Rate Hikes: Why the Economy Doesn’t Adjust Right Away

Monetary transmission is never instantaneous. Existing contracts, balance sheets and investment commitments propagate rate changes progressively rather than as an immediate shock. This inertia shapes the rhythm of the monetary cycle.

Monetary transmission is never instantaneous. Between a central bank’s decision and the real economy’s adjustment, contractual and financial mechanisms impose unavoidable lags. This structural inertia shapes the rhythm of the monetary cycle.

TL;DR

Most euro-area debt is locked in: roughly 85% of new mortgages are fixed-rate (ECB, Q3 2025), so a rate hike only bites at renewal or new origination, spread over years.

- The French household savings rate sits above 17% of gross disposable income (Banque de France, December 2025), a cushion that lets households absorb higher interest costs for several quarters before demand reacts.

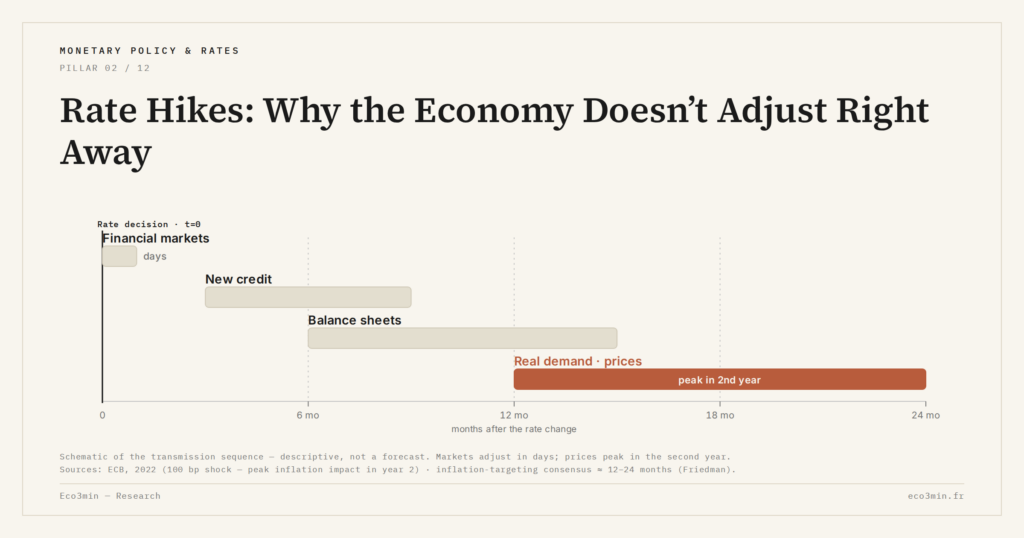

- Transmission runs sequentially — financial markets, then new credit, then balance sheets, then real demand; US corporate credit demand only softened in H2 2025, over three years into the tightening cycle (Fed SLOOS, January 2026).

Understanding these lags prevents conflating slowness with ineffectiveness. Existing contracts, debt commitments and investment decisions operate on fixed horizons that do not reset with every rate move. Monetary policy therefore propagates gradually rather than as an instantaneous shock.

A rate decision acts on activity with a lag, due to existing contracts, balance sheets, and structural rigidities in the economy.

When a policy rate rises, the real economy does not adjust immediately. Existing contracts, debt structures and investment behaviors evolve along preset calendars. This inertia creates a mechanical gap between the monetary decision and its first observable effects. The lag is not a malfunction: it reflects the contractual and sequential nature of economic adjustments. Separating decision time from transmission time helps avoid premature judgments on monetary policy effectiveness. A closer look: Our walkthrough of why earnings lag the monetary cycle. The empirical detail of these episodes is set out in the empirical record of market phases under an inverted yield curve.

Contracts that absorb the shock before transmitting it

The first brake on the diffusion of a rate hike comes from the structure of existing commitments. A fixed-rate mortgage taken out before the hike does not change cost for the borrower. An industrial leasing contract signed for five years retains its initial terms. Companies tied to confirmed credit lines continue borrowing at previously negotiated conditions.

In the euro area, according to ECB data (Q3 2025), about 85% of new mortgages were fixed-rate in the main markets — Germany, France, the Netherlands. The existing debt stock therefore remains largely insulated from policy rate moves for the full duration of these contracts. The real effect only emerges at renewal or new origination, a process spread over several years.

This contractual timing explains why the economy appears to keep moving despite monetary tightening. The absence of visible reaction is not a sign of ineffectiveness — it reflects an economy locked in by its own commitments.

The gradual adjustment of balance sheets

Beyond contracts, the balance sheets of economic agents add a second layer of inertia. A firm whose leverage remains sustainable in the short term does not immediately scale back investment plans. Households holding precautionary savings absorb higher interest costs without changing consumption for several quarters.

Banque de France data published in December 2025 show the French household savings rate above 17% of gross disposable income, a level significantly above the pre-2020 average. This financial cushion delays the transmission of monetary policy to domestic demand. The role of liquidity conditions in the transmission sequence takes on its full meaning here: as long as balance sheets absorb the shock, higher rates do not translate into a contraction in activity.

Equating the absence of an immediate recession after a rate hike with a loss of central bank power. This reading ignores that transmission mechanisms operate sequentially: first financial markets, then new credit, then balance sheets, and finally real demand. The effect exists, but it is distributed over time according to each economy’s financial structure.

The irreversibility of investment decisions

Investment projects committed before a rate hike generally run their course. A factory under construction, a real estate program already launched or an acquisition in final stages does not stop because the cost of capital rises by 100 basis points. The partial irreversibility of these decisions creates a momentum effect that temporarily sustains activity.

According to the Fed’s Senior Loan Officer Opinion Survey (January 2026), corporate credit demand only began to soften visibly from the second half of 2025, more than three years after the start of the US tightening cycle. The lagged effects on productive investment illustrate this structural gap between monetary decision and capital flow adjustment.

This reasoning becomes central whenever observers try to gauge the effectiveness of an ongoing monetary cycle. The real timeline of monetary diffusion through the economy is not read in the first weeks following a decision, but in the cumulative sequence of contractual, balance sheet and decision-making adjustments. Dominant projections expect a rapid return to equilibrium after the recent rate cuts — a scenario that probably underestimates the persistence of these rigidities.

The plurality of channels through which monetary policy diffuses implies that each channel has its own calendar. The calibration of decisions by monetary authorities must integrate this temporal dimension to avoid over- or underestimating the impact of each rate move.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…