Excess CAPE Yield: Shiller’s equity risk premium mechanics and the 10-year forward returns forecast

Formalized by Shiller, Black and Jivraj in their 2020 paper “CAPE and the COVID-19 Pandemic Effect,” the Excess CAPE Yield (ECY) corrects a weakness of the pure CAPE by integrating the 10-year Treasury real yield — an operational metric of the current equity risk premium.

TL;DR

A +0.55 correlation with forward decade returns gives the Excess CAPE Yield an edge the pure CAPE loses in unusual rate regimes like 2021's negative real yields.

- In 2021, a deeply negative real DGS10 (around −0.8% per FRED) held the ECY near its 3.4% median even at CAPE 38-40; by mid-2026, positive real rates near 2.1% push it to 0.5-0.8%, closer to 1929 and 1999.

- The Fed model pairs trailing earnings with nominal yields, while the ECY uses decade-normalized CAPE earnings and real yields; the two can diverge, and the ECY inherits the CAPE's FASB-142 sensitivity (roughly 0.2 to 0.3% lower).

By mid-2026, the U.S. ECY oscillates at 0.5-0.8%, among the lowest levels historically observed over 1881-2025 — an analytical observation on the expected risk premium, not a timing signal.

1. The Mechanical ECY Construction

The Excess CAPE Yield is built in two simple steps that must be treated separately to avoid conceptual confusion. Step 1: invert the CAPE to obtain the CAPE-based earnings yield, representing the implicit real equity return under the Shiller measure. At CAPE 35, this earnings yield equals 1/35 = 2.86%. This inversion produces an intuitive measure of expected real return if decadal-normalized earnings remain constant in real terms — a strong assumption but useful as analytical reference. The same logic extends in the link between the stock index and gold as a real-wealth benchmark.

Step 2: subtract the 10-year Treasury real yield to obtain the spread between the two real yields. The real DGS10 yield itself is built by subtracting the T10YIE breakeven inflation (10-Year Breakeven Inflation Rate) from the DGS10 nominal yield. Concretely in May 2026, with a nominal DGS10 around 4.2% and a T10YIE breakeven around 2.1%, the real DGS10 stands around 2.1%. The current ECY therefore equals 2.86% − 2.1% ≈ 0.76%. The reference grid of the CAPE as academic measure provides the context for both variables.

The ECY conceptually measures the expected risk premium of equities over real Treasuries, read through the Shiller CAPE filter. Our excess-CAPE data sets out how the indicator is built. A positive ECY means equities offer an expected real return above Treasuries — the historically normal configuration. An ECY close to zero or negative means the expected risk premium is weak or null — a historically rare configuration associated with bubble peaks.

The metric was formalized by Shiller, Black and Jivraj in a paper published in November 2020, when Treasury yields were at historically low post-COVID levels and the CAPE was rising rapidly after the March 2020 drop. The authors’ goal was to address a recurring critique of the pure CAPE: what can a high CAPE mean if Treasury yields are also very low, that is, if the bond alternative offers no significant opportunity cost? The ECY mechanically answers this by integrating opportunity cost into the measure.

2. ECY History 1881-2025

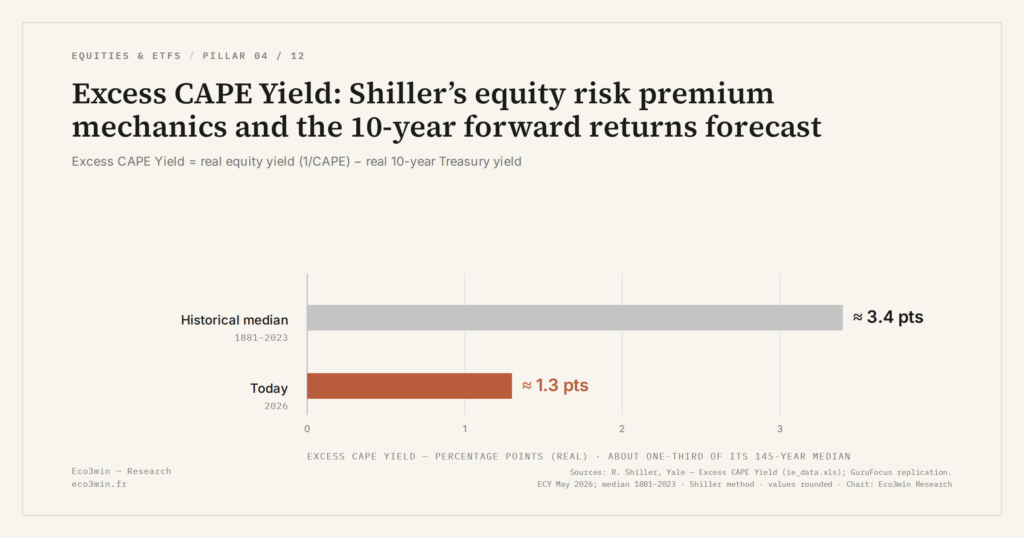

Across 145 years of data, the U.S. ECY has oscillated within a broad range but with a clearly centered distribution. The 1881-2025 median sits around 3.4% per Shiller-data calculations, which can be interpreted as the “normal” expected long-term equity risk premium in U.S. markets. This median value is consistent with academic estimates of realized equity risk premium over long periods, which run around 3-5% across methodologies. Related question: how the equity risk premium is measured.

Extreme low zones (ECY below 1%) have been visited only a few times in the series. The late 1920s before the 1929 crash saw ECY fall to around 0.5-1% over 1928-1929, a configuration combining a high CAPE (32.56 at peak) and moderate but positive real Treasury yields. The late 1990s before the dot-com burst saw ECY briefly drop into negative territory in 1999, a unique configuration in the series where the implicit real return on equities became inferior to the real return on Treasuries — an anomaly that directly preceded the 2000-2009 lost decade.

The 2021 peak — CAPE 38-40 — coexisted with a strongly negative real DGS10 (around −0.8% in early 2021 per FRED), which paradoxically kept the ECY around 3-3.5%, close to the historical median. This configuration distinguishes the 2021 peak from the 1929 and 1999 peaks: the extreme equity valuation was partially justified by the post-COVID real rate compression. At that point, reading the CAPE alone produced an extreme signal; reading the ECY produced a near-normal signal — a divergence that is precisely the diagnostic contribution of the metric. On the same theme: valuation seen through real rates and profits.

The current configuration — CAPE 35-40, positive real DGS10 around 2%, ECY 0.5-0.8% — brings the ECY back to the historically low zone for the first time since 1999. This configuration combines extreme equity valuation and positive real rates, unlike 2021 where real rates were negative. Statistically, it resembles 1929 and 1999 more than 2021 — an observation that structures part of the current debate on the 2024-2026 valuation regime developed in the satellite on the current CAPE level.

3. Documented Predictive Power

The fundamental analytical property of the ECY is its documented predictive power on 10-year forward equity returns. Per Shiller, Black and Jivraj 2020 regressions, the correlation between ECY at time t and forward 10-year real S&P 500 return reaches +0.55 over 1881-2020 — a positive coefficient (a high ECY predicts high forward return) that complements the negative correlation of the pure CAPE (−0.55 to −0.65 depending on the period). A related question: how Shiller CAPE differs from forward P/E.

This predictive power is slightly lower in absolute value than the pure CAPE’s, but the ECY offers a qualitative advantage: robustness to rate regimes. The pure CAPE predicts less well when Treasury yields diverge sharply from their historical average — for example in 2021 when real rates were negative, the CAPE alone would have projected very low forward 10-year returns while the risk premium cushion remained normal. The ECY, by integrating this variable, produces a more stable projection across rate regimes. In the same vein: the CAPE calculation, from real earnings to the Shiller ratio.

Mechanically, the Shiller-Black-Jivraj 2020 regression takes a similar form to the pure CAPE regression but with ECY as the explanatory variable and a positive sign: Real Return 10Y ≈ constant + coefficient × ECY. At ECY 0.76% as observed in May 2026, the forward 10-year projection lands around 3-4% real annual — convergent with the pure CAPE projection at 35-40, validating the coherence of both measures in this specific configuration.

The predictive power is not a timing power. The ECY can remain in the low zone for several years — it did between 1996 and 2000 — without signaling immediate reversal. It is precisely this persistence that distinguishes the ECY from a tactical indicator: it informs about mean expected returns over ten years, not about one-year turns. The same methodological discipline as for the pure CAPE applies to its ECY cousin.

4. Limits and Distinctions with the Fed Model

The ECY carries several limits that must be named explicitly to avoid over-interpretation. First limit: its sensitivity to the choice of real DGS10 measure. The standard method uses the nominal DGS10 minus T10YIE breakeven, but an alternative method uses the 10-year TIPS (Treasury Inflation-Protected Securities) yield directly. The two measures produce close but not identical values — the mean gap runs around 0.1-0.3 points across periods, which can be significant at the margin for interpreting an ECY around 1%.

Second limit: the ECY inherits the underlying CAPE biases — limited reactivity to structural shifts, sensitivity to the 2001 FASB 142 break. If the CAPE is mechanically inflated by 2-4 points per the Siegel critique, the ECY is mechanically depressed by the inverse — roughly 0.2-0.3% lower. The methodological critique of the CAPE and its derivatives covers these inherited biases.

Third limit: the ECY is conceptually close but mechanically distinct from the Fed model — a valuation tool popular in the 1990s-2000s that compares trailing earnings yield (1/trailing P/E) to nominal 10-year Treasury yield. The Fed model uses current earnings and nominal rates; the ECY uses normalized CAPE earnings and real rates. This difference is not cosmetic: the Fed model is sensitive to cyclical earnings distortions and nominal inflation, while the ECY is smoothed by real decadal earnings. Over long periods, the two measures can give opposite signals — the ECY is analytically more rigorous but the Fed model has a longer practitioner usage history. The debate on the empirical relationship between real rates and CAPE documents the complete empirical audit of this articulation.

Fourth limit: as with any expected risk premium measure, the ECY is not directly observable — it is an analytical construction based on explicit methodological assumptions. No “real” measurable ECY exists in the market: what is measurable is the ex-post ECY (computed after the fact on realized returns), not the ex-ante ECY (which anticipates those returns). This distinction is conceptually important and limits ECY use to an analytical framing instrument rather than a deterministic predictive indicator.

- The ECY is built in two steps: CAPE inversion to obtain the CAPE-based earnings yield, then subtraction of the 10-year Treasury real yield (nominal DGS10 minus T10YIE breakeven inflation).

- The historical ECY median over 1881-2025 sits around 3.4%; low zones below 1% have been visited only in the late 1920s, late 1990s and since 2024 — configurations historically associated with extreme valuation regimes.

- The ECY predictive power on 10-year forward returns reaches +0.55 per Shiller-Black-Jivraj 2020 — slightly lower than the pure CAPE in absolute value but more robust to atypical rate regimes (the 2021 case with negative real rates).

- The ECY is conceptually distinct from the Fed model despite apparent proximity: the Fed model uses current earnings and nominal rates, the ECY uses CAPE-normalized earnings and real rates — the two can produce opposite signals.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Reading Earnings Surprises: Cash Flow, Margins, Guidance

How to analyze an earnings surprise beyond the simple beat or miss: cash flow, margins, guidance, and weak…

Equal-Weight ETFs: The Quiet Signal Behind Rising Indices

Equal-weight ETFs reveal the true health of the equity market behind mega-cap-driven indices. Their gap with cap-weighted ETFs…

Smart Beta ETFs: The Hidden Risk Behind Factor Performance

Smart beta ETFs now hold ~15-20% of global equity ETF assets. Stacking factor exposures often rebuilds hidden concentration…