WALCL: QT Runoff 2022-2026, Pace, Projection and Terminal Cycle End

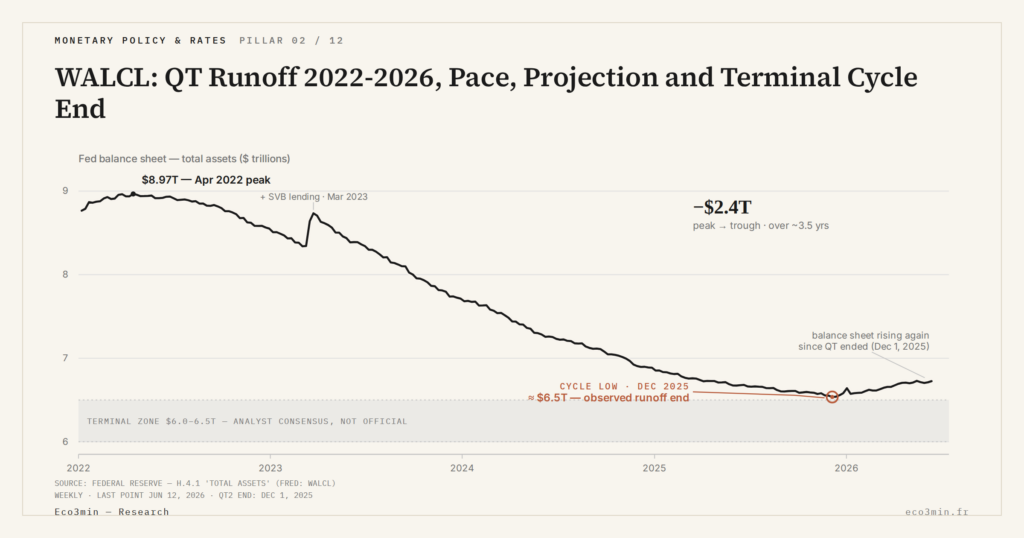

Since June 2022, WALCL has fallen from ~$8.97 to ~$6.8 trillion — a $2.2 trillion drawdown in three and a half years. The cap was modulated in May 2024; actual runoff oscillates between $35 and $50 billion monthly. The terminal size ($6.0-6.5T) is expected between H1 2026 and early 2027.

TL;DR

The Fed's QT2 has run past 42 months by late 2025 at an actual $35-50 billion monthly pace, below its $60 billion cap, longer than any prior balance-sheet runoff.

- Actual runoff trails the -$60 billion cap because Treasuries leave only at maturity and MBS prepayments stay weak with 30-year mortgage rates near 7% since late 2022, leaving the -$35 billion MBS cap rarely binding.

- The "QT phase vs post-QT phase" split may be a false binary: the variable-dosage regime points to a gradual exit (a further cap slowdown, a pause, or a flat terminal hold) read through FOMC Minutes rather than a fixed end date.

Reading the QT trajectory requires distinguishing three things: theoretical cap, actual runoff, and projected terminal size. The gap between these three variables conditions the landing window of the cycle.

Since the start of Quantitative Tightening 2 in June 2022, WALCL has been contracting continuously. See the WALCL series for the underlying data. The Fed has reduced its balance sheet from ~$8.97 trillion at the April 2022 peak to ~$6.8 trillion by late 2025, a drawdown of $2.2 trillion over three and a half years according to weekly FRED WALCL data. This trajectory combines three analytically distinct variables: the monthly cap authorized by the FOMC, the runoff actually realized each week, and the projected terminal size the Fed targets. The gap between these three variables is what makes the current phase interpretable.

The angle of this article is strictly the trajectory of the WALCL tool itself: runoff mathematics, end-of-cycle projection, comparison with the 2018-2019 QT. The ON RRP absorption mechanics that made this trajectory possible are treated elsewhere: the dedicated FAQ on QT market impact and the ON RRP / QT offset dataset develop the absorption argument in depth. The present analysis mentions the ON RRP as an environmental variable without repeating its demonstration. The broader context of WALCL as Fed monetary imprint since 2008 frames this operational reading.

Actual runoff pace vs theoretical cap

The monthly runoff cap set by the FOMC is an authorized upper limit, not a quantity actually removed. This distinction is mechanical but often elided in market commentary. The initial cap, in force from June 2022 to May 2024, was set at -$95 billion per month: -$60 billion on Treasuries and -$35 billion on MBS. On May 1, 2024, the FOMC lowered this cap to -$60 billion per month, primarily by reducing the Treasury cap to -$25 billion, with the MBS cap unchanged at -$35 billion per the FOMC Statements.

Actual runoff differs from the cap for two distinct reasons. On the Treasury side, runoff depends on the actual maturity calendar of held securities: the Fed can only let mature securities run off. When the monthly maturity volume exceeds the cap, the Fed rolls the excess; when it falls below, actual runoff is reduced. On the MBS side, runoff depends on prepayments, themselves a function of prevailing mortgage rates. In the context of 30-year rates at ~7% prevailing since late 2022, prepayments are structurally weak and the -$35 billion MBS cap is almost never binding.

Estimates derived from quarterly NY Fed SOMA reports indicate actual Treasury runoff oscillating between -$20 and -$30 billion per month in 2025, and actual MBS runoff between -$15 and -$20 billion per month. The effective monthly total thus sits around -$35 to -$50 billion depending on the week, markedly below the theoretical -$60 billion cap. This asymmetry deserves analyst attention: using the cap as a proxy for QT pace systematically overstates liquidity withdrawal.

The cap-versus-actual-runoff difference also has a consequence on balance-sheet composition over time. Because MBS run off more slowly than Treasuries, the relative MBS share in WALCL gradually rises — this is the composition asymmetry already documented in the instrument-by-instrument breakdown of Fed assets. The current QT is therefore structurally lopsided toward Treasuries in its pace.

Reading the authorized cap (-$60 billion per month since May 2024) as the quantity actually removed from the balance sheet systematically overstates the QT pace. Actual runoff oscillates between -$35 and -$50 billion monthly depending on the week. For precise reading, track the actual weekly WALCL variation, not the theoretical cap.

The mathematical projection of cycle end

At the actual pace observed since the May 2024 adjustment (~$40-45 billion monthly runoff), WALCL would reach the consensus terminal-size range between the end of the first half of 2026 and early 2027. This projection is purely mathematical: it extends the observed pace without prejudging coming FOMC decisions, and remains conditional on three variables.

The first variable is maintaining the current cap. The FOMC can at any moment further adjust the cap, eliminate it, or raise it depending on monitored-indicator evolution. The current QT regime doctrine, documented in the doctrinal regime defining today’s QT, privileges a gradual variable-dosage approach: an additional cap slowdown is the most likely option per the 2024-2025 FOMC Minutes, rather than an abrupt halt.

The second variable is MBS prepayment stability. A significant drop in 30-year rates (for example below 5%) would trigger a refinancing wave and accelerate MBS runoff toward the cap. Conversely, a rate rise would maintain prepayments at their current low level. The central scenario of most major analytical houses (Goldman Sachs, JPMorgan, Morgan Stanley, BNP Paribas) anticipates 30-year rate stability in the 6.5-7.5% range over 2026, which would maintain prepayments in their current regime.

The third variable is the absence of a stress event requiring QT interruption. The QT1 precedent (October 2017 – July 2019) was prematurely interrupted by the September 2019 repo crisis. Current structural conditions differ (see following section), but a major repo crisis or systemic banking event could force Fed purchase reactivation and close the QT2 cycle before reaching the projected terminal size.

Analyst consensus at major houses converges on a terminal-size zone of $6.0 to $6.5 trillion, without an official figure communicated by the Fed. Chair Powell indicated in May 2024 that the end of runoff would be announced “well before” bank reserves reached too low a level, without specifying a quantified target. The practical uncertainty margin on the end date thus remains significant — the exact timing will depend not on mathematical pace but on forthcoming official communication.

Comparison with QT1 (2017-2019) and structural differences

The QT1 precedent provides the most instructive reading grid for the current phase. Conducted between October 2017 and July 2019, QT1 reduced the balance sheet from ~$4.5 trillion to ~$3.8 trillion, roughly -$700 billion over two years — an actual pace of ~$30 billion monthly, markedly below the authorized cap of the time. The episode ended abruptly on September 17, 2019, when overnight repo rates reached an intra-day peak of 10% while the effective Fed Funds rate sat at 2.30%, breaching the top of the Fed’s target corridor for the first time since the financial crisis. The Fed had to inject emergency liquidity via overnight and term repos, then resumed Treasury purchases in October 2019 under the “not QE” framing per the official communication of the time.

Three structural differences distinguish today’s situation from September 2019. The first is the very existence of the Standing Repo Facility, created in July 2021 to provide a permanent backstop against repo-market stress. In 2019, this structural safety net did not exist; the Fed had to improvise emergency repos in the immediacy of the crisis. The second is the size of bank reserves: ~$3.2 trillion by late 2025 vs ~$1.5 trillion in September 2019. The current cushion is more than twice as thick. The third, more subtle, lies in communicational learning: the FOMC now explicitly documents the expected end of runoff in its Minutes and speeches, whereas in 2019 the official end was presented as a reactive response to repo tensions.

These differences do not guarantee an incident-free ending, but they modify the risk profile. A repeated repo crisis scenario as soon as ON RRP hits zero is not the central scenario for 2026; alternative scenarios include a pre-announced end of runoff coordinated with repo-stress indicators, or a voluntary block of ON RRP at a positive floor as a preserved cushion. Empirical observation of the repo spread SOFR-IORB, deposits at the Fed, and Treasury Bill rates constitute the next early-warning indicators to monitor. For reading-limits of pure WALCL during runoff, these complementary variables are essential.

The current phase remains unprecedented in cumulative duration. QT1 lasted 21 months; QT2 has already exceeded 42 months by late 2025 and could reach 50 to 55 months if the end is confirmed in 2026-2027. This extended duration is a characteristic of the current doctrinal regime — variable dosage rather than discrete operation. The sober analytical conclusion is that no historical QT phase offers a comparable precedent, and that the ongoing learning on the terminal balance sheet will condition the doctrine of future cycles as much as the contemporary transmission of balance-sheet policy to markets.

A final observation deserves explicit treatment: the analytical separation between “QT phase” and “post-QT phase” may itself be a misleading binary. The current regime, with its variable-dosage doctrine, suggests that the transition out of runoff will likely be gradual rather than punctual. The Fed may slow the cap further, pause runoff for a defined period, or hold at a stable terminal size with neither QE nor QT for an extended duration. Each scenario carries different implications for reserves dynamics, repo conditions, and the broader monetary plumbing. Tracking the FOMC Minutes and Powell speeches for shifts in the language used to describe the cycle’s next phase is therefore more informative than fixing a single end date. Related work: the liquidity regime and its price transmission.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…