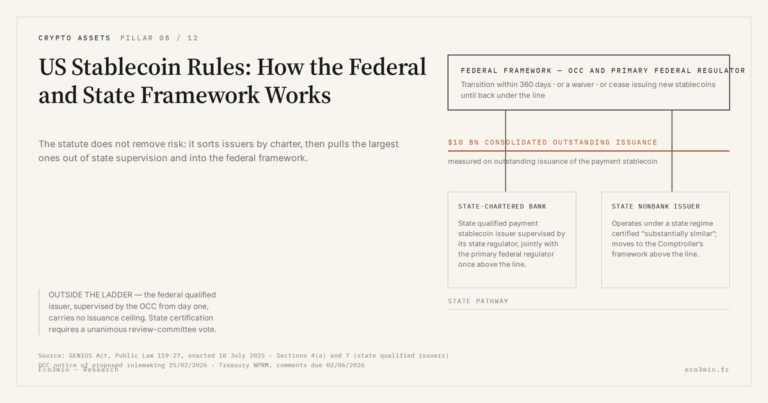

Inside Stablecoin Reserves: The T-Bill Backing Mechanics

Mapping the macro-financial impact of stablecoins requires opening their reserves. Circle’s April 2026 monthly transparency report breaks USDC down line by line: US T-bills with an average maturity of a few weeks, overnight repo collateralized by Treasuries, a limited share of bank deposits. Tether’s Q1 2026 quarterly attestation, less granular, points to a similar concentration on 1-3 month T-bills but retains a meaningful share of historically opaque other exposures. The backing mechanics place stablecoin issuers structurally close to US government money market funds — same underlying assets, same economic role of transforming liquid liabilities into short-dated paper. According to the Federal Reserve’s Flow of Funds (Q1 2026), MMFs held roughly $2.7 trillion in T-bills, against close to $130 billion for stablecoins. The gap remains an order of magnitude, but the stablecoin growth trajectory has been compressing it quarter after quarter, with implications for how short-end Treasury demand is priced.

TL;DR

Stablecoin reserves have converged onto the same short-Treasury assets as US government money market funds, a profile market arbitrage reached before MiCA and the GENIUS Act codified it.

- Circle's April 2026 report breaks USDC into roughly 75-80% short US T-bills, 15-20% Treasury overnight repo and 3-5% insured deposits, with a weighted average maturity near 30 days and the T-bill sleeve managed by BlackRock through the dedicated Circle Reserve Fund.

- Tether's Q1 2026 attestation, certified by BDO Italia, reports about $84 billion in T-bills and $12 billion in Treasury repo but still carries roughly $7 billion of historically opaque 'other' exposures that Circle's line-by-line reporting avoids.

- The distance from government money market funds is regulatory, not compositional: MMFs sit under SEC Rule 2a-7 (WAM ≤60 days, 30% weekly liquidity) and reach Fed facilities such as the MMLF and MMIFF in stress, backstops stablecoin issuers do not have.

- Short maturity keeps price risk negligible (a 100 bp curve shift moves a 30-day-duration reserve about 0.08%), but T-bill liquidity can degrade fast: in March 2020 bid-ask spreads widened from 1 to 5 bp and market depth fell 70%, per June 2020 BIS analysis.

The line-by-line structure of USDC reserves

Circle has published a monthly report since November 2022 detailing USDC reserve composition with a granularity that few shadow banking instruments offer at the same frequency. The April 2026 version breaks the assets into three principal categories: short US Treasuries (between 75% and 80% of the reserve depending on the month), overnight repo exclusively collateralized by Treasuries (15-20%), and insured bank deposits (3-5%). The portfolio’s weighted average maturity stands around thirty days, within an operational range of twenty to sixty days depending on subscription and redemption flows.

The report also names the counterparties: BlackRock manages the T-bill portfolio through the Circle Reserve Fund (USDXX), a dedicated MMF for which USDC is the sole investor. Bank deposits are split across BNY Mellon and a limited number of other systemically important banks, following the excessive concentration revealed at Silicon Valley Bank in March 2023. The architecture of subcontracted reserve management to an institutional asset manager is a particularity of Circle that distinguishes its operational model from Tether’s.

Tether attestations: a residual zone of opacity preserved

Tether publishes quarterly attestations certified by BDO Italia since 2023, covering USDT reserve composition as of the last day of each quarter. Granularity remains below Circle’s: T-bills are reported in aggregate without CUSIP-level detail, overnight repo is mentioned in bulk, and the “other exposures” category historically aggregates assets as varied as bitcoin-collateralized loans, positions in selected corporate bonds, precious metal deposits, and allocations to alternative investment strategies. Related framing: Comparing stablecoins and CBDCs across regimes.

According to the Q1 2026 report, US T-bills represented approximately $84 billion of the reserve, Treasury-collateralized repo about $12 billion, and bank deposits about $6 billion. The “other” share stood at roughly $7 billion, reduced compared to 2022-2023 but persistent. Emerging regulatory pressure — MiCA in the EU, GENIUS Act in the US — has been pushing Tether toward a more homogeneous reserve composition, but the transparency gap with Circle remains visible in the current reports.

For the macro-financial reading of this reserve plumbing, which places these compositions in the broader context of the stablecoin layer as a Treasury market actor, see the macro reading of this dollar plumbing layer, which develops the aggregate implications.

The underlying assets: T-bills, overnight repo, insured deposits

The three asset categories present in stablecoin reserves form a common foundation across regulated issuers and reflect convergent economic constraints. T-bills at 1 and 3 months offer a yield aligned with fed funds, near-instantaneous liquidity on the secondary market, and negligible price risk owing to their short maturity. Overnight repo collateralized by Treasuries provides even more immediate liquidity at the cost of a slightly lower yield. Insured bank deposits (FDIC limit at $250,000 per account) play the role of operational cash for daily subscription and redemption flows. A parallel read: the assumptions that mislead investors on market liquidity.

The European Union’s MiCA regulation and the US GENIUS Act converge on this list of eligible assets. MiCA further imposes a minimum cash share in the reserve (at least 30% for significant Asset-Referenced Tokens), while the GENIUS Act privileges T-bills with maturity of 90 days or less and Treasury-collateralized repo. Both frameworks exclude corporate bonds, equities, crypto-assets and secured loans, which forces convergence of reserve models toward a de facto standard.

Before MiCA and the GENIUS Act were finalized, stablecoin issuers had already converged toward a mix dominated by 1-3 month T-bills. The convergence reflects a simple economic arbitrage: for a liability convertible at par into dollars on demand, T-bills offer the best yield/liquidity/risk ratio among tradeable liquid assets. Regulatory pressure formalizes a state largely already reached through market discipline, rather than constraining the sector to a major operational pivot.

Comparison with US government money market funds

The most direct structural parallel is with US government money market funds, which similarly invest exclusively in short Treasuries and Treasury-collateralized repo. According to the Federal Reserve’s Q1 2026 Flow of Funds, government MMFs held approximately $2.7 trillion of T-bills, an order of magnitude above the aggregated stablecoin position ($130 billion). Both actors share the same economic function of transforming par-redeemable liquid liabilities into short Treasury paper. Read alongside: Our comparison of high-yield savings and money funds.

The differences are nonetheless visible. MMFs are supervised by the SEC under Rule 2a-7, which imposes strict constraints on maturity (WAM ≤ 60 days, WAL ≤ 120 days), liquidity (10% in daily cash, 30% in weekly cash) and credit quality. Stablecoins operate within a regulatory frame under construction that partially copies these constraints but has not yet reached the same degree of operational maturity. MMFs also have indirect access to Fed facilities during stress episodes (MMLF and MMIFF activated in 2008 and 2020), which stablecoin issuers do not enjoy.

For the architectural detail of this issuer and protocol layer, see the architecture of dollar-denominated stablecoins, which examines the relationship between technical infrastructure and economic consequences.

Average maturity and price risk profile

The weighted average maturity of USDC reserves stands around 30 days according to Circle reports, and that of USDT reserves around 45 days according to Tether attestations. The short duration minimizes price risk: a 100 basis point shift on the Treasury curve produces, on a 30-day duration portfolio, a value change of about 0.08% — well below the standard deviation of daily subscription flows. Market risk coverage is therefore essentially structural, embedded in the composition of the reserve itself. That structural, composition-level cover is what the reserve and backing requirements for stablecoins ultimately turn on.

Liquidity risk is more nuanced. In normal conditions, the secondary market for 1-3 month T-bills absorbs without difficulty volumes of several billion dollars. In generalized stress conditions, liquidity can degrade rapidly — the March 2020 episode during the Covid shock saw T-bill bid-ask spreads transiently widen from 1 to 5 basis points, and market depth fall by 70% according to BIS analyses from June 2020. This conditional liquidity profile constitutes the Achilles’ heel of backing mechanics in case of generalized run. For the reading of cases where this mechanism actually broke down, see how these mechanics fracture under run conditions, which traces the Terra 2022 and USDC 2023 episodes.

Synthesis — the nominal mechanics of backing

Stablecoin reserve composition forms a large-scale nominal transformation mechanism between par-convertible liabilities and short Treasury paper. The three actors — issuers, external asset managers (BlackRock for USDC), depository banks — operate within a regulatory frame rapidly converging toward US money market fund standards, without yet reaching their degree of stress-time protection. The nominal reserve profile, in non-stressed conditions, is broadly comparable to that of a government MMF; the residual gaps lie in transparency granularity (Tether vs Circle) and access to public liquidity facilities.

To situate the underlying short-rate series to which the reserve is exposed over a multi-decade horizon, see the FRED DTB3 dataset, which provides the historical record of US 3-month Treasury bill rates.

Frequently asked questions

Typical composition of the USDC reserve in April 2026

According to Circle’s April 2026 transparency report, the USDC reserve breaks down approximately into 78% US T-bills with average maturity of 30 days (managed via the Circle Reserve Fund by BlackRock), 17% overnight repo collateralized by Treasuries, and 5% bank deposits split between BNY Mellon and other systemically important banks.

Typical composition of the USDT reserve in Q1 2026

According to Tether’s Q1 2026 attestation, the USDT reserve breaks down approximately into 75% US T-bills, 11% Treasury-collateralized repo, 5% bank deposits, and about 6% other historically more opaque exposures (including bitcoin-collateralized loans and positions in selected corporate bonds).

Relationship between stablecoin reserves and the definition of a US money market fund

Fiat-backed stablecoin issuers and government MMFs invest in the same underlying assets and perform a similar economic function. The principal difference lies in the regulatory frame: MMFs are SEC-supervised under Rule 2a-7 with strict maturity and liquidity constraints, and benefit from indirect access to Fed facilities during stress. Stablecoin issuers operate within a frame under construction (MiCA, GENIUS Act) that partially copies these constraints without yet offering the same degree of systemic protection.

Last updated — 21 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

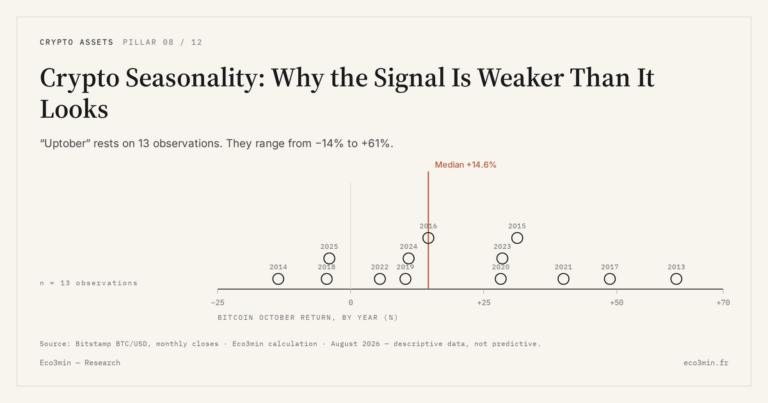

Full pillar →Crypto Seasonality: Why the Signal Is Weaker Than It Looks

Crypto’s cyclical regularities, monthly seasonality or the four-year cycle, rest on a very small number of observations. That…

Bitcoin Halving: How the Programmed Supply Cut Works

The halving writes bitcoin’s scarcity into an immutable rule, applied without exception since 2012. It shapes the pace…

Crypto Cycles: Why Their Amplitude Dwarfs Equity Swings

Crypto cycles post drawdowns two to four times deeper than equity markets. The asymmetry stems from market microstructure,…