Marginal Production Cost and Commodity Price Equilibrium

Marginal cost anchors commodity prices over the long run, but inertia, lead times and inventory dynamics allow market prices to deviate persistently. This analysis examines the conditions under which such gaps remain sustainable.

The marginal cost of production is the principal long-term economic anchor of commodity markets. It defines the viability threshold of installed capacity, shapes investment decisions and structures supply adjustment cycles at both sectoral and macroeconomic levels.

TL;DR

Marginal production cost anchors commodity prices over the long run, but prices can stay decoupled from it for years whenever variable costs remain covered and inventories absorb the gap.

- Marginal cost is the cost of the least efficient unit still needed to meet demand; prices durably below it shut that capacity down, prices above it revive deferred projects.

- In industrial metals, all-in cost estimates rose roughly 20 to 35% between 2019 and 2025, driven by input inflation and tighter financial conditions.

- Since late 2024, positive real interest rates have made the cost of capital a central determinant: projects no longer clear once the real discount rate stays durably above 2 to 3%.

- Existing capacity keeps producing as long as prices cover variable costs, which is why prices can sit below total marginal cost without an instant supply cut.

Over short and medium horizons, however, market prices can deviate persistently from this anchor under the combined effect of productive inertia, lead times, cost structure and inventory dynamics. Conflating observed prices with instantaneous production cost therefore leads to recurring interpretation errors. This analysis examines the role of marginal cost in the formation of commodity equilibrium prices and the conditions under which deviations remain sustainable. The corresponding material is set out in our breakdown of commodity price formation.

Marginal cost as a long-term economic anchor

In extractive and agricultural industries, marginal cost corresponds to the cost borne by the least efficient production unit still required to meet aggregate demand. As long as market prices remain durably below this threshold, marginal capacity is progressively shut down. Conversely, prices above the aggregate marginal cost make previously unviable projects economic, triggering a deferred investment cycle.

Over the long run, this mechanism explains why prices tend to gravitate around a moving marginal cost, itself shaped by wages, energy, taxation and the cost of capital. In industrial metals, aggregate all-in cost estimates rose by roughly 20 to 35% between 2019 and 2025, driven by the combination of input inflation and tighter financial conditions.

Why prices deviate persistently

In the short run, marginal cost is not an immediate anchor. Existing capacity continues to produce as long as prices cover variable costs, even when total cost is breached. This inertia explains extended periods during which prices remain below long-term marginal cost, without any instant supply response.

Conversely, during tight phases, prices can substantially exceed marginal cost without supply reacting quickly. Lead times, often spanning five to ten years in mining and energy sectors, create a structural lag. This point is closely tied to the broader trade-off between physical supply and financial demand, which explains why price signals run well ahead of physical adjustments. A broader view: the stock-to-flow decomposition applied to the yellow metal.

This gap between market price and marginal cost is largely absorbed by inventory movements. As long as physical reserves exist, the market can tolerate prices durably above the economic threshold without an immediate supply response. This mechanism is examined in detail in the analysis dedicated to the role of inventories in commodity price formation, which shows how inventories delay or amplify the transmission of price signals to production.

A backdrop that restores marginal cost as a binding constraint

Since late 2024, the persistence of positive real interest rates has reshaped the hierarchy of viable projects. The cost of capital has once again become a central determinant of effective marginal cost. Projects previously profitable on the basis of high prices are no longer so when the discount rate stays durably above 2 to 3% in real terms.

This shift makes marginal cost a more discriminating anchor than during the prior decade. It does not imply an immediate price alignment, but raises the probability of a gradual adjustment when demand slows or inventory tensions ease.

Mainstream consensus and alternative reading

Part of the consensus holds that market prices primarily reflect cyclical demand pressures, relegating marginal cost to a secondary variable. This reading assumes that supply can adjust quickly once prices deviate too long from fundamentals.

An alternative reading places greater emphasis on cost heterogeneity and financial rigidity. The same reasoning is carried over to silver in how most silver comes out of other metals’ mines. As long as the highest-cost producers remain operational for contractual, regulatory or strategic reasons, prices can stay durably decoupled from theoretical marginal cost. The relevant variable is therefore not the average cost level, but the shape of the cost curve and the speed at which marginal capacity exits. Related framing: the split between arabica and robusta.

What readers really want to understand

The actual question is not whether a price is “expensive” or “cheap” relative to marginal cost, but whether the observed gap is sustainable over time. Behind this question lies the concern of mistaking a transient anomaly for a structural imbalance, when adjustment mechanisms remain slow.

What could invalidate this reading

Several factors could weaken marginal cost’s anchoring role. Rapid technological innovation that materially lowers unit costs would shift the equilibrium threshold. Likewise, a sharp negative demand shock could force accelerated closures, even where variable costs remain covered. Targeted regulatory or fiscal interventions can also artificially keep capacity online beyond its economic viability.

Observable economic implications

When prices deviate durably from marginal cost, the effects spread well beyond the sector concerned. Consumer firms face heightened input volatility, while producing countries see their revenues become more unstable. At the macro level, these gaps influence imported inflation and current account balances, which is why commodities remain a central lens for reading the global economy, as detailed in the pillar page Commodities and the global economy.

Friction points worth keeping in mind

- Marginal cost anchors prices over the long run, not short-term fluctuations.

- Investment lead times and the cost of capital determine the speed of adjustment.

- A persistent gap is not a sufficient signal absent an analysis of cost-curve structure.

This is not the central scenario adopted by all market participants, but the reading helps explain why prices can remain durably detached from marginal cost without an immediate correction. The risk is less visible than an abrupt shock, but more persistent, because it rests on financial and industrial mechanisms that resolve slowly.

Does marginal cost always set a price floor?

It acts as a long-term threshold, but lower prices can persist as long as variable costs remain covered.

Why do some producers continue operating at a loss?

Because shutting down often entails fixed or social costs greater than the temporary operating loss.

Does the cost of capital directly influence marginal cost?

Indirectly yes, by reshaping project viability and therefore the marginal segment of supply.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

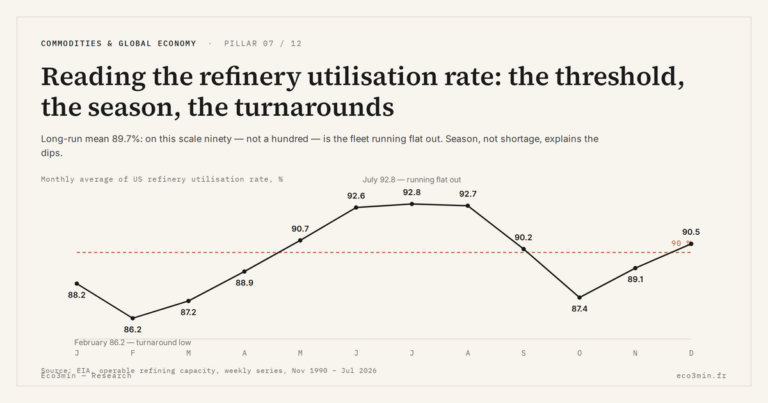

Full pillar →Reading the refinery utilisation rate: the threshold, the season, the turnarounds

A refinery runs full near ninety percent, not a hundred: the last slice of nameplate capacity is a…

IMO 2020: the regulatory shock that rewrote product spreads

An environmental rule on marine sulfur can move a refining spread more than a swing in crude. IMO…

The 2022–2023 refining golden age: anatomy of an episode

In 2022, refined fuel prices climbed faster than crude. That gap, measured by the 3-2-1 crack spread, reached…