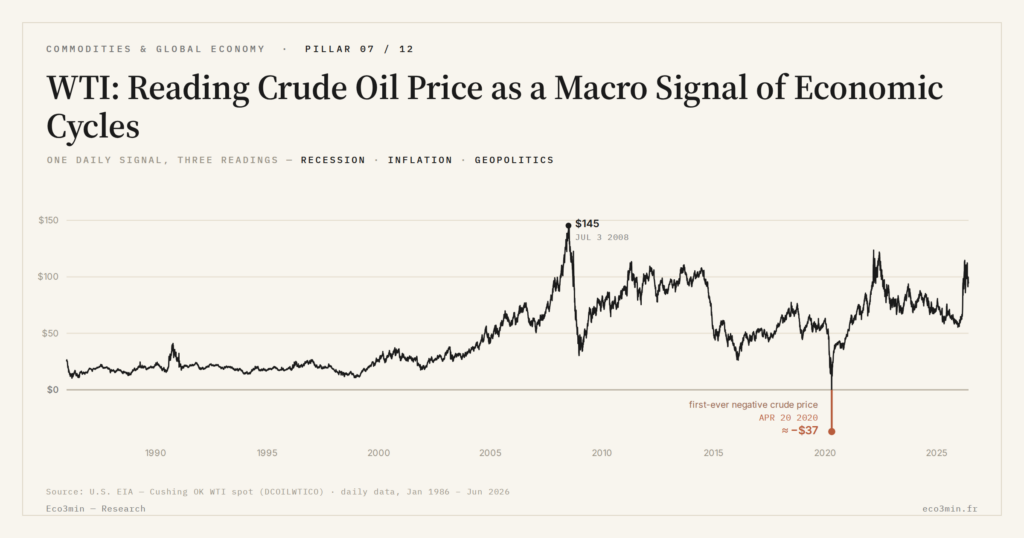

WTI: Reading Crude Oil Price as a Macro Signal of Economic Cycles

WTI, the U.S. barrel priced at Cushing, is not just a price — it is a macroeconomic barometer that compresses physical supply constraints, inflationary transmission, and geopolitical risk premium into a single daily signal.

TL;DR

WTI's grip on U.S. inflation has loosened: the six-month pass-through elasticity to headline CPI fell from 0.32 (1990-2007) to 0.19 (2010-2019).

- Recession precursor: every U.S. recession since 1973 has followed an oil burden (price x consumption / GDP) above 4%; the May 2026 reading near 2.5% reaches it only with WTI held durably above $115-120.

- Geopolitical premium: 20-25% of seaborne oil crosses the Strait of Hormuz; the 2024 Iran-Israel strikes drove $5-8 spikes that faded within days, an event-spike distinct from the event-signal of Russia's March 2022 invasion.

- Why WTI over Brent: DCOILWTICO has run daily since 1986 with physical Cushing settlement and tracks U.S. GDP and CPI, while Brent's statistical definition shifted with BFOE (2002) and WTI Midland's entry into Dated Brent (May 2023).

This piece frames the WTI instrument and its three analytical functions. The cluster’s six satellites unpack each dimension of the macro reading proposed here, without duplicating it.

1. WTI: A Barrel, A Hub, A Time Series

West Texas Intermediate refers to a light sweet crude of 39.6° API and 0.24% sulfur — technical specifications that make it a high-quality grade refinable into gasoline and diesel at low marginal cost. Per NYMEX documentation (2024 revision), this physical precision justifies its status as the U.S. pricing benchmark. At higher density or sulfur content, refiners face desulfurization and cracking costs that compress margins; WTI sidesteps those frictions by construction. See also the spread between crude and refined products.

API gravity measures the relative density of crude compared to water. Above 31° API, crudes are classified as light; below 22°, as heavy. WTI at 39.6° API sits firmly in the light segment. Sulfur is the other critical dimension: below 0.5%, crude is sweet; above, sour. Sour crudes require dedicated desulfurization units (hydrocrackers, Claus units) that weigh on refinery operating costs. WTI combines both qualities required to produce the highest-margin light cuts — gasoline and diesel — without desulfurization investment. This profile is what historically made it the U.S. market’s reference barrel. A related perspective: every oil shock since 1973.

Physical pricing happens at Cushing, Oklahoma. The hub concentrates over 90 million barrels of storage capacity per EIA figures, fed by pipelines draining the Permian Basin, the Bakken, and Canadian inflows. This concentration is not neutral — it makes WTI a landlocked price, inseparable from pipeline logistics. When Cushing saturates, WTI decouples from the global market: the transport premium explodes, exactly what was observed in 2011-2014 when the shale boom overwhelmed evacuation capacity to the Gulf of Mexico. Per FRED data, the WTI-Brent differential reached -$28 in October 2011, until the partial lifting of the U.S. crude export ban in December 2015 and the commissioning of new pipelines (Seaway, Cushing-Houston) restored circulation. More context: uranium versus oil and gas.

The reference quote is the NYMEX front-month contract, whose moves populate FRED’s DCOILWTICO series at daily frequency since January 2, 1986. For extended historical analysis, the monthly series reaches back to 1946. Three temporal anchors structure the modern reading. The March 8, 2022 peak at $123.70, hit in the days following Russia’s invasion of Ukraine. The April 20, 2020 trough at -$37.63, the first historical instance of a negative price on a crude futures contract, the joint product of Cushing storage saturation and a COVID demand collapse. And the current level around $70-80 (FRED DCOILWTICO, May 2026), characterizing a post-2023 stabilization phase whose determinants are addressed in the dedicated WTI 2024-2026 stabilization regime analysis. A broader view: drought’s effect on cocoa yields.

Technical precision matters because the macro reading that follows depends on it. When analysts cite “the oil price,” they almost always mean WTI or Brent — and the angle shifts with the choice. For the U.S. macro reading (oil burden, CPI, recession), WTI dominates; for the global macro reading (geopolitical supply, energy transition, OPEC+ financing), Brent is more relevant. The WTI pricing mechanics at Cushing piece details the technical specifications further and the hub’s physical operation. The structural distinction between the two barrels is treated separately in WTI-Brent spread and comparative reading.

A final technical element deserves mention. The NYMEX WTI contract has physical settlement: at expiration, the long position holder must take physical delivery of crude at Cushing, and the short position holder must deliver it. This physical obligation is what produced the negative April 2020 price. Long positions arriving at expiration without available storage capacity had to pay to discharge their receiving obligation. ICE Brent, by contrast, operates on cash settlement, without equivalent physical constraint — a structural differential that makes WTI more sensitive to short-term logistical constraints and Brent more sensitive to international dynamics. Related framing: Physical Commodity Markets: Oil, Gas, Copper, Critical Minerals, and Structural Signals.

2. First Function: Recession Precursor Through the Oil Burden

The oil burden is the metric that formalizes the intuition that expensive oil weighs on growth. Its definition is simple: oil price × national consumption / nominal GDP. Economist James Hamilton (UCSD) laid out the analytical mechanics in a series of papers starting in 1983, and the formulation has remained stable for four decades.

Per Eco3min calculations on FRED data (DCOILWTICO for price, EIA data for consumption, BEA nominal GDP), every U.S. recession post-1973 has been preceded by an oil burden equal to or above 4% of GDP. The threshold is empirical — it is not inscribed in economic theory in the strict sense — but its statistical robustness over five decades makes it a reference signal. Above 4-5%, the combination of three channels produces a cumulative dynamic that slides into recession.

First channel: wealth transfer to producers. Net oil exporters (OPEC+ historically, more recently the United States since 2019) receive increased revenues, but their marginal propensity to consume or invest in the global economy is lower than that of net importers. A share of the transfer is saved as foreign exchange reserves or invested in international financial assets, producing a net compression of global aggregate demand.

Second channel: terms-of-trade distortion. A net oil-importing country sees its trade balance mechanically deteriorate when the price rises. The macroeconomic counterpart is a compression of aggregate domestic purchasing power. For European economies and Japan, dependent on energy imports at 90-95%, this channel is particularly strong. For the United States, which became a net exporter in 2019, the channel is partially neutralized — but remains active regionally (producing states gain at the expense of importing states). A parallel read: Eco3min’s real commodity price index.

Third channel: contraction of household discretionary demand. Energy’s share in U.S. household budgets went from 4% in 1970 to a peak of 9% in 1980, fell back to 3-4% in the 2000s, then rose again to 5-6% during recent peaks (per BLS Consumer Expenditure Survey). When energy devours a growing share of the budget, households compress discretionary spending — restaurants, leisure, durable goods — which are precisely the most cyclical components of GDP. This discretionary contraction amplifies the slowdown induced by the first two channels.

Current level (May 2026): approximately 2.5% of GDP, per Eco3min calculation (WTI averaging ~$75 × 7.5 billion barrels of U.S. annual consumption / $28.5 trillion nominal GDP). Well below the 4-5% critical threshold — one of the reasons why the $70-85 stabilization phase does not trigger recession despite an accumulation of geopolitical tensions. For the burden to reach 4%, at constant GDP and consumption, WTI would need to be durably above $115-120.

The chronological empirical audit of each pre-recession episode since 1970 is covered in a dedicated Eco3min empirical oil-burden study (case-by-case audit with datavisualizations). The mechanical decomposition specific to this cluster — how the three channels articulate quantitatively — is unpacked in the oil-burden mechanics at the critical threshold.

The 4-5% of GDP oil burden threshold is not a theoretical rule but an empirical regularity over fifty years — its robustness comes from cumulative observation, not from a structural model.

3. Second Function: Inflation Transmitter

Oil enters inflation through two distinct channels. The direct channel runs through household energy prices (gasoline at the pump, heating oil, electricity when the marginal source is itself gas-indexed to oil) and through transport costs passed on by firms to wholesale prices. The indirect channel runs through upstream production prices (energy inputs for chemicals, petrochemicals, plastics, fertilizers) that feed through with a lag to the final price of manufactured goods. Read alongside: the share-versus-volume distinction in power.

Economic literature measures this transmission through the pass-through elasticity. Hamilton (2009), Kilian (2014), and BIS Working Paper 906 (2020) converge on an order of magnitude: a 30% WTI shock transmits between 0.2 and 0.4 of the shock to U.S. headline CPI over six months, with a weaker effect (0.05 to 0.1) on core CPI which excludes energy. The coefficient is not a constant: it depends on the macro regime, on the composition of the consumption basket, and on the nature of the shock itself (supply vs demand).

Per Eco3min calculations on FRED data (DCOILWTICO, CPIAUCSL for headline CPI, CPILFESL for core CPI, period 1990-2025), the pass-through has weakened post-GFC. Over 1990-2007, the average elasticity estimated by simple six-month regression comes out at 0.32; over 2010-2019, it falls to 0.19. The post-2020 period is harder to interpret because the COVID and Ukraine shocks overlaid already-elevated inflation dynamics, making regressions unstable.

Three candidate explanations are advanced in the literature for the structural weakening. First, the better anchoring of inflation expectations post-1980 (the Volcker regime, then the Fed’s 2% target) which prevents price shocks from generating second-round wage-price spirals. Second, the decline in energy intensity of transport and industry: a dollar of U.S. GDP consumed about 1.1 energy units in 1980 (base 1) compared with 0.55 in 2020 (per BTU/dollar EIA data). Third, partial electric substitution, notably in residential heating and progressively in mobility — electric vehicles went from 1% of U.S. new car sales in 2017 to about 10% in 2024 per BloombergNEF.

The distinction between direct pass-through and cyclical amplification is critical for the macro reading. When WTI rises in an already-inflationary regime — typically 2021-2023, when U.S. inflation already exceeded 5% before the Ukraine shock — the pass-through adds to existing inflation rather than creating it. This amplification effect is documented separately by Eco3min in a dedicated piece on WTI supply shocks and U.S. core inflation 1986-2026, which isolates the episodes where WTI contributed to extending an already-installed inflation rather than initiating one.

The mechanical decomposition specific to this cluster — pass-through breakdown by regime, Eco3min measurements over 1990-2025, comparison of headline vs core — is addressed in WTI pass-through to consumer prices. This MAJEUR limits itself to positioning the WTI analytical function as transmitter, without conducting the quantitative audit.

4. Third Function: Geopolitical Indicator

WTI aggregates into its price a geopolitical risk premium that is not measured directly but inferred. When a supply event (strike on oil infrastructure, choke point blockade, sanctions on a major producer) materializes without a compensating demand shock, the gap between observed price and implied fundamental price reveals the market’s valuation of the residual risk.

The Strait of Hormuz is the archetype. Per EIA estimates (Today in Energy, October 2024), 20-21 million barrels per day transit through Hormuz — that is, 20 to 25% of seaborne global oil trade. Any Iranian tension capable of credibly threatening Hormuz navigation translates into an immediate WTI rise, whether or not physical interruption actually occurs. The Iran-Israel crossed strikes of April and October 2024 produced WTI spikes of $5 to $8 that resolved within days once the absence of spillover onto Hormuz was confirmed. The semantics of the move matter: the market prices the tail of the distribution (low-probability, high-impact event), even when the mode of the distribution remains around fundamental equilibrium. A companion piece: Uranium: Why Spot and Long-Term Contract Prices Diverge.

The Bab el-Mandeb Strait and the Suez Canal operate on the same principle, but with lower intensity. Per Suez Canal Authority (SCA) 2024 figures, 8-9% of seaborne global crude trade transits through Suez. The Houthi attacks on Red Sea traffic from late 2023 onwards triggered massive rerouting via the Cape of Good Hope — additional cost for shipowners on the order of $1-2 per barrel per sector estimates, without equivalent impact on WTI because oil flows structurally bypassed Suez via Saudi Red Sea pipelines and Russian crude progressively redirected toward Asia.

Sanctions on major producers constitute another channel. The 1973 Arab embargo, U.S. sanctions on Iran post-1979 and post-2018, the G7 sanctions on Russian crude post-February 2022 (price cap at $60 on Urals) each produce a displacement of the risk premium. The complexity lies in the fact that modern sanctions (post-2022) were designed to limit the supply shock while depriving Russia of part of its revenues — hence the price cap mechanism rather than a total embargo. Observed effects on WTI have been more moderate than what a classical embargo would have produced, because Russian volumes continued to flow to India, China, and Turkey at the capped price.

The geopolitical reading of WTI must therefore distinguish between event-signal (durably reorienting the structural risk premium) and event-spike (absorbed within days or weeks). Russia’s invasion of Ukraine in March 2022 is typically an event-signal: the risk premium on Russian crude remained structurally repriced, the European market durably reoriented toward other suppliers, and the geography of flows was redrawn. The Iran-Israel 2024 strikes are by contrast event-spikes: immediate premium, rapid resorption, return to fundamental equilibrium.

This reading grid is exactly what emerges from the historical decomposition of the seven major oil shocks since 1973 — treated separately in the cluster’s oil shocks since 1973, which proposes the chronological taxonomy with dates, magnitudes, and identified drivers.

5. Why WTI Rather Than Brent as a Macro Barometer

If Brent has more international status (per 2024 ICE figures, about two-thirds of global barrels are referenced against Brent), why prioritize WTI in a macro reading? Three arguments converge.

First, statistical availability. The FRED DCOILWTICO series has been published daily since 1986 by the EIA with minimal monthly revisions — it is an academic reference series, used in nearly all empirical work on oil and U.S. macro. Brent (FRED DCOILBRENTEU) is available but with shorter temporal coverage on FRED (since 1987 daily) and evolving pricing conventions. The introduction of BFOE in 2002 (Brent-Forties-Oseberg-Ekofisk), then the integration of WTI Midland into the Dated Brent basket in May 2023, have successively modified the statistical definition of Brent. For consistent long-term analysis, WTI is methodologically more stable. Related discussion: Gold set against crude as a macro gauge.

Second, alignment with U.S. macro variables. The oil burden is calculated on U.S. variables (BEA U.S. GDP, EIA U.S. consumption), thus with WTI as the relevant price. The U.S. CPI more directly weights U.S. energy prices, themselves more correlated with WTI than with Brent due to internal logistical constraints of the U.S. market (limited light crude imports since the shale revolution, domestic market dominated by Permian-Bakken-Cushing-Gulf flows). To study U.S. macro, WTI dominates mechanically.

Third, pricing transparency. WTI is quoted on NYMEX (CME Group), with physical settlement at Cushing — physical arbitrage is anchored in the futures contract mechanics, creating strong alignment between observed price and local supply-demand fundamentals. Brent has progressively become a reference for physical assessments based on BFOE cargoes, with a higher degree of judgment in fixing the Dated Brent benchmark by Platts (S&P Global Commodity Insights). For an analyst seeking a robust quantitative reference without interrogating the aggregation methodology, WTI offers superior readability. Related data is available in the US retail diesel price dataset.

This does not mean Brent should be ignored. For tracking international arbitrage, OPEC+ financing (whose barrels are mostly sold on Brent or Dated Brent reference), and the Middle East geopolitical premium (which prints first on Brent because of the geographical proximity of the European market to the Middle East), Brent remains more relevant. The Eco3min analytical grid consists of using WTI as the U.S. macro barometer and Brent as the international macro barometer, without absolute hierarchy but with the choice dictated by the question asked.

The cluster’s analytical treatment of the structural mechanics of the differential is addressed in WTI-Brent structural differential in its own right, with decomposition of the three factors (U.S. exports, Cushing logistics, pricing geography) producing the structural WTI discount since 2011.

The idea that Brent would always be preferable to WTI because it is more international misses the point. For the U.S. macro reading, statistical coherence with U.S. variables (GDP, CPI, consumption) imposes WTI. The choice depends on the question asked, not on an abstract hierarchy between the two benchmarks.

6. Reading WTI in the 2024-2026 Stabilization Regime

WTI has settled around $70-85 since late 2023, in a surprisingly narrow corridor despite a tense geopolitical configuration: materialized Iran-Israel tensions (crossed strikes April and October 2024), Red Sea traffic disrupted by Yemeni Houthis, the Russia-Ukraine war still ongoing after more than four years, OPEC+ cumulative voluntary cuts of 3.66 million barrels per day since 2023 per the cartel’s official figures. Historically, any of these factors alone would have triggered strong volatility. Three competing readings explain the observed stability.

First reading: the structural slowdown in Chinese demand. Per the EIA STEO of May 2026, Chinese oil demand grew by +1.2% in 2025, compared with an average of +4.5% per year over 2003-2019. This deceleration stems simultaneously from the structural post-COVID Chinese growth slowdown (around 4.5-5% GDP growth per China’s NBS, vs 9-10% in the 2000s), accelerating EV penetration (BYD sold more than 4 million units in 2024 per CAAM, with a major share on the domestic market), and the structural shift to gas in China’s industrial and electrical mix. China, which was responsible for about 60% of global oil demand growth over 2010-2019, no longer pulls the market upward.

Second reading: U.S. shale’s adjustment capacity. Per the Dallas Fed Energy Survey of Q1 2026, the average break-even for new Permian wells sits between $45 and $55 depending on operators, with a median around $50. When WTI rises above $80, shale increases production with an investment cycle lag of 6 to 12 months (drilling, completion, production start); when WTI drops below $60, producers cut drilling (Baker Hughes rig count slowdown). This shale-as-swing-producer mechanism, where production adjusts at the margin with price, is a structural twenty-first-century novelty that bounds volatility episodes. Before 2010, the swing producer function was assumed mainly by Saudi Arabia and OPEC; since 2014, U.S. shale shares it, and since 2020 combines it with renewed OPEC+ discipline. Our registry of shuttered and converted US refineries documents a neighbouring case.

Third reading: the intermediate position of the U.S. Strategic Petroleum Reserve. The SPR sits at approximately 370 million barrels in May 2026 per the Department of Energy, that is, about 50% of its theoretical maximum capacity of 727 million. This position is intermediate: no significant room to release further (the 2022 releases drained 180 Mb, and going lower would expose to insufficiency risk in case of an actual major shock), but also no immediate pressure to refill at current prices (the DOE has been buying back at indicative prices around $70 per 2024-2025 announcements, and has no operational urgency for refill). This intermediate position neutralizes a volatility factor that played strongly in 2022-2023.

None of the three readings alone suffices to explain the observed stability — it is their conjunction that produces the $70-85 corridor. If Chinese demand structurally rebounds (unlikely in the short term), if shale break-even significantly drifts lower via productivity gains (possible but slow), or if the SPR position becomes prescriptive (likely only in case of a major shock), the corridor could deform.

Eco3min does not opine on WTI’s future trajectory, but maps the three competing readings in three readings of the 2024-2026 regime dedicated to the current regime, with quantitative decomposition of the estimated contributions of each factor.

7. The Historical Grid of Seven Shocks

WTI has traversed seven major shocks since 1973, each combining in variable doses three ingredients: physical supply constraint, structural demand pull, and financial stress. Structural signals from oil, gas and metals unpacks the underlying machinery.

The Arab embargo of October 1973 (price quadrupled in six months, from $3 to $12) is almost pure supply. The Iranian Revolution of 1979 (tripled, from $14 to $39) adds a long regional geopolitical dimension. The 1990 Gulf War produces a short spike to $40 quickly resolved after the launch of Operation Desert Storm in January 1991. The China super-cycle 2003-2008 (from $30 to $147 in five years) is dominated by demand, with weak dollar contribution and financial speculation. The Arab Spring 2011 produces a post-GFC rebound fitting within an inventory-rebuilding dynamic and a Middle East risk reassessment. The COVID shock of April 2020 (historic floor at -$37.63) is purely demand collapse crossed with Cushing saturation. Russia’s invasion of Ukraine in March 2022 (peak $123.70) recombines supply (sanctions on Russian crude, European repositioning) and financial stress (flight to commodities as an asset class). The mechanism is unpacked in the Eco3min reading of physical commodity markets. The empirical record is assembled in Eco3min’s chronology of historical market crises.

The mapping of these seven episodes — dates, magnitudes, triggers, duration of effects — is covered in the historical grid the seven oil shocks grid, which proposes a common chronological framework with datavisualizations. The empirical audit of the oil burden threshold specific to each recession that followed is addressed in the dedicated EN case-by-case oil-burden audit (case-by-case with BEA and FRED data).

Beyond the cluster, WTI monitoring benefits from being cross-referenced with other commodity signals through the commodity regimes pillar. At the sub-pillar level, the reading fits within physical commodity markets, which covers oil, gas, copper, and critical minerals. The specific cross-reading between oil signal and copper signal as twin economic indicators is explored in Dr Copper vs Dr Oil as cross-commodity signals.

Eco3min reads WTI as a composite indicator. Three analytical functions (recession precursor, inflation transmitter, geopolitical risk gauge) that activate neither simultaneously nor with the same intensity. The analytical grid consists of identifying which of the three is mobilized at a given moment, rather than searching for THE cause of a price move. On this point: the case for soft landing or hard landing.

Conclusion: A Composite Signal, Not a Single One

WTI’s macro reach reduces neither to an inflation signal, nor to a recession precursor, nor to a geopolitical barometer taken in isolation — it is the joint reading of the three functions that produces the useful macro information. None of the three alone suffices to explain an observed price move; each participates in the composition of the signal. Analytical competence consists of identifying which of the three dominates at a given moment, and measuring its relative contribution, rather than searching for a single causality that rarely exists in empirical observation. The WTI series itself is tracked daily on the Eco3min WTI dataset on Eco3min.

- WTI = U.S. barrel priced at Cushing (light sweet 39.6° API, 0.24% sulfur), FRED DCOILWTICO series daily since 1986

- Three analytical functions: recession precursor (oil burden, empirical threshold 4-5% of GDP), inflation transmitter (pass-through 0.2-0.4 over 6 months on headline CPI), geopolitical indicator (risk premium on Hormuz, Bab el-Mandeb, and sanctions)

- Current level (May 2026) ~$70-85, stabilization explainable by three factors: slower Chinese demand (+1.2% in 2025 vs +4.5% average 2003-2019), U.S. shale as swing producer (Permian break-even $45-55), SPR at 50% of capacity (370 Mb)

- Current oil burden ~2.5% of U.S. GDP, well below the 4-5% critical threshold — WTI would need to be durably above $115-120 to tip into recessionary territory

Last updated — 13 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →IMO 2020: the regulatory shock that rewrote product spreads

An environmental rule on marine sulfur can move a refining spread more than a swing in crude. IMO…

The 2022–2023 refining golden age: anatomy of an episode

In 2022, refined fuel prices climbed faster than crude. That gap, measured by the 3-2-1 crack spread, reached…

Diesel versus gasoline: why the two crack spreads diverge

The 3-2-1 crack blends gasoline and distillate into a single number, and that convenience hides something the market…