve to be taken seriously rather than dismissed.

First, sustained buybacks can mask the absence of growth opportunities. A firm that repurchases aggressively is implicitly conceding it cannot find a better use for its capital — research, acquisitions, productive investment. Second, buybacks are often financed by debt, especially when the cost of capital is low. The strategy optimizes return on equity as long as the after-tax cost of debt remains below the return on capital. When the rate cycle turns, that arithmetic flips: leveraged firms face higher interest charges precisely when earnings come under pressure — a dynamic that becomes legible when read alongside how phases of the rate cycle transmit to corporate financing.

Third, executive compensation tied to EPS targets creates an incentive to lean on buybacks for cosmetic reasons: a buyback raises EPS mechanically, even if operating performance has not improved. Fourth, buybacks are empirically procyclical: firms repurchase more when their shares are expensive and less when they are cheap, the opposite of what rational capital allocation would suggest. The 2007–2009 episode and the 2020 first quarter both showed peak buyback activity in the quarters preceding sharp drawdowns.

Debt-financed buybacks act as a double-edged lever. They amplify per-share returns when rates are low and earnings are rising, and amplify the pressure on equity holders when rates rise, earnings weaken, or both compress at once.

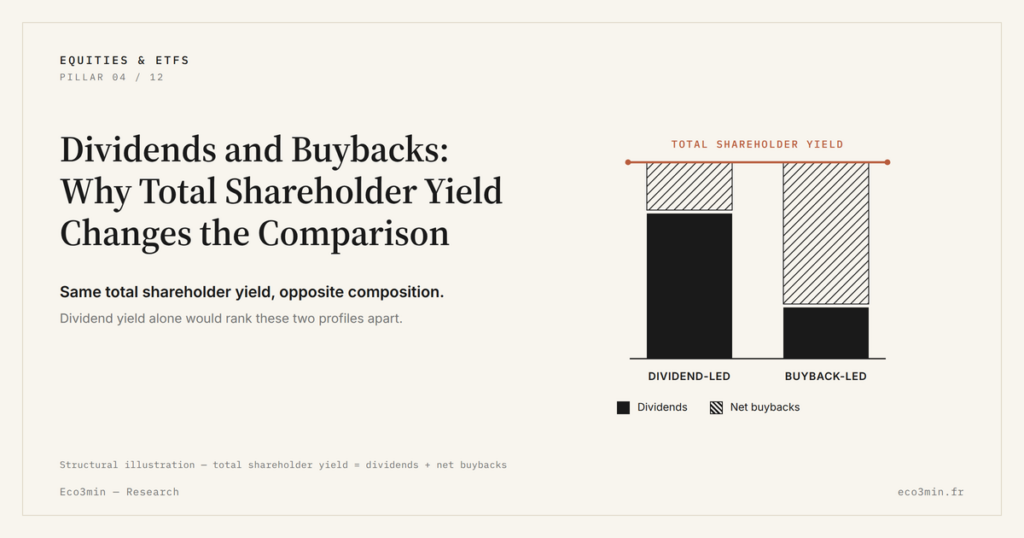

The corrective metric is total shareholder yield: dividends paid plus net buybacks (buybacks minus new share issuance), divided by market capitalization. The construction is simple; what it changes in cross-sectional comparisons is not.

Two examples make the point. A tech firm with a 1% dividend yield that retires 4% of its float each year delivers a 5% total shareholder yield, comparable in magnitude to a utility with no buybacks but a 5% dividend. The headline yield ranking inverts. Conversely, a firm with a nominal buyback program but heavy stock-based compensation can show a high gross buyback figure that net issuance erases entirely — the optical buyback delivers nothing to existing shareholders. Total shareholder yield catches this dilution, where dividend yield alone is silent on it. Related Q&A: the role of buybacks in shareholder yield.

Sustainability and the Business Cycle

For both channels, the central question is sustainability. Three indicators frame the diagnosis: the payout ratio (dividends to net income), the dividend-to-free-cash-flow ratio (which strips out non-cash charges), and the path of net debt. A payout ratio durably above 100% means the firm is distributing more than it earns — viable for a quarter or two, structurally impossible over years.

Distribution policies move with the cycle, but with a measurable lag. In expansion, profits rise and distributions follow gradually. Late in the cycle, both reach their peak — and so do buybacks, often at the worst possible prices. In contraction, earnings drop first, then buybacks are suspended (the flexible channel), and only as a last resort are dividends cut. This sequencing explains why dividend cuts tend to cluster after the worst of a recession has already passed, lagging the trough of the cycle by several quarters. Protecting the dividend before protecting investment reveals a precise ranking of claimants, the one installed by the shareholder primacy doctrine.

Geographic divergence remains stark. In the United States, buybacks dominate cash returns by a wide margin and have done so for two decades. In Europe, the dividend culture remains entrenched — institutional mandates, pension fund liabilities, and tax regimes all favor regular cash distributions over share retirement. The implication is that a like-for-like comparison of US and European equity returns requires aggregating both channels: the dividend-yield gap that headline statistics show overstates the actual difference in cash returned to holders.

Total shareholder yield corrects the geographic illusion: the US-Europe gap in cash returns shrinks once buybacks are added, and inverts for some sector pairs.

- Dividends deliver visible cash and signal management confidence in earnings, but headline yield can mask a coming cut when sustainability is not tested.

- Buybacks have become the primary channel of cash return in the US; their flexibility is a feature, debt financing of buybacks is a vulnerability at rate-cycle turns.

- Total shareholder yield — dividends plus net buybacks — corrects the picture in both directions: it surfaces tech firms that distribute heavily through retirement, and exposes firms whose buybacks are offset by stock-based dilution.

- Distributions are procyclical and lagged: they peak late in the cycle, suspend in contraction (buybacks first), and cut dividends only as a last resort — typically after the trough.

Last updated — 30 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Equal-Weight ETFs: The Quiet Signal Behind Rising Indices

Equal-weight ETFs reveal the true health of the equity market behind mega-cap-driven indices. Their gap with cap-weighted ETFs…

Smart Beta ETFs: The Hidden Risk Behind Factor Performance

Smart beta ETFs now hold ~15-20% of global equity ETF assets. Stacking factor exposures often rebuilds hidden concentration…

Equity Profit Warnings: Risk and Opportunity After the Alert

Profit warnings have become accelerated stress tests in a higher-cost-of-capital regime. How equity risk reconfigures and where structural…