Stablecoins as Structural T-Bill Buyers: The Invisible Layer of Offshore Dollar Plumbing

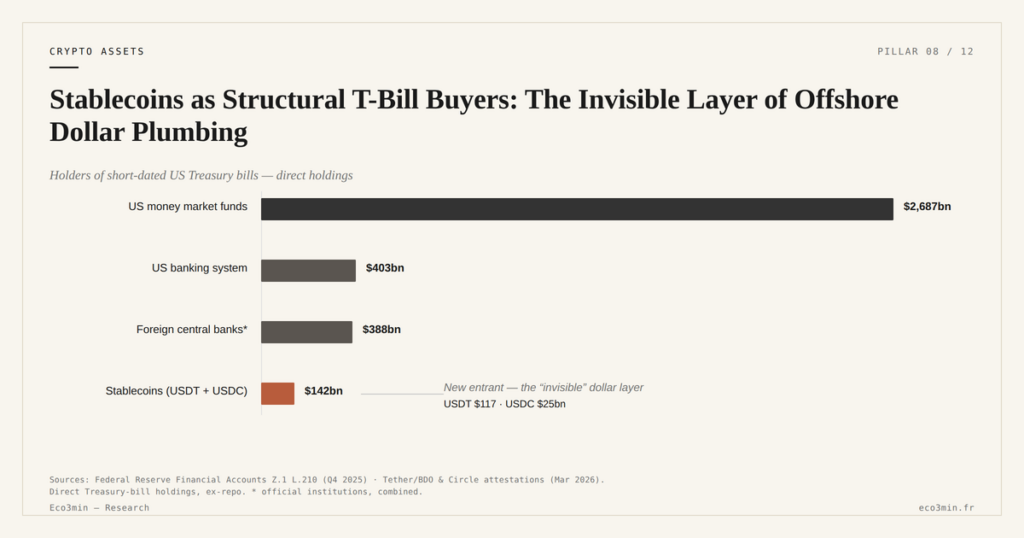

Stablecoin issuers have quietly become structural buyers of US Treasury bills at the short end of the curve. According to Tether’s Q1 2026 attestation and Circle’s monthly transparency reports, USDT and USDC together hold more than $130 billion in 1-3 month T-bills — enough to place them, on this segment, behind US money market funds and the banking system, but ahead of most foreign central banks outside Japan. That demand has turned a market widely framed as speculative into an infrastructural layer of offshore dollar plumbing. The argument of this study: stablecoins are not a crypto asset. They are a new form of dollar-denominated shadow money whose growth presses on short-end T-bill yields, accelerates dollarization outside the traditional banking circuit, and introduces systemic vulnerabilities that the runs of May 2022 and March 2023 began to expose.

TL;DR

With over $130 billion in 1-3 month T-bills, USDT and USDC now buy the short end of US government debt at the scale of a mid-sized foreign central bank.

- Total T-bill outstandings stood near $6.1 trillion at end-March 2026 (Treasury Direct), with money market funds holding about $2.7 trillion; stablecoins at $130 billion trail by an order of magnitude, yet their holdings grew roughly fourfold since end-2022 against about +60% for MMFs.

- The yield effect is small but measurable: Ahmed, Aldasoro and Duley (Journal of Banking and Finance, 2024) estimate 3 to 7 basis points of compression on 3-month T-bills per 10% rise in stablecoin capitalization, and because that demand is price-inelastic the pressure reverses mechanically during redemptions.

- Unlike banks (Fed discount window, BTFP since March 2023) and money market funds (MMLF, MMIFF in 2008 and 2020), stablecoin issuers have no lender of last resort, so generalized stress would force T-bill liquidation at market prices with no public backstop.

What this study covers when it speaks of stablecoins

The term stablecoin, in current crypto usage, refers to a digital asset whose unit price is pegged to a reference currency — most often the US dollar — by a dedicated mechanism. The family contains three subcategories with distinct properties: stablecoins backed by reserves of real fiat-denominated assets, stablecoins overcollateralized by other crypto-assets such as DAI, and so-called algorithmic stablecoins, where stability rests on an arbitrage system with a volatile companion token. The third category was effectively disqualified by the May 2022 collapse of TerraUSD. The present analysis focuses on the first, which carries the bulk of capitalization and all the macro-financial implications of the topic.

The observed perimeter centers on two issuers: Tether (USDT) and Circle (USDC), which together account for more than 90% of fiat-backed stablecoin capitalization at the start of 2026. Total capitalization in the segment crossed $200 billion according to DefiLlama aggregates from February 2026, against less than $30 billion at the start of 2021. The trajectory represents a sevenfold increase in five years, across a rate environment that has been successively zero, sharply rising, then stabilized at a historically elevated level. Growth did not reverse during the 2022-2024 hiking cycle, contrary to the intuitive hypothesis that elevated rates would have eroded the appeal of unremunerated dollar instruments.

The resilience reflects the use case for stablecoins, which is not reducible to crypto speculation. According to Chainalysis Geography of Cryptocurrency reports for 2024 and 2025, the bulk of on-chain USDT volumes corresponds to cross-border transfers — commercial settlements, informal remittances, hedging against domestic inflation in soft-currency jurisdictions. The stablecoin functions as a working digital dollar outside banking rails. The point is central to the macro-financial reading developed below: net stablecoin demand does not move mechanically with crypto risk appetite.

A complementary analytical layer is the digital dollarization layer approached from the perspective of decentralized infrastructure and protocol architecture. The present study departs from that view by anchoring its center of gravity outside the crypto system, in the consequences for global dollar plumbing. Reserve and ledger sit on two different layers, and it is the second that the infrastructure question around distributed ledgers addresses.

Reserve composition: what the T-bill layer actually holds

The macro-financial angle of the topic is won or lost in the reading of the reserves backing these tokens. Circle has published a monthly transparency report since November 2022 detailing USDC’s reserve composition line by line. The April 2026 version shows concentration on US Treasury bills with an average maturity of about thirty days, overnight repo collateralized exclusively by Treasuries, and a minority share of bank deposits held primarily at BNY Mellon. The granularity allows reconstruction of the reserve’s duration profile and its cash-to-securities ratio. Duration profile and cash-to-securities ratio are the very levers set by the composition and liquidity rules for stablecoin reserves.

The history of that publication is instructive. Before the move to line-by-line granularity in November 2022, Circle’s communication was more synthetic and did not isolate individual bank exposures. The concentration of USDC reserves at Silicon Valley Bank, revealed in March 2023 under stress conditions, accelerated the evolution toward finer disclosure. Since then, the monthly report names depository banks, the external manager (BlackRock for the T-bill portion), and weighted average maturity. The sector turned the episode into a de facto market standard.

Quarterly attestations published by Tether are less detailed. The Q1 2026 report, certified by BDO Italia, indicates similar concentration on 1-3 month T-bills but retains a residual “other exposures” line that has historically been more opaque, including in earlier editions bitcoin-collateralized loans and positions in selected corporate bonds. According to the same report, US T-bills represented roughly $84 billion of the Tether reserve at end of March 2026, which alone constitutes one of the largest individual positions on that market.

The convergence is documentable: the two principal issuers concentrate their reserves on the short end of the Treasury curve, with weighted average duration below two months. The concentration is not accidental. It reflects a simple economic arbitrage — short T-bills offer the best compromise between yield, near-instantaneous liquidity and negligible price risk — coupled with an emerging regulatory constraint that the forthcoming MiCA framework in the European Union and the GENIUS Act in the United States have begun to formalize.

This convergence places stablecoin issuers structurally close to US government money market funds, which similarly invest exclusively in short Treasuries and Treasury-collateralized repo. The comparison is more than analogical: it carries regulatory and systemic implications that US authorities have made explicit since 2023. For the granular asset breakdown, maturity buckets and comparative market shares, see inside the T-bill backing mechanics, which decomposes Circle and Tether reports line by line.

The actual weight on the short Treasury bill market

The 1, 3 and 6 month T-bill segment is, by construction, one of the most liquid debt markets in the world. Total Treasury bill outstandings stood at approximately $6.1 trillion at end of March 2026 according to Treasury Direct data, or close to 20% of marketable federal debt. The distribution of holders on this segment is concentrated: according to the Federal Reserve’s Flow of Funds for Q1 2026, US money market funds held about $2.7 trillion of T-bills, the commercial banking system about $700 billion, households and miscellaneous institutions about $1.1 trillion, and foreign holders about $1.3 trillion.

Stablecoins, at $130 billion, sit on this market at a rank that compares directly to mid-sized foreign central banks. As a reference point, according to Treasury International Capital System data, the Central Bank of Brazil held about $230 billion of total Treasuries at end-2025, of which only a fraction in short T-bills. Hong Kong’s financial system, combining the Monetary Authority and major banks, holds volumes of similar magnitude. Restricted to the short T-bill segment specifically, the stablecoin holdings approach those of actors such as Switzerland or Norway. A related perspective: our reading of persistent dollar strength against the Fed-cuts paradox.

The absolute gap with money market funds remains an order of magnitude — $2.7 trillion against $130 billion. But the growth trajectory has been compressing the gap. Aggregate stablecoin T-bill holdings expanded roughly fourfold between end-2022 and early 2026, while MMF holdings grew by about 60% over the same window. Extrapolated at constant growth, the stablecoin share would reach $300-400 billion by end-2027.

The yield effect is more delicate to isolate. Several academic studies have attempted the measurement. A paper published in the Journal of Banking and Finance in 2024 by Ahmed, Aldasoro and Duley, using weekly USDT and USDC capitalization changes to identify exogenous demand shocks on 3-month T-bills, finds a marginal yield compression of 3 to 7 basis points for a 10% increase in total stablecoin capitalization. The interval is narrow, but it confirms an econometrically detectable effect. The Bank for International Settlements, in Working Paper No. 1058 of February 2023, reaches a consistent order of magnitude using a different methodology grounded in market microstructure.

The effect is asymmetric. Stablecoin demand for T-bills is largely price-inelastic: an issuer places capital inflows almost instantaneously into eligible collateral, with little tactical room for maneuver. The inelasticity makes downward pressure on yields mechanical during growth phases, and upward pressure during contraction phases equally mechanical. The March 2023 episode, during the temporary USDC depeg, provided a real-world test of the dynamic: forced redemptions contributed to a transient rise in 1-month yields over a 48-hour window, observed by the BIS in a March 2023 note.

The stablecoin layer within offshore dollar plumbing

Offshore dollar plumbing refers to the ecosystem of dollar-denominated deposits and claims held outside the US banking system. The layer, whose contours are imprecisely measured, is historically dominated by the eurodollar market — interbank dollar deposits and loans operated by non-US banks, with outstandings estimated by the BIS at over $12 trillion in 2024. Alongside that classical system, a stablecoin layer is now developing whose annual on-chain transfer volumes crossed $2.5 trillion in 2024 according to the Chainalysis Geography of Cryptocurrency 2024 report.

The geography of usage is documented. Southeast Asia accounts for close to 30% of global USDT volumes according to Chainalysis, with particular concentration in Vietnam, the Philippines and Indonesia. Latin America carries about 15%, with rising weight from Argentina and Brazil. Turkey, Nigeria and parts of East Africa complete the map. In these jurisdictions, stablecoin usage is not speculative: it serves as a working dollar store of value in contexts of elevated domestic inflation, capital controls or banking instability. The use profile explains why correlation between stablecoin capitalization and the CoinGecko Top 100 ex-stablecoins index has remained low over 2023-2025, around 0.3, when intuition would have suggested a high correlation.

The distinction with the classical eurodollar system is economic in nature. Eurodollars operate on a fractional reserve banking model: a dollar deposit in a bank outside the United States serves as the base for a dollar-denominated loan, creating endogenous money. Fiat-backed stablecoins operate on a full-reserve model: each token issued corresponds, in theory and according to attestation reports, to one dollar-equivalent immobilized in a liquid asset. The absence of internal leverage changes the systemic profile. The stablecoin layer, at equal volume, mechanically generates fewer credit cycles than the eurodollar layer. The difference is partly attenuated by emerging practices of yield-bearing stablecoins and DeFi-replicated stablecoins with leverage, whose share remains minor but is growing according to DefiLlama 2025 data.

The historical comparison with the rise of the eurodollar market in the 1960s and 1970s offers context. Eurodollar deposits grew from a few billion at the start of the 1960s to over $1 trillion by the late 1970s, reshaping the offshore financing structure of multinational corporations and creating regulatory blind spots that took two decades for the BIS and central banks to map. The stablecoin trajectory, on a different scale and with different drivers, displays the same property of regulatory exteriority during its formative phase. Faced with that exteriority, several central banks have opened a file of their own: the state of play on central bank digital currencies.

The M1 and M2 aggregates published by the Federal Reserve do not capture stablecoins. Extended aggregates including shadow banking, published by the New York Fed, do not systematically integrate them either. The stablecoin layer remains largely invisible to traditional dollar money supply indicators. According to BIS estimates from 2024, including stablecoins would add approximately $200 billion to a global dollar aggregate that already incorporates eurodollars and MMFs, or about 1% of the total. The relative weight is small, but the growth angle and distinct risk profile justify a separate reading.

For broader monetary plumbing context — global financial conditions, QT-era dynamics, market impact channels — see the broader monetary plumbing context, which frames the operating environment in which any new dollar liability layer takes shape.

Digital shadow money: a distinct risk profile

The shadow money characterization of stablecoins is by now an established academic thesis. Gary Gorton, Yale professor, and Jeffery Zhang, then at the Federal Reserve, published in 2023 in the Michigan Law Review an article titled “Taming Wildcat Stablecoins” that formalizes the argument: stablecoins share the economic features of private money issued by US wildcat banks of the nineteenth century — par-redeemable liabilities into sovereign money, backed by assets whose quality is not guaranteed by a public authority, and susceptible to runs when issuer solvency is questioned. The historical lens has predictive utility: wildcat banks produced, between 1837 and 1863, recurring sequences of defaults and holder losses, until the National Banking Act standardized monetary issuance.

The analogy has been empirically tested twice in recent years. The May 2022 collapse of TerraUSD wiped out close to $18 billion in capitalization within four days. The March 2023 USDC depeg saw the token trade as low as 87 cents for 48 hours before regaining parity following the public intervention on Silicon Valley Bank. The two episodes do not rest on the same mechanism: Terra suffered an endogenous algorithmic failure tied to the reflexive dynamics of its backing model, while USDC suffered a transmitted banking shock from its reserve concentration at SVB. But both produced the same secondary market dynamic: rapid price decoupling, rush to redemption, partial freezing of redemption channels for USDC during the hours when the US banking market was closed. The comparative reading is developed in what the 2022 and 2023 stablecoin runs revealed, which traces the minute-by-minute chronology of both episodes.

A run on a stablecoin does not have the same topology as a classical bank run. It triggers within minutes on a 24/7 secondary market, with no counter to close and no available regulatory intervention in the short window separating initial decoupling from stabilization or collapse. The Terra 2022 and USDC 2023 episodes demonstrated that this temporal compression alters the very nature of operational risk for holders. Compression of that order leaves no window for any escalation chain built on business hours, which is operational risk measured in minutes rather than business days.

The absence of a lender of last resort is the property that most distinctly separates the stablecoin layer from the regulated commercial banking system. US banks benefit, through the Fed, from access to the discount window and, in case of systemic stress, to specific facilities such as the BTFP created in March 2023 during the regional banking crisis. US money market funds benefit indirectly from guarantees through the MMLF and MMIFF facilities activated in 2008 and 2020. Stablecoin issuers have no equivalent. In a generalized stress event on the layer, forced liquidation of T-bill reserves would occur at market prices, with no public backstop. More context: DeFi and traditional finance, two rails compared.

The absence defines the residual risk profile. It has two implications. The first is microeconomic: backing quality becomes the principal discipline mechanism for issuers, which explains the convergence toward short T-bills as reference asset and the rising pressure for reserve transparency. The second is systemic: a major stress event on a dominant issuer could trigger significant forced selling of T-bills, whose effect on the short segment is not trivial to isolate from other market movements.

The regulatory frameworks under construction aim precisely at mitigating these vulnerabilities. The European Union’s MiCA regulation, in force for the stablecoin chapter since June 30, 2024, imposes strict reserve, liquidity and disclosure rules on issuers of reference stablecoins (Asset-Referenced Tokens and E-Money Tokens). The GENIUS Act adopted by the US Congress in 2025 introduces an equivalent federal framework, with supervision combining the OCC for bank issuers and a specific status for non-bank issuers. The two frameworks converge on three principles: full reserve, eligible liquid assets restricted to T-bills, Treasury repo and insured bank deposits, and regular publication of attestations.

According to the IMF’s Global Financial Stability Report of October 2025, the cross-border footprint of stablecoins remains the dimension least covered by current frameworks. Issuers serve users across jurisdictions whose regulators have no jurisdiction over the issuer, creating a coordination gap that the Financial Stability Board has begun to address but has not yet closed.

Three documentable macro-financial implications

Marginal pressure on short Treasury bill yields

The effect of stablecoin demand on 1-3 month T-bill yields is modest at the individual issuer scale, but aggregated it becomes measurable. According to converging academic estimates (Ahmed et al. 2024, BIS WP 1058 of 2023), a 10% growth in global stablecoin capitalization compresses 3-month yields by approximately 3 to 7 basis points. On a capitalization trajectory from $50 billion to $200 billion between 2021 and early 2026, the cumulative effect would be on the order of 12 to 28 basis points on the 1-3 month segment. The order of magnitude remains below that of major monetary policy decisions — a 25 basis point fed funds move in direct transmission — but it is significant on the short compartment specifically. A broader view: How stablecoins and CBDCs compare.

Acceleration of dollarization outside the banking circuit

Dollarization refers to the use of foreign currency, here the dollar, in the monetary functions of a domestic economy — store of value, unit of account, medium of exchange. Historical episodes of dollarization (Argentina, Lebanon, Zimbabwe) rested on the use of physical banknotes or dollar-denominated bank accounts in jurisdictions that permitted them. The stablecoin layer bypasses the banking circuit by allowing dollar-denominated digital holding and transfer without a bank account. According to Chainalysis 2024 reports and IMF Working Paper 24/123 of June 2024, stablecoin adoption in soft-currency jurisdictions follows dynamics distinct from classical dollarization, with a lower adoption threshold (a smartphone and an internet connection are sufficient) and higher usage volatility than dollar-denominated bank deposits. For the broader macro frame in which the dynamic sits, see the real return record of US 3-month T-bills, which contextualizes the short-end dollar instrument over a multi-decade horizon.

A category of systemic risk with a distinct profile

The systemic risk specific to the stablecoin layer combines three unusual characteristics. The first is concentration: USDT and USDC together hold more than 90% of the segment, creating a very high idiosyncratic issuer risk. The second is partial opacity: despite improvements in transparency reporting, Tether’s quarterly reports do not provide the daily granularity needed for stress monitoring. The third is the absence of a lender of last resort, already documented. The Financial Stability Board, in its October 2023 report, explicitly classified reference stablecoins among emerging systemic vulnerabilities, recommending an internationally coordinated supervision framework that, by end-2025, has been only partially implemented.

An open architectural tension with the assigned sub-pillar

The present study is classified within the crypto infrastructure sub-pillar, which reflects the technical origin of stablecoins. But the macro-financial angle developed here belongs structurally to the sub-pillar dedicated to the global dollar system and offshore monetary plumbing. The tension is readable and deliberate. It reflects the current state of the topic’s evolution: stablecoins were born as crypto infrastructure, but their implications now reach far beyond that perimeter. Resolution of the architectural tension is a long-horizon editorial choice — either creating a dedicated digital monies sub-pillar within the monetary pillar, or maintaining the current attachment with explicit derivation. The present study leaves the question open, while acknowledging the dual framing.

Synthesis — what this invisible plumbing changes for reading the dollar system

The thesis defended in this study reduces to three empirical propositions. First, the stablecoin layer has become, at $130 billion of T-bills held by early 2026, a structural actor on the short Treasury bill market, comparable in size to mid-sized foreign central banks and exerting documentable marginal pressure on 1-3 month yields. Second, the layer functions as a new form of offshore dollar plumbing, with an economic profile distinct from classical eurodollars by the absence of internal leverage and the documented presence of non-speculative cross-border use. Third, it introduces into the global financial system a category of systemic risk previously unobserved, characterized by issuer concentration, partial reserve opacity, and the absence of a lender of last resort.

Four families of series allow empirical tracking of the stablecoin layer: capitalization and net flows via DefiLlama and CoinMarketCap (daily frequency); reserve composition via Circle transparency reports (monthly) and Tether attestations (quarterly); market effects via DTB3 and the Treasury yield curve published by the Fed (weekly); regulatory framework via ECB MiCA publications and US Treasury reporting for the GENIUS Act. Triangulation across these sources permits a reading that does not depend on intra-ecosystem narratives.

The reading completes naturally when placed against global monetary regimes and liquidity conditions in which the layer is embedded. It does not substitute for them: it adds an analytical layer to a macro-financial frame whose principal components — major central bank policies, dollar liquidity conditions, yield curve cycles — remain the primary determinants of the short Treasury segment.

Frequently asked questions

Difference between fiat-backed and algorithmic stablecoins

Fiat-backed stablecoins such as USDT and USDC rest on a reserve of real fiat-denominated assets — short Treasuries, Treasury repo, bank deposits — meant to fully cover circulation. Algorithmic stablecoins, of which TerraUSD was the archetype, rest on an arbitrage system with a volatile companion token without external asset backing. The May 2022 Terra collapse effectively disqualified the second model in its purest form. The present study deals exclusively with the first category.

Stablecoin holdings of US Treasury bills as of early 2026

According to Tether’s Q1 2026 attestation and Circle’s April 2026 transparency reports, USDT holds approximately $84 billion of US T-bills, and USDC about $36 billion. The aggregated total including other regulated issuers stands close to $130 billion, or 2.1% of total Treasury bill outstandings ($6.1 trillion according to Treasury Direct).

Relationship between stablecoins and US money market funds

Fiat-backed stablecoin issuers and US government money market funds invest in the same underlying assets — short T-bills and Treasury repo — and perform a similar economic function of transforming liquid liabilities into short-dated paper. According to the Federal Reserve’s Q1 2026 Flow of Funds, MMFs hold about $2.7 trillion of T-bills, against approximately $130 billion for stablecoins, a ratio of roughly 21 to 1. The stablecoin growth trajectory has been compressing the gap quarter after quarter.

Effect of stablecoins on short Treasury bill yields

Academic estimates converge around a yield compression on 3-month T-bills of 3 to 7 basis points for a 10% increase in global stablecoin capitalization (Ahmed, Aldasoro and Duley 2024; BIS Working Paper 1058 of 2023). The effect is below that of monetary policy decisions, but it is econometrically detectable and asymmetric in contraction phases.

Last updated — 30 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Bitcoin Halving: How the Programmed Supply Cut Works

The halving writes bitcoin’s scarcity into an immutable rule, applied without exception since 2012. It shapes the pace…

Crypto Cycles: Why Their Amplitude Dwarfs Equity Swings

Crypto cycles post drawdowns two to four times deeper than equity markets. The asymmetry stems from market microstructure,…

Bitcoin Cycle: A Quiet Inflection the Market Is Still Ignoring

A quiet on-chain indicator points to a different Bitcoin market regime, with material implications for allocation framing and…