ACMTP10 Meaning and Computation: Understanding the Adrian-Crump-Moench (2013) Model

ACMTP10 is not an analyst opinion but the output of a five-factor regression published by the New York Fed in 2013, reproducible with standard statistical software and refreshed monthly on the ACM dashboard.

TL;DR

Built in 2013 for the FOMC's post-2008 QE diagnostics, the ACM term-premium model now anchors decomposition frameworks from the ECB to the Bank of England and the BIS.

- Published as NY Fed Staff Report 340 in May 2013, then as NBER Working Paper 19774 and in the Journal of Financial Economics, the model emerged from the FOMC's effort to read its QE programs.

- Five latent factors come from principal component analysis since 1961: level alone explains over 90% of yield variance, slope 5-8%, curvature about 2%, with the last two below 1% each yet essential to a clean term-premium read.

- The model outputs ACMTP10 and ACMY10, whose sum is a fitted yield that tracks FRED's DGS10 within 2-5 basis points in calm markets and 10-15 during stress episodes like March 2020 and October 2023.

- Because the series is re-estimated on the full history, past figures carry retrospective revisions, which is why the model is presented as an analytical tool rather than a basis for real-time automated decision rules.

Three economists — Adrian, Crump, Moench — operationalized in 2013 what the affine term-structure theory had promised since Vasicek (1977): decomposing the Treasury yield into economically interpretable components.

1. Origin, Publication and Institutional Status of the ACM 2013 Model

The Adrian-Crump-Moench model was published in May 2013 in the New York Fed Staff Reports series as number 340, under the title Pricing the Term Structure with Linear Regressions. A revised version later appeared as NBER Working Paper 19774, and the paper went on to a peer-reviewed publication in the Journal of Financial Economics. In 2013 the three authors held research positions at the Federal Reserve Bank of New York: Tobias Adrian then led the Capital Markets Function group, before joining the International Monetary Fund in 2017 as Director of the Monetary and Capital Markets Department; Richard K. Crump and Emanuel Moench belonged to the same research team, Moench later moving to the Bundesbank and then to the Halle Institute for Economic Research.

The model’s institutional status matters. Unlike many academic contributions on the term structure, ACM 2013 was produced in the explicit context of the FOMC’s diagnostic work on the effects of QE programs running since 2008. The model was immediately integrated into the Fed’s analytical toolkit: the New York Fed has been publishing since 2013 an ACM dashboard updated monthly, which makes term-premium and expected-short-rate estimates available for maturities from 1 to 10 years. The 10-year series, identifiable on FRED as ACMTP10 (term premium) and ACMY10 (cumulative expectations), is the most closely tracked by macro-financial analysts.

Beyond the Fed, ACM 2013 adoption has been gradual but is now established. The European Central Bank publishes its own Bund 10-year term-premium estimate using an ACM-inspired methodology adapted to the euro curve structure. The Bank of England has provided since 2014 a Gilt 10-year estimate following the same class of multi-factor affine models. The Bank for International Settlements (BIS) regularly references ACM estimates in its Quarterly Review for comparative analyses of global financial conditions. Central-bank steering of the term structure thus rests on a common decomposition framework, without making it an explicit communication object toward the broader public.

2. The Five Latent Factors and What They Capture

The heart of the ACM 2013 model is the extraction of five latent factors via principal component analysis applied to the historical matrix of Treasury yields across maturities. The choice of five factors is not arbitrary: it extends the Litterman-Scheinkman (1991) tradition that had shown three factors — level, slope, curvature — already capture more than 99% of yield variance, adding two additional factors to capture residual movements the term premium needs isolated. A related fiscal angle is developed in the mechanics tying the federal deficit to gold reserves.

The first factor captures the level component of the curve. It represents parallel movements affecting the entire term structure in the same direction. Empirically, this factor explains more than 90% of daily yield variance since 1961. When the FOMC revises aggregated expectations of policy rates over the visible horizon, or when an inflationary shock shifts the entire curve upward, it is primarily the level factor that moves.

The second factor captures slope. It represents the difference between the long end and the short end of the curve: when it rises, the curve steepens; when it falls, the curve flattens or inverts. This factor typically explains between 5 and 8% of residual variance. It moves when the market revises its read of the monetary cycle — slowdown expectations (flattening), return of growth (steepening).

The third factor captures curvature. It describes the hump or trough in the intermediate zone of the curve (typically 5 to 7 years) relative to a simple linear interpolation between the short and long ends. This factor explains about 2% of variance and generally moves during technical adjustments tied to the composition of Treasury supply across intermediate maturities.

The fourth and fifth factors capture fine residuals — typically maturity-specific spreads, microstructure effects (segmentation among buyers seeking different duration profiles), inventory biases at primary dealers. Individually, each of these factors explains less than 1% of variance. Collectively, they are indispensable for a clean term-premium estimate: these are precisely the residuals that carry information about the economic compensation demanded beyond what level, slope and curvature already determine.

Adrian, Crump and Moench argue in their original publication that using five factors rather than three significantly improves fit quality to the data and the stability of term-premium estimates. Cochrane and Piazzesi (2005), in earlier work, had also suggested that a fifth factor carried most of the predictability of excess bond returns — an additional empirical argument for the ACM choice.

3. Two-Stage Regression: Why Linear and Not Maximum Likelihood

The methodological specificity of ACM 2013 versus prior affine models (Duffie-Kan 1996, Dai-Singleton 2000) lies in the estimation procedure. Classical affine models are estimated by joint maximum likelihood over all dynamic and pricing parameters — a numerically heavy procedure, sensitive to initial conditions, that can converge to local optima depending on starting specifications. Adrian, Crump and Moench propose a decomposition of the estimation into two successive stages via linear regressions.

First stage: extraction of latent factors and estimation of their dynamics under the physical measure. Treasury yields across maturities are regressed on the five extracted principal components, yielding the loadings B(τ) for each maturity τ. The factor dynamics under the physical measure are estimated via a standard VAR(1). This first stage uses only classical econometric tools — OLS regression, vector autoregression — available in any statistical software package.

Second stage: estimation of risk prices under the risk-neutral measure. From observed excess returns and the factor innovations derived in the first stage, a linear regression yields the matrix of risk prices that transforms the physical measure into the risk-neutral measure. This regression directly delivers the parameters needed to compute the term premium.

The practical advantage is considerable: the full procedure can be coded in a few dozen lines in Matlab, R, Python or Stata. The authors’ reference Matlab code is published on the NY Fed website, which allows any researcher to reproduce the estimates. The potential drawback is that stagewise estimation does not exploit all information from the joint structure — full likelihood would in principle have superior asymptotic efficiency properties. Bauer and Hamilton (2018) documented that this gap can introduce small-sample biases, and proposed bootstrap-based corrections now applied by the NY Fed in certain supplementary publications.

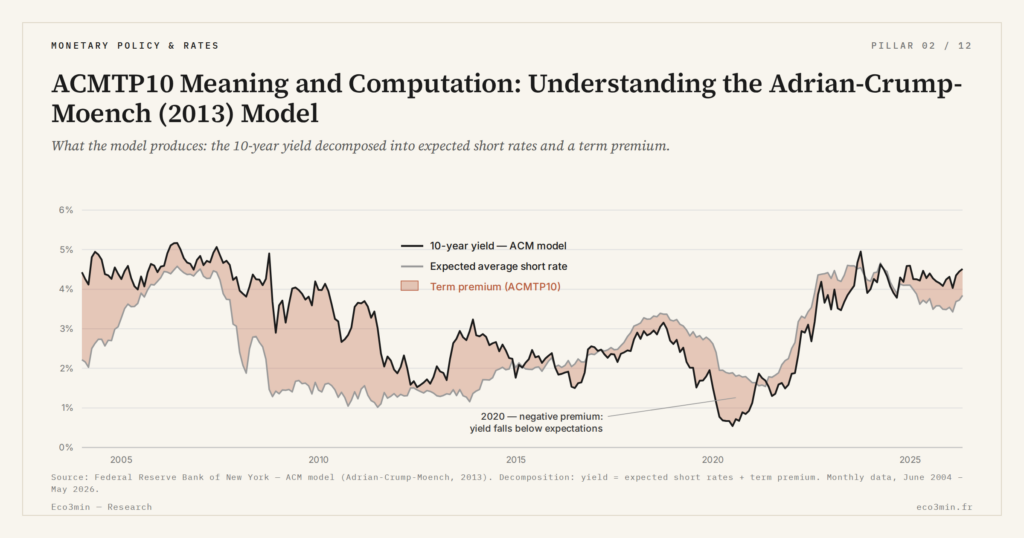

4. What the Model Produces: Term Premium, Expectations, Decomposed Yield

The ACM 2013 model produces three families of outputs for each maturity from 1 to 10 years, updated monthly on the NY Fed dashboard. The first is the term premium — for the 10-year maturity, that is ACMTP10. The second is the cumulative expected short rate over the maturity horizon — for the 10-year, that is ACMY10. The third is the model-fitted yield, which should match the market-observed yield to a few basis points: its gap with FRED DGS10 serves as a fit-quality diagnostic.

The accounting identity the model produces reads: fitted yield = cumulative expectations + term premium. For the 10-year: fittedʹ10yʹ=ʹACMY10ʹ+ʹACMTP10. This is the framework for applying the decomposition to the 10-year yield that allows every Treasury market episode to be reread along two dimensions. The fitted yield typically matches DGS10 to within 2 to 5 basis points in calm regimes; the gap can momentarily widen to 10-15 basis points during stress periods (March 2020, October 2023, April 2025).

Outputs are published in two formats. Daily series are available through FRED under codes ACMTP10, ACMY10 and their equivalents for other maturities (ACMTP01, ACMTP02, …, ACMTP09). The NY Fed ACM dashboard complements these with monthly charts, historical decomposition tables, and a full downloadable estimation file in CSV format, also available through the FRED ACMTP10 dataset reference page. The monthly update frequency reflects the fact that model parameters are not re-estimated daily but refreshed periodically, typically at month-end for next-month publication.

5. Limitations, Retrospective Revisions and Alternative Models

The ACM 2013 model has several limitations that its authors do not hide and that any operational user must keep in mind. The first concerns sensitivity to estimation choices: the historical window used, the assumptions on factor-innovation distributions, the exact number of factors retained — all these methodological decisions affect the final estimates at the margin. The NY Fed made a fixed specification choice and has maintained it since 2013, which guarantees the temporal consistency of the series but does not mean that other reasonable choices would produce identical numbers.

The second limitation concerns retrospective revisions. When the NY Fed re-estimates the model on the full history — an operation done periodically to incorporate new observations — past term-premium estimates can be revised. The June 2018 figure published in June 2018 is not exactly identical to the June 2018 figure read today on the dashboard; the gap typically remains modest (a few basis points) but can be larger on particularly hard-to-estimate points (March 2020, October 2023). This revisability property disqualifies ACMTP10 use for real-time automated decision rules but does not reduce its analytical value.

The third limitation concerns the epistemological status of the decomposition. The model assumes risk-neutral pricing for the mathematical derivation — precisely the residual unexplained by that assumption constitutes the term premium. The approach is defensible but remains one modeling convention among others. Kim and Wright (2005), in an alternative model also published and maintained by the Fed, make slightly different specification choices (three factors instead of five, distinct dynamic assumptions) and obtain qualitatively close but quantitatively different estimates — typically 20 to 40 basis points of gap depending on periods. Joslin, Singleton and Zhu (2011) propose an approach with different canonical restrictions that also converges with ACM 2013 on directions but diverges at the margin on levels.

For broader context on the decomposition and its role in modern Treasury analysis, back to the decomposition identity.

Conclusion

The ACM 2013 model is neither a black box nor a truth. It is a reproducible empirical instrument, defended by its authors, adopted by the global central-banking community, and accompanied by alternative models published in parallel to allow methodological cross-checks. Its solidity rests on three properties: transparency of code and method, regular monthly publication, and explicit acceptance of its own limitations. For anyone wishing to read the 10-year Treasury as more than a single number, ACMTP10 remains the most rigorous methodological entry point available.

- The ACM 2013 model (NY Fed Staff Report 340) extracts five latent factors via principal component analysis of Treasury yields since 1961, then derives term premium and expectations through a two-stage linear regression procedure.

- The ACMTP10 (10-year term premium) and ACMY10 (cumulative expectations) outputs are published on FRED and on the NY Fed dashboard with monthly refresh, and remain reproducible with standard statistical software via the authors’ Matlab code.

- Estimates are subject to retrospective revisions when the model is re-estimated — typically a few basis points, sometimes more during the hardest-to-estimate episodes (March 2020, October 2023).

- The Kim-Wright 2005 model and the Joslin-Singleton-Zhu 2011 approach provide alternative decompositions that converge qualitatively with ACM 2013 but can diverge by 20 to 40 basis points at the margin.

Last updated — 10 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…