ACMTP10 vs DGS10 vs Expected Short Rates: The Full Decomposition of the 10-Year Treasury Yield

The nominal 10-year Treasury yield has not one decomposition but two, operating simultaneously on different layers — temporal for ACM, inflationary for Fisher — that intersect to form the reference grid of modern Treasury analysis.

TL;DR

Modern Treasury analysis splits the nominal 10-year yield along two simultaneous grids, temporal (ACM) and inflationary (Fisher), whose intersection yields four economically distinct components.

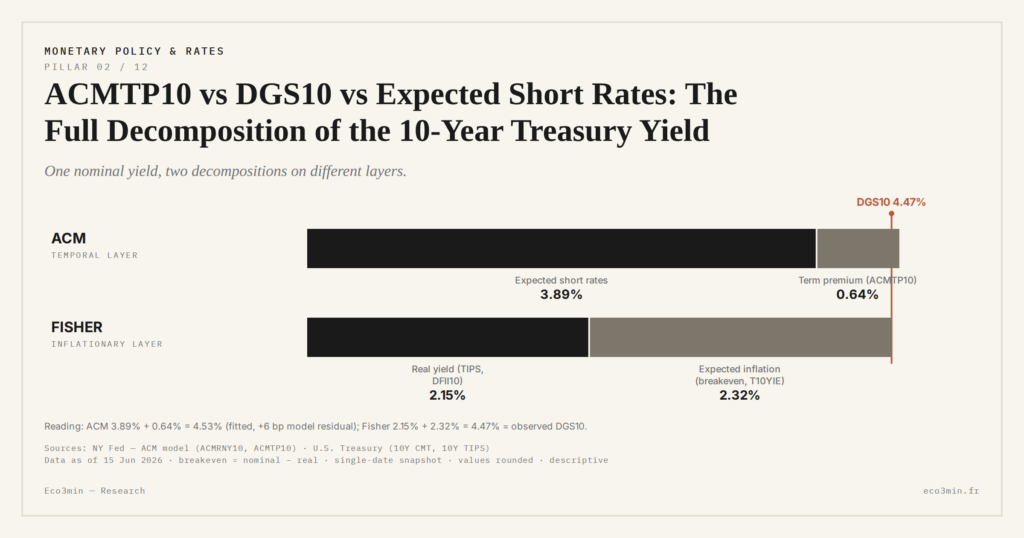

- The Adrian-Crump-Moench (2013) identity breaks DGS10 into cumulative expected short rates (ACMY10) plus a residual term premium (ACMTP10), both published on FRED and updated monthly on the New York Fed dashboard.

- The Fisher identity (1930), operationalized by the TIPS market since 1997, splits the same yield into real yield (DFII10) and breakeven inflation (T10YIE), with three imperfections (TIPS liquidity premium, inflation risk premium, tax treatment) aggregating to roughly ten basis points.

- Crossing the two grids isolates four distinct drivers (FOMC expectations, duration demand, r-star, inflation expectations), letting an analyst attribute a daily DGS10 move to the component that carried it.

- The decompositions are not additive: summing ACMTP10, DFII10, T10YIE and ACMY10 has no economic meaning, because ACMTP10 and DFII10 each embed, by construction, an overlapping share of term premium.

Reading DGS10 under a single grid means losing half the information. ACMTP10 and breakeven inflation are not redundant: they measure two distinct economic constraints priced by different market participants.

1. Why a Nominal Yield Is Not a Primitive Data Point

The nominal 10-year Treasury yield (FRED DGS10) is observed daily as a single number. This simple observation masks a composite economic reality. All modern Treasury market analysis — that practiced by the FOMC in its internal deliberations, by primary dealer research desks, by pension funds in their actuarial matching — relies on the breakdown of DGS10 into economically interpretable components. The yield is the aggregate; the components are the object of analysis.

Two principal decompositions structure this analysis. The first, Adrian-Crump-Moench (2013), separates the yield along a temporal dimension: expected short-rate component over the decade + residual term premium. The second, inherited from the Fisher identity (1930) and operationalized by the TIPS market since 1997, separates the yield along an inflationary dimension: real yield + expected breakeven inflation. These two decompositions are not competing — they operate on different layers of the same financial object and are mathematically compatible. Related figures: the long-run term-premium data.

To go back to the core definition of the term premium, ACMTP10 measures what a duration holder demands beyond the expected short-rate path. For the inflationary dimension, the T10YIE breakeven measures what the market expects as average inflation over ten years. The two quantities cohabit within DGS10 without conceptually overlapping.

2. First Identity — ACM: Cumulative Expectations + Term Premium

The ACM identity reads, for the 10-year maturity: DGS10ʹ≈ʹACMY10ʹ+ʹACMTP10. ACMY10 is the cumulative average of expected short rates over the decade, derived from the Adrian-Crump-Moench five-factor model. ACMTP10 is the residual term premium. Both components are published on FRED and updated monthly on the NY Fed dashboard. The sum reconstructs the observed 10-year yield to within a few basis points — the residual gap quantifying the model’s fit quality.

This identity operates on a temporal dimension. The ACMY10 component answers questions about the monetary trajectory: where will the FOMC take the policy rate over three, five, ten years? Which growth and employment regimes will justify which levels? The ACMTP10 component answers a different question: how much do marginal long-duration holders demand to carry that risk, independent of the expected path? Two questions, two mechanisms, two market communities — macro hedge funds and rates trading desks for expectations, pension funds and life insurers for the term premium. Also relevant: our mapping of monetary-policy action.

ACM analysis carries a specific institutional status. The FOMC has explicitly cited these estimates in its communications since 2020 — Jerome Powell, John Williams, Lael Brainard before her departure for the NEC — making it the common language of the global central-banking community. For precise methodological details on the five-factor regression and the two-stage estimation procedure, see the Adrian-Crump-Moench methodology. For the operational framing of this article, only the accounting decomposition identity matters: DGS10 = ACMY10 + ACMTP10, to within a few basis points.

3. Second Identity — Fisher: Real Yield + Breakeven Inflation

The Fisher identity (1930) applied to Treasuries reads, in its empirical form: DGS10ʹ≈ʹDFII10ʹ+ʹT10YIE. DFII10 is the 10-year TIPS yield, i.e. the real yield offered by Treasury Inflation-Protected Securities. T10YIE is the 10-year breakeven inflation, computed as the difference between DGS10 and DFII10, and interpreted as the market’s cumulative average inflation expectation over the decade.

This identity operates on an inflationary dimension. DFII10 answers the question: how much does an investor receive in constant purchasing power for holding ten-year duration? The real yield simultaneously incorporates the equilibrium-rate component (r-star), expected growth, and — implicitly — a part of real term premium. T10YIE answers the question: how much average cumulative inflation does the market expect over ten years? The breakeven is an indirect measure, derived from secondary-market arbitrage between nominal Treasuries and TIPS.

The Fisher identity is not perfectly exact. Three imperfections qualify it. First imperfection: a TIPS liquidity premium term exists, generally positive (TIPS are less liquid than nominal Treasuries and demand compensation). Fleckenstein, Longstaff and Lustig (2014) documented this “TIPS-Treasury mispricing” which can reach tens of basis points during TIPS market stress — typically in March 2020, when the TIPS dislocation briefly distorted the breakeven reading. Second imperfection: an inflation risk premium term exists symmetrically. Holders of nominal Treasuries demand compensation for the risk that inflation surprises to the upside; this inflation risk premium is positive on average, meaning T10YIE structurally overstates central inflation expectations. Third imperfection: TIPS and nominal Treasuries do not share the same tax treatment for all holders, creating marginal gaps. D’Amico, Kim and Wei (2018) proposed a refined breakeven decomposition into pure inflation expectations and inflation risk premium, which serves as the academic reference for these adjustments.

For most operational analyses, these three imperfections aggregate to about ten basis points and the direct reading DGS10 = DFII10 + T10YIE remains valid. For finer analyses, particularly during stress periods, separate examination of the liquidity premium and the inflation risk premium components becomes indispensable.

4. Reading Both Grids Simultaneously: the Treasury Grid

What distinguishes rigorous Treasury analysis from event-driven commentary is the simultaneous reading of both identities. DGS10 can be decomposed via ACM into two components (expectations + term premium), and via Fisher into two other components (real yield + breakeven inflation). A related fiscal angle is developed in Gold and the question of U.S. debt sustainability. Crossing the two grids produces a four-dimensional Treasury grid:

1. ACMY10 — cumulative expected nominal short rates over ten years. Moves with market revisions to the FOMC trajectory.

2. ACMTP10 — residual term premium. Moves with structural duration demand, net Treasury supply, holder base composition.

3. DFII10 — TIPS real yield. Moves with r-star, expected growth, and a real term-premium component.

4. T10YIE — 10-year breakeven inflation. Moves with average inflation expectations, the inflation risk premium, and the TIPS liquidity premium.

When DGS10 rises 20 basis points on a single session, the Treasury grid allows the analyst to identify which of the four components carried the move. Three typical cases. First case: ACMY10 rises 20 bp, the rest stable. Reading: the market revised upward its expected short-rate trajectory, likely on the basis of a macro data point suggesting more restrictive monetary policy. Second case: ACMTP10 rises 20 bp, ACMY10 and real components stable. Reading: marginal duration holders demand higher compensation, perhaps due to a fiscal event or an unexpected Treasury supply flow. Third case: T10YIE rises 20 bp, DFII10 stable. Reading: inflation expectations have shifted upward, the nominal effect passes through the pure inflation component.

Crossing this grid with the central-bank toolkit gives readers an operational framework to distinguish what stems from policy rate (federal funds target, forward guidance) from what stems from balance sheet (QE/QT acting primarily on ACMTP10). This distinction is central to how the Fed balance sheet moves the premium, treated separately.

5. Operational Use and Pitfalls to Avoid

The Treasury grid is not a predictive tool but a descriptive one. Its function is to reread past and present market moves under a coherent analytical grid, not to forecast where DGS10 will go tomorrow. This methodological precision matters because it conditions the correct use of components.

The most frequent pitfall is double-counting components. ACMTP10 and DFII10 both contain, by construction, a part of the term premium — ACMTP10 measures the total nominal term premium, DFII10 measures the real yield which includes a real term premium. Confusing the two leads to reading errors: ACMTP10 and DFII10 do not add up, they partially overlap.

Conflating the two decompositions or summing them as if they were additive produces artifacts. ACM (expectations + term premium) and Fisher (real + breakeven) operate on different layers of the same yield: the Treasury grid crosses the two grids to produce a four-dimensional reading, but the naive addition ACMTP10 + DFII10 + T10YIE + ACMY10 has no economic meaning.

The second pitfall is over-interpreting very short-term variations. ACM model components are published with monthly frequency, meaning that the daily figures sometimes displayed on FRED come from interpolation based on monthly parameters. Intra-month variations do not reflect daily model re-estimation but the application of monthly coefficients to daily yields. For analyses at frequencies above two weeks, the use of interpolated daily components is defensible; below that, the artifact risk is high.

The third pitfall is mechanically transposing the US framework to other sovereign markets. The ECB publishes a Bund 10-year term-premium estimate, the Bank of England a Gilt 10-year, but market structures differ: the elasticity of the premium to central balance sheet composition, to net sovereign supply, and to the holder base varies across regions. The ACMTP10 variation amplitudes documented for the US do not symmetrically reproduce on Bund or JGB.

Conclusion

The dual decomposition identity is what makes modern Treasury analysis possible. ACM separates the temporal dimension, Fisher separates the inflationary dimension, and crossing the two produces the four-component grid that now serves as the common framework for central-bank analyses, research desks, and duration managers. The nominal 10-year yield remains the aggregate observable. The four components are the variables of analysis — each answering a distinct economic mechanism, each priced by a different market community.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…