CAPE vs forward P/E vs trailing P/E: three valuation measures, three horizons, three readings

Three equity valuation measures circulate continuously in financial commentary and are regularly conflated: the CAPE (P/E on 10-year real earnings), the trailing P/E (on GAAP earnings of the last 12 months) and the forward P/E (on consensus sell-side earnings projected over the next 12 months). Their levels diverge sharply and that very divergence carries distinct analytical information.

TL;DR

The three common P/E measures each price a different earnings horizon, so the S&P 500 reads near 36 on CAPE yet near 21 on forward P/E in late 2025.

- The roughly 15-point spread between CAPE near 36 and forward P/E near 21 in late 2025 prices the same index about 70% higher on one measure than the other: extreme against the historical CAPE median near 17, merely elevated on forward P/E.

- At the 2008-2009 trough the trailing P/E ran above 100 as TTM earnings collapsed, while CAPE held near 13-15 and forward P/E sat between 14 and 18, a case where reading the trailing measure alone reverses the conclusion.

- Documented biases differ by measure: cyclically unstable trailing P/E, a sell-side forward P/E running 5 to 10% optimistic versus realized earnings (FactSet, McKinsey, 2000-2020), and a CAPE mechanically lifted by the 2001 FASB 142 goodwill break.

- The spreads themselves carry cyclical information: a widening CAPE-minus-forward gap flags consensus expecting margin expansion, while convergence of all three in the high zone, as in 1999 and 2021, marks a robust extreme-valuation regime.

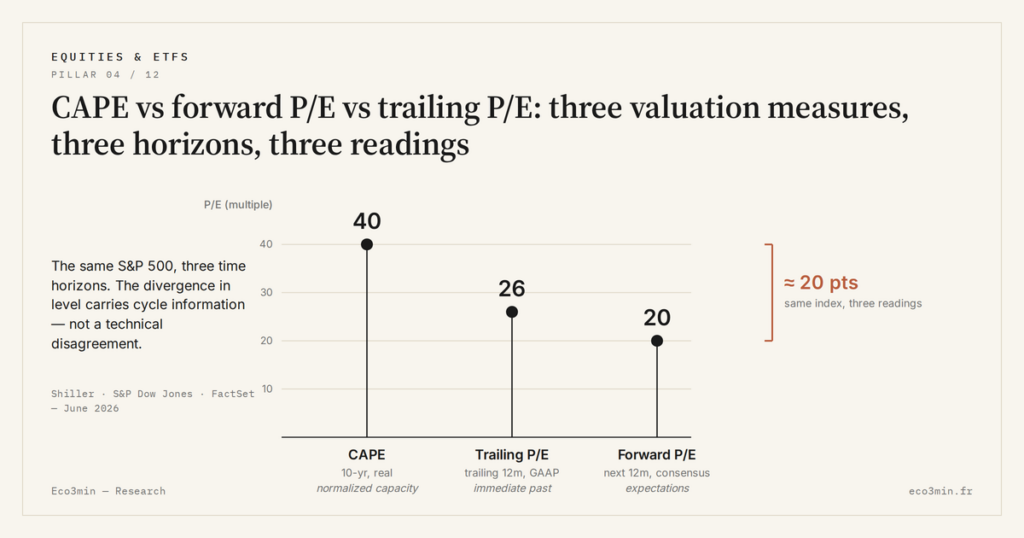

For the S&P 500 in late 2025 per FactSet and Shiller Online Data, the CAPE runs near 36, the trailing P/E near 26, the forward P/E near 21 — a dispersion that does not reflect a technical disagreement but three distinct temporal optics on the same asset.

1. Three Constructions, Three Optics

Trailing P/E — abbreviated to P/E without qualifier in most analytical material — is the historically dominant measure. Its construction is mechanical: current S&P 500 price divided by the sum of GAAP earnings for the past four quarters (Trailing Twelve Months, TTM). It captures the immediate-past optic: how much the market currently pays for earnings actually realized over the last twelve months. Its interpretive simplicity explains its popularity, and its continuous publication by S&P Dow Jones Indices ensures the availability of a long historical series.

Forward P/E is built from sell-side projected earnings over the following twelve months. The figures are published monthly by FactSet from aggregated consensus estimates of analysts covering S&P 500 companies. The optic is anticipations: how much the market currently pays for earnings the consensus expects in the next twelve months. Forward P/E is less volatile than trailing P/E — anticipations move more slowly than realized earnings — but it embeds a documented bias I return to in section 3.

The CAPE is the third construction, formalized by Shiller in 1988. Its optic differs from the other two: long-term retrospective. The current price is divided by the average of real (CPI-adjusted) earnings over the past ten years. The detailed CAPE calculation methodology covers the technical choices. What the ratio analytically measures is valuation against earnings normalized over a complete business cycle — capturing structural earning power rather than point-in-time earnings. the gap between CAPE and forward earnings multiples sets out the mechanism in detail. Adjacent reading: how real rates move equity multiples.

The three measures are not in competition for the same analytical use. They answer three distinct questions: how much am I paying for the immediate past (trailing), how much for the expected future (forward), how much for normalized earning power (CAPE). Conflating the three is the most frequent interpretive error in mainstream market commentary.

2. Historical Level Divergences

Over 1990-2025, the three measures have systematically diverged in level, with a relatively stable order of magnitude: CAPE above trailing P/E above forward P/E in normal expansive regimes. This hierarchy stems from the combination of mean inflation (which pushes the CAPE upward, ten-year-old earnings being in pre-inflation dollars) and the optimistic bias of sell-side consensus (which pushes forward P/E downward).

On the S&P 500 in late 2025, the gap between CAPE and forward P/E reaches roughly 15 points of multiple — 36 vs 21 per Shiller and FactSet data. This gap is significant: it means the same asset class is valued at roughly 70% more if the CAPE rather than forward P/E is used as reference. No reading of the equity market “level” can be indifferent to this divergence: depending on the chosen measure, one concludes that the S&P 500 sits in the extreme zone (CAPE against historical median ~17) or merely elevated (forward P/E against its 1990-2025 median ~16-18).

The divergences fluctuate over time. At the 2008-2009 crisis trough, trailing P/E exploded above 100 because TTM earnings had temporarily collapsed, while the CAPE stayed around 13-15 and forward P/E oscillated between 14 and 18 as the consensus updated. This dispersion in crisis is diagnostically informative: an explosive trailing P/E at cycle trough signals the temporariness of the earnings collapse, not a structural overvaluation. Reading the trailing P/E alone in this configuration would have produced an entirely opposite reading to that of CAPE and forward P/E — one of the most documented cases where measurement choice modifies economic interpretation. Related reading: The historical mapping of the equities-to-gold relationship.

Conversely, at bubble peaks (1999, 2021), the three measures converge toward the high zone. Trailing P/E and forward P/E rise because TTM earnings inflate less rapidly than prices, and the CAPE is structurally in the extreme zone. This convergence of the three measures in the high zone is precisely what empirically distinguishes extreme-valuation phases from mere cyclical distortion phases — the CAPE as the academic reference measure draws from this convergence its robustness as regime thermometer.

3. Documented Biases of Each Measure

Each measure carries a documented bias that must be internalized to avoid over-interpretation. Trailing P/E is cyclically unstable: its values at cycle troughs and peaks are not directly comparable to its values in expansion plateaus. This instability is not a conceptual defect — it reflects actual earnings mechanics — but it limits the use of trailing P/E as a long-term regime thermometer.

Forward P/E embeds the documented optimistic bias of sell-side consensus. Over 2000-2020, several FactSet and McKinsey studies have measured that actually realized earnings come out on average 5 to 10% below the twelve-month-ahead consensus. This structural bias is not neutral: it means that forward P/E published at time t systematically understates the P/E that will be observed retrospectively over the same period. A rigorous reading of forward P/E should mentally apply a 5-10% discount on the denominator to estimate the likely realized P/E.

The CAPE carries two documented biases. The first is its reduced reactivity to structural shifts: a change in underlying S&P 500 profitability — rotation toward high-margin services for example — takes ten years to fully incorporate into the decadal mean, which can keep the ratio in the “elevated” zone while the fundamental justification has structurally shifted. The second bias stems from the 2001 FASB 142 accounting break on goodwill treatment, which artificially depressed post-2001 GAAP earnings and therefore mechanically inflated the CAPE over the past two decades. The methodological critique of the CAPE by Jeremy Siegel and others documents both biases in detail.

Acknowledging these biases does not disqualify any of the three measures — it is precisely what allows their correct use. A rigorous reading of equity valuation combines the three optics without privileging one, and reads divergences as analytical signals of their own.

4. The Signal of Divergences

The gaps between the three measures carry cyclical information of their own, independent of their absolute level. First signal: a CAPE − forward P/E gap widening beyond the historical mean signals an anticipation of future margin compression by sell-side consensus. Forward P/E embeds twelve-month earnings anticipations; if anticipations are elevated, forward P/E falls, widening the gap with the CAPE which remains anchored on the decadal retrospective average. This configuration is observed in late-cycle phases, where consensus anticipates sustained earnings expansion whose intensity is not yet reflected in the decadal history.

Second signal: a forward P/E − trailing P/E gap widening signals a bullish consensus disproportionate to realized earnings. Mechanically, if forward P/E is significantly above trailing P/E — a rarer configuration — it means the consensus anticipates a sharp earnings drop over the next twelve months. This occurred briefly in 2008-2009 and again in 2020, in both cases before confirmed recessions.

Third signal: simultaneous convergence of the three measures in the high zone (all above their respective historical medians) signals the robustness of an elevated valuation regime, as observed in 1999 and 2021. This convergence differs from a static reading of a single ratio in the elevated zone: it eliminates cyclical artifacts (explosive trailing P/E at troughs) and anticipational artifacts (optimistic forward P/E).

Fourth signal: the Excess CAPE Yield level adds a transversal information layer by integrating real rates. The ECY construction from the CAPE and real DGS10 enables the distinction between extreme-valuation phases with and without a risk-premium cushion — the analytical extension of the pure CAPE that is most useful over the long run.

Beyond these four direct signals, the practical use of the three measures together requires a discipline of horizon-matching. The trailing P/E is the natural reading for short-term valuation against realized fundamentals, and is most useful in interpreting one-year forward P/E expansion or compression. The forward P/E is the natural reading for evaluating the alignment between current valuation and consensus expectations, and is most useful at points of divergence between sell-side optimism and underlying earnings momentum. The CAPE is the natural reading for evaluating the regime against historical norms, and is most useful for setting expectations on the decadal return distribution. Mixing horizons — using the CAPE to time short-term moves, or the trailing P/E to project decadal returns — produces interpretive errors that have nothing to do with the quality of the underlying measures and everything to do with their misuse. Further reading: our guide to the all-time-high debate.

- The three equity valuation measures answer distinct analytical questions: trailing P/E (how much for the immediate past), forward P/E (for the expected future), CAPE (for normalized earning power) — none universally superior.

- On the S&P 500 in late 2025, divergences reach ~15 multiple points between CAPE (36) and forward P/E (21) — a gap that radically changes regime diagnosis depending on the measure retained.

- Documented biases: cyclically unstable trailing P/E (P/E > 100 on S&P 500 in 2009), 5-10% forward P/E optimism vs realized earnings (FactSet, McKinsey), CAPE poorly reactive to structural shifts and sensitive to the 2001 FASB 142 break.

- Divergences between the three measures carry their own cyclical information — convergence in the high zone = robustness of an extreme regime, CAPE > forward P/E > trailing P/E divergence = bullish margin anticipations.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Reading Earnings Surprises: Cash Flow, Margins, Guidance

How to analyze an earnings surprise beyond the simple beat or miss: cash flow, margins, guidance, and weak…

Equal-Weight ETFs: The Quiet Signal Behind Rising Indices

Equal-weight ETFs reveal the true health of the equity market behind mega-cap-driven indices. Their gap with cap-weighted ETFs…

Smart Beta ETFs: The Hidden Risk Behind Factor Performance

Smart beta ETFs now hold ~15-20% of global equity ETF assets. Stacking factor exposures often rebuilds hidden concentration…