VIX vs HY OAS: the equity volatility / high-yield credit spread divergence as a 2024-2026 regime marker

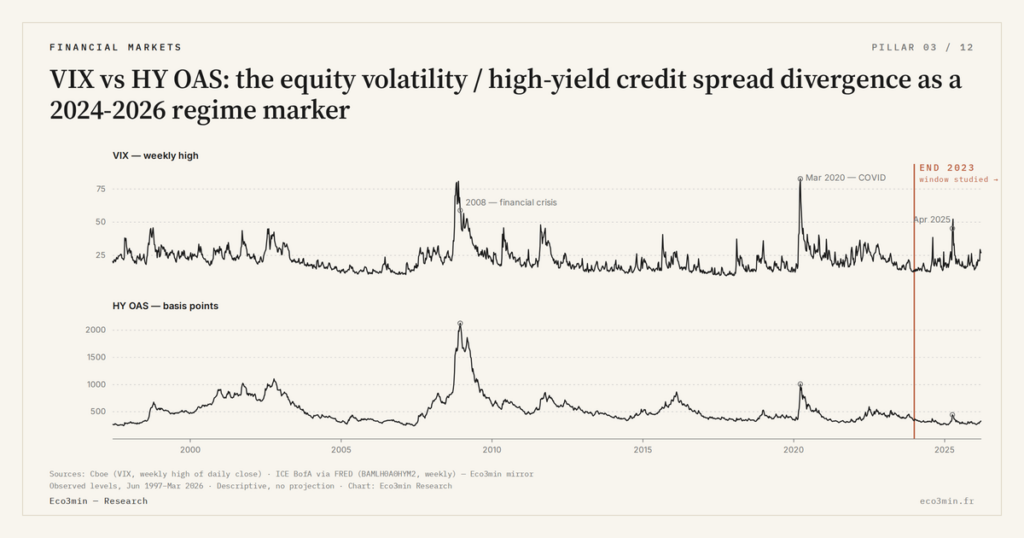

The VIX and the high-yield credit spread were correlated at 0.65-0.80 over 2000-2019, equity mirror of the same stress signal. That correlation collapsed at end-2023: both indicators are simultaneously compressed, but their historical synchronicity has vanished.

TL;DR

Correlated at 0.65-0.80 over 2000-2019, the VIX and HY OAS credit spread saw their 180-day rolling correlation collapse to 0.28 at end-2025, its lowest since 2000.

- The correlation ran through three channels (earnings, liquidity, information) and held at every shock: GFC 2008 at 2150 bps HY OAS for a VIX of 89, COVID March 2020 at 1100 bps for a VIX of 82.

- Since end-2023 both are compressed yet desynchronised: HY OAS pinned between 280 and 310 bps since December 2024, VIX between 14 and 18; in June 2025 HY energy tension at 320 bps left the VIX closing at 15.4.

- Three competing readings, none demonstrated: options-market maturation (0DTE), VIX suppression by short-volatility positions (the BIS thesis, Bulletin No. 78 of September 2025), or structural cycle desynchronisation; the HY default rate sits at 2.4% at end-2025 versus a 4.1% historical average (Moody's).

- The three comparable precedents (mid-2007, summer 2014, end-2019) all resolved through simultaneous repricing; the concurrence of low VIX, low HY OAS and negative T10Y3M over more than 24 months is unprecedented since 1990.

The decoupling observed between equity implied volatility and the credit spread has no equivalent since 2000. Three readings compete to explain it; none has been demonstrated. What follows maps the historical baseline, the post-2023 break, and comparable configurations. More context: what breaks of 30, 40 and 50 on the VIX have meant historically.

1. The 2000-2019 baseline: one stress signal, two windows

The High Yield Option-Adjusted Spread (HY OAS), published daily by ICE and accessible via the BAMLH0A0HYM2 series on FRED, measures the yield gap between US high-yield corporate bonds and the Treasuries curve. The wider the spread, the higher the premium investors demand to carry credit risk; in stress regimes, the HY OAS mechanically widens as anticipated defaults rise and segment liquidity contracts. the grid of credit segments along the cycle traces this mechanism across cycles. A broader view: the weak signals ahead of market dislocations.

Over 2000-2019, the correlation between VIX and HY OAS stands at 0.65-0.80 depending on calculation windows. See our implied-volatility record for the construction and sources. Both indicators react together to the same macro-financial events: LTCM-Russia 1998 peak (HY OAS at 1100 bps, VIX at 45), GFC 2008 (HY OAS at 2150 bps, VIX at 89), European sovereign debt crisis 2011 (HY OAS at 870 bps, VIX at 48), Volmageddon 2018 (HY OAS at 460 bps, VIX at 50), COVID March 2020 (HY OAS at 1100 bps, VIX at 82). This synchronicity has a mechanical explanation: a shock that widens credit spreads alters equity valuations, and conversely, an S&P 500 shock degrades corporate valuations and tightens credit access for HY issuers.

The link operates through three channels. The earnings channel: an equity repricing reflects a downward revision of future profits, degrading HY issuers’ debt service capacity. The liquidity channel: equity stress retracts demand for risky assets, including HY bonds. The informational channel: VIX and HY OAS are watched jointly by risk desks, and the resulting hedging flows reinforce the correlation by construction.

2. The post-2023 break: empirical description

Since end-2023, the historical pattern has broken. The HY OAS has been oscillating between 280 and 310 basis points since December 2024, a level comparable to the 2014, 2018 and 2021 troughs. The VIX trades in a 14-18 range over the same period. Both indicators are simultaneously compressed. But this joint compression no longer translates into strong correlation of daily moves: the 180-day rolling correlation has fallen to 0.28 at end-2025, an unprecedented level since 2000.

Three discrete episodes illustrate the break. In April 2025, a weak US manufacturing PMI lifted the VIX from 14 to 22 in two sessions while the HY OAS stayed at 295 bps. In September 2025, a second below-consensus NFP release pushed the VIX to 24; the HY OAS widened by only 8 basis points. Conversely, tensions in the HY energy segment in June 2025 (HY OAS at 320 bps) did not reflect at all in the VIX, which closed the session at 15.4.

This desynchronisation is not a statistical artifact. It appears on all tested calculation windows (30, 60, 90, 180 days) and across sub-periods (2024 vs 2025 vs 2026). It manifests both on daily co-movements and on level correlations. And it persists long enough to rule out an episodic explanation. The specific analysis of the 2023-2026 VIX compression regime and its historical comparables documents the equity leg of this joint desynchronisation separately.

3. Three hypotheses to explain the divergence

The first reading, the most widespread among sell-side strategy desks, attributes the break to differentiated market maturation. The SPX options market has financialised through 0DTE and structured products, compressing the VIX. The HY market, lacking comparable innovation, retains a structure closer to its 2010-2019 form. This thesis implies that correlation will re-establish if markets converge in sophistication, or if a new dislocation forces simultaneous repricing.

The second reading, advanced by the BIS in its September 2025 Bulletin No. 78, sees in the divergence a symptom of differentiated short-volatility accumulation. Autocalls, covered call ETFs and volatility carry funds would compress the VIX beyond what underlying risk justifies. The HY OAS, by contrast, would more faithfully reflect actual default risk — which is indeed low in 2024-2026 (HY trailing default rate at 2.4% at end-2025 per Moody’s, below the historical 4.1% average). Under this view, the VIX is artificially compressed while the HY OAS is correctly priced.

The third reading, more structural, attributes the divergence to a macroeconomic regime change. High nominal growth in 2023-2026 (+5% to +6% in the United States) supports HY debt service capacity independent of equity sentiment. Record large-cap US profits (S&P 500 EPS up 11% YoY in 2025) sustain equity valuations at levels consistent with a low VIX. In this framework, both indicators faithfully reflect two now-desynchronised dimensions of the cycle, and the historical correlation was an artifact of the 2000-2019 cycles.

None of the three theses has been demonstrated. The observation period (24 months) remains insufficient to settle the question, and comparable historical configurations are rare. The overall mapping of the VIX as an equity compass documents this divergence as one of the most structuring open questions of the 2024-2026 market regime.

4. Comparable historical configurations

The 2024-2026 desynchronisation is not absolutely unprecedented, but it is rare. Three episodes are worth examining.

Summer 2014: VIX between 10 and 14, HY OAS between 340 and 380 bps. The 60-day rolling correlation falls to 0.31. The episode resolves at end-2014 / early 2015 through an equivalent re-stress on both indicators linked to the oil collapse and HY energy stress. The next peak comes in January 2016.

Mid-2007: VIX between 12 and 16, HY OAS between 290 and 340 bps. The correlation loosens for six months. The resolution of this divergence is known: the August 2007 BNP Paribas money-market fund episode marks the first signal of the subprime crisis, and both indicators widen simultaneously from September 2007.

End-2019: VIX at 11-14, HY OAS at 350-400 bps. 60-day correlation at 0.38. The resolution comes in March 2020 through the COVID crash, which pushes both indicators to their simultaneous record levels.

Three precedents, three different resolutions: a sectoral repricing (HY energy 2014), a progressive systemic repricing (subprime 2007-2008), a brutal exogenous shock (COVID 2020). No mechanical extrapolation is possible from this trio, but the qualitative pattern is constant: prolonged VIX-HY OAS divergences resolve through simultaneous repricing, in one direction or the other. Related framing: the 2008 episode read by financial conditions.

One important nuance distinguishes the 2024-2026 configuration from the three precedents. In the 2007 and 2019 episodes, the yield curve gave a complementary stress signal — T10Y3M inversion in July 2007, inversion in May 2019 — that anticipated a macro deterioration. The analysis of the T10Y3M recession signal and its limits documents that dimension. The T10Y3M has been negative since October 2022 in the current cycle, yet no US recession has materialised — another indicator whose historical reading appears scrambled. The concurrence low VIX / low HY OAS / negative T10Y3M over more than 24 months is itself without precedent over 1990-2026.

5. Monitoring indicators to detect a re-convergence

Three indicators are tracked by risk desks to anticipate a possible VIX-HY OAS re-convergence. The first: the HY OAS over IG OAS ratio (investment grade corporate). A widening of this ratio signals a differentiated deterioration of the HY segment independent of equity sentiment. At end-2025, the ratio sits at 4.8x, slightly above its 4.3x historical average but without acute signal.

The second: the HY trailing 12-month default rate published by Moody’s. A break above 4% (historical average) would signal credit risk materialisation that would likely reflect in the HY OAS. The current 2.4% rate keeps the HY OAS low by fundamental, not by artificial compression.

The third: dealer positioning on VIX futures published weekly by the CFTC. A prolonged accumulation of short positions by non-commercials preceded the 2018 Volmageddon; the same signal observed in 2025-2026 feeds the BIS artificial-suppression thesis. The mapping of hidden tension indicators documents the cross-tracking of these signals as a surveillance methodology for joint-compression phases.

- VIX and HY OAS were correlated at 0.65-0.80 over 2000-2019; the 180-day rolling correlation fell to 0.28 at end-2025, a level unseen since 2000.

- Three competing readings explain the divergence: differentiated market maturation, artificial VIX suppression by short-volatility positions, or structural cycle desynchronisation.

- The three comparable historical episodes (2007, 2014, 2019) all resolved through simultaneous repricing in very different contexts — no mechanical extrapolation possible.

- The monitoring indicators tracked by risk desks are the HY OAS / IG OAS ratio, the HY trailing default rate, and CFTC positioning on VIX futures.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Euro Below Parity in 2022: What Parity Means

In September 2022, the euro fell below parity with the dollar, to around 0.95, a low not seen…

Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…