WALCL: Composition by Instrument — Treasuries, MBS, Fed Assets Breakdown

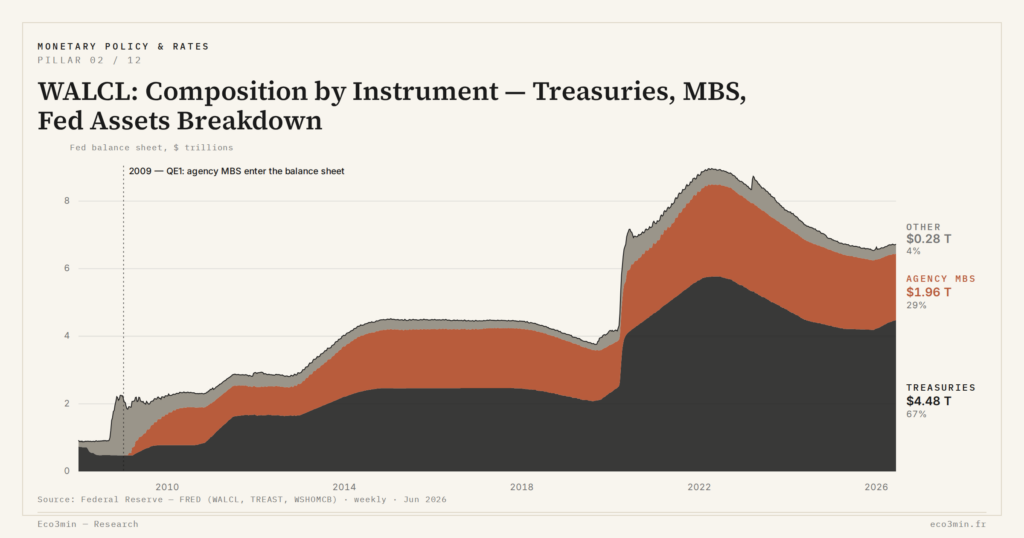

By late 2025, the ~$6.8 trillion WALCL splits into roughly $4.3 trillion of Treasuries, $2.3 trillion of agency MBS and $200 billion of residual assets. This recent composition mechanically conditions what the current QT can produce.

TL;DR

Agency MBS, added via QE1 in January 2009 and held by no other G7 central bank at this scale, now leave the Fed balance sheet only when mortgage prepayments allow.

- The -$35 billion monthly MBS cap (FOMC, since June 2022) is rarely binding: with 30-year rates elevated since late 2022, actual runoff held between -$15 and -$20 billion over 2024-2025.

- Because Treasuries run off faster, the MBS share of WALCL rose from about 30% at the April 2022 peak to about 34% by late 2025, widening the balance sheet's sensitivity to mortgage rates.

Three asset families structure the contemporary Fed balance sheet. Each obeys distinct absorption dynamics that the aggregate-level reading entirely masks.

Reading the aggregate WALCL level without looking at instrument-level composition is like watching a thermometer without reading the scale. Composition determines what the Fed can do mechanically at each phase of the cycle, how it can do it, and at what pace. Before 2008, the Fed balance sheet was almost entirely composed of short and medium-maturity Treasuries, held against currency in circulation. The introduction of agency MBS via QE1 in January 2009 inaugurated a doctrinal rupture that no other G7 central bank has replicated at this scale, and which still structures today the constraints on WALCL as a monetary-stance indicator.

This analysis runs parallel to but distinctly from the technical definition of the FRED ticker. The definition lays out what WALCL aggregates; composition describes what is inside it, and why this internal structure changes the operational analysis of the balance sheet. For direct time-series access to the underlying data, the FRED WALCL dataset for time-series access provides the canonical entry point.

Treasuries in WALCL: maturity distribution and runoff mechanics

By late 2025, the Fed’s Treasury portfolio reaches roughly $4.3 trillion according to FRED data and the NY Fed’s quarterly SOMA reports. This envelope breaks down into four main categories: Bills (under one year) represent ~$280 billion per the September 2025 SOMA reports, Notes (1 to 10 years) constitute the bulk at ~$2.3 trillion, Bonds (over 10 years) reach ~$1.1 trillion, and TIPS plus inflation-indexed securities total roughly $360 billion.

This maturity distribution is not neutral for the runoff mechanism. The Fed does not actively sell Treasuries to remove them from the balance sheet: it lets these securities mature and chooses, within the authorized monthly cap, not to reinvest the repaid principal. The actual Treasury runoff pace is therefore a direct function of the portfolio’s maturity calendar. The current profile concentrates a significant share of maturities over the 2026-2028 window, supplying the mechanical raw material for QT in the coming years.

The Treasury monthly cap, set at -$60 billion between June 2022 and May 2024 then lowered to -$25 billion since May 2024 per the FOMC Statements, is not always saturated. When the volume of securities maturing in a given month exceeds the cap, the Fed rolls the excess; when it falls below the cap, actual runoff is reduced. SOMA reports document actual Treasury runoff oscillating between $20 and $30 billion per month in 2025, sometimes below the theoretical cap depending on the month.

This mechanics has a rarely explicit consequence: a reduced Treasury cap does not necessarily signal an intentional QT slowdown, but may reflect the effective maturity of the observed window. The distinction matters for how composition mirrors doctrinal regimes in reading successive phases. Bills (under one year) play a specific role: they roll over rapidly, but their actual runoff is traditionally managed to target relative stability of outstanding exposure — the Fed has generally not aimed to reduce its short-maturity exposure.

The Treasury portfolio’s sensitivity to long-rate moves is substantial. According to data in the Federal Reserve System annual financial report, the Fed booked roughly $1.1 trillion of unrealized losses on its entire portfolio (Treasuries plus MBS) in 2023, mainly attributable to the 2022-2023 yield increase. These losses are not recognized in WALCL, which values securities at amortized cost, but they are revealed at the time of actual runoff and compress Treasury remittances.

Agency MBS: the specificity of passive runoff via prepayments

The Fed’s MBS portfolio totals roughly $2.3 trillion by late 2025, mainly composed of agency MBS guaranteed by Fannie Mae, Freddie Mac and Ginnie Mae, issued on the 30-year and secondarily 15-year segments. Nearly all of these securities were acquired during the four successive QE programs between 2009 and 2022, mostly at the low mortgage-rate levels that prevailed during that period.

The analytical specificity of MBS in WALCL lies in the runoff mechanism. Unlike Treasuries that leave the balance sheet on a known date per their maturity calendar, MBS leave the balance sheet via prepayments — early repayments of the underlying mortgage loans by US households. These prepayments are themselves a function of mortgage rates prevailing in the secondary market.

The mechanics works as follows: when 30-year rates fall significantly below the average rate on existing loans, households refinance and prepay, which accelerates MBS runoff. When 30-year rates remain elevated, as has been the case since late 2022, households retain their existing low-rate loans and prepayments collapse. The -$35 billion monthly MBS cap authorized since June 2022 by the FOMC has almost never been hit in practice. According to estimates derived from SOMA reports, actual MBS runoff has hovered between -$15 and -$20 billion per month over 2024-2025, roughly half the authorized cap.

This asymmetry between theoretical cap and actual runoff has a structural consequence. If Treasuries leave the balance sheet faster than MBS, the relative MBS share in WALCL mechanically rises over time. The MBS share in WALCL thus moved from roughly 30% at the April 2022 Covid peak to roughly 34% by late 2025, despite a nominal reduction in the overall balance sheet. This drift modifies the Fed balance sheet’s effective sensitivity to mortgage-market conditions: a 30-year rate move now acts on a wider fraction of the asset.

The recurring question of active MBS sales (“outright sales”) has been raised several times in the FOMC Minutes since 2018 without ever being implemented. Current doctrine privileges exclusive passive runoff, but this choice is not unconditional: it reflects the Fed’s preference to minimize disruption of the secondary MBS market, where the Fed has become the largest historical holder. Active sales would alter the price equilibrium on agency MBS, with direct consequences for US mortgage financing conditions.

The residual line: emergency facilities and support liquidity

The Fed balance sheet’s residual line, roughly $200 billion by late 2025, groups several heterogeneous categories: repurchase agreements overnight and term resulting from routine open-market operations, primary credit extended via the discount window to banks demanding liquidity, historical gold reserves and special drawing rights, and balances of special facilities still active. This envelope is small relative to Treasuries and MBS, but its volatility during stress periods is incomparable.

The most recent example is the Bank Term Funding Program (BTFP), opened on March 12, 2023 in response to the Silicon Valley Bank and Signature Bank failures, and closed to new draws on March 11, 2024. The program carried roughly $167 billion at its peak in January 2024 per the weekly BTFP reports published by the Fed, and its residual balance continues to decay through 2025 as loans mature. This temporary addition to the Fed balance sheet did not reflect a QE intent — it answered emergency funding demand from bank counterparties. The same logic is developed in the monetary plumbing and its market effects.

Emergency support facilities share a common feature: their WALCL impact is non-discretionary in the monetary-policy sense. The Fed announces a program and sets its parameters; counterparties then decide whether to use the facility. WALCL reflects the resulting aggregate but does not distinguish in its level what stems from monetary intent versus what stems from market response. Rigorous reading requires unpacking the residual line when it becomes material.

The historical March 2020 facilities under the Covid framework (PMCCF, MLF, MSLP and others) were mostly closed between late 2020 and early 2021. Some accounting traces persist in affiliated accounts, but their impact on WALCL is now negligible. These facilities are however reactivable in case of a future crisis, and the March 2020 doctrinal precedent remains a structuring element of the Fed’s monetary palette for the monetary plumbing and Fed transmission in future stress phases.

Tying these three asset families back together: the contemporary Fed balance sheet is not a homogeneous block but a heterogeneous portfolio whose internal dynamics differ markedly. Treasuries dominate by size and provide the calendar-driven runoff backbone. MBS introduce a structural dependence on the mortgage market that no rate decision alone can override. The residual line absorbs unpredictable demand shocks from emergency facilities. Reading WALCL as a single number aggregates all three dynamics into one, masking the fact that a policy move on any one of them does not propagate identically across the others.

This heterogeneity is also what explains why successive Federal Reserve chairs since Bernanke have devoted substantial communication effort to the composition question, not just to the size question. The composition is the practical lever; the size is the headline result.

- Late-2025 WALCL splits into ~$4.3T Treasuries (by maturity: Notes dominate, then Bonds, Bills and TIPS), ~$2.3T agency MBS, ~$200B residual (repos, primary credit, residual BTFP).

- MBS leave the balance sheet via prepayments that depend on mortgage rates, not on a known schedule. The authorized cap of -$35B/month is not binding: actual runoff is -$15 to -$20B under current 30-year rates.

- The Treasuries-vs-MBS runoff asymmetry gradually shifts the relative composition toward MBS as QT continues (30% in 2022, 34% by late 2025).

Last updated — 21 June 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…