VIX contrarian thresholds and historical equity rebounds: what 30, 40 and 50 breaches preceded for the S&P 500

Since 1990, seven of the eight breaches of the 50 threshold by the VIX have been followed by an S&P 500 rebound over the twelve-month horizon. The empirical regularity is documented and stable; its operational scope remains nevertheless limited by short-term return dispersion.

TL;DR

A VIX above 50 marks acute stress but not its end: five of eight troughs since 1990 landed over a month after the breach, though 12-month rebounds followed in seven. Eco3min documents this dynamic in our analysis of the VIX as an implied-volatility gauge.

- The eight breaches above 50 run from LTCM 1998 to the 2024 yen carry unwind; COVID 2020 produced the strongest 12-month rebound (+66.4%), Volmageddon 2018 the weakest positive one (+5.1%).

- The trough arrived more than a month after the breach in five of the eight cases, so the level confirms an acute stress phase without dating its end.

- Risk desks never read the level alone: VIX above 30 paired with term-structure backwardation and a high-yield OAS beyond 600 basis points is more informative than the threshold by itself.

The expression contrarian signal is used in market literature to describe the observation that extreme VIX levels historically coincide with equity troughs. What follows maps this observation, its statistical limits, and the configurations where it proved misleading. This specific point is developed further in the Eco3min framework on systemic risk indicators.

1. The empirical observation: extreme VIX levels and 12-month returns

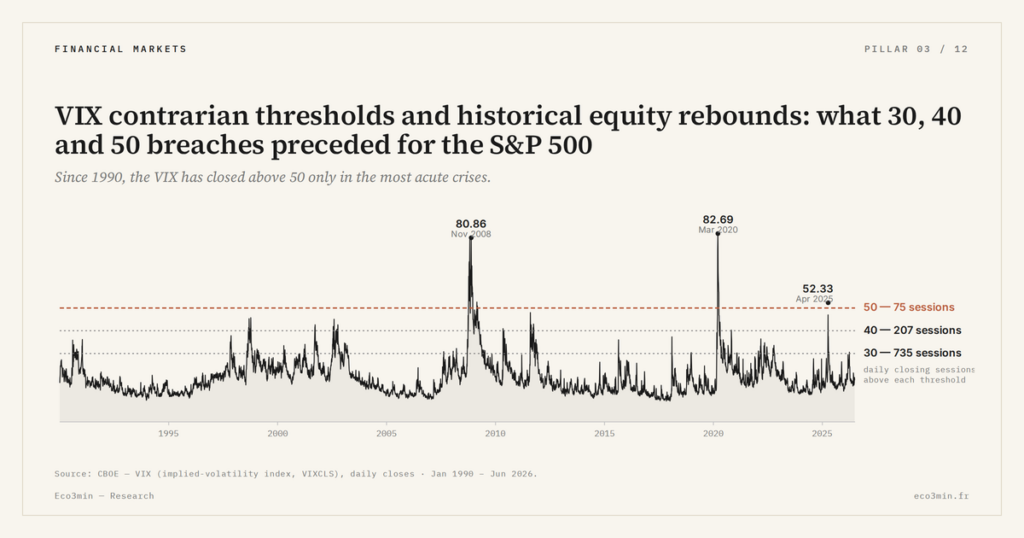

Over the 1990-2025 period, the VIX has crossed the 30 threshold twenty-four times, the 40 threshold twelve times, and the 50 threshold eight times. For each breach, the S&P 500 return over the following twelve months was calculated from the breach date. The observed distribution differs by threshold.

For the eight breaches of the 50 threshold (LTCM-Russia 1998, GFC 2008, Flash Crash 2010, eurozone 2011, Volmageddon 2018, COVID 2020 on multiple occasions, yen carry trade unwind 2024): seven were followed by a positive 12-month S&P 500 return (median +22.1%), only one saw a negative 12-month return — the October 2008 breach during the GFC, where the S&P 500 continued falling until March 2009 before rebounding.

For the twelve breaches of the 40 threshold: ten were followed by a positive 12-month return (median +18.4%), two saw a negative return (both linked to the GFC, September and October 2008). For the twenty-four breaches of the 30 threshold: eighteen saw a positive 12-month return (median +14.7%), six negative (concentrated in the 2000-2002 and 2008 phases).

The qualitative pattern is consistent: the higher the reference threshold, the higher the probability of a positive 12-month return. This regularity is descriptive, not prescriptive. None of the eight breaches of the 50 threshold occurred in the same macroeconomic context, and the sample (eight cases over 35 years) remains statistically limited.

2. Detail of the eight breaches of the 50 threshold

LTCM-Russia, September-October 1998: VIX peak at 45.7 on 8 October. 12-month S&P 500 return: +21.3%. Cross-asset stress configuration followed by coordinated Fed intervention.

GFC, September 2008 (first breach): VIX at 41.4 on 17 September. 12-month return: -10.8%. The S&P 500 continued falling to the 9 March 2009 trough; the subsequent rebound only brought the index 8% above the September 2008 level around March 2010. Atypical case.

GFC, October-November 2008 (second breach): VIX at 89.53 intraday on 24 October, 80.86 on close on 20 November. 12-month return from 24 October: +20.7%. The later peak coincided with a better entry point than the initial September breach.

Flash Crash, May 2010: VIX at 45.8 intraday on 6 May. 12-month return: +18.4%. Technical shock without severely degraded macro context; quick resolution after market-maker stabilisation.

European sovereign debt crisis, August-October 2011: VIX at 48.0 on 8 August. 12-month return: +25.4%. European geopolitical stress, final resolution via Draghi in mid-2012.

Volmageddon, February 2018: VIX at 50.3 intraday on 6 February. 12-month return: +5.1%. Atypical configuration: structural shock (forced unwinding of short-vol ETNs) without underlying macro deterioration; the S&P 500 spent most of the subsequent 12 months digesting the repricing.

COVID, March 2020: VIX at 82.69 on close on 16 March. 12-month return: +66.4%. Strongest post-spike rebound of the series, linked to massive and rapid Fed + Treasury intervention.

Yen carry trade unwind, August 2024: VIX at 65.73 intraday on 5 August. 12-month return calculated to end-April 2026 (8 months elapsed): +14.2% annualised, equivalent to a 12-month projection near +18%. Cross-asset configuration (FX/futures) without deep equity repricing.

The empirical detail of each case, including 1, 3 and 6-month post-breach returns, is available in the full table of individual cases with detailed returns.

3. Why short-term dispersion limits operational scope

The regularity observed at 12 months does not extend to shorter horizons. The dispersion of 1-month and 3-month post-breach returns remains elevated, and the median only becomes positive from the 6-month horizon onward.

For the eight breaches of the 50 threshold: at 1 month post-peak, six out of eight cases saw a negative return (median -3.8%); at 3 months, five out of eight (median +1.2%); at 6 months, two out of eight (median +12.4%); at 12 months, one out of eight (median +22.1%). The median sign inversion occurs primarily between 3 and 6 months.

This short-term dispersion produces two practical consequences. First: a breach of the 50 threshold provides no information about when the equity trough will be touched. In five of the eight cases, the S&P 500 trough was reached more than one month after the breach (sometimes up to six months after for the GFC). Second: materialising the 12-month positive return may require accepting a significant intermediate drawdown. In the GFC case, the maximum drawdown post-breach of the 50 threshold reached -25% before the March 2009 trough.

The 12-month pattern is therefore statistically robust but operationally constrained by intermediate dispersion. An honest reading is: extreme VIX levels have historically coincided with phases whose exit was followed by an equity rebound over 12 months, without any precise timing signal being extractable.

4. Configurations where the observation proved misleading

Three historical configurations warrant separate examination, because they produced atypical behaviours.

The GFC of September 2008 remains the most important counter-example. The initial breach of the 40 threshold in September was not followed by a quick rebound; the VIX continued rising for two months and the S&P 500 fell an additional 28% before the March 2009 trough. The crisis nature — global forced deleveraging, interbank dislocation, progressive intervention — explains this anomaly. The September 2008 breach demonstrates that an elevated VIX level provides no guarantee on repricing duration.

Volmageddon of February 2018 is another atypical case, but in the opposite direction. The breach of the 50 threshold was followed by a quick rebound (+5.1% at 12 months, but especially +13% at 6 months). The structural nature of the shock — forced unwinding of short-vol positions without underlying macro deterioration — explains this rapid resolution. But the modest 12-month return (+5.1%, below the +22.1% historical median) shows that quick resolution did not allow strong post-peak upside.

The 2007 (VIX trough at 9.89) and 2017 (trough at 9.14) configurations also documented a case no high VIX threshold illuminates: the durable compression preceding a brutal repricing. Reading VIX thresholds only on the upside (extreme highs) ignores that extreme lows (durable compressions) are themselves historically informative, but in the other direction. The compression phase observed since 2024 documents this symmetric dimension.

5. Complementary indicators used by risk desks

No institutional risk desk uses a VIX threshold alone as an operational indicator. Three complementary indicators are systematically cross-referenced.

First: the flip of the VIX term structure into backwardation. The twenty-two total backwardation episodes since 2004 have preceded twenty-one S&P 500 drawdowns above 5% within the next 30 days. The combination VIX > 30 + backwardation is statistically more informative than VIX > 30 alone. The mechanical detail of this signal is documented in the curve analysis and its regimes.

Second: the HY OAS. A simultaneous widening of the high-yield credit spread beyond 600 basis points, in addition to a VIX > 30, signals cross-asset deterioration that is generally not followed by a quick rebound. Conversely, a VIX > 30 without HY OAS widening (2018, 2024 configurations) is statistically more likely to be followed by a rebound. This dimension is central to the joint reading of the two indicators.

Third: the trigger nature. Structural cross-asset shocks (Volmageddon 2018, yen carry trade unwind 2024) resolve more quickly than systemic shocks (GFC 2008) or deep exogenous shocks (COVID 2020). This classification is qualitative, not statistical, but it is systematically used by desks to calibrate resolution expectations. The empirical catalog of the seven major spikes 1990-2026 documents this typology in the detailed historical analysis of episodes.

6. Conclusion: empirical observation, not trading rule

The statistical regularity between extreme VIX levels and 12-month S&P 500 returns is documented and stable. Its operational scope is nevertheless limited by three factors: short-term dispersion (frequent intermediate drawdown), heterogeneity of macro contexts (eight cases over 35 years, no two identical), and asymmetry of preliminary information (VIX > 50 says nothing about the residual repricing duration).

The contrarian observation — extreme VIX levels historically coincide with phases of 12-month equity rebound — is therefore a historical statistic, not a timing rule. Its value for risk desks is diagnostic: it confirms entry into an acute stress phase, without specifying when it will end. Combining this observation with the VIX term structure, HY OAS, and trigger nature is the standard methodology.

- Over 1990-2025, seven of the eight VIX breaches of the 50 threshold coincided with a positive 12-month S&P 500 return (median +22.1%); the atypical case remains the GFC of September 2008.

- The 12-month regularity does not extend to shorter horizons: medians remain negative at 1 month, marginally positive at 3 months, with structural inversion between 3 and 6 months.

- The 2008 GFC and 2018 Volmageddon illustrate the two extremes of post-spike variability: long trajectory with additional drawdown, or quick resolution without strong upside.

- No risk desk uses a VIX threshold alone; the combination VIX > 30 + term structure backwardation + HY OAS widening is statistically more informative than the isolated VIX threshold.

Last updated — 27 June 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Euro Below Parity in 2022: What Parity Means

In September 2022, the euro fell below parity with the dollar, to around 0.95, a low not seen…

Eurozone Fragmentation: Sovereign Spreads and the Euro

The euro is issued by a monetary union without a complete fiscal union: nineteen sovereign debts coexist under…

The Euro’s Energy Import Bill: the Gas Shock and the Currency

In 2022, the surge in gas prices turned the euro area's historic current-account surplus into a deficit and…