DTWEXBGS vs DXY: The Difference Between Broad and Narrow Dollar Indices

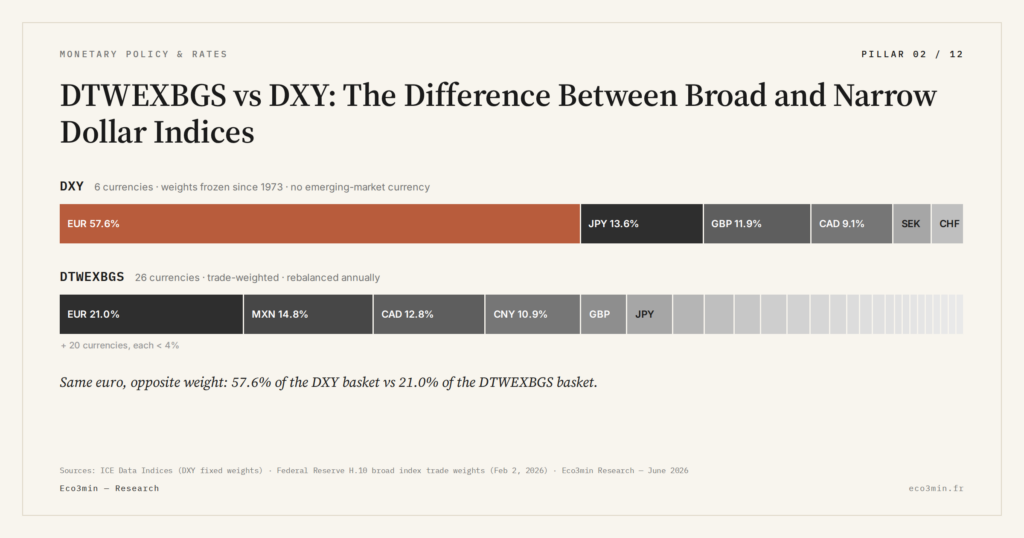

The DXY covers six developed-market currencies with weights frozen since 1973, 57.6% of which is the euro. DTWEXBGS covers 26 trade-partner currencies with annual rebalancing, including 14.8% in yuan. The two indices answer different questions.

TL;DR

In 2022 one dollar surge read as +18% on the DXY but +12% on DTWEXBGS, the gap tracing almost entirely to the DXY's 57.6% euro weight.

- The DXY's weights have not been revised since 1973: the euro sits at 57.6%, the yen 13.6%, the pound 11.9%, and no emerging-market currency appears.

- DTWEXBGS, in its current form since January 2019, weights 26 currencies by U.S. trade share and rebalances annually, with the yuan alone at 14.8%.

- Those same three currencies make up 83.1% of the DXY but only 21.8% of DTWEXBGS, so a dollar move against the yuan, peso or won barely registers on the narrow index.

- A global-macro reading built on the DXY alone risks missing 30 to 40% of the signal, the emerging-market share that carries most of the stress in tightening phases.

This piece does not arbitrate between them. It exposes the structural divergence between DXY and DTWEXBGS, and identifies the configurations in which their readings diverge analytically.

The DXY — U.S. Dollar Index, quoted by Intercontinental Exchange — is the most visible dollar instrument and the most traded on derivatives markets. DTWEXBGS — published by the Federal Reserve — is far less visible, despite broader commercial coverage. The structural distinction between the two has a direct effect on macro reading: depending on the regime, one may signal that the dollar is rising while the other signals flat. Reading DTWEXBGS as systemic strength signal — and more broadly the role of the dollar in the international monetary system — starts with putting the two indices side by side.

Two indices, two opposing logics

DXY: a basket frozen since 1973

The DXY was created in March 1973, just after Bretton Woods ended. Its basket comprises six currencies: euro (≈57.6%), Japanese yen (≈13.6%), British pound (≈11.9%), Canadian dollar (≈9.1%), Swedish krona (≈4.2%), Swiss franc (≈3.6%). The full account is given in our dollar shortage regime framework. The structural reading is developed in how the dollar index (DXY) is built. Weights have never been revised in fifty-three years. No emerging-market currency is included — no yuan, no peso, no won, no real, no rupee. The basket reflects U.S. commercial and monetary geography in 1973: a world where China stood outside the global trade system, where Mexico exported primarily oil, and where South Korea was barely beginning its industrialization.

The euro weight itself is a technical legacy. In 1973, the DXY separately weighted the Deutsche mark, the French franc, the Italian lira, the Dutch guilder, and the Belgian franc. When the euro launched in 1999, those weights were mechanically added without methodological revision. The result: a purportedly global index that allocates 57.6% to a single currency. Related discussion: how the euro-dollar rate is formed.

DTWEXBGS: a dynamic trade-weighted basket

DTWEXBGS, in its current form since January 2019, rests on three opposing methodological choices. First, the universe: 26 currencies selected because they carry the largest weight in U.S. trade in goods and services. Second, weighting: each currency receives a weight proportional to its country’s share of U.S. exports plus imports. Third, rebalancing: weights are recomputed annually to capture actual trade-flow evolution. The detailed DTWEXBGS calculation documents this mechanism and the full table of contemporary weights.

Between 2006 and 2026, the yuan weight receded by approximately 6.7 points, the peso gained approximately 2.8 points, and the euro declined by approximately 4 points. None of these moves is visible in the DXY.

The euro weight changes everything

The sum of euro (57.6%) + yen (13.6%) + pound (11.9%) reaches 83.1% of the DXY. Three developed currencies concentrate most of the signal. For the same three currencies, DTWEXBGS allocates 21.8% combined — less than a quarter. This divergence is not anecdotal: it determines what each index can reveal.

A sharp dollar appreciation against the yuan, peso, and won — typical of a U.S. monetary tightening episode — will mechanically be barely visible in the DXY if it coincides with a stable euro/dollar. Conversely, euro weakness tied to a regional shock — such as the European energy crisis of autumn 2022 — will push the DXY well beyond what truly reflects the dollar pressure on the full set of U.S. trade partners. Between January and September 2022, the DXY rose +18%, DTWEXBGS rose +12%. The 6-point gap is almost entirely attributable to the euro component. On this point: the mapping of bullion records outside the dollar zone.

The DTWEXBGS series on Eco3min provides the raw data for cross-comparing the two indices over their full common history.

Historical configurations of divergence

Divergences between DXY and DTWEXBGS are not random. They occur in three identifiable configurations documented by FRED data over the past fifty years.

First configuration: an asymmetric regional shock hits one of the major developed economies without affecting emerging markets. Euro-area sovereign debt crisis 2010-2012, Brexit 2016, European energy shock 2022. The DXY, dominated by its euro component, overreacts. DTWEXBGS remains measured because emerging markets are unaffected, or affected with different timing. Between August and October 2022, the DXY gained +6.1%, DTWEXBGS +3.4%. The 2.7-point gap captures the euro share of the shock.

Second configuration: a tariff or financial shock hits emerging markets without affecting the euro or yen. Taper tantrum May 2013, Turkish crisis August 2018, surprise yuan devaluation August 2015. DTWEXBGS rises significantly; the DXY barely moves. During the May-August 2013 taper tantrum, DTWEXBGS rose +3.7%, against +1.2% for the DXY. No serious macro reading of EM transmission could rely on the DXY alone.

Third configuration: restrictive U.S. monetary policy simultaneously tightens global financial conditions. The 2022 case. Both indices rise, but DTWEXBGS remains a better proxy for effective dollar pressure on the world economy, because it captures the emerging-market component — which carries most of the stress in those phases. A DXY rising faster than DTWEXBGS signals a euro-centered shock; the reverse signals an EM shock.

Three uses, three readings

The hierarchy between the two indices is not absolute. It depends on the question being asked.

For short-term trading and currency arbitrage, the DXY retains a structural advantage. Its derivatives liquidity is massive — ICE futures, options, ETFs. Intraday quotation has existed since 1985. DTWEXBGS, computed by the Fed at daily frequency with a publication lag, is not suited for trading use.

For global macro reading — dollar pressure on trade balances, transmission to emerging markets, monetary-policy signal — DTWEXBGS is the only coherent instrument. Its dynamic trade-weighted coverage reflects the actual dollar pressure on the world economy, where the DXY essentially measures an extended dollar/euro bilateral relationship.

For regional analysis, the Fed publishes since January 2019 two sub-indices built on the same methodology as DTWEXBGS: DTWEXAFEGS for Advanced Foreign Economies and DTWEXEMEGS for Emerging Market Economies. Reading the three indices jointly allows disaggregation of a broad move into developed and emerging components — something neither DXY nor DTWEXBGS in isolation can deliver.

Neither is universal

The best reading of the DXY/DTWEXBGS pair is to treat them as complementary instruments. The thread is followed through in this analysis of carry trade emerging currencies. The DXY is a thermometer of the dollar against a monetary history — that of the major developed currencies post-Bretton Woods. It remains relevant where that history matters: developed FX markets, immediate transmission to European assets, short-term market sentiment. DTWEXBGS is a thermometer of the dollar against an actual commercial geography — that of the United States in 2026, no longer that of 1973. Its relevance is macro, structural, and increasingly dominant as emerging economies gain weight in global trade and finance. For more detail: the dollar’s role in the monetary system.

The right question is not “which to choose” but “what is being read.” A global macro analysis relying on the DXY alone risks missing 30 to 40% of the signal — the emerging-market share — precisely when that signal matters most. A short-term trading analysis relying on DTWEXBGS alone loses intraday granularity and derivatives liquidity. The two indices were built for different uses. Confusing them amounts to using a seismograph to measure temperature.

“The dollar rose” is an incomplete statement until the reference index is specified. A DXY move may reflect a euro-specific shock without global dollar pressure. A DTWEXBGS move may reflect emerging-market stress invisible in the DXY. The question is not which index is right, but which one measures what is being read.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…