T10YIE vs TIPS Yield: Decomposing Real Yield and Inflation Expectations

The nominal 10-year Treasury yield is not an indivisible number: it decomposes into the TIPS real yield and T10YIE inflation expectations. This accounting identity is the key to the contemporary macro reading of the US Treasury market.

TL;DR

Of the 261-basis-point rise in DGS10 over 2022, the New York Fed traced roughly 80% to the real yield (DFII10) and only 20% to T10YIE inflation expectations.

- DGS10 = DFII10 + T10YIE is a no-arbitrage identity, so the same nominal move can come from a rising real yield or from drifting inflation expectations, two opposite macro readings.

- Factor models refine the raw figure: the ACM model (New York Fed, since 2015) put pure 10-year expectations near 2.1% in Q1 2024 against a raw T10YIE of 2.35%, with the inflation risk premium running 25 to 60 basis points across 2003-2025.

This article decomposes the formula DGS10 = DFII10 + T10YIE, takes the 2022 episode as textbook case, and exposes the inflation premium extracted by factor models. For the underlying logic, see the breakeven inflation component.

1. The accounting identity: DGS10 = DFII10 + T10YIE

The nominal 10-year Treasury yield, FRED series DGS10, is by construction the sum of the expected real yield over the decade — captured by the equivalent-maturity TIPS, series DFII10 — and the compensation for expected average inflation over the next ten years, captured by T10YIE. This decomposition results from a no-arbitrage condition: if markets expect average inflation, the nominal Treasury must offer a nominal yield consistent with the TIPS yield plus that inflation, otherwise arbitrage shifts prices until equality is restored. The point is put in perspective in our decoding of the limits of indexation.

The identity is rigorously exact in theory, net of two premia that blend into it in practice: an inflation risk premium (demanded by arbitrageurs to bear the risk of inflation surprise) and a TIPS liquidity premium (which makes the TIPS yield slightly higher than it should be). These two premia were detailed in the T10YIE series calculation method; the present article takes them as given and focuses on the reading of movements.

The analytical importance of the decomposition comes from the fact that the same nominal move can be carried by two opposite dynamics. When DGS10 rises by 50 basis points, either the real yield rises (Fed tightening, improved growth outlook, expanding term premium), or T10YIE rises (drifting expectations, widening inflation premium). These two scenarios call for entirely different macro readings. Without decomposition, the nominal move is ambiguous — which is why every Treasury curve analyst now starts by separating the two components. Each option is weighed on its own terms in how TIPS and nominal Treasuries compare.

The decomposition does not apply to the 5Y/10Y slope of the breakeven curve itself, which is the subject of separate analysis. The present reading covers a single point on the curve — the 10Y — and decomposes that point into its two components. For the 5Y vs 10Y term-structure segmentation, the angle is complementary but distinct.

2. Decomposing a nominal move: the 2022 episode as textbook case

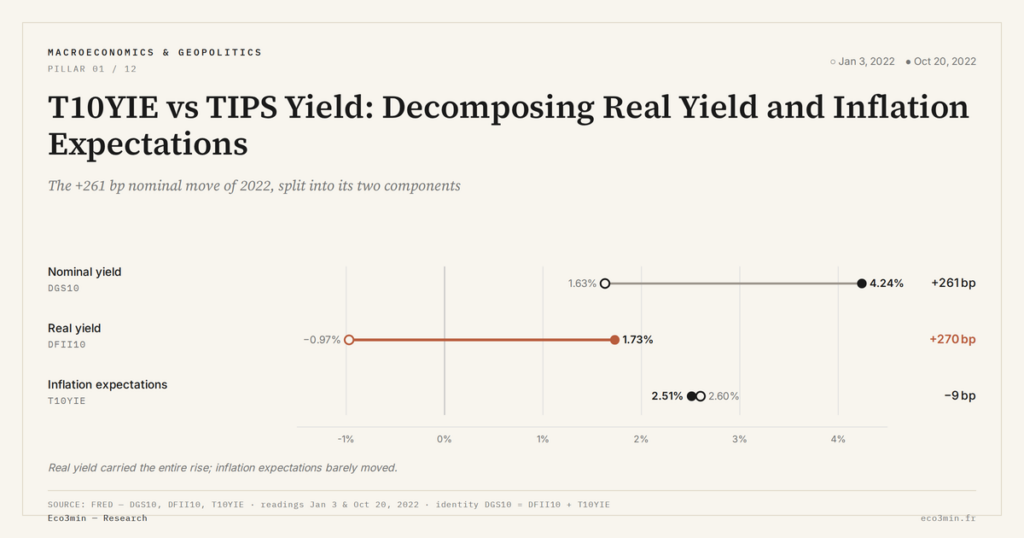

The year 2022 provides the clearest textbook case of decomposition. Between January and October 2022, DGS10 rose from 1.63% to 4.24%, a dramatic 261-basis-point increase. This rise could, in theory, have reflected three different scenarios: pure rise in the real yield (credible Fed tightening), pure rise in expectations (de-anchoring), or a combination.

Calculations published by the Federal Reserve Bank of New York in August 2022 settled the matter empirically. Of the 261-basis-point nominal rise, roughly 80% came from DFII10 (real yield going from about -1.0% in January to +1.5% in October, i.e. 250 basis points) and only 20% from T10YIE (breakeven going from 2.55% in January to 2.99% in April, retreating to 2.40% in October, a net move of only 11 basis points over the period). The nominal rise was almost entirely carried by real tightening, not by expectations de-anchoring.

This decomposition was fundamental in calibrating Fed communication from summer 2022 onward. The anti-inflation credibility remained largely intact — T10YIE topped at 2.99% and then retreated — and the challenge was transmitting real tightening to the economy. Without decomposition, the Fed could have read the DGS10 surge as a de-anchoring signal and tightened more than necessary. With decomposition, it could calibrate the tightening pace on the real-yield trajectory rather than on the expectations component.

The 2022 episode illustrates an empirical rule for reading monetary cycles: a nominal move carried only 20% by expectations is a signal of real tightening being transmitted effectively, not a loss of inflation control. Conversely, a nominal move carried 80% by expectations is an emergency signal — the Fed must react with reinforced communication tools before the drift becomes self-fulfilling. Systematic decomposition between the two components is therefore the central analytical tool for reading the Treasury market macro.

The raw identity DGS10 = DFII10 + T10YIE says nothing about the three finer components blended into T10YIE: pure expectations, inflation risk premium, TIPS liquidity premium. To isolate the expectations component stricto sensu, economists use factor models that decompose T10YIE into three additive terms. The reference is the ACM model (Adrian, Crump, Moench) published by the Federal Reserve Bank of New York since 2015.

The ACM model decomposes T10YIE into: a pure expectations component, an inflation risk premium, and a residual tied to the real risk premium. According to the April 2024 publication, pure 10-year inflation expectations stood around 2.1% in Q1 2024, against a raw T10YIE of 2.35% — a total premium of 25 basis points. This decomposition is not directly usable by a non-specialist — it requires factor-modeling infrastructure — but it provides a reference on the magnitude of the raw bias. Full series: Our market-implied inflation data.

The inflation risk premium has historically oscillated between 25 and 60 basis points over 2003-2025 according to ACM calculations. The phases close to zero correspond to 2009-2015 — post-crisis deleveraging, compressed expectations, low realized inflation volatility. The phases above 50 basis points correspond to 2022-2024 — memory of the post-COVID shock, higher premium demanded by arbitrageurs to bear the residual surprise risk. This cyclical variation in the inflation premium explains why T10YIE can diverge from SPF even when true expectations are stable.

For the standard macro reader, the pragmatic reading is the following: T10YIE is a good approximation of 10-year expectations, but with a variable bias of 25 to 60 basis points that factor models allow to estimate. For current phases (May 2026), the premium is probably around 30-40 basis points, which places pure expectations in a 1.9% to 2.1% zone while raw T10YIE shows 2.2-2.4%. This nuance is what allows Powell to assert that expectations remain anchored, despite a raw breakeven above the 2% target.

4. Implications for macro reading and TIPS vs nominal allocation

The decomposition DGS10 = DFII10 + T10YIE has a direct consequence on the reading of bond positions. An investor holding a nominal Treasury bears two distinct risks: a real-yield variation risk (depending on expected growth and Fed policy) and an inflation expectations variation risk (depending on Fed credibility and external shocks). An investor holding a TIPS bears only the first risk; inflation is neutralized by principal indexation. A closer look is offered in how inflation-protected bonds work. This is the central reading angle of the inflation-linked bond mechanics.

This risk-profile difference has a concrete implication for reading nominal-TIPS arbitrages. When a manager shifts allocation from nominal to TIPS, they neutralize the expectations risk without necessarily neutralizing the real-yield risk. When the arbitrage goes the other way — from TIPS to nominal — it typically signals that the investor finds the real yield attractive and judges the expectations risk contained. Observing net TIPS / nominal flows therefore provides a near-daily reading of market inflation risk aversion. On the same theme: the Eco3min frame for reading inflation.

Another consequence concerns cycle reading. In a credible-disinflation phase — typically after an inflation shock contained by the Fed — DGS10 falls primarily by compression of T10YIE, while DFII10 remains relatively stable because growth does not slow immediately. In an anticipated-recession phase, DGS10 falls primarily by compression of DFII10 (anticipated real policy rate declining) while T10YIE remains stable. These two configurations call for opposite macro readings that decomposition reveals.

A final implication concerns the analysis of exogenous shocks. An oil shock pushing CPI temporarily higher should not, in pure expectations theory, affect T10YIE — which measures a 10-year average and should neutralize transitory shocks. In practice, T10YIE moves even on energy shocks, revealing that markets partially incorporate the recent past into their long-run projection — behavior sometimes called adaptive expectations in academic literature. For tracking this divergence between breakeven and realized inflation, see divergence with realized inflation.

A practical observation worth emphasizing for asset managers: the DGS10 decomposition allows separating beta exposures that would otherwise be conflated in a portfolio risk model. A long Treasury nominal position is not equivalent to a long TIPS position plus a long inflation expectations exposure — the two construct profiles only converge when liquidity and inflation risk premia are stable, a condition rarely satisfied across regimes. Modern factor-based risk attribution frameworks therefore systematically break down nominal Treasury holdings into real-yield duration and breakeven duration, treating each leg as a separate factor exposure that requires its own hedging consideration. This methodological refinement, increasingly standard on institutional desks, is a direct outcome of the analytical framework presented here. In the same vein: the framework linking the copper/gold ratio to the macro cycle.

Reading a rise in the 10-year nominal Treasury as a mechanical signal of inflation expectations de-anchoring. This is inaccurate in 80% of cases: the majority of significant nominal moves are carried by the real yield (DFII10), not by the breakeven (T10YIE). The 2022 episode, where 80% of the 261-basis-point rise came from real yields and only 20% from expectations, is the paradigmatic counter-example. Without decomposing, one confuses real tightening with loss of inflation control.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Monetary Tightening: How Central Banks Are Reshaping Financial Markets

After more than a decade of ultra-accommodative policy, monetary tightening has reintroduced the real cost of capital as…

Hidden Unemployment: Reading the Real Labor Market in 2026

Headline unemployment is stabilizing while broad underemployment still runs above pre-2020 levels. Reading the gap between official rates…

2026 Economic Outlook: Key Trade-Offs After the End of Cheap Money

2026 ushers in a more constrained macro regime where real rates stay positive, fiscal space narrows and geoeconomic…