Real Estate vs Financial Assets: Two Incomparable Balance-Sheet Logics

Comparing real estate and financial assets through gross yield alone misses leverage, liquidity, taxation, and horizon. Two distinct balance-sheet logics that don’t translate into each other.

Comparing real estate and financial assets through gross yield alone misses leverage, liquidity, taxation, and horizon. Two distinct logics, not interchangeable.

TL;DR

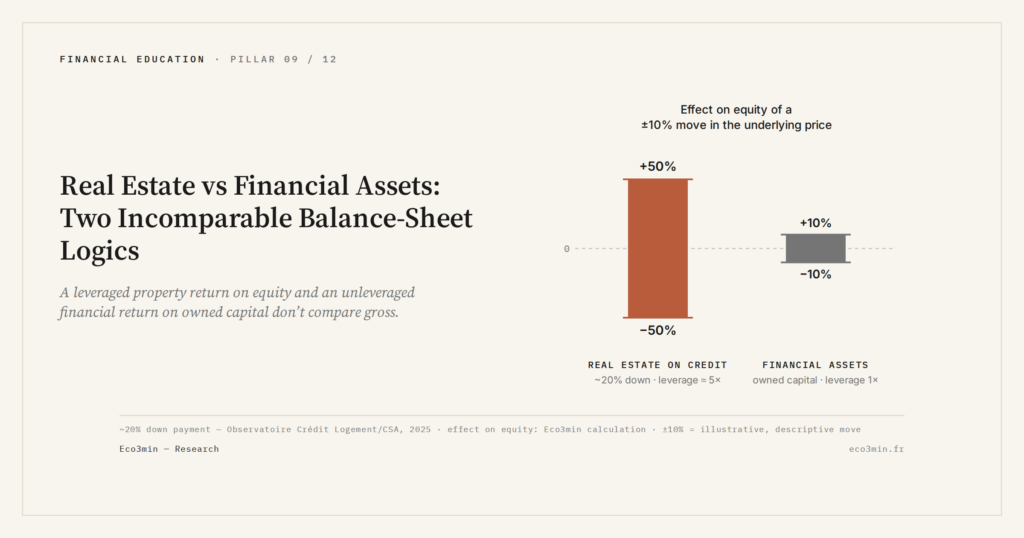

Bank leverage averaging above 80% of a French property's price turns real estate into an amplified position, making its return non-comparable to an unleveraged equity yield.

- On a €300,000 purchase with €60,000 of equity, a 10% price move swings equity by 50% either way, an amplification absent from an unleveraged ETF that tracks the market one-for-one.

- Selling listed equities takes seconds; a French home takes three to six months on average plus two to three months of notarial steps (FNAIM, 2025), and cannot be sold in 5% slices.

- Over 1988-2023 the MSCI World returned about 8% annualized in euros against 3-5% for French residential real estate (Notaires-INSEE), before leverage, taxation and owner-occupier implicit rent.

- Both track the rate cycle through different channels: French transaction volume fell 22% between 2022 and 2023 under tightening (Notaires de France), while equities reprice via earnings multiples.

A balance sheet distinguishes assets along several axes: liquidity, horizon, taxation, leverage, exposure to the cycle. Real estate and financial assets sit at almost opposite positions on each of these axes. Comparing their gross yield, as one would between two funds, ignores everything that determines their behavior in a real-world context. Bank leverage transforms real estate into an amplified position. The instant liquidity of financial markets allows adjustments impossible in bricks and mortar. These structural differences, not past performance, ground the distinction between the two logics.

Leverage: an amplifier that changes the nature of the yield

Residential real estate is mostly acquired on credit. In France, the loan share in financing a real estate acquisition averages above 80%, according to data from the Observatoire Crédit Logement (Q3 2025). This bank leverage radically transforms the yield profile. A €300,000 purchase financed with a €60,000 personal down payment exposes the buyer to a multiplier effect: a 10% price increase represents a €30,000 gain on €60,000 of capital committed — a 50% return on equity.

The effect operates in both directions. A 10% drop produces a 50% loss on the initial capital. Real estate on credit is structurally a leveraged position, with a real volatility on equity well above what the nominal price of the property suggests. Financial markets, by contrast, mostly operate on owned capital for retail investors. An ETF portfolio bought without leverage tracks the market exactly, without amplification.

This asymmetry is what makes the comparison between real estate yield and equity yield structurally misleading. One compares a leveraged return on equity with an unleveraged gross return — two incommensurable quantities. The broader framework these arbitrages belong to overlaps with the one set out in the three patrimonial vehicles and their evaluation criteria.

Liquidity: an invisible cost in bricks and mortar

Selling a portfolio of listed equities takes seconds. Selling a residential property takes on average three to six months in France (FNAIM data, 2025), excluding two to three additional months for notarial procedures. The difference is not anecdotal. It means that real estate cannot be adjusted quickly in response to a change of circumstances — relocation, separation, urgent liquidity need.

On financial markets, liquidity also enables an allocation granularity impossible in real estate. An investor can sell 5% of a portfolio without touching the rest. An owner cannot sell 5% of an apartment. This indivisibility creates a concentration risk that listed assets avoid by construction. The effect of what liquidity changes about real risk is particularly marked in periods of stress: the financial investor adjusts, the property owner endures. Related analysis: the Eco3min study of our hub of financial simulators.

- Comparing a real estate yield that includes bank leverage with an equity yield on owned capital, without correcting for the asymmetry.

- Ignoring real estate transaction costs (7 to 10% on purchase, 3 to 6% on resale) when computing net performance, while no significant equivalent exists in equity markets.

Taxation: two regimes, two accumulation logics

The tax regimes applicable to real estate and financial assets differ deeply in France. The primary residence enjoys full capital gains exemption on resale — a tax advantage with no equivalent in the financial sphere. Rental real estate, by contrast, is subject to a capital gains regime that tapers with holding period, with full exemption after 22 years for income tax and 30 years for social contributions.

Financial assets held in a PEA (French equity savings plan) benefit from reduced taxation after five years of holding. In life insurance contracts, tax allowances kick in after eight years. The ordinary securities account applies the 30% flat-rate withholding on capital gains and dividends, with no duration condition. That flat-rate withholding has a crossover with the progressive scale, mapped in where progressive tax overtakes the flat rate.

These tax gaps radically alter net yield. A property held for twenty-five years and resold under full capital gains exemption produces a net yield very different from the same nominal gain subject to the 30% flat-rate withholding. Conversely, a PEA portfolio held for ten years carries a reduced tax burden that rental real estate cannot match over the same horizon. The comparison can only be meaningful on a net-of-tax basis — a calculation few comparators integrate correctly.

Horizon: the factor instant comparison ignores

Real estate is structurally a long-horizon asset. High entry costs — notary fees of 7 to 8% on existing property — impose a minimum holding period of five to seven years simply to amortize transaction costs, according to Banque de France estimates (2024). Below that threshold, the probability of a net loss is high, regardless of price evolution.

Listed financial assets do not carry this minimum-horizon constraint. Their liquidity and low transaction costs make them suitable for a range of horizons spanning very short to very long term. Over long periods, global equities have historically outperformed real estate in nominal gross yield — the MSCI World Index produced around 8% annualized in euros over 1988-2023, against 3 to 5% for French residential real estate according to the Notaires-INSEE indices. But this comparison omits leverage, taxation, and the implicit rent of the owner-occupier, which substantially modify the real balance. On the same theme: listed versus unlisted real estate.

The relevant question is not real estate or equities, but what structural role each asset class plays in the household balance sheet — and the two answers are not mutually exclusive.

The angle few analyses highlight involves the correlation between these two asset classes and the rate cycle. Real estate is directly sensitive to credit conditions — transaction volume in France fell 22% between 2022 and 2023 under the effect of monetary tightening, according to data from the Notaires de France. Equity markets, in turn, react to rate expectations through the channel of earnings multiple valuation. In a rising-rate phase, both asset classes suffer — but not for the same reasons, not on the same timeline, and not with the same capacity to adjust.

Understanding these structural divergences reshapes the way one thinks about the composition of household wealth. The logic is not to choose between real estate and financial assets, but to grasp why the two obey distinct mechanics — and why spreading exposures rather than vehicles produces a more coherent patrimonial outcome. These arbitrages belong to the broader framework of recurring patrimonial decisions that commit long-term allocation.

- Real estate operates with bank leverage (around 80% loan share on average), which amplifies both yield and risk on equity — retail financial assets mostly operate without leverage.

- Liquidity, taxation, and minimum horizon impose structurally different constraints that make a gross yield comparison non-meaningful.

- Correlation with the rate cycle affects both asset classes, but through different channels and on lagged timelines.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Series I and EE Savings Bonds: Locked Formulas in a Moving Rate World

US savings bonds lock a rate formula at the moment you buy them, for the life of the…

Where the Livret A’s Money Goes: The Caisse des Dépôts Circuit and Social-Housing Finance

The savings held on Livret A accounts do not sit idle. A regulation-set share is centralised at the…

France’s LEP vs the Livret A: A Means-Tested Higher Rate, Explained

France’s Livret d’épargne populaire is often described as "the Livret A, only better". The description misleads: the LEP…