DTWEXBGS: Reading the Broad Dollar Index as a Systemic Strength Signal

DTWEXBGS, the Federal Reserve’s broad dollar index, measures the dollar against 26 partner currencies weighted by bilateral trade flows. Its analytical reach differs structurally from the better-known DXY — a six-currency basket dominated by the euro and frozen in composition since 1973.

TL;DR

DTWEXBGS has held in its upper band for 28 straight months, a run unseen since Volcker, even as the Fed eased 100 basis points from September 2024.

- Over September 2024–May 2026, DTWEXBGS slipped only from 121.3 to 119.8 per FRED, against the 3-to-5% depreciation that interest-rate parity would project for a 100bp gap.

- The IMF's April 2026 WEO puts 2026 US growth at +2.3%, versus +1.5% in the euro area and +0.7% in Japan, channeling long-term capital toward US assets regardless of the short-rate gap.

- The IMF COFER report shows the dollar near 58% of global FX reserves in Q1 2026, down marginally from ~60% in 2015, well short of the de-dollarization tipping point often announced.

According to FRED data (May 2026), the index sits at 119-122, close to its September 2022 all-time high. The reading matters: the Fed has delivered -100 basis points of cuts since September 2024 with no meaningful erosion of broad dollar strength. How the distinction holds up across regimes is the subject of how strong dollar and weak dollar compare.

This article is not about the consequences of dollar strength on emerging economies, on the margins of U.S. multinationals, or on the cross-asset performance hierarchy. Eco3min covers those questions across five dedicated analyses, notably the structural regime of broad-dollar transmission to markets. The object here is upstream: framing the measurement instrument. What does DTWEXBGS actually measure, how is it constructed, and how can it be read as a signal without conflating it with the DXY? The link with the systemic role of the U.S. dollar in the global monetary system is not incidental: an aggregated index is never neutral, and the DTWEXBGS/DXY confusion has produced several flawed macro readings over the past decade.

1. What DTWEXBGS actually measures

The acronym stands for Daily Trade Weighted Exchange Rate Broad Goods and Services. The current construction dates to the methodological revision of January 2019, which replaced a family of earlier Fed indices (DTWEXB, DTWEXM, DTWEXO) with a unified architecture. The Federal Reserve Statistical Release H.10 publishes the detailed documentation weekly: 26 partner currencies, bilateral trade weights, annual rebalancing, January 2006 = 100.

1.1 Dynamic trade-weighted construction

The DTWEXBGS logic rests on three explicit methodological choices. First, the universe: the Federal Reserve includes the 26 economies that account for the largest share of U.S. foreign trade in goods and services. The selection threshold is not an absolute volume but a minimum share of bilateral trade. Second, weighting: each currency receives a weight proportional to its country’s share of U.S. exports plus imports, goods and services combined. Third, rebalancing: weights are recomputed annually to reflect actual trade-flow evolution. This dynamic separates DTWEXBGS from any fixed-composition construction. Related material: every dollar bull and bear market since 1973.

The yuan weight stood at approximately 21.5% in 2006, the first reference year of the rebased index. According to the latest Fed update (Statistical Release H.10, December 2025 revision), it sits at around 14.8% in 2026 — a significant decline tied to the falling Chinese share of U.S. trade in goods and services since the first round of tariffs in 2018. The Mexican peso, by contrast, has risen from approximately 11.4% in 2006 to nearly 14.2% in 2026, reflecting the nearshoring trend documented by the BIS and the OECD. The index therefore captures, by construction, the recomposition of U.S. foreign trade since the GFC, the 2018-2019 tariff shock, the COVID episode, and the post-2022 fragmentation.

1.2 The 26 currencies and current weights

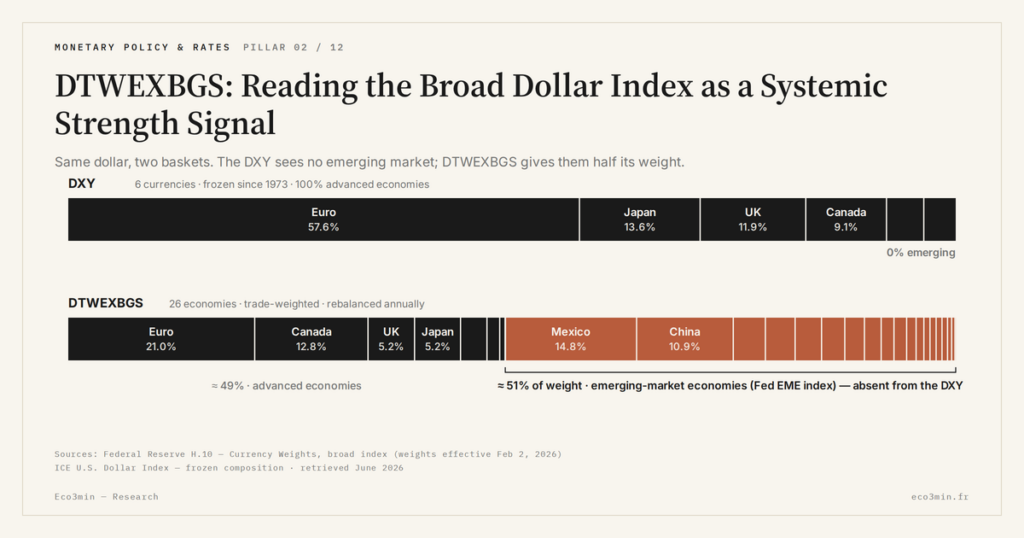

The 2026 DTWEXBGS composition, in descending order of approximate weight per Fed H.10 (December 2025): Chinese yuan (14.8%), Mexican peso (14.2%), euro (12.1%), Canadian dollar (11.7%), Japanese yen (5.9%), South Korean won (4.3%), British pound (3.8%), Brazilian real (2.2%), Indian rupee (2.1%), Singapore dollar (1.9%), Swiss franc (1.7%), Taiwan dollar (1.7%), Thai baht (1.3%), Hong Kong dollar (1.3%), Australian dollar (1.2%), Colombian peso (0.9%), Swedish krona (0.8%), Polish zloty (0.6%), Israeli shekel (0.6%), New Zealand dollar (0.5%), Chilean peso (0.5%), Norwegian krone (0.4%), Philippine peso (0.4%), Czech koruna (0.3%), Argentine peso (0.2%), Venezuelan bolivar (negligible).

This weight structure changes everything. DTWEXBGS jointly assigns nearly 29% to two emerging currencies (yuan + peso) that are completely absent from the DXY. Add the won, the real, and the rupee, and emerging-market economies account for more than 37% of total weight — a window the DXY closes entirely.

1.3 Base 100, frequency, and historical depth

The index is rebased to 100 in January 2006. This date is not narratively chosen: it is the first year for which the Fed has consistent trade data across all 26 selected currencies. what the DXY actually tracks sets out the mechanism in detail. Prior to 2006, earlier series (DTWEXB notably) cover the same conceptual perimeter but rest on a less homogeneous methodology. Publication has been daily since January 2019. Before that date, DTWEXBGS was computed weekly — a point that matters when comparing short-term volatility with the DXY, which has been quoted intraday since 1985.

According to FRED data extracted in May 2026, the historical record provides several useful reference points. Absolute trough: ~85 in July 2011, the low of the post-crisis cycle. Absolute peak: ~129 in September 2022, after ten months of accelerated Fed hikes and an acute European energy crisis. Current level: ~119-122. For context, the index reconstructs the 1973-2005 trajectory via earlier Fed series, allowing reconstruction of the Volcker peak of March 1985 at an equivalent ~127 and the post-Plaza Accord trough of 1995 at ~80. A related perspective: our analysis of what drives EUR/USD.

For the exact currency-by-currency calculation and the complete history of weighting revisions, the DTWEXBGS calculation methodology documents the official formula and the table of 26 weights.

2. Why the DXY is not enough

The DXY — U.S. Dollar Index — is the most visible instrument in daily dollar analysis. It benefits from massive derivatives liquidity (ICE futures, options, ETF) and intraday quotation since 1985. But its structure makes it unfit for the global macro reading DTWEXBGS is designed to deliver. More context: the dollar at the centre of the monetary system.

2.1 A composition frozen since 1973

The DXY was created in March 1973, just after the collapse of Bretton Woods. Its composition has been frozen since: euro (≈57.6%), Japanese yen (≈13.6%), British pound (≈11.9%), Canadian dollar (≈9.1%), Swedish krona (≈4.2%), Swiss franc (≈3.6%). The weights have never been revised in 53 years. No emerging-market currency is included: no yuan, no peso, no won, no real, no rupee. The basket reflects the U.S. commercial and monetary geography of 1973 — a world where China was outside the global trade system, where Mexico exported mainly oil, and where South Korea was barely beginning its industrialization. A useful reference here: The U.S. Dollar as a Systemic Variable in the Global Monetary System.

The euro weight itself is a historical artifact: in 1973, the DXY separately weighted the Deutsche mark, the French franc, the Italian lira, the Dutch guilder, and the Belgian franc. When the euro launched in 1999, these weights were mechanically added without methodological revision. Result: a purportedly global index that allocates 57.6% to a single currency.

2.2 EUR/JPY/GBP overrepresentation

The sum of euro (57.6%) + yen (13.6%) + pound (11.9%) reaches 83.1% of the DXY. Three developed currencies concentrate most of the signal. DTWEXBGS, for the same three currencies, allocates 21.8% combined — less than a quarter. This divergence is not anecdotal: it determines what each index can reveal.

A sharp dollar appreciation against the yuan, peso, and won — typical of a U.S. monetary tightening episode — will mechanically be invisible in the DXY if it coincides with a stable euro/dollar. Conversely, a euro weakness tied to a European energy crisis — as in autumn 2022 — will push the DXY well beyond what truly reflects the strength of the dollar against the full set of U.S. trade partners. The example is documented: between January and September 2022, the DXY rose +18%, the DTWEXBGS +12%. The 6-point gap is almost entirely attributable to the euro component. A broader view: gold’s real highs denominated in non-U.S. currencies.

2.3 When DXY and DTWEXBGS diverge

Divergences between the two indices are not random. They occur in three identifiable configurations. First, when an asymmetric regional shock hits one of the major developed economies without affecting emerging markets: euro crisis 2010-2012, Brexit 2016, European energy shock 2022. The reasoning is spelled out in the dollar shortage macro regime atlas. The DXY overreacts; DTWEXBGS remains measured. Second, when a tariff or financial shock hits emerging markets without affecting the euro or yen: EM crisis 2013 (taper tantrum), Turkish crisis 2018, Chinese devaluation August 2015. DTWEXBGS rises significantly; the DXY barely moves. Third, when restrictive U.S. monetary policy simultaneously tightens global financial conditions: 2022. Both indices rise, but DTWEXBGS remains a better proxy for the effective dollar pressure on the world economy.

The structural difference between DTWEXBGS and the narrower DXY deserves a separate treatment, comparing the two indices over fifty years and identifying the episodes where their readings diverge most.

3. Reading DTWEXBGS as a signal

Once it is clear what DTWEXBGS actually measures, the operational question becomes: how to read it? The signal lies not in absolute level but in three intertwined dimensions: level relative to history, speed of change, and cycle configuration.

3.1 Historical reference levels

Since 1973, the reconstructed DTWEXBGS has traced a wide band between ~80 and ~129. Four reference zones emerge. Below 90: structural weak-dollar regime — Plaza Accord 1986-1995, post-GFC 2009-2014. Between 90 and 105: broad neutral regime — Clinton-Greenspan 1995-1999, Obama 2014-2016. Between 105 and 118: moderate strong-dollar regime — late Volcker 1983-1985, Trump 2017-2019, Biden 2021. Above 118: marked strong-dollar regime — Volcker peak 1985, Plaza peak 1985, Powell peak 2022-2026.

According to FRED data of May 2026, the index sits at ~120 — in the upper zone for 28 consecutive months, a persistence not seen since the Volcker phase. This duration is the most analytically debated element: persistent dollar strength in 2024-2026 despite -100 basis points of Fed cuts has no precedent in the rebased index history.

3.2 Cycle dynamics

Absolute level does not say everything. The speed of variation materializes stress episodes. Over the 1973-2026 history, annual variations greater than +12% are rare — roughly once every five to six years. They coincide systematically with phases of accelerated U.S. monetary tightening: Volcker 1982, Plaza inverse 1984, Greenspan 1994, Bernanke 2014 (taper tantrum), Yellen 2016, Powell 2022.

The inverse — annual variation below -10% — is even rarer and systematically marks the ends of restrictive cycles: Plaza Accord 1985-1986, GFC exit 2009, post-COVID 2020-2021. The complete cycle signal, seven phases from 1973 to 2026, is documented in the historical taxonomy of broad-dollar cycles, which breaks down each pivot and its dominant driver.

3.3 Useful and misleading correlations

DTWEXBGS correlates well with some variables and poorly with others. Strong historical correlations: emerging-market financial conditions (strong positive correlation between DTWEXBGS and EM stress indices), sovereign EM CDS spreads (positive correlation), dollar prices of commodities (robust negative correlation over 30 years). Weak or misleading correlations: DTWEXBGS against U.S. equities (non-linear relationship across regimes), against gold (the classic negative correlation broke down in 2022-2024), against Bitcoin (no stable relationship identifiable). Related framing: the dollar leg inside gold’s return.

The most frequent analytical trap is conflating correlation and causation in the DTWEXBGS/commodities pair. The mechanism is real — a stronger dollar mechanically raises the price of dollar-denominated commodities for non-dollar buyers — but the inverse also holds: a demand shock on commodities affects trade balances and therefore dollar flows. Neither systematically precedes the other. A parallel read: Dollar vs gold: the reserve-asset tension.

Reading DTWEXBGS as a broader substitute for the DXY misses what the two indices actually measure. The DXY captures the value of the dollar against a frozen basket of six developed-market currencies dominated by the euro. DTWEXBGS captures the weighted force of the dollar against actual trade flows — including the yuan, the peso, and the won. When an analyst writes “the dollar rose,” the right question is: against what, and what was meant to be measured?

4. The 2024-2026 paradox

The current cycle presents a macro-reading problem that standard equilibrium models handle poorly. The Federal Reserve began its cutting cycle in September 2024: an initial -50 basis points, followed by -25 and another -25, for a cumulative -100 basis points as of May 18, 2026 according to FRED data. Classical interest-rate parity predicts that such an adjustment progressively weakens the currency concerned — at 100 basis points of differential, the expected effect over twelve months would typically run at -3 to -5%.

4.1 Fed cuts without dollar erosion

DTWEXBGS, over the same September 2024 – May 2026 period, moved from 121.3 to 119.8 per FRED. That is -1.2%. Compression exists but is ten times smaller than what parity models would predict. The fact is documented, but its analytical reading remains disputed. Three competing hypotheses are debated in central-bank and clearinghouse literature.

4.2 Three competing hypotheses

First hypothesis: the U.S. growth differential. According to the IMF (WEO April 2026), expected U.S. growth for 2026 is +2.3%, against +1.5% in the euro area and +0.7% in Japan. The differential attracts long-term capital flows toward U.S. assets — equities, corporate bonds, listed real estate — independently of the short-rate gap. This explanation is favored by the IMF and ECB working papers of late 2025.

Second hypothesis: fiscal risk premium and term premium. The nominal term premium on 10-year Treasuries stands at approximately +0.9% in May 2026 per the ACMTP10 series published by the New York Fed, compared with negative values throughout most of the 2014-2022 decade. The trajectory of U.S. federal debt — federal budget deficit persistently above 6% of GDP per CBO — imposes a risk premium on Treasuries that mechanically supports the dollar by attracting flows from foreign investors seeking to capture this term premium.

Third hypothesis: defensive attractiveness in a phase of geopolitical fragmentation. BRICS+ expanded with six new members in January 2024, tensions over Taiwan, Ukraine, Iran, and the Red Sea remain elevated, and reserve flows observed via the IMF COFER report (Q1 2026) show that the dollar’s share of global FX reserves remains at ~58% — marginal erosion compared with ~60% in 2015, but not the tipping point narratively announced. The dollar retains its safe-asset status, and the geopolitical premium offsets the short-rate decline.

None of these three hypotheses has received exclusive empirical validation. The most prudent reading acknowledges that the three mechanisms operate simultaneously, with relative weights that vary across sub-periods.

5. Limits of the signal

A measurement instrument is not an oracle. DTWEXBGS suffers from structural limits that any serious reading must integrate.

5.1 What DTWEXBGS does not measure

The index only measures trade flows in goods and services. It ignores by construction financial capital flows — portfolio investment, FDI, interbank swap lines, repo, derivatives markets. According to BIS Triennial Survey data (April 2025), daily FX market volume reaches approximately $7.5 trillion, the majority of which is non-commercial. DTWEXBGS therefore reflects commercial dollar pressure, not global dollar pressure in the market sense. A companion question: our primer on swap lines.

Second limit: it does not distinguish nominal from real. The nominal version (DTWEXBGS) does not account for inflation differentials between the United States and its partners. The Fed also publishes a real version (RBUSBIS) but only at monthly frequency, making it of limited use for real-time monitoring. During episodes of U.S. inflation outpacing partner-country inflation — typically 2021-2023 — the nominal DTWEXBGS structurally overstates the real strength of the dollar.

Third limit: it aggregates. A -3% move in DTWEXBGS may hide -10% against Asian emerging currencies and +4% against the euro. Disaggregation is not directly accessible from the main series; the index must be decomposed pair by pair to extract the geographic signal.

5.2 Frontier with de-dollarization

DTWEXBGS measures the strength of the dollar as a relative price on foreign-exchange markets. It does not measure the dollar’s share of global reserves, of international trade invoicing, or of sovereign and corporate debt issuance. These dimensions — which structure the de-dollarization debate — belong to other instruments. The IMF COFER report measures reserves. SWIFT publishes the dollar’s share of interbank payments (around 47% in March 2026). BIS publishes the dollar’s share of international debt (around 64% at end-2025). Read alongside: the dollar index since Bretton Woods.

A dollar whose share of reserves is gradually declining could perfectly coexist with an elevated DTWEXBGS, if institutional demand weakening is offset by transactional demand strengthening. Conversely, a falling DTWEXBGS does not imply structural de-dollarization. The confrontation between de-dollarization narrative and measured reserve flows resolves this question analytically.

6. An analytical reading grid

The grid proposed here is not a prescriptive method: it is a set of empirically verifiable observations to confront with the prevailing macro regime. First, consider DTWEXBGS as the reference instrument whenever measuring the strength of the dollar in terms of global trade flows. The DXY remains relevant for short-term trading and for measuring the dollar against developed-market historical currencies. This finding is put in perspective by the dollar as a systemic global variable.

Second, read the index in its cycle configuration. A level of 120 in a rising dynamic is analytically very different from the same level in a falling dynamic — particularly when anticipating the pressures on broad-dollar transmission to emerging markets and credit crises that follow.

Third, integrate the temporal dimension. A dollar strength that persists 28 consecutive months above 118 does not carry the same signal as a peak at 122 retracing within six months — the 1973-2026 history shows that prolonged durations without pivot are rare and coincide with durable global stress phases.

Fourth, never read the index in isolation. DTWEXBGS combined with the term premium, EM financial conditions (FCI indices), COFER flows, and CIPS volumes produces a far more robust reading than its standalone use. See the term-premium dataset for the construction and sources.

The full historical record is documented in the empirical audit of global crises associated with broad-dollar strength, accessible via the Eco3min historical dataset study covering 1973-2023.

The DXY has never measured dollar strength — it measures the inverse of the euro. DTWEXBGS is the only coherent tool for reading global dollar pressure.

A persistence that interrogates more than it resolves

Twenty-eight consecutive months above 118. One hundred basis points of Fed cuts without measurable erosion. A term premium that reappears after a decade of absence. A de-dollarization narrative that reflects neither in COFER nor in trade flows. DTWEXBGS, in May 2026, tells a story that standard equilibrium models translate poorly — and one that will be read sequence by sequence across the six satellite analyses of the cluster, from technical index calculation to emerging-market transmission, from the Fed paradox to the narrative-versus-real-flows confrontation.

- DTWEXBGS measures dollar strength against 26 trade-partner currencies weighted by bilateral flows and refreshed annually. It does not measure financial flows, the dollar’s reserve share, or differential inflation.

- The DXY, by contrast, has been frozen since 1973 and concentrates 83% of weight on euro, yen, and pound. The two indices answer different questions; neither is universal.

- In May 2026, DTWEXBGS sits at ~120 — 28 consecutive months above 118, a persistence not seen since the Volcker peak. The cumulative -100 basis points of Fed cuts since September 2024 has produced only marginal compression.

- Three competing hypotheses feed the reading of the current paradox: growth differential, fiscal risk premium via term premium, and defensive attractiveness in a phase of geopolitical fragmentation.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…

Inverted Yield Curve: Reading a Regime Signal Without Immediate Effect

The inverted yield curve operates as a regime signal, not a timing tool. Its lagged effects are constitutive…