DTWEXBGS 2024-2026: Persistent Dollar Strength Despite Fed Cuts

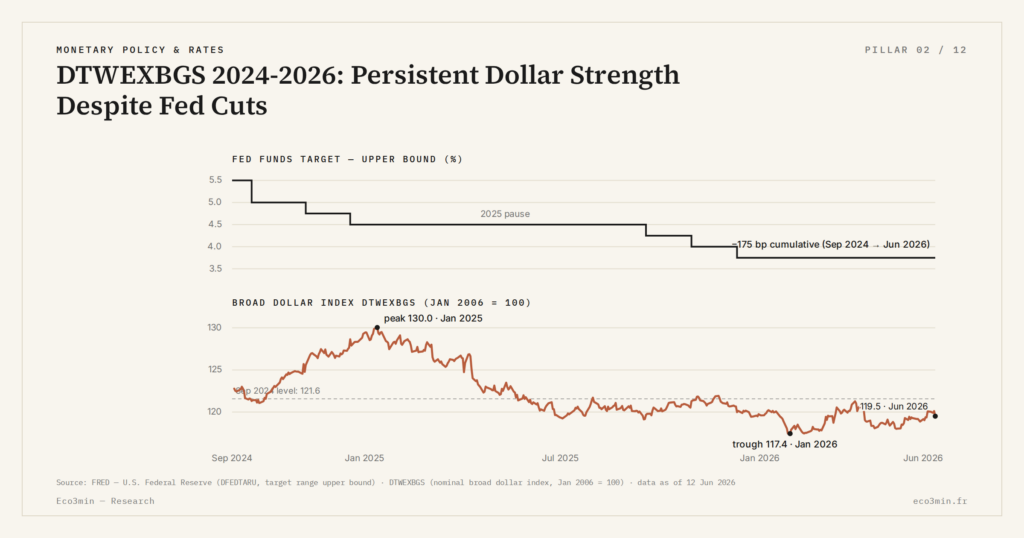

September 2024, the Fed launched its cutting cycle: -100 cumulative basis points by May 18, 2026. Classical theory predicted a broad-dollar depreciation of -3 to -5%. Observed: -1.2%. Three competing hypotheses feed the analysis.

TL;DR

DTWEXBGS slipped just 1.2% across fourteen months of Fed easing, a persistence with no precedent in the index's reconstructed history since 1973.

- 100 bp of Fed cuts since September 2024 moved DTWEXBGS only from 121.3 to 119.8 (-1.2% over fourteen months), ten times less than the -3% to -5% that interest-rate parity implied.

- Growth differential: the IMF (WEO April 2026) projects +2.3% U.S. growth in 2026 against +1.5% in the euro area and +0.7% in Japan, steering long-term capital toward dollar assets.

- The 10-year term premium (ACMTP10 series, New York Fed) returned to roughly +0.9% in May 2026 after a decade in negative territory, while the dollar's reserve share (COFER, Q1 2026) holds near 58% despite the January 2024 BRICS+ expansion.

This piece maps the three readings of the paradox. It does not arbitrate — none has yet received exclusive empirical validation.

The 2024-2026 dollar cycle produces a macro-reading anomaly with few equivalents in the documented history of reconstructed DTWEXBGS since 1973. The Federal Reserve has cumulated -100 basis points of cuts between September 2024 and May 2026, according to FRED data (Federal Funds Rate, DFF series). Over the same period, DTWEXBGS retreated from 121.3 to 119.8, a compression of -1.2% over fourteen months. The classical interest-rate parity theory predicted a depreciation of -3% to -5% on this horizon. The gap between expected and observed is precisely what this cluster, and notably the reading of DTWEXBGS as a systemic strength signal, seeks to make explicit.

The documented paradox

Standard interest-rate parity theory — formalized by Dornbusch in 1976 and refined in DSGE literature — postulates that a short-rate differential of 100 basis points between two economies translates, at equal expectations, into a cumulative depreciation of the currency whose rates are falling. The expected amplitude depends on the precise model parameters, but the order of magnitude typically converges toward -3% to -5% over twelve months for 100 basis points of differential.

DTWEXBGS, over the September 2024 – May 2026 window, shows a compression ten times smaller than this projection. More precisely: -1.2% cumulative against -3 to -5% expected. This gap constitutes a notable empirical phenomenon. It does not mean parity is invalidated — parity is not a law of physics but a theoretical equilibrium condition — but it means other forces operate and offset the expected effect of Fed cuts on the currency. The historical taxonomy of DTWEXBGS cycles documents no precedent of such persistent strength following a cutting cycle of this magnitude.

Three hypotheses are currently debated in central-bank and clearinghouse literature: the growth differential, the fiscal risk premium via term premium, and defensive attractiveness in a phase of geopolitical fragmentation. None is exclusive; they may operate simultaneously with variable relative weights. Our ACM term-premium series sets out how the indicator is built.

Hypothesis 1: the U.S. growth differential

The first reading rests on the expected growth differential. According to the IMF (World Economic Outlook, April 2026), expected 2026 U.S. growth is +2.3%. Euro area: +1.5%. Japan: +0.7%. United Kingdom: +1.1%. The U.S. differential against major developed economies is documented and significant.

The proposed mechanism: a growth differential attracts long-term capital flows toward U.S. assets — equities, corporate bonds, listed real estate, FDI — independently of the short-rate gap. These flows mechanically support the dollar through demand for dollar-denominated assets. The IMF published this explanation in the April 2026 WEO, and ECB working papers from late 2025 document the mechanism with structural models integrating portfolio flows and productivity. A closer look: our frame for the systemic dollar.

This reading has the advantage of coherence with previous historical episodes where the U.S. growth differential supported the dollar — notably 1995-2000 and 2014-2016. Its limit: it assumes execution of growth projections that remain uncertain. If 2026 U.S. growth were to disappoint, the argument would mechanically weaken.

The second reading runs through the term premium on long Treasuries. According to the ACMTP10 series published by the New York Fed, the nominal term premium on 10-year Treasuries stands at approximately +0.9% in May 2026. For context, this term premium was negative throughout most of the 2014-2022 decade — a phenomenon tied to structural demand for safe assets and to the Fed’s expanded-balance-sheet policy.

The reappearance of a positive and substantial term premium reflects a new risk premium demanded by investors to hold long U.S. debt. The proposed mechanism: the trajectory of federal debt — federal budget deficit persistently above 6% of GDP per CBO — imposes a compensation that short Treasuries no longer sufficiently offer, and which mechanically attracts foreign flows seeking to capture this term premium.

This explanation is favored by several Wall Street chief economists and the BIS in its March 2026 Quarterly Review. Its empirical coherence is strong: the correlation between the reappearance of positive term premium (mid-2023) and the maintenance of DTWEXBGS above 118 is observable. Its limit: the fiscal risk premium may pivot abruptly if markets lose confidence in the budget trajectory — the mechanism that today supports the dollar could tomorrow penalize it.

Hypothesis 3: defensive attractiveness and geopolitical fragmentation

The third reading places dollar persistence in the broader frame of geopolitical fragmentation. BRICS+ expanded with six new members in January 2024 (Saudi Arabia, United Arab Emirates, Egypt, Iran, Ethiopia, Argentina — the latter having since withdrawn). Tensions over Taiwan, Ukraine, Iran, and the Red Sea remain elevated. Western financial sanctions against Russia (freezing of Russian central bank reserves in February 2022) materialized a geopolitical risk on non-dollar FX reserves.

The proposed mechanism: in a more fragmented world, the dollar retains its default safe-asset status. Reserve flows observed via the IMF COFER report (Q1 2026) show that the dollar’s share of global FX reserves stands at approximately 58% — marginal erosion compared with 60% in 2015, but not the tipping point narratively announced. The confrontation between the de-dollarization narrative and observed reserve flows documents this resilience. More on this: the yellow metal gauged against the major currencies.

This reading has the advantage of direct observability — COFER flows, SWIFT volumes, and BIS statistics on international debt converge. Its limit: it assumes that defensive attractiveness will not reverse, an assumption the rapidity of monetary recompositions over the past ten years makes fragile.

The three hypotheses operate simultaneously

Current literature does not arbitrate between the three explanations. The most prudent reading acknowledges that they operate simultaneously, with relative weights that vary across sub-periods. The U.S. growth differential is documented and durable. The reappeared positive term premium is observable. The defensive attractiveness of the dollar is measurable.

The Eco3min analysis confines itself to posing the paradox and the three readings. The specifics are documented in our mapping of dollar shortage dynamics. It formulates no forecast for the remainder of the cycle. DTWEXBGS could continue its plateau trajectory above 118 for several more quarters — Volcker precedent supporting — or pivot abruptly if one of the three factors reverses. EM transmission in the current cycle is itself a feedback factor: a regional EM crisis would modify safe-haven flows and reinforce the dollar in the short term before penalizing it via trade-balance deterioration.

Concluding that Fed cuts have failed because the dollar has not declined ignores the coexistence of three simultaneous mechanisms. Interest-rate parity is not a law: it is a theoretical equilibrium condition that holds only all else equal. In the presence of a growth differential, a reappeared term premium, and active geopolitical fragmentation, the “all else equal” is precisely what does not hold.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…