DTWEXBGS and De-Dollarization: Geopolitical Narrative Versus Actual Reserve Flows

De-dollarization is among the most discussed macro theses since 2022. The measured flows — IMF COFER, SWIFT, BIS statistics — tell a more contained story than the geopolitical narrative. DTWEXBGS itself has not declined.

TL;DR

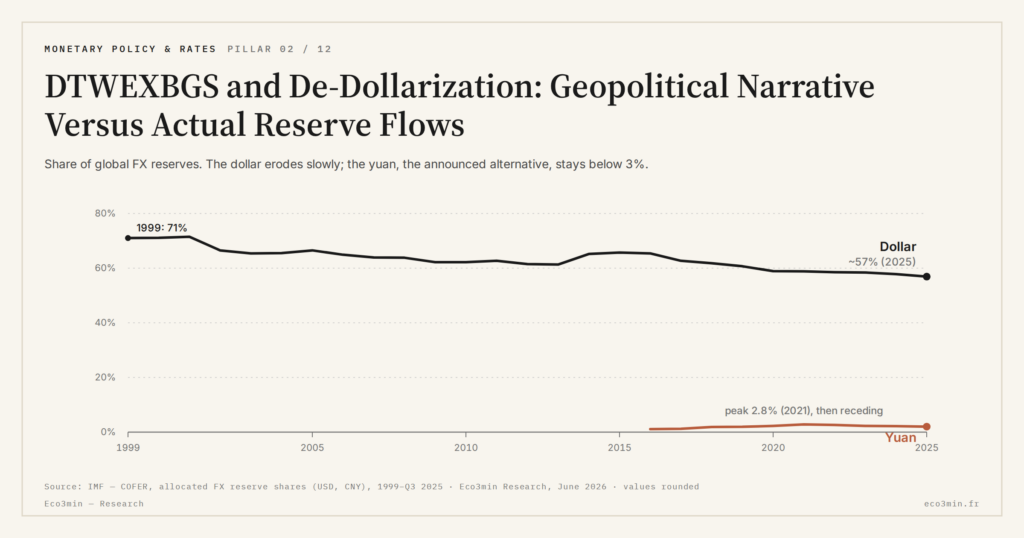

The yuan's share of global reserves has slipped to 2.4% from its 2022 peak, one sign that measured de-dollarization flows lag well behind the geopolitical narrative.

- Reserves (IMF COFER, Q1 2026): the dollar holds about 58%, down from roughly 71% in 1999 and 60% in 2015, an erosion of 1 to 2 points per decade; the gains accrued mostly to 'other currencies' (9% to 12% since 2015), not the yuan.

- Yuan momentum stalled from mid-2023: about 2.4% of COFER reserves in 2026 after a 2.9% peak in 2022, and roughly 4.5% of SWIFT payments after the cyclical 4.7% spike of January 2024.

- International debt is the steadiest channel (BIS, Q1 2026): around 64% dollar-denominated, in a 62% to 66% band since 2015, anchored by U.S. Treasuries that make up more than 60% of the global investment-grade sovereign market.

- DTWEXBGS, above 118 for twenty-eight months, tracks the dollar's relative price, not its share in reserves, payments or debt: the two dimensions move independently.

This piece exposes the tension between narrative and data. It does not say whether de-dollarization will occur. It says what the figures show in May 2026.

The de-dollarization thesis has gained visibility since February 2022 — freezing of Russian central bank reserves by Western sanctions — and then since the BRICS+ expansion of January 2024. Several commentators announced a structural pivot of the international monetary system: end of the dollar as dominant reserve currency, rise of the yuan as a credible alternative, emergence of a multipolar system. The debate is legitimate. Its empirical translation, as of May 2026, shows a far more measured trajectory than the narrative suggests. Reading these flows requires returning to what DTWEXBGS actually measures and to the position of the dollar in the global monetary system.

COFER figures: marginal erosion, not pivot

The COFER report (Currency Composition of Official Foreign Exchange Reserves) of the IMF is the official reference for the currency shares of global FX reserves. This is treated at length in the framework for reading dollar scarcity regimes. Published quarterly, it covers reserves declared by central banks of IMF member countries. According to the latest published data (COFER report, first quarter 2026), the dollar share of global reserves stands at approximately 58%. Background: the international arbitrage of gold against exchange-rate moves.

This value must be read in historical series. In 1999, at the birth of the euro, the dollar share reached approximately 71%. In 2015, it stood at approximately 60%. In 2020, approximately 59%. In 2024, approximately 58.5%. The 2015-2026 trajectory shows erosion of 1 to 2 points per decade — significant but far from the announced pivot. The euro share has remained stable around 20%, the yen share around 5.5%, the pound share around 4.9%. The rise has mainly benefited “other currencies” — an aggregate including Canadian dollar, Australian dollar, yuan, and Scandinavian currencies — which moved from approximately 9% in 2015 to approximately 12% in 2026.

The yuan share of global reserves deserves focus. The yuan was included in the SDR basket in October 2016. The full picture is drawn in this question on dollar weaponization reserves. Its COFER share was approximately 1.1% in 2016, peaked at approximately 2.9% in 2022, and stands at approximately 2.4% in 2026. The trajectory is non-linear: the war in Ukraine and Western financial sanctions against Russia initially accelerated diversification, but the move lost momentum from mid-2023. The yuan has not reached the critical mass of use that would make it an alternative to the dollar for major central banks’ strategic reserves.

Beyond reserves, the dollar share of international payments is a complementary indicator. SWIFT (Society for Worldwide Interbank Financial Telecommunication) publishes monthly the currency distribution of cross-border payments. According to the SWIFT RMB Tracker report (March 2026), the dollar share of international payments stands at approximately 47%. The euro share at approximately 22%. The pound share at approximately 7%. The yuan share at approximately 4.5%.

For context, the yuan SWIFT share was approximately 1.5% in 2015 and briefly exceeded 4.7% in January 2024 — a peak mediatized as a de-dollarization signal, but which proved cyclical. The 2024-2026 trajectory shows stabilization around 4-5%, a level that reflects gradual internationalization of the yuan in bilateral China-partner trade, but which remains far from the critical threshold to compete with the dollar.

The CIPS (Cross-Border Interbank Payment System), the Chinese alternative system to SWIFT for yuan payments, processes growing volumes that nonetheless remain marginal at global scale. According to statistics published by the PBoC (People’s Bank of China) for 2025, CIPS volumes exceeded 175,000 billion yuan for the year — approximately $24,000 billion equivalent. Compare to SWIFT volumes estimated at approximately $150,000 billion annually by major clearinghouses. CIPS therefore represents approximately 16% of SWIFT volumes. Significant, but far from a rebalancing of the system.

International dollar debt: marked resilience

The dollar share of international debt is the most stable of the three indicators. The BIS (Bank for International Settlements) publishes quarterly international debt statistics by issuance currency. According to BIS Quarterly Review (March 2026), the dollar share of international debt outstanding reaches approximately 64% at end-2025. This value has been stable since 2015 in a 62%-66% range, and has not evolved after 2022.

This stability is revealing. Issuing dollar debt presupposes a deep and liquid secondary market for placing it with international investors. No other currency offers the depth of the U.S. Treasury market, which remains the default safe-asset instrument of global institutional investors. The BIS estimates that U.S. sovereign bonds represent more than 60% of the global investment-grade sovereign bond market, against approximately 20% for the euro area and less than 5% for China.

Three readings of the narrative-data tension

The gap between de-dollarization narrative and measured figures can be read in three ways.

First reading: the narrative anticipates a structural move that will take time. The international monetary system has already experienced two major pivots — end of the gold standard 1933-1944, end of Bretton Woods 1971-1973. Both required at least a decade of preparation and a systemic shock to be accomplished. De-dollarization, in this reading, is underway but has not yet crossed the threshold of quantitative visibility. Current figures would constitute the start of a trajectory that will accelerate. This reading is defended by several heterodox economists and by BRICS+ central banks. For context: the case for dollarization or de-dollarization.

Second reading: the narrative overestimates the dynamic because it conflates political intentions and monetary execution. Governments can announce diversification of their reserves or increased use of the yuan in bilateral trade, but effective execution depends on the existence of an alternative market sufficiently deep and liquid. In the absence of a credible substitute for the U.S. Treasury market, political declarations produce little quantitative effect. This reading is defended by the BIS in its March 2026 Quarterly Review and by several IMF working papers.

Third reading: the narrative and the data coexist because they describe two distinct phenomena. The narrative describes a geopolitical movement of fragmentation of the international system. The data describes structural inertia of the dollar in the basic monetary functions — reserve, payment, debt. The two may coexist without contradicting each other: a politically more fragmented system can retain a dollar economically dominant, because monetary function and political function do not align mechanically. This reading is defended by several mainstream monetary economists. Worth reading alongside: the dollar at the centre of the monetary system.

What DTWEXBGS does not say about de-dollarization

An important methodological clarification. DTWEXBGS measures the strength of the dollar as a relative price on FX markets. It does not measure the dollar share of reserves, of payments, or of international debt. A dollar whose share of reserves were gradually declining could perfectly coexist with an elevated DTWEXBGS, if the decrease in institutional demand is offset by an increase in transactional demand or by the other mechanisms documented in the 2024-2026 Fed cuts paradox.

DTWEXBGS above 118 for twenty-eight months does not refute the de-dollarization thesis. Nor does it confirm it. It says that effective dollar pressure on global trade flows remains elevated, independently of the trajectory of dollar shares in the monetary functions of reserve, payment, and debt. The two dimensions are to be read in parallel, not one through the other.

- The dollar share of global reserves (IMF COFER Q1 2026): ~58%, eroding by 1 to 2 points per decade since 2015. Not the announced pivot.

- The dollar share of SWIFT payments (March 2026): ~47%. The yuan share: ~4.5%, stabilized after a cyclical peak at 4.7% in early 2024.

- The dollar share of international debt (BIS Q1 2026): ~64%, stable since 2015 — resilience carried by the depth of the U.S. Treasury market.

- DTWEXBGS measures the dollar’s relative price, not its share in monetary functions. The two dimensions evolve independently and are to be read in parallel.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…