The limits of the CAPE: why Siegel criticises Shiller, the role of buybacks and the FASB 142 accounting break

The CAPE has never enjoyed full academic consensus. The most structured critique comes from Jeremy Siegel who, in his 2016 paper “The Shiller CAPE Ratio: A New Look,” identifies three major methodological biases: the 2001 FASB 142 accounting break, the rise of buybacks as a shareholder-return channel, and the S&P 500’s sectoral shift toward services and tech.

TL;DR

Three methodological biases Jeremy Siegel flagged in 2016 (FASB 142, the buyback shift, the S&P 500's sectoral tilt) would together reclassify today's CAPE 35-40 from extreme to merely elevated.

- From July 2001, goodwill stopped being amortized over forty years and is now impaired in one GAAP charge, a shift Siegel estimates lifts the CAPE by 2-4 points across 2001-2025.

- Buybacks rose from roughly 15% of shareholder distributions in the early 1980s to over 60% in the 2010s after SEC Rule 10b-18; Vanguard and AQR put the distortion at 1-2 multiple points.

- Cumulating the three corrections recasts the CAPE 35-40 as an adjusted 25-30 against a raised median of 22-25; Shiller calls it double-counting, with verification due from 2026-2036 returns.

Articulating these critiques without concluding them is the intellectual discipline exercise that distinguishes a rigorous reading of the CAPE from an uncritical adoption of the ratio as a universal framework.

1. The 2001 FASB 142 Break

Siegel’s first critique targets a structural accounting break that occurred in July 2001: the adoption of FASB Statement 142 by the Financial Accounting Standards Board. Before that date, the goodwill (acquisition premium) of U.S. listed companies was amortized over a maximum of forty years, spreading its accounting impact across very long periods without abrupt shocks. From July 2001, goodwill ceases to be amortized and is subject to annual impairment tests — any depreciation is immediately and fully booked as a GAAP earnings charge.

The practical effect on S&P 500 earnings has been significant and asymmetric. In expansion phases, post-2001 GAAP earnings are no longer reduced by goodwill amortizations smoothed over forty years — slight mechanical rise. In recession phases, conversely, massive goodwill impairments are booked abruptly, which strongly depresses consolidated S&P 500 earnings in the year they occur. The net long-term effect is asymmetrically negative: post-2001 earnings peaks are marginally higher, but post-2001 earnings troughs are markedly lower than they would have been under the previous regime.

For the CAPE, which uses GAAP earnings in the denominator of the decadal mean, this asymmetry produces a structural upward bias of the ratio post-2001. Siegel estimates this effect at 2-4 CAPE points on average over 2001-2025 — roughly 10% of the current level. If this estimate is correct, the FASB 142-corrected CAPE in May 2026 would not be around 36 but around 33-34. Still in the historical extreme zone but markedly less extreme than the raw value. The historical CAPE series since 1881 does not methodologically distinguish pre- and post-break, which is precisely what Siegel reproaches the measure for.

Shiller responded to this critique without fully conceding in several post-2016 publications. His main argument: the FASB 142 effect is real but marginal, and the empirical predictive property of the CAPE over 1881-2025 remains statistically robust including over the post-2001 sub-period. Shiller regressions over 2001-2015 vs 1881-2000 produce similar coefficients, suggesting the accounting break has not significantly modified the ratio’s predictive power. This debate is not academically closed and occupies a central place in the critical revisit of the CAPE as academic reference measure.

2. The Rise of Buybacks

Siegel’s second critique targets a structural transformation of the shareholder-return mode over the past forty years. In the early 1980s, share buybacks represented about 15% of total shareholder distributions of U.S. listed companies per S&P Dow Jones Indices data, the remaining 85% being dividends. This split progressively reversed: in the 2010s, buybacks crossed 50% and then 60% of total distributions, surpassing dividends as the dominant shareholder-return channel.

The institutional rupture that enabled this shift is SEC Rule 10b-18 adopted in 1982, which clarified the legal conditions under which companies can repurchase their own shares without exposure to market manipulation charges. This regulatory clarification opened the path for massive buyback use as a capital management tool, structurally modifying the S&P 500’s shareholder-return profile.

Siegel’s argument: buybacks mechanically reduce the number of outstanding shares and therefore raise earnings per share (EPS) without changing total consolidated earnings. The CAPE, computed on total S&P 500 earnings divided by the decadal mean, does not directly capture this EPS effect. If a growing share of value returned to shareholders flows through buybacks rather than dividends, then the CAPE structurally understates total equity return and therefore overstates relative valuation. A complementary angle appears in the U.S. equity market seen through the monetary-metal lens.

This critique is technically valid but its quantitative magnitude is debated. Some analyses, including work from Vanguard and AQR Research, estimate the buyback effect on CAPE interpretation at 1-2 multiple points on average over 2010-2025 — meaningful but marginal. Other analyses, including Siegel’s, estimate it higher. The comparison with alternative valuation measures addresses this point in the context of each ratio’s documented biases.

3. The S&P 500 Sectoral Shift

Siegel’s third critique concerns the progressive sectoral transformation of the S&P 500 since the 1980s. At that date, the index was dominated by traditional industrial sectors (manufacturing, energy, materials), financial services, and diversified conglomerates — sectors characterized by high capital intensity, modest margins and pronounced cyclical volatility. By the early 2020s, sectoral composition had shifted: technology, communication services, healthcare and asset-light financial services now dominate, while traditional sectors saw their relative weight fall sharply.

This shift carries structural implications for return on invested capital. Services and technology have structurally lower capital intensity than heavy industry — a dollar of invested capital on average produces more earnings in a software publisher than in a steel mill. Over the long run, these differences translate into higher and more stable ROE (Return on Equity). If sectoral composition shifts durably toward high-ROE sectors, then the average profitability of the S&P 500 should structurally rise — and the justified relative valuation (the “normal” P/E) should mechanically increase.

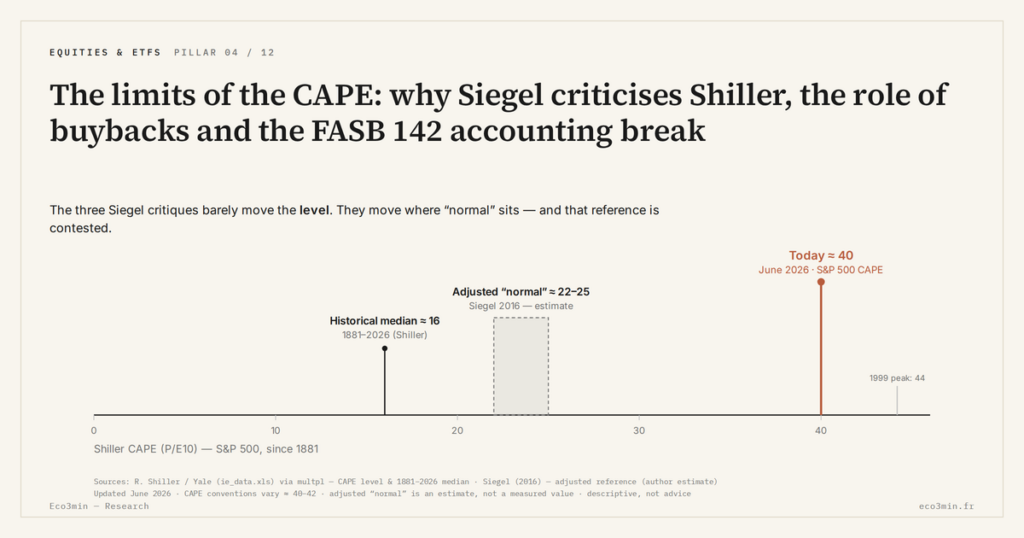

Siegel’s argument: if the “normal” fundamentally-justified P/E is structurally higher in 2025 than it was in the 1970s-1980s, then the historical CAPE median around 16-17 is no longer the relevant reference for evaluating the present. The “normal” zone threshold should be raised to 22-25 per Siegel’s estimates, which would make the current CAPE 35-40 elevated but far less extreme by reference to an adjusted comparison threshold.

Shiller has not conceded this critique but acknowledged it as analytically valid in principle. His response argument: if the sectoral shift effectively justifies a permanent rehaussement of the normal P/E, this must validate empirically on observed forward 10-year returns. The Shiller regression will continue to apply; simply, if Siegel is right, the forward 10-year returns should prove higher than the regression projects in reference to the unadjusted historical median. By mid-2026, this empirical verification is not yet available — it will require the observation of 2026-2036 returns.

4. What the Siegel-Shiller Debate Does Not Resolve

The Siegel-Shiller debate is not settled as of mid-2026 and it is instructive to note what it does not resolve, rather than seeking to arbitrate between the two positions. First unresolved point: the cumulative quantitative magnitude of the three biases identified by Siegel — FASB 142 (2-4 points), buybacks (1-2 points), sectoral shift (median readjustment from 16-17 to 22-25). Cumulating these three corrections, the current CAPE 35-40 would become approximately equivalent to an “adjusted” CAPE 25-30 against an “adjusted” historical median of 22-25 — that is, in the elevated zone but not extreme. This cumulative estimate has nevertheless been contested by Shiller as methodological double-counting.

Second unresolved point: the validity of the Shiller regression post-2001. If the three biases accumulate and effectively distort the measure, the empirical regression on pre-2001 data should no longer apply mechanically to post-2001 data. Yet empirically, regressions on the 2001-2015 sub-period produce coefficients similar to those on 1881-2000. This empirical stability of coefficients is interpretable in two opposite ways: either the biases are marginal and the regression remains valid (Shiller reading), or the biases are self-compensating and the regression masks an underlying break (Siegel-critical reading).

Third unresolved point: the practical use of the CAPE for the end investor. If the Siegel critique is accepted in its strong version, then the current CAPE 35-40 is not extreme but merely elevated, and the Shiller forward 10-year projection of 3-4% real would probably be revised upward. If the Siegel critique is rejected, then the 3-4% real projection remains the relevant analytical observation. The reading of the CAPE 35-40 level in 2024-2026 integrates this indeterminacy as contextual data rather than as a parameter to arbitrate.

For an investor readership, the operational lesson of the Siegel-Shiller debate is that no equity valuation measure, however rigorous, is exempt from permanent methodological audit. The CAPE remains the academic reference measure because its predictive property is documented over 145 years and its limits are themselves documented by its critics — precisely what distinguishes a rigorous analytical framework from an opaque indicator. Background: our reading of multiples and earnings dynamics.

- Three structured critiques from Jeremy Siegel (2016 paper) target the July 2001 FASB 142 accounting break on goodwill, the rise of buybacks from 15% to over 60% of total payout since the 1980s, and the S&P 500’s sectoral shift toward services and tech with structurally higher ROEs.

- Cumulative effect estimated by Siegel: CAPE corrected roughly 2-4 points below the raw value (FASB 142), historical reference median raised from 16-17 to 22-25 — recasting the current CAPE 35-40 as elevated but not extreme.

- Shiller responded without conceding the essentials: the empirical predictive property over 1881-2025 remains statistically robust including post-2001, and sub-period regressions produce similar coefficients.

- The debate is not settled by mid-2026; empirical verification will come mechanically through realized 2026-2036 returns — either the Shiller regression validates (measure reinforced), or Siegel validates (framework revision).

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Reading Earnings Surprises: Cash Flow, Margins, Guidance

How to analyze an earnings surprise beyond the simple beat or miss: cash flow, margins, guidance, and weak…

Equal-Weight ETFs: The Quiet Signal Behind Rising Indices

Equal-weight ETFs reveal the true health of the equity market behind mega-cap-driven indices. Their gap with cap-weighted ETFs…

Smart Beta ETFs: The Hidden Risk Behind Factor Performance

Smart beta ETFs now hold ~15-20% of global equity ETF assets. Stacking factor exposures often rebuilds hidden concentration…