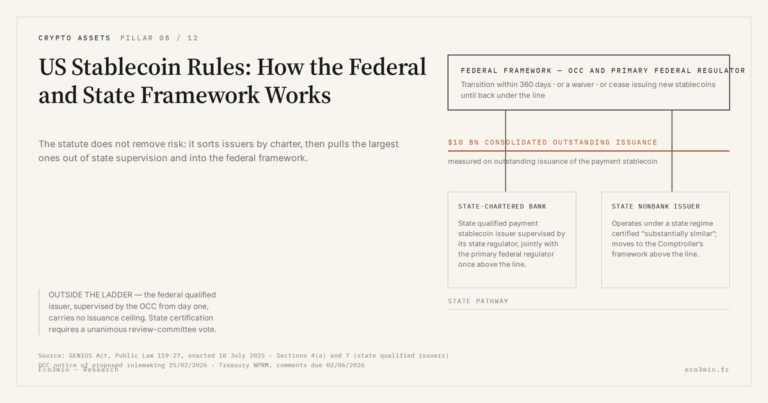

Stablecoin Runs: What Terra and USDC Revealed About Digital Shadow Banking

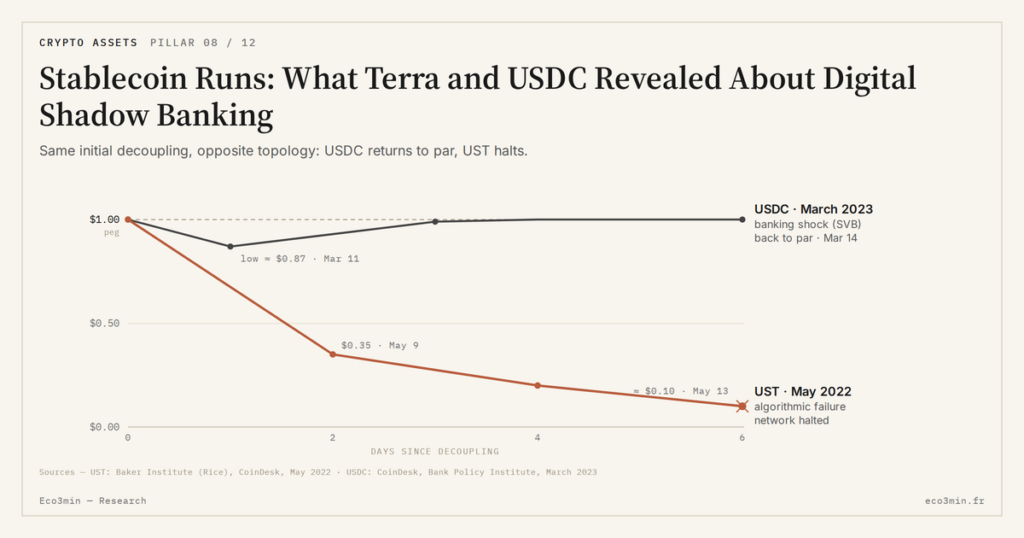

Two stablecoin runs delivered, ten months apart, a real-world stress test of digital shadow-money fragility. In May 2022, the collapse of TerraUSD wiped close to $18 billion in market capitalization within four days — an algorithmic failure rooted in a backing mechanism keyed to a volatile sister token, the reflexive dynamics of which had been documented well before the collapse (BIS Working Paper No. 1058, February 2023). In March 2023, USDC’s temporary depeg to 87 cents exposed a concentrated reserve allocation at Silicon Valley Bank in the 24 hours following the FDIC’s closure of the bank — a transmitted banking failure, not an algorithmic one. The two episodes illuminate a structural asymmetry: a stablecoin’s liquidity holds as long as the secondary market clears, but evaporates the moment confidence in the backing fractures. The mechanics resemble a classical bank run, without an equivalent regulatory backstop.

TL;DR

A stablecoin's liquidity holds only while confidence in its backing does, and both Terra's algorithmic collapse (2022) and USDC's SVB-driven depeg to 87 cents (2023) drained the secondary market within hours.

- Opposite triggers underlay the two runs. Terra was an endogenous algorithmic failure; USDC was a transmitted shock closer to a money market fund hit by a failing sponsor, after Circle disclosed that $3.3 billion of reserve (about 8%) sat at Silicon Valley Bank.

- TerraUSD lost 70% of its value in 72 hours after roughly $7 billion left Anchor Protocol (a 19.5% yield) between May 7 and 9, 2022, forcing escalating LUNA issuance that collapsed LUNA's market cap from about $30 billion to under $1 billion.

- With no lender of last resort and reserve reports monthly at best for Circle and quarterly for Tether, the only safety net is reserve composition itself; the par-redemption window stayed shut over the weekend while the 24/7 secondary market kept clearing, the desync that broke USDC.

TerraUSD, May 2022 — algorithmic collapse in four days

TerraUSD (UST) rested on an arbitrage backing mechanism with a volatile sister token, LUNA. At any moment, a UST holder could redeem it for a dollar’s worth of LUNA, and conversely mint UST by burning a dollar of LUNA. The system promised peg stability through automated arbitrage: if UST traded below $1, arbitrageurs would burn UST against LUNA to capture the spread; if UST traded above, the reverse operation would compress the price. The model rested entirely on the assumption that LUNA’s market capitalization would remain sufficient under all circumstances to absorb redemption of outstanding UST.

The trigger of the collapse was a massive capital outflow from Anchor Protocol, a Terra-chain lending protocol that offered a 19.5% yield on UST — an unsustainable rate that was the engine of structural demand. Between May 7 and 9, 2022, approximately $7 billion of UST was withdrawn from Anchor Protocol and pushed to secondary markets, triggering selling pressure that the arbitrage mechanism could not absorb. To restore the peg, the system had to mint growing volumes of LUNA, whose price collapsed under the weight of dilution. By May 10, UST traded below $0.70; by May 12, below $0.30; on May 13, the Terra network was halted.

The reflexive dynamics of the model had been documented in academic work before the collapse, notably in a Bank for International Settlements note dated January 2022, which identified precisely the downward spiral risk in the event of a demand shock. The academic lesson drawn rested less on the rarity of stress than on the predictability of its mechanics: an arbitrage system with a volatile sister token produces, under stress, effects opposite to those it aims for — accelerating the collapse rather than containing it. For the macro reading of the broader dollar layer in which these stablecoins sit, see the dollar plumbing layer these runs stress-tested.

USDC, March 2023 — depeg by banking contagion

The USDC episode of March 2023 obeys a different mechanic. On Friday March 10, 2023, the FDIC closed Silicon Valley Bank after a classical bank run — massive outflow of uninsured deposits in reaction to announced losses on the bond portfolio. Circle, the issuer of USDC, had communicated shortly before that $3.3 billion of the USDC reserve (roughly 8%) was deposited at SVB. The concentration was not known to the market before that disclosure. Related question: why SVB failed so quickly in March 2023.

The news triggered an immediate depeg: USDC, which traded at $1.00 before SVB’s closure, traded as low as $0.90 on Saturday March 11 on DEX secondary markets. The trough reached approximately $0.87 in the night of March 11-12. During those 48 hours, Circle’s institutional redemption channels were frozen — the par-redemption window operates only during US banking hours, and the episode broke precisely over a weekend. Recovery was gradual after the joint Treasury / Fed / FDIC announcement of Sunday March 12 evening, which guaranteed all SVB deposits. USDC returned to par on Tuesday March 14. A companion piece: the case for stablecoins or CBDCs.

The episode revealed two structural elements. The first is the combination of reserve concentration and partial opacity: without Circle’s proactive March 10 disclosure, the depeg might have taken longer to manifest on secondary markets, which would not have reduced the problem but altered its chronology. The second is the temporal asymmetry between a 24/7 secondary market and a 5-day banking window — the incident demonstrates that the par-redemption mechanism, which constitutes the ultimate guarantee of peg stability, is desynchronized from the secondary market in the most stressed periods.

Compared topology of the two runs

The two episodes do not rest on the same mechanism. Terra suffered an endogenous algorithmic failure: peg degradation self-amplified by construction, without a major external initiating shock. An endogenous failure of that kind is the case study driving the regulatory treatment of stablecoin reserves. USDC suffered a transmitted banking shock: peg degradation was triggered by the failure of an external counterparty (SVB), with a transmission mechanic that resembles more closely that of a money market fund exposed to a struggling sponsor than that of an algorithmic stablecoin. For the detail of nominal mechanics underlying this comparison, see the nominal backing mechanics outside stress, which decomposes USDC and USDT reserves line by line.

But the two episodes produced the same secondary market dynamic: rapid price decoupling in the first hours, widening of bid-ask spreads, rush to institutional redemption until channel saturation. The convergence is not accidental. It reflects a property common to any layer of par-redeemable shadow money: secondary market liquidity is conditional on confidence in par-convertibility. Once that confidence fractures, the secondary market shifts rapidly from an abundant-liquidity regime to a discrete-gap regime, irrespective of the exact backing mechanic.

The mechanics of digital runs and their asymmetries

A classical bank run unfolds over several hours or several days, in a window where authorities can intervene: withdrawal suspension, public guarantee, lender of last resort. A stablecoin run unfolds within minutes on a 24/7 secondary market, with no counter to close and no available regulatory intervention in the short window separating initial decoupling from stabilization or collapse. UST lost 70% of its value in 72 hours; USDC reached its trough in less than 24 hours before US authorities intervened indirectly through the SVB deposit guarantee announcement.

Three asymmetries define the risk profile of this layer. The first is temporal: the speed of secondary dynamics exceeds the reaction speed of public authorities, which operate on institutional horizons measured in business hours. The second is structural: the absence of a lender of last resort means the only safety net is reserve composition itself — a passive net, without discretionary reaction capacity. The third is informational: reserve reports, monthly at best for Circle and quarterly for Tether, do not provide the daily granularity needed for stress monitoring.

These asymmetries define the structural vulnerabilities specific to the stablecoin layer that past runs revealed without exhausting the perimeter — other failure modes remain conceivable and untested. To place these vulnerabilities within the broader architecture of dollar stablecoins, see the structural risks of this infrastructure.

What the regulatory frameworks under construction address — and what they do not

The MiCA regulation in the European Union and the GENIUS Act adopted in the United States in 2025 address part of the vulnerabilities revealed by UST 2022 and USDC 2023. On reserve concentration, both frameworks impose minimum diversification and exclude illiquid assets — which would, in principle, have attenuated USDC’s exposure to SVB. On transparency, they impose regular publication of attestations, without going as far as the daily granularity that would be needed for real-time stress monitoring. On resolution, they introduce orderly liquidation frameworks for failing issuers, but without direct access to a lender of last resort equivalent to that of regulated banks.

Three zones remain largely unaddressed by current regulations. The first is the cross-border dimension: an issuer can serve users in jurisdictions whose regulators have no jurisdiction over the issuer, creating a coordination gap that the Financial Stability Board began to address in its October 2023 report without yet closing it. The second is the absence of an equivalent of the Fed’s discount window for non-bank issuers. The third is the risk profile of residual algorithmic stablecoins and emerging yield-bearing stablecoins, which reintroduce through other paths the fragilities that regulatory frameworks aim to eliminate.

A comparison can be drawn with other forms of shadow banking whose regulation took shape in fits and starts following documented stress episodes — US money market funds before the 2008 and 2020 runs, and the broader debt-driven shadow banking layer with its own vulnerabilities. For broader systemic fragilities and shadow banking, that frame provides a comparison point on regulatory dynamics in the face of partially opaque maturity transformation.

Frequently asked questions

Mechanism difference between the May 2022 UST run and the March 2023 USDC depeg

UST suffered an endogenous algorithmic failure tied to the reflexive dynamics of its volatile sister token (LUNA) backing mechanism: peg degradation self-amplified without a major external initiating shock, triggered by massive Anchor Protocol outflows between May 7 and 9, 2022. USDC suffered a transmitted banking shock: the depeg was triggered by the FDIC’s closure of Silicon Valley Bank on March 10, 2023, followed by the disclosure that $3.3 billion of the USDC reserve was held there. Both episodes produced the same secondary market dynamic despite distinct initiating mechanisms.

Capitalization volume lost in the TerraUSD collapse

The collapse of TerraUSD between May 7 and 13, 2022 wiped approximately $18 billion in UST capitalization. The associated LUNA capitalization, which constituted the backing mechanism, fell from about $30 billion in early May 2022 to less than $1 billion at the end of the sequence. Cumulative loss for holders of both tokens exceeded $40 billion according to CoinMarketCap aggregates.

Lowest level reached by USDC during the March 2023 depeg

USDC reached a low of approximately $0.87 in the night of March 11-12, 2023 on DEX secondary markets. Recovery toward parity was gradual after the joint Treasury / Fed / FDIC announcement of Sunday March 12 evening, which guaranteed all SVB deposits. The return to $1.00 was observed on Tuesday March 14, 2023.

Last updated — 21 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Crypto Seasonality: Why the Signal Is Weaker Than It Looks

Crypto’s cyclical regularities, monthly seasonality or the four-year cycle, rest on a very small number of observations. That…

Bitcoin Halving: How the Programmed Supply Cut Works

The halving writes bitcoin’s scarcity into an immutable rule, applied without exception since 2012. It shapes the pace…

Crypto Cycles: Why Their Amplitude Dwarfs Equity Swings

Crypto cycles post drawdowns two to four times deeper than equity markets. The asymmetry stems from market microstructure,…