Why a Strong Dollar Redefines the Hierarchy of Financial Performance

A durably strong dollar acts as a silent filter that reshapes the hierarchy of financial performance, dissociating local returns from real returns once converted into the pivot currency.

Financial performance is most often grasped through a local lens. Domestic indices, reported earnings, nominal growth and valuation gains constitute the usual benchmarks for judging the winners and losers of a cycle. This reading, however, quickly becomes misleading when international monetary conditions reorganize around a strong dominant currency. This redistribution of performance does not constitute a regime in itself, but one of the major effects of a durably strong dollar.

TL;DR

Measured in the dollar, the system's pivot currency, the ranking of winners and losers reorganizes, and an asset can rise at home yet underperform once converted into that pivot.

- A durably strong dollar filters performance through monetary exposure: international flows favor currency-adjusted returns, lifting some zones and penalizing others at constant fundamentals.

- At company level, revenues, costs and financing are rarely in the same currency, so when the dollar appreciates margins can compress before showing up in consolidated figures.

- The dollar reveals existing divergences and works as a permanent stress test: balance-sheet structure, external-financing exposure and flexibility decide which zones absorb the constraint.

In this context, an asset, a company or even an economic zone can display satisfactory apparent performance while deteriorating in real terms. The strong dollar then acts as a silent filter, redefining the hierarchy of performance without immediately altering local narratives. Strong dollar versus weak dollar, by the data unpacks where the two genuinely diverge.

Local Performance and Real Performance: A Structural Dissociation

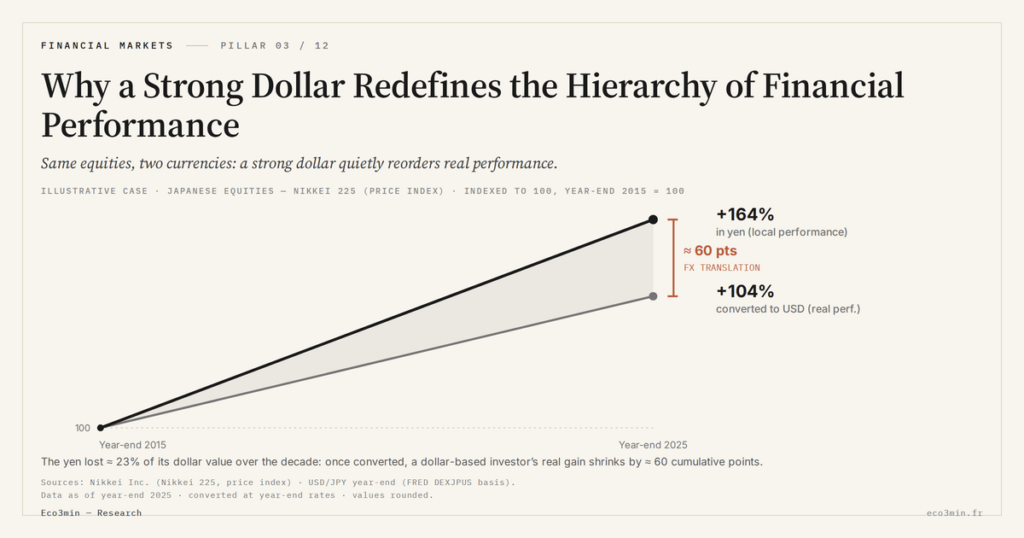

Any financial performance is expressed in a unit of account. Yet that unit is not neutral. When the dollar strengthens durably — a dynamic structurally tied to our currencies and FX markets sub-pillar — it modifies the relative value of performance expressed in other currencies, independent of local price developments. A concrete illustration appears in bullion records observed off the U.S. standard.

An asset can thus rise in domestic currency while underperforming once converted into the pivot currency of the financial system. This dissociation is not marginal: it constitutes a central mechanism of performance redistribution on a global scale.

The strong dollar imposes an implicit hierarchy. Performances are no longer only compared across assets or sectors, but filtered by their monetary exposure. This filter operates continuously, without visible signal, and explains a growing share of performance gaps observed across markets.

To correctly interpret this silent redistribution of performance, the role of the dollar must be placed within the global architecture of flows, valuations and arbitrage, as described in the reference analysis of how financial markets function.

The Dollar as Arbiter of Asset Performance

In a strong-dollar regime, the performance of financial assets can no longer be analyzed independently of their monetary anchor. International flows tend to favor returns adjusted for currency risk, which benefits some zones and penalizes others, even at constant fundamentals.

This logic extends beyond equity markets. It also concerns bonds, real assets and financing strategies. The dollar acts as an implicit cost or hidden advantage, depending on the structure of revenues and debts.

This mechanism helps explain why aggregate performance becomes less and less representative of the underlying economic reality. This dissociation between indices and real dynamics is examined more broadly in the study on the growing disconnect between index performance and company performance.

Companies and Margins: The Currency Effect as Silent Constraint

At the corporate level, the strong dollar acts as a revealer of structural vulnerabilities. Revenues, costs and financing are not necessarily denominated in the same currency. This asymmetry becomes critical when the reference currency appreciates durably. Related discussion: a map of what moves the euro.

Margins can compress without immediately appearing in consolidated figures. Trade-offs occur upstream: adjusting investments, renegotiating value chains, prioritizing cash management. Stock market performance can remain resilient in the short term, while real economic performance deteriorates.

This gap explains why some companies or sectors appear to outperform in a strong-dollar environment, even as their value-creation capacity progressively weakens.

Geographic Zones: Asymmetric, Not Synchronous, Performance

At the macro-financial scale, the strong dollar accentuates divergences between economic zones. Relative performance no longer reflects only internal dynamics, but the capacity to absorb an external monetary constraint.

Some zones see their assets supported by flows seeking relative currency stability, while others experience an erosion of their attractiveness despite acceptable domestic indicators. This hierarchy is neither fixed nor universal: it depends on balance sheet structure, exposure to international financing and economic flexibility.

The dollar does not create these divergences, it reveals them. It acts as a permanent stress test, redistributing global performance without necessarily provoking a visible macroeconomic rupture. The empirical test of this link is run in the analysis of dollar resilience absent systemic stress.

Common Errors in Reading Performance Under a Strong Dollar

A common error is to analyze performance exclusively in local currency. This approach masks the essential dynamic when the pivot currency moves sharply. Real performance then becomes a relative concept, dependent on the monetary reference point.

Another frequent bias is conflating market resilience with structural soundness. As long as prices hold and volatility remains contained, the implicit hierarchy imposed by the dollar is often underestimated.

Finally, excessive attention to domestic narratives leads to ignoring international flows. Yet it is those flows, filtered by the dollar, that largely determine relative performance in a globalized cycle.

Toward a More Structural Reading of Financial Performance

Understanding the hierarchy of performance in a strong-dollar regime requires shifting the analysis. The reference macroeconomic framework is laid out in the comprehensive guide on inflation. It is no longer just about comparing returns, but examining balance sheets, reference currencies and financing flows.

From this perspective, the dollar appears as an invisible arbiter. It does not directly dictate performance, but conditions its real meaning. This role becomes central in an environment where local performance and global performance increasingly diverge. On this point: The analysis of strong-dollar stress on the global economy.

This structural reading is deepened in the analysis of the impacts of a durably strong dollar on financial markets, which examines the channels through which the currency durably redefines performance balances.

Conclusion

The strong dollar does not just influence currency markets. It silently redefines the hierarchy of financial performance — a framework that fits within our reading of market regimes by dissociating local returns and real performance. This dissociation is one of the manifestations of imported inflation through exchange rates.

This redistribution does not occur through visible crises, but through progressive, asymmetric and often misinterpreted adjustments. The winners and losers of the cycle are not always those identified by domestic indicators.

When the reference currency shifts regime, performance ceases to be a number and becomes a relationship. foreign exchange markets and monetary regimes extends this reading across the cycle.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…

The ECB-Fed Rate Differential: the Driver of EUR/USD

The rate differential between the ECB and the Fed is the first-order driver of EUR/USD. But it is…