ACMTP10 and the Fed Balance Sheet: How QE and QT Compress and Release the Term Premium

The central bank’s balance sheet is not an accounting byproduct of monetary policy but a standalone instrument that acts directly on the 10-year Treasury term premium, by removing or returning duration to the market.

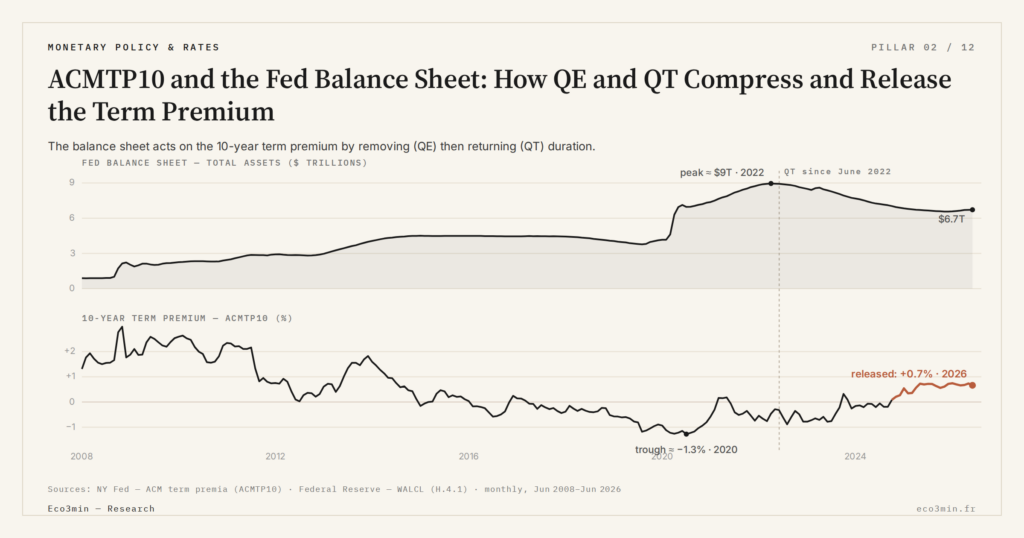

TL;DR

The Fed balance sheet moves the 10-year term premium through three separable channels (portfolio, signaling, habitat), at roughly 20 to 40 basis points per trillion dollars of duration.

- Three compounding channels carry the transmission: a portfolio effect (collateral removal), a signaling effect on short rates, and preferred-habitat (holder segmentation, Vayanos-Vila 2009).

- Operation Twist (September 2011-June 2012), 667 billion dollars of long Treasuries bought against short ones at an unchanged balance sheet, cleanly isolates the portfolio channel: roughly 15 to 30 basis points of compression attributable, with no signaling effect or injected cash.

- QE and QT are not symmetric (different macro conditions, communication, regulatory frictions), and post-2022 QT explains only part of the rise: federal deficits, an upward r-star revision, and foreign-holder recomposition act simultaneously.

Three transmission channels documented since 2011 explain how QE programs compress ACMTP10 and how post-2022 QT releases it, without thereby making the balance sheet the sole driver of the positive territory regained in 2024.

1. Why the Term Premium Reacts to Central Bank Balance Sheet Composition

The term premium is not a variable the Fed controls directly through its policy rate. For the term premium definition, recall that it is the residual demanded by marginal duration holders as compensation beyond expected short rates. The policy rate (federal funds rate) acts primarily on short rates and therefore on the ACMY10 expectations component, not directly on the ACMTP10 residual. The thread is followed through in how the Fed balance sheet differs from QE. To act on the term premium, the central bank must modify the quantity of duration available on the market — something only its balance sheet can do. Directly related: the role of central banks across the cycle.

The mechanism has been documented since the first quantitative easing program (QE1) launched by the Fed in November 2008. Gagnon, Raskin, Remache and Sack (2011) produced the reference study, followed by D’Amico and King (2013) on QE2 and several later works. The central proposition is simple: by buying long-duration Treasuries against short-term bank cash, the Fed effectively removes duration from the market and forces marginal holders to accept lower compensations. QT — quantitative tightening — runs the mechanism in reverse: the Fed lets its Treasury holdings mature without rolling them, which progressively returns duration to the market and widens the premium demanded. A related answer: why the term premium turned negative.

The empirical magnitude of the effect is substantial. Gagnon et al. (2011) estimate that QE1 reduced the 10-year term premium by 30 to 100 basis points depending on the assumptions. For the complete series, see our term-premium history series. Krishnamurthy and Vissing-Jorgensen (2011) produce comparable estimates while distinguishing effects on Treasuries, Agency MBS and corporate bonds. Across the full set of QE1, QE2, Operation Twist and QE3 programs, the cumulative effect on ACMTP10 is estimated between 100 and 200 basis points depending on sources — an order of magnitude consistent with the prolonged negative-premium phase observed through 2024.

2. Three Transmission Channels: Portfolio, Signaling, Habitat

The transmission from central bank balance sheet to term premium operates through three distinct channels that compound. Identifying each channel separately is not an academic finesse — it is what allows analysts to understand why certain QE episodes had stronger effects than others, and why QT transmission is not a perfect symmetry of purchase programs.

The first channel is the portfolio effect. By buying long Treasuries, the Fed removes collateral from the market. Sellers receive cash and must reallocate it to other assets — corporate bonds, MBS, equities, municipal bonds. This upward price pressure on other assets propagates the compression through the risk structure, and marginal holders now accept lower compensation for long duration. This is the most directly measurable channel because it acts on the physical quantity of duration in circulation. The Operation Twist episode (September 2011 – June 2012) is particularly informative on this channel: the Fed sold short Treasuries (under 3 years) and bought long Treasuries (6 to 30 years) for 667 billion dollars, keeping the total balance sheet unchanged. Neither a signaling effect on short rates, nor an effect of injected cash. Academic estimates converge on a 10-year term-premium reduction of roughly 15 to 30 basis points specifically attributable to Operation Twist — a figure that cleanly isolates the portfolio balance channel from the other channels.

The second channel is signaling. QE purchases signal a commitment to keep short rates low for longer than the policy-rate tool alone would suggest. The effect, foregrounded by Bauer and Rudebusch (2014), operates more on the ACMY10 expectations component than on ACMTP10 strictly speaking. But the two components are empirically hard to separate perfectly, and the ACM model can attribute part of the yield decline to the term premium when the underlying economic mechanism is signaling. The share attributed to each channel varies across episodes: QE3 (September 2012 to October 2014) likely operated more through the portfolio effect (expectations being already anchored by forward guidance), while the March 2020 Covid emergency programs combined strong portfolio effects with an immediate signaling impact in a context of liquidity panic.

The third channel is preferred-habitat. The theory of Modigliani and Sutch (1966), updated by Vayanos and Vila (2009), posits that certain investors have strong preferences for specific maturity segments: pension funds for the very long end (30 years), life insurers for the 10-20 year tenor, banks for the short end, money market funds for the very short end. When the Fed removes duration from a particular segment — for instance by concentrating purchases on the 10-year tenor during QE3 — it forces the preferred habitants of that segment to accept lower compensations or migrate to other segments. The compression then propagates by chain effect across the curve. Greenwood and Vayanos (2014) empirically calibrated this effect: a 1% change in 10-year duration free float translates into a few basis points on the demanded premium, nonlinearly and with threshold effects.

3. Stock Effect vs Flow Effect: the Empirical Calibration

A technical distinction structures the literature: does the balance sheet effect on the term premium operate through stock (cumulative balance sheet size) or through flow (monthly purchase/sale pace)? The empirical answer is: both, but with different weights depending on episodes.

The stock effect predicts that what matters is the total quantity of duration removed from the market. If the Fed holds 5 trillion of long Treasuries, the term premium reflects that stock independently of whether the Fed is actively buying or selling at the margin. This reading privileges the long-term inventory function of the balance sheet. The flow effect predicts on the contrary that what matters is the instantaneous purchase or sale pressure: the premium falls during purchases and rebounds as soon as they cease, independently of the cumulative stock. For the broader picture: Positive Term Premium: Implications for Treasuries and Equities.

Empirical evidence leans toward a combination of both. During QE3 (2012-2014), ACMTP10 fell during active purchases then partially rebounded when the Fed announced tapering in May 2013 — the “taper tantrum” that pushed the 10-year yield from 1.63% to 2.99% between May and September 2013. This violent reaction suggests a flow effect dominant in the short term. Conversely, over 2014-2017 when the Fed balance sheet remained stable around 4.5 trillion dollars without active purchases, the term premium remained durably low — suggesting a stock effect dominant in the medium term.

Post-2022 QT illustrates the same asymmetry. The June 2022 start of QT at a capped pace of 60 billion dollars in Treasuries per month (95 billion cumulative with Agency MBS) coincided with a progressive rise in the term premium. The June 2024 FOMC decision to reduce the pace to 25 billion in Treasuries per month marked a slowdown in flow pressure, but the stock continues to shrink — from about 8.9 trillion in mid-2022 to about 6.8 trillion in mid-2025 per FRED WALCL. The premium continues to widen, which argues for the persistence of a stock effect.

The combined empirical elasticity — aggregating stock and flow — can be read through the central-bank instrument set as a whole. A 1 trillion-dollar variation in Fed Treasury holdings empirically translates into about 20 to 40 basis points of variation in the 10-year term premium, depending on ambient market conditions. This order of magnitude is consistent with Vayanos-Vila and Greenwood-Vayanos estimates.

4. QE and QT Are Not Symmetric

A frequent error is to assume QT perfectly reverses QE effects. The empirical reality is more nuanced. Hanson and Stein (2015) documented an important indirect effect: QE purchases pushed certain actors into longer-duration assets than they would normally hold, creating an asymmetric vulnerability at the moment of QT. When these actors seek to unwind, the demanded premium can widen faster than the nominal pace of balance-sheet runoff.

Three sources of asymmetry explain this phenomenon. First source: macroeconomic conditions differ between QE and QT phases. QE is typically deployed in response to a deflationary or recessionary shock, in a context of structural demand for Treasuries as a safe asset. QT is typically deployed in an expansion or post-crisis adjustment phase, in a context where safe-haven demand is loosening. The same amount of duration removed then returned therefore does not have the same effects, because the underlying structural demand is not constant.

Second source: communication does not symmetrize. QE comes with dovish forward guidance that reinforces the signaling effect. QT comes with autonomization communication — the Fed explicitly indicates that QT is not the front line of monetary policy (Powell repeating that the policy rate remains the principal tool), which dilutes the QT signaling effect relative to the symmetric QE effect. This communication asymmetry is not accidental: it allows the Fed to run a balance-sheet policy in the background without interfering with its messages on the policy rate. The gap between the common account and the evidence is the focus of the false assumptions investors make about the Fed and monetary policy.

Third source: institutional frictions. Regulated holders (banks, life insurers, pension funds) face capital constraints, Solvency II, and actuarial matching constraints that modify their responsiveness to QT signals. A bank required to hold a certain duration stock for LCR (Liquidity Coverage Ratio) will mechanically absorb part of the returned duration, which dampens the premium effect. A pension fund whose funded status improves with rising yields will see its appetite for additional duration diminish, which on the contrary amplifies the premium effect. These frictions are documented by Du, Tepper and Verdelhan (2018) on covered interest parity deviations, and by Klingler and Sundaresan (2019) on pension funds.

5. Channel Limits: What QT Does Not Explain

Post-2022 QT does not suffice to explain the entirety of the ACMTP10 rise between 2022 and 2026. Several other factors contribute simultaneously, which the literature explicitly acknowledges. Identifying these other drivers is important to avoid overstating the share attributable to the central balance sheet.

First other driver: the expansion of US fiscal deficits. The Treasury Department has increased its net issuance of long Treasuries under two consecutive administrations (Biden then Trump’s second term), with a structural deficit projected around 6% of GDP over 2025-2030 per the Congressional Budget Office. This rise in net supply mechanically adds to QT in terms of effect on duration to be carried by the market. Second other driver: the upward revision of r-star — the real equilibrium rate — discussed by Powell at FOMC press conferences since 2024 and by Williams at NABE in October 2024 (revision toward a 1.0-1.5% real range versus a prior estimate near 0.5%). An upward r-star revision lifts the long-term anchor of all nominal rates, including the ACMY10 expectations component, which indirectly affects the global pricing of duration. Third other driver: the recomposition of the foreign holder base documented by Treasury International Capital Reports since 2016, with a structural reduction in the share held by China and Japan. Companion analysis: monetary metal and the management of federal debt. The point is developed in the copper-gold lens on financing conditions.

The detailed history of these factors is treated separately in the 2016-2024 negative episode and in the 2024-2026 positive phase. For analysis of the causal channel strictly speaking, it suffices to retain that the balance-sheet channel is a powerful but non-exclusive channel, and that the observed term premium is always the result of a combination of forces.

Conclusion

The Fed balance sheet is a documented transmission instrument of monetary policy onto the 10-year Treasury term premium, operating through three empirically separable channels — portfolio, signaling, habitat — with a combined elasticity of about 20 to 40 basis points per trillion dollars of duration removed or returned. QE and QT are not perfectly symmetric: different macroeconomic conditions, asymmetric Fed communication, and institutional frictions produce effects whose magnitude differs in absolute value. Reading ACMTP10 as a simple indicator of balance-sheet policy would ignore that other forces — fiscal deficits, r-star, holder base — act simultaneously and sometimes in opposing directions.

- The Fed balance sheet acts on the ACMTP10 term premium through three distinct but compounding channels: portfolio effect (duration removal), signaling effect (short-rate expectations), preferred-habitat effect (holder segmentation).

- Combined empirical elasticity stands around 20 to 40 basis points per trillion dollars of duration removed or returned, a calibration consistent with Gagnon et al. (2011), D’Amico-King (2013) and Greenwood-Vayanos (2014).

- QE and QT are not symmetric: different macroeconomic conditions, asymmetric Fed communication, and institutional frictions produce effects whose absolute magnitude differs.

- Post-2022 QT contributes to the ACMTP10 rise without being the sole driver — widened fiscal deficits, upward r-star revision, and recomposition of the foreign holder base operate simultaneously.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…