Fed Funds, 2024-2026 Cutting Cycle: Triangulating the Readings and an Observation Framework

The Fed Funds cutting cycle initiated in September 2024 sits within the post-disinflation normalization phase. As of May 2026, three readings coexist on the current 4.25-4.50% level — none of them decisive.

TL;DR

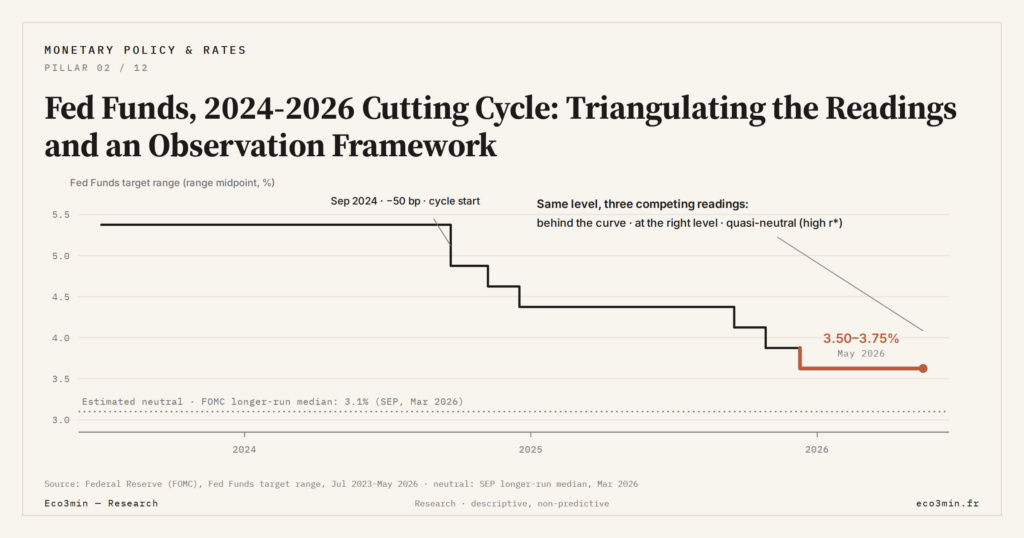

Since September 2024 the Fed cut 100 bp (a 50 bp opening, then two quarter-points) and held through 2025, leaving the 4.25–4.50% rate open to three rival readings. This thread is taken further in the ECB versus Fed policy gap.

- The 50 bp September 2024 opening doubled the usual normalization step, followed by 25 bp in November and December; the median SEP projection for end-2025 drifted from 3.50% (March 2025) to 4.25% (December 2025).

- The three readings split on r-star: Fed still behind (a 125–150 bp gap to the 3.00% neutral median, Summers, Goldman), at the right level (core PCE at 2.7%, supercore 3.5–4.0%), or quasi-neutral if r-star is 1.5% (Bauer-Rudebusch).

- The same observable data feed all three: with output gap near zero, the Taylor prescription spans 3.75–4.55% across r-star estimates, placing the 4.25–4.50% rate inside the range and settling nothing.

This article describes the chronology of FOMC decisions, exposes the three competing readings (behind / ahead / r-star adjusted), and offers an observation framework for the variables that will inform the debate — without terminal rate forecast.

1. Descriptive Chronology of the Cutting Cycle Since September 2024

The 2024-2026 Fed Funds cutting cycle began in September 2024 with an unusual FOMC decision. After fourteen months on a plateau at 5.25-5.50% (July 2023 – September 2024), the FOMC opened the cutting cycle with a 50-basis-point decision — an exceptional opening step size for a normalization cycle, generally initiated with 25 bp. The target range thus moved to 4.75-5.00%. The official motivation, expressed in the FOMC statement and confirmed at the Powell press conference, invoked a rebalanced equilibrium between inflation risks (converging) and employment risks (in slow deterioration). Related study: Our US monetary-policy meeting calendar.

Two 25 bp decisions followed at the November 2024 meeting (target range to 4.50-4.75%) and December 2024 meeting (target range to 4.25-4.50%). The inaugural sequence of the cycle thus totals 100 basis points of cuts over the final three meetings of 2024. The first decision of the cycle is documented in the daily FEDFUNDS history on FRED.

2025, by contrast, is characterized by a prolonged plateau. No FOMC cut occurred throughout 2025, placing Powell in a pause posture after the inaugural cuts. This pause is documented by successive 2025 SEP dot plots, which saw the median Fed Funds end-2025 projection progressively revised upward — moving from approximately 3.50% at the March 2025 SEP to 4.25% at the December 2025 SEP, signaling an FOMC expectation of a higher terminal than initially projected. The internal FOMC debate on the reasons for this pause documents several factors: core PCE settled at a plateau around 2.7% without fully converging to the 2% target, persistent services CPI, still-resilient labor market despite slow deterioration, financial conditions measured by the Chicago Fed NFCI in a neutral neighborhood. Adjacent reading: the drivers behind policy-rate decisions.

As of May 2026, the Fed Funds target remains at 4.25-4.50%, that is 100 bp below the July 2023 peak (5.25-5.50%) and 425 bp above the 2020-2022 floor (0.00-0.25%). The March 2026 SEP signals a median projection of 3.75-4.00% for end-2026, that is 50 to 75 bp of additional cuts anticipated by the FOMC by December 2026 — median projection, with wide dispersion across the 19 dots.

The 2024-2026 cycle therefore hybridizes several analytical categories from the analytical typology of Fed Funds cycles: post-disinflation normalization component, with moderate pace (100 bp over 4 inaugural months then pause) and an intermediate trigger between pure normalization and the start of recalibration. This hybridization is the object of the debate documented below.

2. The Three Competing Readings of the Current Cycle

Three readings of the 2024-2026 cycle coexist in contemporary economic and financial literature. None imposes itself as dominant — their coexistence reflects objective uncertainty on the structuring parameters.

First reading: Fed Funds still behind the curve. This reading observes that the nominal Fed Funds at 4.25-4.50% remains significantly above the neutral Fed Funds estimated by most models (FOMC longer-run median at 3.00% via SEP). The 125-150 bp gap between observed and median neutral signals that policy remains materially restrictive. Combined with core PCE already at 2.7% and labor market leading indicators in slow deterioration (Sahm Rule near triggering threshold, modest rise in unemployment rate from 3.8% in 2024 to 4.1% in early 2026), this reading concludes that the Fed has remained too restrictive for too long and that the cutting phase should accelerate. This reading is held by several economists (Larry Summers, certain bank-side analyses such as Goldman Sachs Research) and is partly validated by Fed Funds futures contracts which price approximately 75 bp of cuts over the 12-month horizon in May 2026. Data reference: Our Sahm-rule dataset.

Second reading: Fed Funds at the right level to bring inflation to target. This reading observes that core PCE remains at 2.7%, that is 70 bp above the explicit Fed 2% target. Services CPI ex-housing (Powell has called this sub-index “supercore” since 2022) remains persistent around 3.5-4.0% annualized. The labor market’s resilience (unemployment 4.1%, NAIRU Fed staff at 4.0-4.4%) signals that the gap to the inflation target has not yet fully materialized the slowdown necessary for its convergence. Under this reading, the Fed Funds at 4.25-4.50% is precisely the level required to bring inflation to mandate without yielding to premature accommodation that would rekindle the inflationary cycle. This reading is held by several more restrictive FOMC members (“hawkish” reading) and echoes the prolonged 2025 plateau.

Third reading: Fed Funds quasi-neutral under high r-star estimate. This reading mobilizes the open r-star debate and its stance implications: if r-star has durably climbed to 1.5% (Lubik-Matthes estimate, several academic contributions 2024-2026), the nominal neutral Fed Funds stands at 4.2%. The observed Fed Funds at 4.25-4.50% is then only 5 to 30 bp above neutral — quasi-neutral policy. The chain of effects is traced in the framework for reading secular stagnation regimes. Under this reading, neither the behind-the-curve reading nor the restrictive-right-level reading is relevant: the Fed is already essentially neutral, and the trajectory could be a prolonged plateau without substantial additional cuts. This reading emerges in certain recent analyses (Bauer-Rudebusch via TIPS forwards, certain 2024-2026 FOMC minutes where members mention a nominal neutral above 3.00%), without dominating institutional discourse.

The three readings share the same observable data. They diverge on the value retained for r-star, on the lagged effect of cumulative restrictive policy, and on the assessment of services CPI persistence. None of the three can be settled by the data available alone in May 2026.

3. What Observable Data Says — Without Pre-deciding

Several observable variables inform the debate without closing it. Their joint reading allows identifying what the data factually say, distinct from what analysts infer from them.

Core PCE at 2.7% in April 2026 (Bureau of Economic Analysis): 70 bp above the 2% target, but 250 bp below the June 2022 peak of 5.2%. The disinflation trajectory is clear, its final convergence speed has slowed.

Services CPI ex-housing (supercore) at 3.5-4.0% annualized on 6-month moving average (Bureau of Labor Statistics): documented persistence, attributed by several analyses to wage rigidity in certain services. This measure is closely followed by the FOMC in its communications since 2022.

Unemployment rate at 4.1% in April 2026 (Bureau of Labor Statistics): 30 bp rise over 12 months, Sahm Rule signal near the triggering threshold without materially crossing it as of May 2026.

10Y – Fed Funds spread: the short slope of the yield curve, a key indicator for calibrating restrictive stance, has been converging since the 2023 inversion peak. The point-by-point detail of the series is tracked in the yield curve slope vs Fed Funds dataset.

r-star: no directly observable variable. Current estimates dispersed between 0.7% (certain HLW vintages) and 1.5% (Lubik-Matthes), with implicit FOMC median at 1.0%.

Steering by central-bank rate steering and r-star in the Taylor prescription for the current cycle: the Taylor prescription under the retained assumptions gives i = r-star + 2.7 + 0.5 × 0.7 + 0.5 × output_gap. With output gap near zero, Taylor 1993 prescription = r-star + 3.05. So 3.75% (r-star = 0.7%) to 4.55% (r-star = 1.5%). The observed Fed Funds at 4.25-4.50% is within the Taylor range depending on the retained r-star estimate — policy is neither clearly behind nor clearly ahead under high r-star estimates.

SEP dot plot longer-run at 3.00% (March 2026): FOMC median projection of nominal neutral Fed Funds. Subtract π* = 2% → implicit FOMC r-star = 1.00%. But intra-FOMC dispersion (2.50-3.75%) remains wide.

The gap between observed Fed Funds (4.25-4.50%) and the retained nominal neutral level determines the perceived restrictive stance. Depending on the estimates, this gap ranges from a few bp (quasi-neutral stance) to 150 bp (modestly restrictive stance). The Fed reaction function thus materially depends on the retained neutral estimate.

4. Indicators to Observe — Non-prescriptive Pattern

Several indicators are regularly followed to inform the cycle reading, without any of them allowing a prescriptive forecast. Their joint observation allows tracking the debate’s evolution without settling it.

Core PCE and services CPI ex-housing trajectory: sustained convergence or re-acceleration. Stable convergence to 2% reinforces the “Fed can accelerate” reading; re-acceleration reinforces the “Fed must maintain” reading. Monthly BLS publications (CPI) and monthly BEA publications (PCE) are the reference sources.

Labor market leading indicators: Sahm Rule, U-3 and U-6 unemployment, NFP, JOLTS openings and quits. A material crossing of the Sahm Rule threshold (0.5-point rise of 3-month moving average unemployment vs 12-month minimum) historically signals a labor market tipping point.

Quarterly FOMC meetings and SEP: Fed Funds decisions, FOMC statement, Powell press conference, dot plots revised every 3 months (March, June, September, December). Longer-run medians and end-of-year medians of dots are the official forward markers of the reaction function.

Institutional r-star estimates: quarterly HLW publications (NY Fed), irregular Lubik-Matthes publications (Richmond Fed) and Bauer-Rudebusch (San Francisco Fed). Any substantial revision of one of these estimates modifies the stance diagnostic.

Financial conditions: Chicago Fed NFCI and Goldman Financial Conditions Index. A material easing of conditions without corresponding FOMC cut can signal “stealth easing” that modifies the stance diagnostic even at unchanged Fed Funds.

CME Fed Funds futures market: market pricing for FOMC decisions at 3, 6, 9 and 12 months. These implicit probabilities are a market consensus measure, distinct from the FOMC SEP median. The gap between the two informs on information or judgment asymmetry between Fed and market.

Joint monitoring of these variables allows identifying potential tipping points — without forecasting their direction or timing. For the integrated reading of Fed Funds within its ecosystem — where the 2024-2026 cycle is only one phase among others — see the FEDFUNDS analytical hub.

- The 2024-2026 Fed Funds cutting cycle began in September 2024 with a 50 bp cut (followed by 25 + 25 bp), before a prolonged plateau over 2025. As of May 2026, the target remains at 4.25-4.50%; the March 2026 SEP signals 50-75 bp of additional cuts anticipated by the median FOMC by December 2026, with wide dispersion.

- Three competing readings coexist: (1) Fed still behind the curve, cuts should accelerate; (2) Fed at the right level to bring inflation to mandate, the plateau is necessary; (3) Fed quasi-neutral under r-star = 1.5% estimate, neither behind nor ahead. The three mobilize the same observable data and diverge on the retained r-star value.

- Observable data (core PCE 2.7%, supercore 3.5-4.0%, unemployment 4.1%, SEP longer-run 3.00%) inform the debate without settling it. The Taylor prescription yields 3.75-4.55% depending on the retained r-star: the observed Fed Funds is within the range.

- The observation framework tracks core PCE, supercore, labor market (notably Sahm Rule), quarterly SEP, institutional r-star revisions, financial conditions (NFCI), Fed Funds futures pricing. None of these indicators alone allows an isolated terminal rate forecast.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…