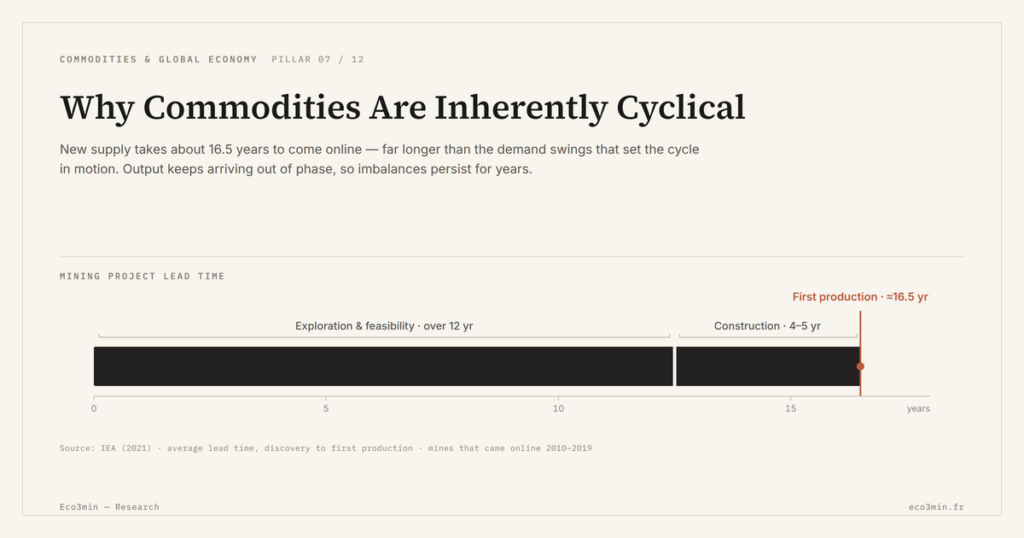

Why Commodities Are Inherently Cyclical

Commodity cycles stem from long investment lead times, rigid short-run supply and demand sensitive to the macro backdrop. Accumulated imbalances often take years to resolve, making these cycles both persistent and hard to forecast.

Macroeconomic analysis of commodity cycles: investment lead times, supply rigidity and long-term adjustment dynamics.

TL;DR

A new mine or energy project takes five to ten years to reach production, which is why commodity supply chronically arrives late, often just as demand begins to slow. This mechanism is detailed in how Eco3min reads commodity price formation.

- In mining and energy, turning a project into operating production typically takes five to ten years, so investment surges land well after the price signal that triggered them.

- Supply is largely inelastic in the short run: higher prices can't quickly add volume, while falling prices don't force immediate cuts, because fixed costs stay high and shutdowns are costly. This asymmetry stretches downturns.

- Since 2024–2025, durably positive real interest rates have raised the cost of capital for extractive projects, lengthening lead times further and stiffening supply adjustment just as capacity was already short.

Commodity markets are marked by recurring phases of expansion and contraction. These cycles stem from long investment lead times, supply that is rigid in the short run and demand sensitive to macroeconomic conditions. Accumulated imbalances often take several years to resolve. A common misreading is to interpret these cycles as simple cyclical alternations. This page analyses the structural mechanisms that make commodity cycles both persistent and difficult to forecast.

Investment lead times that structure the cycle

The core of commodity cyclicality is time. Between the decision to invest and the effective arrival of new capacity, lead times are exceptionally long. In mining and energy, it typically takes between five and ten years to turn a project into operating production, once regulatory, financial and technical constraints are factored in. Related discussion: the mean-reversion seen after copper price peaks.

This inertia explains why supply adjustments often arrive too late. When prices rise persistently, investments multiply, but their actual impact only materialises several years later, often just as demand begins to slow. The cycle reinforces itself through temporal lags.

Supply rigidity and asymmetric adjustments

In the short run, commodity supply is largely inelastic. A price rise does not allow available volumes to be increased quickly. Conversely, a price fall does not lead to an immediate cut in production, because fixed costs remain high and shutdowns are costly.

This asymmetry amplifies cycles. Tight phases translate into rapid and at times excessive price increases, while easing phases tend to be prolonged, with excess capacity slow to clear. This mechanism is central to understanding why commodity markets do not return rapidly to a stable equilibrium.

These cyclical imbalances materialise primarily through inventory dynamics. When supply arrives late or when demand turns, it is the inventory level that temporarily absorbs the gap, before prices fully adjust. This mechanism is detailed in the analysis dedicated to the role of inventories in commodity price formation, which shows how inventories amplify or cushion the various phases of the cycle.

Macroeconomic demand and lagged reactions

Commodity demand depends closely on the global business cycle. Industrial acceleration, fiscal policy, credit conditions and global trade dynamics directly influence consumed volumes. These demand variations, however, propagate faster than supply adjustments.

This produces phases in which prices very quickly incorporate a change in macroeconomic outlook, even as physical volumes remain unchanged. This dissociation between price signal and material reality is also at the heart of the opposition between physical supply and financial demand, which explains why cycles can be amplified by flows unrelated to immediate consumption.

Why this mechanism is becoming more visible now

Since 2024–2025, the persistence of positive real interest rates has reshaped the economic calculus of extractive projects. A higher cost of capital has slowed certain investments at precisely the moment when capacity was still missing in several sectors. This lag makes cycles more legible, because the financial constraint acts as an amplifier of the supply lead times already in place.

This point can only be properly interpreted by placing it within a reading of the rate cycle : when real rates remain durably positive, the cost of capital mechanically extends investment lead times and stiffens supply adjustment, reinforcing the persistence of commodity cycles.

Mainstream consensus and alternative reading

Part of the consensus expects that the gradual normalisation of global growth would suffice to smooth commodity cycles. This scenario assumes a relatively rapid capacity for supply to adjust to past price signals.

An alternative reading places more weight on accumulated investment delays and the growing fragmentation of production chains. Within this framework, even a slowdown in demand does not guarantee a rapid exit from the cycle, because imbalances were built up over an extended period.

What readers really want to understand

The actual question is not whether a bullish or bearish cycle is under way, but whether these moves reflect a durable dynamic or a simple intermediate adjustment. Behind this question lies the concern of misreading a cyclical signal as a regime change, when structural forces remain unchanged.

What could invalidate this reading

Several factors could mute the observed cyclicality. A coordinated acceleration of investment, supported by more favourable financial conditions, would shorten adjustment lags. Conversely, a sharp negative demand shock or major technological innovations could shorten certain phases of the cycle. These scenarios remain conditional and depend on variables that are still uncertain.

Structural indicators to monitor

- Average lead times for new mining and energy projects to reach production

- Multi-year evolution of sectoral capital expenditure

- Inventory levels relative to historical averages

- Long-term financing conditions and cost of capital

Macro reading and economic implications

Commodity cyclicality has direct effects on inflation, industrial profitability and macroeconomic stability. Prolonged cycles of rising or falling prices influence margins, public policy and trade balances. On this point: Industrial metal set against monetary metal. As such, commodities are an essential lens for reading the global economy, as developed in the pillar page Commodities and the global economy.

What this dynamic concretely implies

- Cycles are built on long lead times, not on isolated shocks.

- Supply adjustments often arrive after the demand turn.

- Volatility is a structural consequence, not a market anomaly.

This is not the central scenario adopted by all market participants, but the reading helps explain why commodity cycles persist despite repeated stabilisation attempts. The risk is less visible than an abrupt shock, but more durable, because it rests on slow mechanisms that are difficult to correct rapidly.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

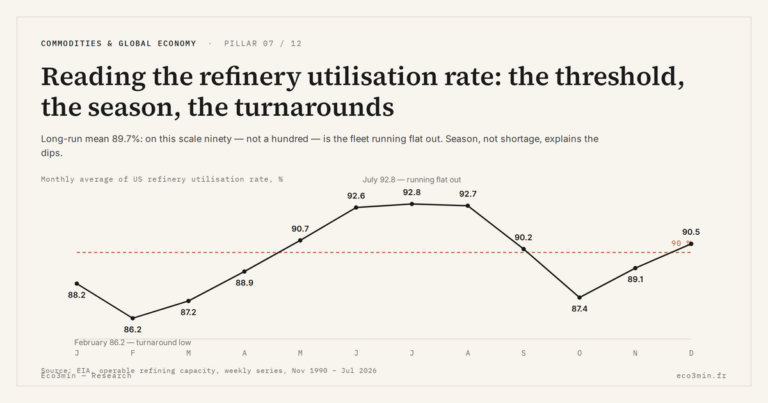

Full pillar →Reading the refinery utilisation rate: the threshold, the season, the turnarounds

A refinery runs full near ninety percent, not a hundred: the last slice of nameplate capacity is a…

IMO 2020: the regulatory shock that rewrote product spreads

An environmental rule on marine sulfur can move a refining spread more than a swing in crude. IMO…

The 2022–2023 refining golden age: anatomy of an episode

In 2022, refined fuel prices climbed faster than crude. That gap, measured by the 3-2-1 crack spread, reached…