VIX 2023-2026: not a compression but a low calm twice broken by violent spikes

Since November 2024, the average VIX stands at 15.1 over eighteen months, 4.4 points below its 1990-2025 average. This durable compression recalls 2017 and 2019 — levels that preceded Volmageddon and the COVID crash — but the macro composition underlying it is unprecedented.

TL;DR

Three past low-volatility regimes (2017, 2019, and 2003-2007) each ended in a repricing the VIX never anticipated; the 2024-2026 compression, averaging 15.1 over eighteen months, now resembles them in duration.

- The maturation reading: zero-day (0DTE) options, introduced in May 2022, now make up 47% of SPX option volume per the CBOE Q4 2025 report, shifting hedging intraday where the 30-day VIX cannot capture it.

- The BIS Bulletin No. 78 (September 2025) reads the same low VIX as artificial suppression, citing autocalls above USD 730 billion and the February 2018 precedent, when retail short-vol open interest near USD 4.5 billion unwound and the VIX quintupled in five days.

- The combination of a low VIX, low HY OAS, a negative T10Y3M and record profits sustained over 24 months has no precedent since 1990.

Three structural factors — 0DTE, autocalls, record profits — feed the compression without any one of them being sufficient to explain its magnitude. What follows maps the observed regime, its historical comparables, and the monitoring indicators tracked by risk desks.

1. Empirical description of the 2024-2026 compression

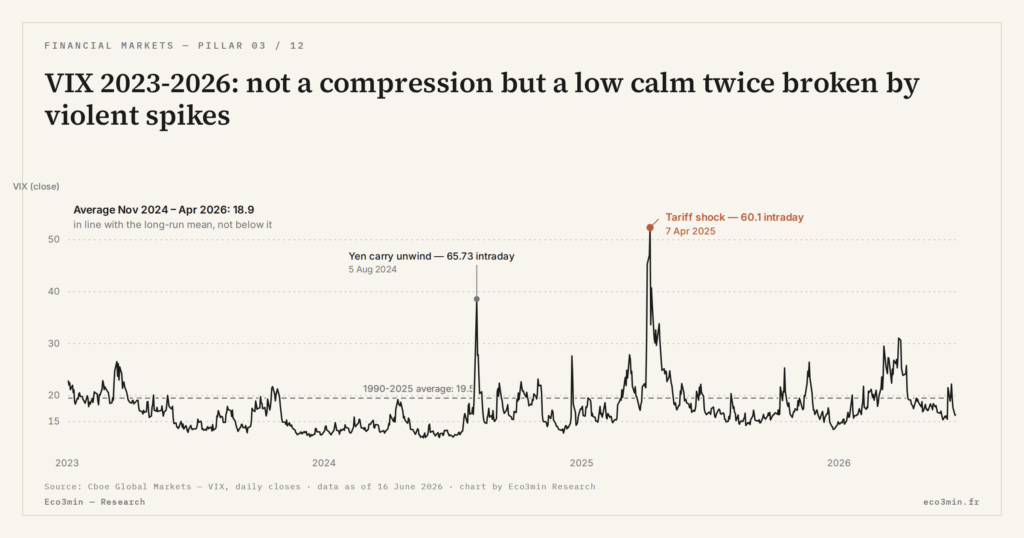

The VIX peaked at 65.73 intraday on 5 August 2024 during the yen carry trade unwind. Since then, its trajectory has been near-continuous decline. The average closing level between 1 November 2024 and 30 April 2026 stands at 15.1, against a 1990-2025 average of 19.5. Our note on the carry trade walks through the concept. Volatility of the VIX itself (30-day rolling standard deviation) stands at 3.2, against 5.8 historical average: compression is not only on level but also on within-regime dispersion. The underlying series: our VIX data series.

Four statistics characterise the phase. First: the percentage of sessions closing below 15 reaches 62% over the period, against a 31% historical average. Second: no spike above 30 has been recorded since the August 2024 yen carry trade unwind — the longest sequence without breaching 30 since 2017. Third: the VIX term structure (VX6 / VX1) is compressed at 1.06 on average, against 1.15-1.20 historically. Fourth: the volatility risk premium (VIX minus subsequent 30-day realised volatility) averages +1.8 points over the period, against +3.2 points over 1990-2025 — the seller-favour gap has tightened.

The pattern is not uniformly observed across all equity markets. The VSTOXX (Euro Stoxx 50) remains slightly higher on average (16.8 over the period); the VXN (Nasdaq 100) is compressed in similar proportions to the VIX (15.9 on average). The compression is therefore primarily a US phenomenon, with partial transfer to Europe via transatlantic hedging flows.

2. Historical comparables: 2017, 2019, and the 2003-2007 Greenspan phase

Three past periods show comparable VIX configurations. The closest and most discussed: 2017. The 2017 average VIX reached 11.1 — absolute annual record of the series —, with exceptionally low dispersion (standard deviation 1.6). The phase lasted roughly twelve months before the brutal repricing of 5 February 2018 (Volmageddon).

2019 (pre-COVID) constitutes a second comparable. The 2019 average VIX reached 15.4 with a trough at 11.03 in November. The phase lasted eight months between the late-2018 stress exit and the pandemic eruption in March 2020 (four months after the trough).

The 2003-2007 phase constitutes the third comparable, but over a much longer horizon. The five-year average VIX reached 14.7, with a historical trough at 9.89 in January 2007 — a level that would be followed seven months later by the first signal of the subprime crisis. The duration of this compression (five years) is exceptional and remains the longest of the full series to this day.

The qualitative pattern common to the three precedents: a durable compression followed by a repricing whose trigger was not anticipated by the VIX itself. The current 2024-2026 compression (18 months and growing) approaches in duration the middle of the 2017 / 2019 range, without reaching the 2003-2007 exception.

3. First reading: SPX options market maturation

The most widespread argument among sell-side strategy desks attributes the compression to the structural transformation of the SPX options market since 2022. Three elements compose this thesis. A companion piece: the VIX explainer: VIXCLS ticker and CBOE methodology.

The introduction of 0DTE options (zero days to expiration) in May 2022 and their subsequent explosion — now 47% of SPX option volume per the CBOE Q4 2025 report — has shifted institutional hedging into the intraday segment. Actors who hedged against 30-day risk via 30-day OTM SPX puts can now do so via more precise and less costly intraday 0DTE strategies. The VIX, which measures 30-day implied volatility, does not capture this intraday hedging — which mechanically keeps it at a low level. Related discussion: the Eco3min explainer on the VIX fear index.

Structural improvement of SPX liquidity is the second pillar of the thesis. Average daily volume rose from 1.8 million contracts in 2015 to 4.2 million in 2025. Book depth on deep OTM puts has densified. Bid-ask spreads have tightened. This improvement allows desks to hedge more efficiently, which compresses the volatility premium embedded in the VIX.

The third pillar is dispersion: hedging flows have fragmented across multiple instruments (SPX options, VIX futures, VIX options, volatility ETPs), which dilutes the impact of each individual flow on the 30-day VIX. Under this view, a low VIX reflects more efficient market infrastructure, not latent fragility.

4. Second reading: the BIS artificial-suppression thesis

The BIS Bulletin No. 78, published in September 2025, advances the opposite reading. The observed VIX compression would be the symptom of an accumulation of structured short-volatility positions exerting mechanical downward pressure on implied premiums.

Three vehicles are identified. European and Asian autocalls, whose outstanding amounts exceeded USD 730 billion at end-2025 per Citigroup Global Markets estimates: these structured products implicitly sell volatility to the market through their barrier mechanics. Covered call ETFs (notably JEPI, JEPQ, XYLD), whose assets grew from USD 28 to USD 117 billion between 2022 and 2025 per Morningstar: these vehicles systematically sell out-of-the-money calls, pressing down put-call asymmetry and therefore the VIX. Volatility carry funds, specialised hedge funds capturing the VIX futures contango slope: their estimated assets grew from USD 12 to USD 38 billion between 2022 and 2025 per HFR.

The BIS’s central analogy is the February 2018 precedent. Before Volmageddon, short-vol open interest on retail ETPs (XIV, SVXY) had reached USD 4.5 billion per SEC figures; in five days of forced unwinding, the VIX quintupled. If current short-vol positions are structurally larger and more opaque, VIX sensitivity to a trigger — whatever it might be — could be higher.

This thesis is not demonstrated, but it is supported by several indicators: CFTC non-commercial positioning is more net-short than in 2017; OTM put SPX open interest concentration has decreased relative to calls; monthly flows into covered call ETFs remain positive despite the low VIX level. For the cross-asset reading of this divergence with credit, see the joint VIX vs HY OAS analysis as a regime marker.

5. Third reading: structural macro change

The third thesis, more structural, attributes the compression to an unprecedented macroeconomic regime. High US nominal growth in 2023-2026 (+5% to +6% on average) supports corporate profits beyond consensus expectations. S&P 500 EPS grew 11% YoY in 2025 per FactSet, the fastest pace since 2018 excluding the COVID 2021 rebound. This profit growth absorbs part of the equity risk that, in other cycles, would have fed hedging demand.

The other structural factor is profit concentration on a small number of mega-cap tech names. The seven largest US capitalisations now generate 42% of S&P 500 profits per Bloomberg, which homogenises the equity risk distribution and reduces dispersion across sectors. This concentration can be read in two ways: as a source of fragility (a shock on a few names breaking the entire index) or as a source of short-term stability (profits remain solid as long as mega-caps hold). Both readings are compatible with the observed compression.

Under this view, the low VIX faithfully reflects an unprecedented macro reality, and the historical correlation between VIX, cycle and stress indicators was an artifact of the 2000-2019 cycles. This thesis implies that no brutal repricing is mechanically programmed as long as nominal growth and profit concentration persist.

6. Monitoring indicators tracked by risk desks

Five monitoring indicators are tracked by institutional risk desks to qualify the compression’s robustness. First: the VX2/VX1 slope of the VIX futures curve. A flip below 1.00 (partial backwardation) without identified shock on spot would be one of the first signs of latent destabilisation. This flip is not observed at end-April 2026.

Second: the VVIX/VIX ratio. An elevated VVIX without an elevated VIX signals latent anticipation of volatility increases. The 2024-2026 average VVIX stands at 95, slightly above its 92 historical average — a weak signal but consistent with the BIS thesis. On this point: our analysis of systemic risk indicators.

Third: the SKEW index. An elevated SKEW indicates investors pay heavily for crash protection even when the VIX is low. The 2024-2026 average SKEW is at 142, against 139 historical average — slightly elevated but without extreme signal.

Fourth: net flows into covered call ETFs. A brutal retraction of these flows would signal a turnaround of appetite for structured short-vol strategies. Flows remain positive and growing at end-2025 (+USD 3.2 billion in December 2025 per Morningstar).

Fifth: CFTC non-commercial positioning on VIX futures. A prolonged accumulation of short positions by non-commercials preceded Volmageddon 2018; current positioning remains net-short at a historically elevated level but without acceleration. The mapping of major historical episodes is documented in the catalog of the seven major spikes 1990-2026.

7. Overall reading: durable compression without identical macro precedent

The three readings are not mutually exclusive. SPX options market maturation and profit concentration coexist; structured short-vol positions accumulate in an environment where maturation makes their unwinding less risky than in 2018. The dominant sentiment among risk desks is that the compression may last another six to eighteen months without brutal repricing, but no historical precedent allows extrapolation beyond.

The most structuring observation is negative: the combination low VIX / low HY OAS / negative T10Y3M / record profits over 24 months is unprecedented since 1990. None of the three historical comparables (2017, 2019, 2003-2007) presents this exact combination. The current regime is therefore both reassuring in the short term (the absence of stress signal on three simultaneous indicators is consistent with real stability) and unstable over the medium term (the exit from this regime will necessarily be through an event not anticipated by traditional indicators).

- The average VIX between November 2024 and April 2026 stands at 15.1, 4.4 points below the 1990-2025 historical average; 62% of sessions close below 15.

- Three competing readings coexist: SPX options market maturation (0DTE, liquidity, dispersion), BIS artificial suppression (autocalls, covered call ETFs, vol carry funds), structural macro change (record profits, mega-cap concentration).

- Historical comparables (2017, 2019, 2003-2007) show durable compressions followed by repricings not anticipated by the VIX itself; none repeats identically.

- The combination low VIX / low HY OAS / negative T10Y3M / record profits over 24 months is unprecedented since 1990 — the most structuring negative observation of the current regime.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Euro Below Parity in 2022: What Parity Means

In September 2022, the euro fell below parity with the dollar, to around 0.95, a low not seen…

Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…