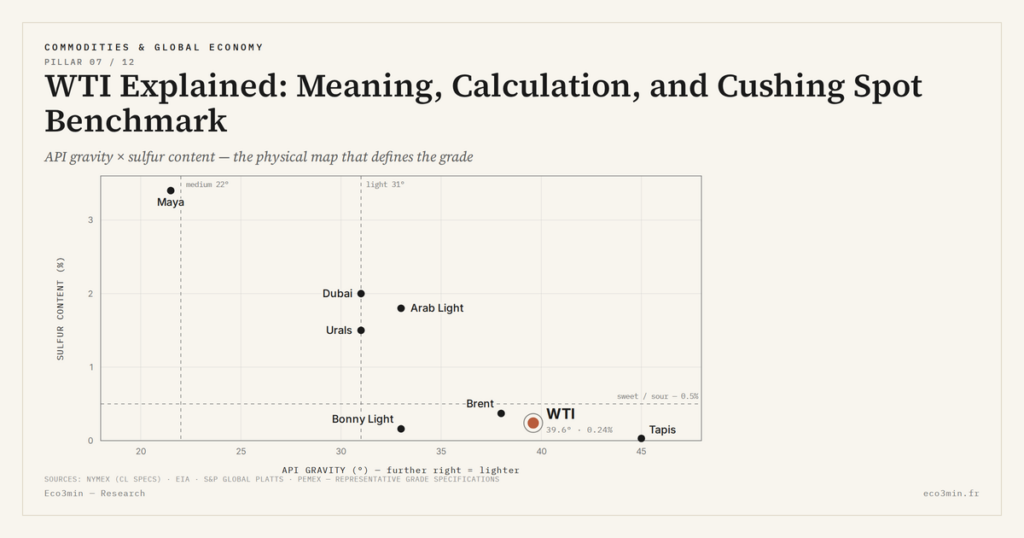

WTI Explained: Meaning, Calculation, and Cushing Spot Benchmark

WTI is a precise object: light sweet crude at 39.6 degrees API and 0.24% sulfur, priced at Cushing, Oklahoma, tracked by FRED’s DCOILWTICO series at daily frequency since 1986. These three technical coordinates condition every macroeconomic reading that follows.

TL;DR

The -$37.63 print of April 20, 2020 was a contract-mechanics artifact: with the May future expiring and Cushing storage full, long holders paid to shed physical delivery.

- Quality economics: at 39.6 degrees API and 0.24% sulfur, WTI trades at a historical $5-15 per barrel premium over medium-sour grades such as Saudi Arab Light or Mexican Maya, refinable without desulfurization units.

- Cushing: the world's largest crude storage hub (90+ million barrels, around twenty operators) and a landlocked convergence of Permian, Bakken and Canadian flows that lets WTI decouple from the global price when it saturates.

- The reference series: DCOILWTICO runs daily since January 2, 1986 (monthly back to 1946) and anchors most empirical work on oil shocks, the oil burden and inflation pass-through; its extremes include $145.29 on July 3, 2008.

This piece does not discuss the macro signal WTI sends — that belongs to the cluster’s main article. It does one thing: expose what WTI is technically, because the macro reading rests on that precision.

1. Light Sweet Crude: The Technical Definition

West Texas Intermediate is defined by two fundamental physical characteristics per NYMEX specifications (2024 revision). First, a density of 39.6 degrees API. The API scale (American Petroleum Institute) measures the density of crude relative to water: above 31° API, crudes are classified as light; between 22° and 31°, as medium; below 22°, as heavy. At 39.6° API, WTI sits firmly in the light segment, placing it close to comparable grades like Brent (38° API), Nigerian Bonny Light (33° API), or Malaysian Tapis (45° API). The lighter the crude, the more light fractions it contains directly refinable into gasoline, naphtha, and diesel — the highest-margin cuts for a refinery.

Second, a sulfur content of 0.24%. The standard classification distinguishes sweet crudes (below 0.5%) from sour crudes (above, sometimes up to 3-4% for certain Venezuelan grades). A sweet crude can be refined directly without major desulfurization investment; a sour crude requires dedicated units (hydrocrackers, Claus sulfur recovery units) that are expensive to install and operate. WTI at 0.24% is therefore clearly sweet, making it a “premium” grade for U.S. refineries that can extract the maximum high-margin refined products from it. Source data: the heating oil spot price dataset.

The light + sweet combination is not economically neutral. Per EIA refining margin data, a light sweet crude historically trades at a premium of $5 to $15 per barrel over a reference medium sour like Saudi Arab Light (33° API, 1.8% sulfur) or Mexican Maya (22° API, 3.3% sulfur). This premium reflects the additional economic value a refinery can extract without desulfurization overhead. When an analyst compares WTI prices to Maya or Urals prices, they are in reality comparing two different physical qualities that are not interchangeable barrel-for-barrel for the refiner.

This material precision has a direct consequence for the macro reading. The major oil shocks (1973, 1979, 2008, 2022) that affect the crude market weigh differently depending on available physical qualities. When Russian supply (Urals, medium sour) is sanctioned, the European market — historically a major Urals consumer — must substitute with other grades. Not all crudes are interchangeable: the Urals → WTI substitution requires refinery adjustments that are neither instantaneous nor free. This physical friction is what produces the observed price spreads between benchmarks during stress episodes.

2. The Cushing Hub: Oklahoma as Pricing Point

Physical WTI pricing happens at Cushing, a town of about 7,800 inhabitants in the state of Oklahoma. This choice is neither arbitrary nor anecdotal: per EIA data, Cushing concentrates over 90 million barrels of storage capacity in cylindrical tank farms operated by some twenty operators (Enbridge, Plains All American, Magellan Midstream, among others). This physical infrastructure makes Cushing the largest crude oil storage hub in the world, behind only the port terminals of Rotterdam and Singapore for equivalent capacities.

Cushing’s centrality is explained by its pipeline geography. The hub is a convergence point receiving flows from the Permian Basin (Texas-New Mexico, the largest U.S. shale basin), the Bakken (North Dakota), the Niobrara Basin (Wyoming-Colorado), and Canadian inflows descending via the Keystone pipeline (Alberta oil sands). On the evacuation side, Cushing supplies Mid-Continent refineries and, via the Seaway and Cushing-Houston pipelines commissioned after 2012, the refineries of the Gulf of Mexico (Texas, Louisiana). This dual function — receiving North American flows and redistributing to refineries — makes Cushing the natural fixation point for the U.S. reference price.

This physical concentration has an important consequence: WTI is a landlocked price, inseparable from the pipeline logistics that serves it. When Cushing’s evacuation capacity saturates — which occurred massively in 2011-2014 when the shale boom outpaced existing pipeline capacity — WTI can decouple from the global market. Per FRED data, the WTI-Brent differential reached -$28 in October 2011 (WTI at $86 vs Brent at $114) precisely because crude produced in the Permian and Bakken was accumulating at Cushing without being able to flow to Gulf refineries or to export. The partial lifting of the U.S. crude export ban in December 2015 (Crude Oil Export Ban Repeal of the Consolidated Appropriations Act) and the construction of new pipelines (Seaway, Diamond Pipeline, Cactus II) progressively restored circulation. For more detail: the regime signal drawn from the gold-energy pair.

For the futures contract, Cushing as a pricing point implies physical settlement. At the expiration of a NYMEX WTI contract, the long position holder must take physical delivery of crude at Cushing — either via a leased nominal tank, or by swap with a storage operator. The short position holder must deliver it. This physical mechanism is what fundamentally distinguishes WTI from Brent (cash settlement on the ICE contract) and explains price anomalies like the -$37.63 of April 20, 2020: at the expiration of the May 2020 contract, long holders without storage capacity had to pay to discharge their delivery obligation, with Cushing storage saturated by the COVID demand collapse.

3. The NYMEX Contract and the FRED DCOILWTICO Series

Official WTI pricing happens on the New York Mercantile Exchange (NYMEX) futures contract, a CME Group subsidiary since 2008. The NYMEX Light Sweet Crude Oil contract (symbol CL) is one of the most liquid in the world: per CME statistics, the 2024 average daily volume exceeds 1 million contracts traded, each corresponding to 1,000 barrels — meaning a daily notional equivalent of more than one billion barrels, infinitely greater than global physical production (about 100 million barrels per day). This financial liquidity far exceeds the contract’s physical function: the majority of transactions are position rollovers, hedging by producers and refiners, and speculative positioning by hedge funds and CTAs.

The reference price cited by the press, analysts, and official statistics is the front-month contract price — that is, the contract closest to expiration. This convention introduces an effect called “roll”: at each monthly expiration, the front-month contract switches from month M to month M+1, which can produce apparent price jumps that do not reflect a fundamental move. For long-term analyses, some databases use continuous contracts reconstructed by interpolation (Bloomberg CL1 Comdty, Refinitiv) to smooth these effects. The FRED DCOILWTICO series is for its part based on the spot price published daily by the EIA, which aggregates physical transactions at Cushing and partially smooths the roll effect.

The FRED DCOILWTICO series is the reference instrument for macro reading. Published by the Federal Reserve Bank of St. Louis from EIA data, it covers the daily WTI spot price at Cushing since January 2, 1986. For extended historical analyses, the monthly series reaches back to January 1946 (under code WTISPLC for the spot series, or various preceding series for older periods). This statistical continuity over 80 years makes it one of the most widely used series in U.S. empirical macroeconomics. The major shocks of the modern series concentrate on three points: peak of March 8, 2022 at $123.70 (Russian invasion of Ukraine), trough of April 20, 2020 at -$37.63 (Cushing saturation + COVID collapse), historical peak at $145.29 on July 3, 2008 (China super-cycle pre-GFC).

Beyond the NYMEX contract, WTI is also tracked via derivative contracts: options on futures, financially settled contracts (NYMEX WTI Cushing Crude Oil Last Day Financial Future, symbol BZ for Brent and symbol WTI for Cushing), inter-market spreads (WTI-Brent), and calendar spreads (M1-M2, M1-M6, M1-M12) that measure the term structure and reveal contango/backwardation expectations. For macro reading, the front-month spot price suffices; term structures interest mainly physical operators and arbitrageurs.

4. Why This Technical Precision Matters for the Macro Reading

The three technical coordinates exposed — light sweet at 39.6° API, physical Cushing pricing with long-short settlement, daily FRED DCOILWTICO series since 1986 — are not specialist details. They condition what WTI can signal and what it cannot signal. Four direct implications for reading WTI as a macro signal.

First, WTI primarily measures the dynamics of the U.S. market. Physical pricing at Cushing reflects U.S. supply-demand equilibrium (shale production, storage capacity, U.S. refinery demand, export capacity). For international macro reading, Brent — physical pricing in the North Sea, but dominant reference for OPEC+ barrels and international flows — is more relevant. The WTI vs Brent choice thus depends on the macro question asked, as explained in the comparison with the Brent benchmark.

Second, physical settlement introduces specific sensitivity to short-term logistical constraints. The -$37.63 of April 2020 is an anomaly produced by the physical contract mechanics, not a fundamental signal on the value of crude as a commodity. Any analyst interpreting that point as a signal on real macro commits a reading error. The Brent contract’s cash settlement avoids this anomaly, making Brent more stable as a fundamental indicator during episodes of extreme logistical stress. Companion research: structural signals from critical minerals and energy.

Third, the daily coverage since 1986 and monthly since 1946 makes WTI the most usable series for long-period empirical analyses. Nearly all academic work on oil shocks, oil burden, and inflation pass-through uses DCOILWTICO or WTISPLC as reference. This is one of the reasons why U.S. macro reading has structurally anchored itself to WTI.

Fourth, the light sweet physical quality implies that shocks on other qualities (medium sour, heavy) do not reflect directly and instantaneously in WTI. When Iran faces sanctions mainly affecting its medium sour exports, or when Venezuela sees its heavy production contracted, the impact on WTI passes through an indirect substitution mechanism that can be slower and more attenuated than on Brent or Dubai. This asymmetry is one of the reasons analysts of the physical market simultaneously track multiple benchmarks.

For the rest of the cluster reading, WTI thus defined serves as an input variable. The six satellites exploit this technical precision to address the WTI-Brent spread, the historical record of shocks, oil-burden mechanics, inflation pass-through, and the contemporary stabilization regime. The present article has framed the instrument; the macro reading that follows is elsewhere. Beyond the cluster, commodity regimes and physical constraints situates WTI within the broader commodities panorama, and structural signals in physical commodity markets addresses the structural constraints common to energy, metals, and critical minerals. The series itself is tracked daily on the live WTI series on Eco3min.

- WTI = light sweet crude 39.6° API, 0.24% sulfur — quality directly refinable into gasoline/diesel without expensive desulfurization

- Physical pricing at Cushing (Oklahoma), 90+ Mb storage capacity, convergence point Permian/Bakken/Canada → Mid-Continent and Gulf refineries

- NYMEX CL futures contract with physical settlement (vs cash on Brent) — cause of the negative -$37.63 price of April 20, 2020

- FRED DCOILWTICO daily series since January 2, 1986, monthly series back to 1946 — academic reference base for empirical macro analysis over 80 years

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

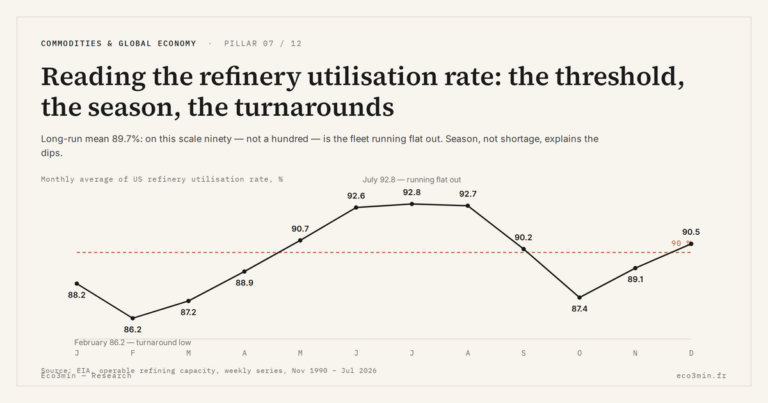

Full pillar →Reading the refinery utilisation rate: the threshold, the season, the turnarounds

A refinery runs full near ninety percent, not a hundred: the last slice of nameplate capacity is a…

IMO 2020: the regulatory shock that rewrote product spreads

An environmental rule on marine sulfur can move a refining spread more than a swing in crude. IMO…

The 2022–2023 refining golden age: anatomy of an episode

In 2022, refined fuel prices climbed faster than crude. That gap, measured by the 3-2-1 crack spread, reached…