Shiller CAPE ratio: why the cyclically adjusted P/E remains the academic reference for long-term equity valuation

An academic valuation ratio formalized by Robert Shiller in 1988 and popularized by Irrational Exuberance in 2000, the CAPE — S&P 500 price-to-earnings divided by the 10-year average of real earnings — concentrates since 1881 the most robust documented predictive power for 10-year forward U.S. equity returns.

TL;DR

With the S&P 500 CAPE stuck at 35-40 since mid-2024, two readings compete: AI capex justifying the multiple, or an Excess CAPE Yield near 0.5-0.8% flagging a thin risk premium.

- Historical CAPE peaks led corrections by lags ranging from zero months in 2007 to roughly eight years; the ratio held above 30 for three years before the 1999 top and has done so for four years since 2021, which is why its signal is decadal rather than a reversal trigger.

- The current ECY of 0.5-0.8% pairs extreme valuation with positive real rates, a mix closer to 1929 and 1999 (real DGS10 near 4% in 1999) than to the 2021 peak, when a negative real DGS10 around -0.8% kept ECY near its 3-3.5% historical median.

- Two readings frame the four-year cluster: a sell-side thesis tying the multiple to hyperscaler AI capex (Microsoft, Alphabet, Amazon, Meta) likened to 1880s railroads and 1920s electrification, against AQR and Vanguard work treating the thin ECY as a structural warning.

The current phase — CAPE oscillating at 35-40, the third extreme cluster in 145 years after 1929 and 1999 — tests this analytical reading framework without forcing a conclusion.

1. What the CAPE Measures — the Shiller Methodology

Technically, the CAPE — acronym for Cyclically Adjusted Price-Earnings — is the ratio of the real S&P 500 price at time t to the arithmetic mean of the index’s real earnings over the previous ten years. Both terms — price and earnings — are deflated by the U.S. consumer price index (CPI), which makes levels comparable across the entire historical series. Robert Shiller formalized this construction in a 1988 academic paper co-authored with John Campbell, then popularized it for a broader audience in Irrational Exuberance, published in March 2000 a few months before the Nasdaq collapse. The ratio was indirectly recognized through the Nobel Prize in Economics awarded to Shiller in 2013.

The central methodological choice is the ten-year average. Why ten years rather than five or twenty? Shiller’s argument is cyclical: ten years approximately cover a complete business cycle, smoothing transitory recession distortions (which depress earnings without signaling a loss of intrinsic value) and overheating phases (which inflate them artificially). A shorter average would remain cycle-sensitive; a longer one would dilute information across an increasingly heterogeneous sample. Ten years capture the empirical rhythm of U.S. cycles since 1881 without overshooting it, and that cyclical invariance property is what distinguishes the CAPE from higher-frequency valuation measures. The detailed CAPE calculation methodology makes each design choice explicit.

The second methodological choice is inflation adjustment. Comparing CAPE levels between 1929 and 2026 would be meaningless if nominal earnings were compared directly — 97 years of cumulative inflation mechanically transforms multiples. Eco3min charts this dynamic in equity valuation against real rates and earnings. Double CPI deflation — on the price numerator, on the earnings denominator — ensures the ratio measures valuation in homogeneous real terms. This statistical discipline is what Shiller conceptually inherited from Benjamin Graham and David Dodd, whose Security Analysis published in 1934 already advocated averaging earnings over seven to ten years to neutralize the cycle.

The third choice is the S&P 500. The index is broad (500 largest U.S. capitalizations), covers roughly 80% of U.S. market cap, and benefits from a series back-calculated to 1881 thanks to Shiller’s own work reconstructing the history prior to the index’s formal creation in 1957. This 145-year historical continuity is unique: no other equity valuation series offers comparable depth, which makes the CAPE the only ratio whose regimes can be studied statistically across multiple long cycles. For a synthetic introduction to the concept before the analytical deep-dive, the entry-level note what the CAPE ratio is and how it is used gives the condensed version.

2. From Graham and Dodd to Shiller — the Academic Lineage

The CAPE is not an ex nihilo innovation by Shiller but the culmination of an academic lineage whose origin lies in Security Analysis, published by Benjamin Graham and David Dodd in 1934 in the immediate wake of the Great Depression. Graham, later a reference for Warren Buffett, observed even then that valuation multiples calculated on a single year of earnings — the dominant method among Wall Street analysts — produced massive distortions at cyclical troughs and peaks. His proposal: smooth earnings over seven to ten years to neutralize atypical phases and obtain a measure of structural earning power.

This idea remained dormant for five decades in practitioner financial literature, marginalized by the rise of the forward-earnings paradigm — sell-side 12-month projections — that dominated Wall Street practice in the 1970s and 1980s. Robert Shiller, then a Yale professor, revived it within a formal statistical framework in 1988 through his article co-authored with John Campbell, “Stock Prices, Earnings, and Expected Dividends,” published in the Journal of Finance. The Campbell-Shiller contribution went beyond the Graham-Dodd intuition: it empirically established that long-term equity price variation was primarily explained by expected-return variation, not by revisions to future dividends — placing valuation at the heart of market pricing.

Irrational Exuberance, published in March 2000, transformed the CAPE from academic instrument into public reference. The title itself echoed a phrase Alan Greenspan had used in December 1996 in an American Enterprise Institute speech, where the Federal Reserve chairman wondered whether equity markets were experiencing “irrational exuberance.” Shiller’s book, released precisely as the CAPE reached its absolute historical peak at 44.19 in December 1999 per Shiller Online Data, served as immediate prospective validation: the Nasdaq Composite lost 78% of its value between March 2000 and October 2002 per FRED data. This temporal validation anchored the CAPE as the academic reference for long-term equity valuation — a status that has not been frontally contested since, even by its critics. Related discussion: what investors often get wrong about valuations and bubbles.

The Nobel Prize awarded to Shiller in 2013, shared with Eugene Fama and Lars Peter Hansen, explicitly cited his work on the predictability of long-term equity returns — that is, the foundational property of the CAPE. This institutional recognition closed a theoretical controversy: Fama’s efficient-markets reading excluded return predictability; Shiller’s reading, grounded in the CAPE, documented it empirically. The Nobel committee did not arbitrate between the two theses — it praised them as complementary across different horizons, short-term for Fama, long-term for Shiller. This academic legitimation durably anchors the CAPE in the analytical corpus of equity markets, ETFs, valuations and cycles alongside short-term pricing frameworks whose reading it complements on the decadal horizon.

3. Decadal Predictive Power — Dismantling the Timing Reading

The CAPE’s foundational property reduces to a regression. Over 1881-2025, computing the correlation between the CAPE level at time t and the S&P 500 real total return over the following ten years (dividends reinvested, deflated by CPI) produces a coefficient in the −0.55 to −0.65 range depending on the temporal window, per Shiller Online Data and published calculations. No other single-factor valuation ratio — trailing 12-month P/E, consensus forward P/E, dividend yield, price-to-book — matches that predictive robustness over the decadal horizon. A companion question: cyclically adjusted versus forward valuation.

The reference regression, published by Shiller in several updated versions of his work, takes a simple form: Real Return 10Y ≈ 9.04% − 0.16 × CAPE, with a coefficient of determination R² of roughly 0.40 over 1881-2020. Mechanically, this means that at a CAPE of 35, the Shiller model points toward a mean real annual return of roughly 3.4% over the next ten years — analytical observation, not forecast. The regression explains 40% of the forward-10Y return variance, which is exceptional for a single variable in empirical finance, but it leaves 60% of variance unexplained. It is precisely this 60% residual that makes any timing reading of the CAPE systematically misleading.

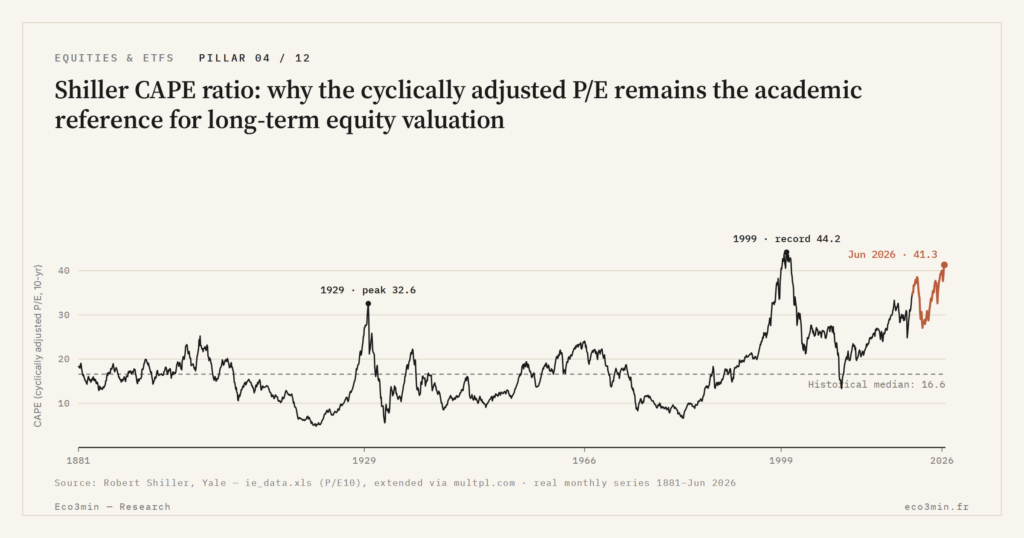

The timing reading — selling when the CAPE crosses a threshold, buying back when it falls below another — conflates two statistically distinct properties. The CAPE predicts with strong correlation the decadal averages of returns, but with weak correlation short-term turns. Empirically, historical CAPE peaks have preceded marked corrections, but with temporal lags ranging from zero months (2007, when the CAPE peak coincided with the S&P 500 peak) to roughly eight years in certain intermediate configurations. The 1929 peak at 32.56 was followed by the Black Tuesday crash within less than a year; the 1999 peak at 44.19 preceded the Nasdaq collapse by about three months; the 2021 peak around 38-40 was followed by a 25% S&P 500 correction in 2022 per FRED data, then a complete re-pricing. On this point: the evidence on record-level entries.

This temporal variability of lags — zero to eight years across configurations — is what separates a valuation-regime thermometer from a market-timing instrument. The CAPE can remain in the extreme zone for several years without correcting, as it did between 1996 and 1999 (CAPE > 30 for three years before the peak) and as it has since 2021. This persistence does not invalidate the 10-year predictive property — it simply invalidates its use as an immediate reversal signal. The distinction between CAPE, forward P/E and trailing P/E structures precisely what to expect from each measurement horizon.

4. The Four Historical Valuation Regimes

Across 145 years of Shiller data, the U.S. CAPE has oscillated within four empirically distinguishable regimes whose cartography is not a theoretical convention but a statistical reading of the historical distribution. First regime, “deep value”: CAPE below 10, observed briefly after major shocks — Great Depression trough at 5.57 in June 1932, post-WWII trough around 9 in 1949, Volcker-stagflation trough at 6.64 in August 1982 per Shiller Online Data. This regime, statistically rare, has coincided historically with the initial phases of secular bull markets: the 1932-1937 market, the 1949-1968 market, the 1982-2000 market. Further on this: our primer on stagflation.

Second regime, “normal” valuation: CAPE between 13 and 20, the dominant zone of the U.S. historical distribution. The 1881-2025 CAPE median sits around 16-17 per calculations, and the 13-20 zone has covered the bulk of 20th-century moderate-expansion phases — between WWI and the late 1920s, the 1950s, the 1980s-1990s before the dot-com acceleration. This regime conceptually corresponds to a forward real annual return of roughly 6-8% per the Shiller regression — the historically standard long-term return zone for U.S. equities.

Third regime, “elevated” valuation: CAPE between 20 and 30, observed notably in the mid-1960s during the Nifty Fifty episode (peak at 24.1 in January 1966 per Shiller), and durably through the 2010s post-GFC where the CAPE oscillated between 22 and 30 for nearly a decade. This regime is not extreme in the historical sense — valuation is high but sustainable — and it has been associated with positive but below-average 10-year forward returns (~4-6% real per the regression).

Fourth regime, “extreme” valuation: CAPE above 30, observed only three times in 145 years. September 1929 (peak at 32.56), December 1999 (peak at 44.19, absolute record), and the post-2021 sequence that maintains the CAPE between 30 and 40 over four years. Statistically, this zone represents less than 5% of the time covered by the historical series. The first two passages through the extreme regime preceded decades of weak or negative real returns: 1929-1939 with a real S&P 500 return of roughly −0.5% annual per Shiller-data calculations, 2000-2009 with a real return of roughly −2.7% annual. The detailed CAPE history of peaks and troughs since 1881 documents each of these inflection points, and the reading framework for equity market valuation, real rates, multiples and earnings situates these regimes within the general analytical frame of equity multiples. The reference series is published openly via the canonical S&P 500 CAPE dataset updated monthly.

5. CAPE and Real Rates — the Excess CAPE Yield Extension

A recurring critique of the CAPE read in isolation is that it ignores the opportunity cost offered by Treasuries. A complementary angle: Equity Market Valuation: Real Rates, Multiples and Earnings Dynamics. A “high” equity valuation takes a different meaning depending on whether real rates are at 5% or −1% — in the first case, bonds offer a competitive alternative; in the second, the equity risk premium can justify higher multiples. Shiller responded to this critique in 2020, in a paper co-authored with Laurence Black and Farouk Jivraj — “CAPE and the COVID-19 Pandemic Effect” — where he introduced the Excess CAPE Yield (ECY), a derived metric integrating the 10-year Treasury real yield. For more detail: the secular yardstick comparing the equity index to monetary metal.

The ECY construction is mechanical. Step 1: invert the CAPE to obtain the CAPE-based earnings yield, representing the implicit real return on equities under the Shiller measure. At CAPE 35, this earnings yield equals 1/35 = 2.86%. Step 2: subtract the 10-year Treasury real yield, itself computed as the DGS10 nominal yield minus the T10YIE breakeven inflation. In May 2026, with a nominal DGS10 near 4.2% and a T10YIE breakeven near 2.1%, the real DGS10 stands around 2.1%. The current ECY therefore equals 2.86% − 2.1% ≈ 0.76%. The full Excess CAPE Yield mechanics detail each step and the documented predictive power of the metric.

The current ECY level sits among the lowest historically. The 1881-2025 median oscillates around 3.4% per Shiller-data calculations, and the sub-1% zone has been visited only during a few documented periods: the late 1920s before the 1929 crash, the late 1990s before the dot-com bust, and the current sequence since 2021. As with the pure CAPE, the ECY is not a timing prediction but a measure of the expected risk premium. See the ECY series for the construction and sources. A low ECY signals that the expected equity payoff above Treasuries is statistically thin — analytical observation on the risk premium, not an immediate arbitrage signal.

The ECY has a diagnostic advantage over the pure CAPE: it distinguishes extreme-valuation phases with and without real-rate support. The 1999 peak — CAPE at 44.19 — coexisted with a real DGS10 around 4%, producing an ECY close to zero or even negative per estimates. The 2021 peak — CAPE 38-40 — coexisted with a negative real DGS10 (around −0.8% in early 2021), which maintained an ECY around 3-3.5%, paradoxically close to the historical median. The current level — CAPE 35-40, ECY 0.5-0.8% — combines extreme valuation and positive real rates, a configuration that resembles 1929 and 1999 more than 2021. The empirical real-rates-vs-CAPE relationship documented through historical audit illuminates this comparison.

6. The 2024-2026 Phase — Third Extreme Cluster

By mid-2026, the S&P 500 CAPE oscillates between 35 and 40, placing the current phase within the third durable passage through the “extreme valuation” regime in modern history. This persistence is not a one-off event: the CAPE crossed the 30 threshold in fall 2020, has never durably fallen back below since, and has oscillated in the 35-40 zone since mid-2024. Four years in the extreme zone is a duration statistically comparable to the 1996-2000 phase, which held the CAPE above 30 for three consecutive years before the December 1999 terminal peak.

Two competing theses structure the analytical reading of this phase by mid-2026. The dominant thesis, advanced by a significant share of the sell-side industry and by some academic commentary, makes Big Tech AI capex the fundamental justification for current multiples. Cumulative investments by U.S. hyperscalers — Microsoft, Alphabet, Amazon, Meta — in AI-dedicated data centers and chips have reached levels historically comparable to major transformative investment cycles (railroads in the 1880s, electrification in the 1920s, internet infrastructure in the 1990s). In this reading, the elevated CAPE would be justified by an anticipated acceleration of economic productivity and therefore future earnings.

An alternative thesis, advanced notably by AQR, Vanguard and several academic works published in 2024-2025, treats the ECY 0.5-0.8% as a structural warning. The Shiller regression applied to the current CAPE projects a forward 10-year real return of roughly 3 to 4% annual, well below the post-WWII historical average of 6-7% real. For this thesis, the fundamental justification through AI capex reproduces a pattern already observed in 1929 (justifications via electrification) and 1999 (justifications via internet) — patterns that did not prevent the subsequent decades of weak returns. The argument is not that AI capex lacks value — it manifestly has some — but that its monetization to shareholders over ten years is not mechanically guaranteed by current valuation. The detailed reading of the CAPE 35-40 level in 2024-2026 articulates both theses without privileging one.

Neither has been demonstrated by data available by mid-2026. The AI capex thesis will be validated if S&P 500 real returns over 2026-2036 significantly exceed the Shiller projection of 3-4% real — which would require unprecedented productivity acceleration and an unusual rise in the profits share of GDP. The ECY-warning thesis will be validated if the Shiller projection materializes, a scenario empirically compatible with both historical extreme-regime precedents. The verdict will come mechanically over the next ten years.

Reading the CAPE as a timing signal — selling when it crosses a threshold, buying back when it falls below another — conflates two statistically distinct properties of the ratio. The CAPE predicts decadal averages of returns with a strong correlation of −0.55 to −0.65, but short-term turns with a weak correlation. Empirically, the CAPE can remain in the extreme zone for several consecutive years before any reversal — it did between 1996 and 1999 and has since 2021. This persistence does not invalidate the decadal predictive power: it simply invalidates the timing use, which has never appeared in Shiller’s work and arises primarily in market commentary. The methodological limits of the CAPE document in parallel the other interpretive traps the measure exposes to.

7. What the CAPE Framework Enables and What It Does Not Settle

Reading the CAPE as a valuation-regime thermometer enables three useful analytical operations. First operation: position a particular cycle relative to the historical base. The four regimes — deep value, normal, elevated, extreme — provide an empirical comparative reference that clarifies what is typical and what is not. At CAPE 16, the regime reading is clear; at CAPE 35, the regime reading is also clear — but in a zone that calls for specific analysis of past configurations, not for a mechanical reading of deviations from the median. Second operation: project a distribution of plausible forward 10-year returns using the Shiller regression, explicitly acknowledging the 60% of unexplained variance. Third operation: cross-read the CAPE with real rates via the Excess CAPE Yield, to distinguish extreme regimes with and without a risk-premium cushion. Related deep-dive: The case for value or growth.

The framework does not settle three important questions. It does not say whether the timing reading — which has never been Shiller’s reading — can occasionally provide useful information in certain configurations (the “CAPE > X as tactical trigger” question is empirically tested with weak to mixed results across periods). It does not say whether the S&P 500’s changing sectoral composition — shift toward services and tech, sectors structurally more profitable on invested capital — justifies a permanent upward shift in the reference CAPE median, the central point of the Jeremy Siegel critique developed in his 2016 paper. It does not say whether the 2001 FASB 142 accounting break on goodwill treatment significantly biases the pre-post comparability in the historical series.

For an investor readership, CAPE use must reflect this perimeter. The level alone informs about regime; the forward 10-year projection informs about expected mean returns; the cross-read with the financial “U-6” (the ECY) informs about the current risk premium. None of these three pieces of information is a tactical timing signal, and none is invalidated by prolonged CAPE persistence in the extreme zone. The framework remains analytically useful precisely because it does not claim what it cannot do — predict the exact instant of the reversal — while delivering what it can — illuminate expected mean returns over the decadal horizon for which it was calibrated.

The CAPE has never been a timing signal — it is a regime thermometer, and ignoring its extreme zones three times in 145 years is statistically costly over ten years.

The current CAPE cluster — fourth consecutive year in the extreme zone — will remain a case study whatever its outcome. If S&P 500 real returns over 2026-2036 validate the Shiller projection at 3-4% real, the framework will have held a third time and the regime reading will be reinforced. If returns significantly exceed that projection, the framework will require revision — and the AI capex justification will have constituted the theoretical breaking factor that forced this revision. As of mid-2026, both scenarios coexist in academic and institutional debate without either being eliminated by available data. It is precisely this indeterminacy that justifies reading the CAPE with methodological rigor rather than routine confidence — in either direction. Reference data: the Buffett Indicator (market cap to GDP).

- The CAPE is technically the S&P 500 P/E computed on the 10-year average of real CPI-adjusted earnings — a construction inherited from Graham and Dodd (1934), formalized by Shiller and Campbell (1988), popularized by Irrational Exuberance (2000) and recognized through the 2013 Nobel.

- The ratio’s predictive power is empirically documented over 1881-2025 with a −0.55 to −0.65 correlation between CAPE at time t and forward 10-year S&P 500 real return — the reference regression Real Return 10Y ≈ 9.04% − 0.16 × CAPE explains roughly 40% of variance.

- Four empirical regimes structure the ratio’s history: deep value (below 10, post-major-shock), normal (13-20, historical median), elevated (20-30, 1960s and 2010s), extreme (above 30, observed three times in 145 years: 1929, 1999, and since 2021).

- The 2024-2026 phase — CAPE 35-40, ECY 0.5-0.8% — combines extreme valuation and positive real rates, a configuration that resembles 1929 and 1999 more than 2021; two competing theses (AI capex justifies / ECY warning) coexist without empirical resolution before the decadal horizon.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Equal-Weight ETFs: The Quiet Signal Behind Rising Indices

Equal-weight ETFs reveal the true health of the equity market behind mega-cap-driven indices. Their gap with cap-weighted ETFs…

Smart Beta ETFs: The Hidden Risk Behind Factor Performance

Smart beta ETFs now hold ~15-20% of global equity ETF assets. Stacking factor exposures often rebuilds hidden concentration…

Equity Profit Warnings: Risk and Opportunity After the Alert

Profit warnings have become accelerated stress tests in a higher-cost-of-capital regime. How equity risk reconfigures and where structural…