WALCL vs Market Liquidity: Real Signal Limits of the Fed Balance Sheet

WALCL aggregates the size of the Fed balance sheet, not the liquidity available to markets. Three structural limits distort the signal: the TGA, the ON RRP, and the accounting value of MBS. Each introduces a gap between the WALCL level and effective bank liquidity.

TL;DR

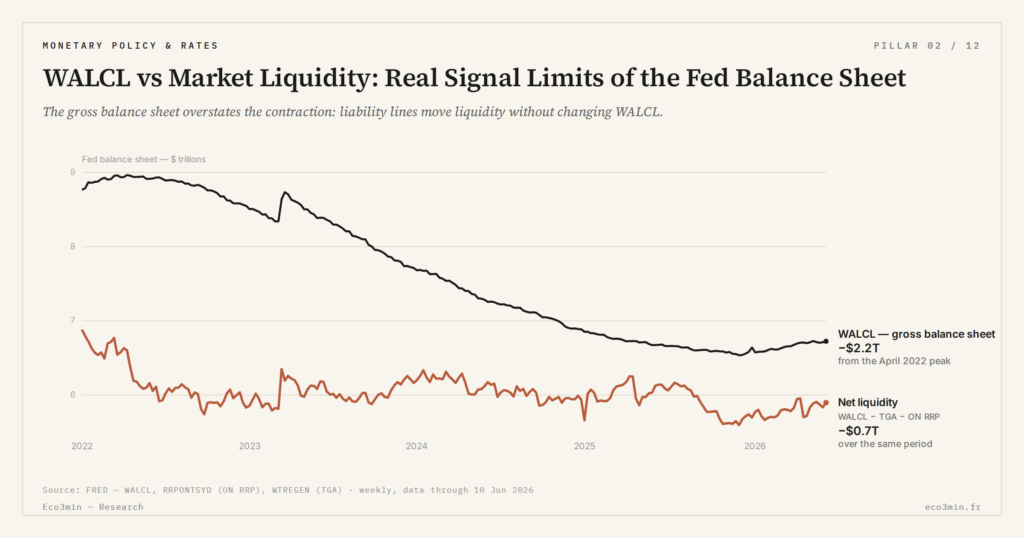

Three Fed liability lines — the TGA, the ON RRP, and amortized-cost MBS — sit between WALCL's headline level and the reserves banks actually hold, each moving liquidity without changing the aggregate.

- The Treasury General Account swings reserves with no WALCL change: it rebuilt from roughly $50 billion in June 2023 to roughly $700 billion by September 2023 after the debt-ceiling resolution, draining about $650 billion from bank liquidity.

- The ON RRP fell from about $2.55 trillion at its December 2022 peak to about $50 billion by September 2025, an offset that absorbed most of the parallel ~$2.2 trillion WALCL runoff and let QT2 run 42 months without a repo crisis.

- Held at amortized cost, the Fed portfolio carried roughly $1.1 trillion of unrealized losses in 2022-2023 (Federal Reserve System Annual Financial Report 2023) — a gap to market value the WALCL series never shows.

A rigorous reading requires knowing these three limits before interpreting a weekly WALCL move as a system-liquidity shift. Our Fed balance-sheet data compiles the full historical series.

WALCL is an indicator of the size of the Fed balance sheet, not of liquidity available to markets. This distinction is mechanical: between WALCL and effective bank reserves, several lines of the Fed’s liabilities absorb or release liquidity without changing aggregate WALCL. Knowing these lines and their dynamics distinguishes the rigorous analyst from the naive observer, even for someone who simply uses WALCL as the raw reference aggregate. A companion question: what the Fed balance sheet actually measures.

This article lays out the three main limits of the pure WALCL signal with their dated examples. It does not develop the construction of an alternative liquidity indicator: that more extensive argumentation is treated in the Liquidity Illusion deep study with its synthetic indicator. The present entry functions as an alert guide: when you see a strong WALCL signal, check these three variables before concluding. For the underlying time series, the daily Net Liquidity Index CSV download provides the data, and the formal computation of net liquidity documents the construction method.

Limit 1: the TGA and the US Treasury

The Treasury General Account (TGA) is the operational account of the US Treasury at the Fed. When Treasury issues debt and receives the proceeds, the TGA balance rises; when it spends, the balance falls. The TGA is a line of the Fed’s liabilities, on par with bank reserves. A TGA change therefore mechanically shifts liquidity between Treasury and the banking system, with no modification of WALCL. Related material: the Fed balance sheet compared with the ECB, BoJ and BoE.

The most telling example is the debt-ceiling episodes. When the US Congress blocks the ceiling increase, Treasury progressively depletes the TGA to keep paying federal obligations. Conversely, upon resolution of the block, Treasury reconstitutes the TGA to a target level, draining bank liquidity. According to the US Treasury Daily Statements, the TGA moved from roughly $50 billion in June 2023, in the final depletion phase pre-resolution, to roughly $700 billion by September 2023 after debt-ceiling resolution. This ~$650 billion reconstitution drained bank reserves by the same amount, with no WALCL change.

For an analyst watching only WALCL, the June-September 2023 episode would have suggested stable monetary conditions. The banking reality was a significant compression of available liquidity. The inverse holds in debt-ceiling block periods: a TGA decrease injects liquidity without modifying WALCL. The June 2020 episode (TGA at $1.8 trillion under Covid issuance) then August 2020 (TGA reduced to $300 billion through spending) injected ~$1.5 trillion of liquidity to banks in two months — invisible in WALCL. A related perspective: liquidity at the heart of price formation.

The operational conclusion is simple: watch the TGA alongside WALCL, especially during budget tensions or proximity to the debt ceiling.

A less spectacular but recurring variant concerns quarterly tax deadlines. US tax receipts arrive in concentrated waves — mid-April for income tax, mid-September and mid-December for quarterly corporate payments. During these few-day periods, the TGA can rise by $200 to $400 billion before contracting as Treasury redeploys spending. These TGA oscillations produce symmetric moves on bank reserves, sometimes wrongly interpreted as changes in monetary stance when they are purely fiscal chronology.

Limit 2: the ON RRP and the absorption of excess liquidity

The Overnight Reverse Repo Facility (ON RRP) is a Fed liability line that absorbs excess liquidity from money market funds, banks, and certain eligible non-bank actors. Counterparties deposit cash at the Fed against Treasuries as collateral, at a rate set by the Fed as a system floor. When the ON RRP grows, liquidity effectively available to the banking system decreases; when ON RRP shrinks, this liquidity is released. The daily FRED RRPONTSYD download provides the underlying time series.

The 2022-2025 phase provides the most spectacular illustration of this limit. At the December 2022 peak, ON RRP reached roughly $2.55 trillion according to Fed Reverse Repo Operations data. By September 2025, the outstanding fell to ~$50 billion. This ~$2.5 trillion decline spread over the same period during which WALCL fell by ~$2.2 trillion (see the current runoff phase where these limits matter most). Mechanically, the ON RRP drawdown offset most of the WALCL runoff: effective bank reserves remained relatively stable instead of compressing.

This offset explains why QT2 has been able to last 42 months without a repo crisis, in contrast to QT1 whose lack of a similar cushion led to the September 2019 tensions. An analyst who had projected liquidity compression proportional to the WALCL decline would have concluded to a crisis long ago. The reality is that effective liquidity has been recomposed, not compressed.

The operational conclusion: track WALCL and ON RRP jointly. The true bank-liquidity variable is their net differential, not WALCL taken in isolation.

A precision deserves mention on ON RRP eligible counterparties. The list determines which liquidity is absorbable: it includes the main money market funds, commercial banks, certain GSEs (Fannie Mae, Freddie Mac), and a limited number of primary dealers. Money market funds are historically the largest users, typically representing 80-90% of outstanding usage during intensive phases. This concentration creates an ON RRP sensitivity to MMF dynamics: when MMFs receive net inflows (typically during market-stress periods or rapid rate rises), they place a significant share in ON RRP. Conversely, when MMFs face outflows (typically during risk-on phases), they withdraw from ON RRP. This mechanic is a transmission channel often overlooked.

Reading WALCL as a direct indicator of bank liquidity regularly leads to errors. The TGA absorbs and releases reserves without changing WALCL; the ON RRP does the same on a larger scale; and MBS carry an accounting value decoupled from their market value. To interpret a WALCL signal, systematically check these three complementary variables.

Limit 3: the WALCL accounting value does not reflect market value

The third limit is more subtle but structurally important. WALCL aggregates the securities held by the Fed at amortized cost, not at market value. This accounting convention, specific to “hold-to-maturity” portfolios, masks valuation changes for long-duration securities.

The most documented case is the unrealized losses of the Fed portfolio in 2022-2023. According to the Federal Reserve System Annual Financial Report 2023, the Fed booked roughly $1.1 trillion of unrealized losses on its entire portfolio (Treasuries and MBS), mainly attributable to the rapid rise in yields in 2022-2023. These losses are not recognized in WALCL, which only records the acquisition cost minus amortization. The gap between accounting and market value reached historic levels with no signal in the WALCL series.

This limit has two practical consequences. The first is that Fed remittances to the US Treasury collapsed in 2022-2023, falling from ~$80 billion per year on average pre-2022 to a negative balance booked as a deferred asset. This fiscal compression — invisible in WALCL — remains relevant for the macro-fiscal analysis of the Fed-Treasury circuit. The second is that low-rate MBS held by the Fed and financed at high policy rates generate a structural negative carry: the Fed pays more in interest on its reserves than it receives in coupons on its MBS.

For reading the monetary stance, this limit is less critical than the prior two but deserves attention during duration stress periods. A sharp rate rise could widen unrealized losses to a level where the question of the Fed’s accounting solvency would return to academic debate — without that appearing in WALCL for quarters. What WALCL actually measures clarifies these structuring accounting choices.

The academic debate on the implications of a central-bank technical insolvency has resurfaced in 2023-2025 papers from authors at the Brookings Institution, the Hoover Institution, and several Fed regional research staffs. The dominant analytical view is that a central bank operating in fiat currency cannot be insolvent in the operational sense — it can always meet its obligations by creating reserves. The deferred-asset accounting treatment institutionalizes this view: the negative balance is carried forward and offset by future positive remittances, with no impact on the Fed’s ability to conduct monetary policy. But the political and communicational implications of large unrealized losses remain a non-trivial element of the contemporary policy landscape, and WALCL alone gives no information on this dimension.

The rigorous analyst thus has three reflexes to apply before interpreting a WALCL move: check the TGA (spot a debt-ceiling effect), check the ON RRP (spot a compensating absorption), and keep in mind the accounting-versus-market-value gap during rate-stress periods. These three checks are a necessary but not sufficient condition: for an integrated view, the deep study cited above builds a synthetic indicator that aggregates these variables. The present entry only signals the frequent-error zones for occasional users of WALCL and for those wishing to explore the multiple dimensions of liquidity in the system. Practical reading discipline matters more than indicator sophistication: a single weekly WALCL chart, looked at without these three checks, will produce false signals at every cycle inflection.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…