WTI vs Brent: Spread Structure and the U.S.-Europe Crude Oil Arbitrage

Since 2011, WTI has structurally priced $3 to $5 below Brent. This discount is not anecdotal: it results from three mechanical factors — U.S. export capacity, Cushing logistics, pricing geography — that clarify what each benchmark actually measures.

TL;DR

WTI has priced a structural $3-5 below Brent since 2011, a gap that measures logistical friction between a landlocked U.S. barrel and a waterborne global one, not crude quality.

- The 2011 rupture: the spread hit -$28.12 on September 14, 2011 (WTI $86.76 vs Brent $114.88) as shale crude saturated landlocked Cushing under the still-active export ban.

- Resolution came with the partial lifting of the export ban in December 2015 (Consolidated Appropriations Act) plus new Cushing-to-Gulf pipelines, pulling the spread to its current -$3 to -$5.

- That structural gap maps marginal transport cost: roughly $2-3 pipeline from Cushing to the Gulf plus $2-3 tanker to Europe (Argus Media estimates), with Cushing sitting 1,100 km inland.

- Transitory widenings track asymmetric shocks: the spread reached -$11 in March 2022 after Russia's invasion, while Gulf hurricanes such as Harvey 2017 and Ida 2021 can briefly invert it.

This piece does not rebuild the year-by-year chronology of the spread. It does something else: expose the structural mechanics that produce the spread, and the conditions under which it can invert or widen.

1. WTI vs Brent: Two Barrels, Two Worlds

WTI and Brent are the world’s two reference barrels, and their spread is one of the most heavily traded relationships in commodities markets. On the physical side, they are close: Brent at 38° API and 0.4% sulfur, WTI at 39.6° API and 0.24% sulfur. Both are light sweet crudes, refinable without major desulfurization investment. At the level of atmospheric distillation, a refiner does not make a major distinction between them. Adjacent reading: our guide to frequent errors about commodities and gold.

The divergence comes from elsewhere. WTI is a U.S. barrel priced at Cushing, Oklahoma — a landlocked pipeline convergence point. Brent is a European barrel priced in the North Sea, whose reference basket (BFOE: Brent-Forties-Oseberg-Ekofisk, extended in May 2023 with WTI Midland integrated into the Dated Brent basket) aggregates Norwegian and British offshore production. This geographical opposition — internal pipeline vs international maritime — is the primary origin of the spread. The same geography drives the TTF–Henry Hub gas spread.

On market conventions, WTI is quoted on NYMEX (CME Group) with physical settlement at Cushing. Brent is quoted on ICE with cash settlement. Per ICE and CME 2024 statistics, the Brent contract remains slightly more liquid in notional volume (about two-thirds of global barrels referenced against it for physical transactions), while WTI dominates in financial futures volume on the U.S. market. The WTI technical specifications have been addressed separately within the cluster: what matters here is that the two barrels are not logistically substitutable, even when they are physically substitutable for the refiner.

This dual identity — physically almost equivalent, logistically radically different — produces a spread that is not a quality signal but a friction signal. When the spread widens, it is not that WTI is worth less as a crude; it is that the logistical friction between the U.S. market and the global market intensifies. When it tightens, it is not that WTI improves, it is that the friction reduces. The macro reading of the spread is therefore primarily a reading of physical circulation, not of fundamental value.

2. Before and After 2011: The Spread Rupture

For the twenty years preceding 2011, WTI and Brent traded at parity, with the spread typically oscillating between -$1 and +$2. This is examined closely in this analysis of oil refining margins crack spread. Over the 1987-2010 period, the average WTI-Brent spread (calculated on FRED DCOILWTICO and DCOILBRENTEU series) comes out at +$0.60, meaning WTI slightly more expensive than Brent. This parity reflected an equilibrium of international physical markets where U.S. crude production was roughly sufficient for U.S. refining demand, and where the U.S. crude export ban instituted in the 1970s had no significant impact for lack of a U.S. surplus to export. Related reading: gold measured in barrels of oil over the long run.

The rupture comes from 2011 onwards. The U.S. shale boom — initiated by the combination of hydraulic fracturing and horizontal drilling in the Bakken and then the Permian — produces a growing surplus of light sweet crude in the United States. U.S. production rises per EIA figures from 5.5 million barrels per day in 2010 to 9.4 in 2015, then to 12.3 in 2019. This surplus cannot flow to export due to the export ban still in force (Crude Oil Export Ban instituted in 1975 by the Energy Policy and Conservation Act post-1973 embargo). The crude therefore accumulates at Cushing. On the European energy-cost counterpart, see the weight of the energy import bill.

Per FRED data, the WTI-Brent spread reaches its extreme at -$28.12 on September 14, 2011 (WTI at $86.76 vs Brent at $114.88). This differential directly reflects logistical saturation: crude produced in the Bakken and Permian arrived at Cushing without being able to flow to Gulf refineries or to export. To sell, U.S. producers had to accept a massive discount versus the international reference price.

The progressive resolution begins in 2012-2013 with the commissioning of pipelines evacuating Cushing toward the Gulf (Seaway reverse flow, Diamond Pipeline, Permian-Gulf Coast pipelines). The decisive moment is the partial lifting of the export ban in December 2015 (Consolidated Appropriations Act). From 2016 onwards, the spread progressively reduces and stabilizes around -$3 to -$5, a level that now reflects the marginal cost of transporting U.S. crude to international markets. This structural level has prevailed since and forms the implicit backdrop of the WTI 2024-2026 price regime.

3. Three Structural Factors of the Post-2011 Spread

The structural WTI discount of -$3 to -$5 prevailing since 2016 results from three mechanical factors acting simultaneously.

First factor: U.S. export capacity, lifted but constrained. The lifting of the ban in December 2015 allowed the United States to become a net crude exporter in September 2019 per EIA statistics. But physical export capacity remains constrained by port terminals (Corpus Christi, Houston, Beaumont, Saint James) and their loading capacity. Per EIA 2024 figures, total U.S. crude export capacity reaches about 7-8 million barrels per day, versus actual exports around 4 million barrels per day. The theoretical margin exists, but loading logistics friction, maritime insurance, and Jones Act constraints on internal coastal shipping create a persistent transport cost that imprints in the spread.

Second factor: Cushing logistics as bottleneck. Even after the commissioning of the Cushing-Houston pipelines and the lifting of the ban, Cushing remains a periodic bottleneck. When shale production accelerates faster than evacuation, Cushing stocks rise. Per EIA data, Cushing stocks oscillate between 30 and 65 million barrels over the 2020-2026 period (maximum capacity around 90 Mb), and stock peaks correspond to WTI-Brent spread widenings. Cushing logistics has become an operational barometer closely tracked by spread traders.

Third factor: pricing geography. Cushing is landlocked 1,100 kilometers from the Gulf; Brent is waterborne, accessible from any European port and exportable to any global market without pipeline constraint. This geography creates asymmetric transport cost: for a Cushing barrel to reach the European market, it must transit by pipeline to the Gulf (cost ~$2-3 per barrel per Argus Media estimates), then by tanker to Europe (cost ~$2-3 depending on routes and seasonality). The $3-5 differential prevailing since 2016 corresponds approximately to this marginal pipeline + tanker transport cost.

These three factors are structurally linked. If U.S. export capacity expanded significantly (new port terminals under construction in Texas and Louisiana), if Cushing logistics relaxed (new evacuation pipelines), or if pricing geography was modified (deeper integration of WTI Midland in the Dated Brent basket, which began in May 2023), the spread could structurally reduce. But none of these evolutions act over a few months — they belong to heavy capital with long investment cycles.

4. Under What Conditions the Spread Can Invert or Widen

The -$3 to -$5 structural spread is neither carved in stone nor mechanically permanent. Three types of situations can deform it.

First situation: an asymmetric supply shock on European or Middle Eastern crude. When the European market loses access to part of its supply (Russia sanctions post-February 2022, Strait of Hormuz blockade, Trans-Alpine pipeline disruption), Brent rises faster than WTI because the European market is directly exposed. The WTI-Brent spread can then temporarily widen (WTI further behind), up to $8-10 of gap over a few weeks, before substitution flows rebalance. The March-April 2022 episode after Russia’s invasion of Ukraine is an example: the spread temporarily reached -$11 in March 2022 per FRED. Further reading: the physical side of the commodity complex.

Second situation: an asymmetric supply shock on U.S. crude. This is rarer, but it has occurred during major Gulf of Mexico hurricanes (Harvey 2017, Ida 2021) which temporarily shut down U.S. offshore production installations and export port terminals. WTI can then rise faster than Brent, and the spread can tighten or even briefly invert (WTI above Brent). These episodes are typically short (days to weeks) and resolve with the resumption of installations.

Third situation: an asymmetric demand shock. When Chinese demand collapses (Q1 2020 COVID, post-2022 slowdown) without an equivalent shock on U.S. demand, Brent can fall faster than WTI because Asia is a more important outlet for Middle Eastern and African crude referenced against Brent. Symmetrically, when U.S. demand collapses (U.S. recessions) without an equivalent global shock, WTI can decouple.

Beyond these transitory situations, a structural inversion (WTI durably above Brent) would presuppose a major reversal of global crude logistics — for instance a return of Russian crude on the European market combined with a structural contraction of U.S. shale production. No serious analyst anticipates this scenario in the short term. The -$3 to -$5 structural spread therefore remains the anchor point for cluster analyses in 2026.

For the chronological year-by-year audit of the spread since 1987, Eco3min has published a dedicated study covering 39 years of divergences and their determinants episode by episode in the historical WTI-Brent spread audit. For the broader macro reading of WTI as a barometer, the reference is the WTI as the U.S. macro barometer. Beyond the cluster, the spread dynamic fits within the broader panorama of broader commodities panorama and within energy resources geoeconomics which structures the Eco3min analysis of physical markets. Brent itself is tracked daily on the Brent dataset on Eco3min.

- WTI and Brent are physically very close (light sweet, 38-40° API) but logistically opposite: WTI landlocked Cushing, Brent waterborne North Sea

- Structural spread -$3 to -$5 since 2016, after an extreme episode at -$28 in September 2011 tied to Cushing saturation during the shale boom

- Three mechanical factors produce the spread: constrained U.S. export capacity, Cushing logistics as pivot, landlocked vs waterborne pricing geography

- The spread can widen transitorily (asymmetric supply shocks: Russia 2022 at -$11), but a durable structural inversion would presuppose a major reversal of global crude logistics

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

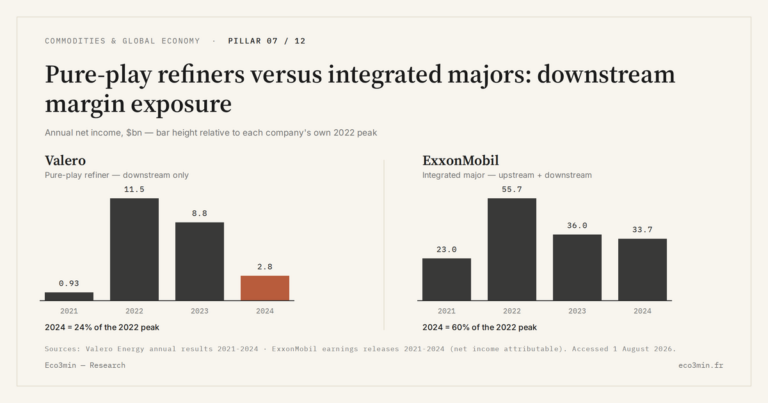

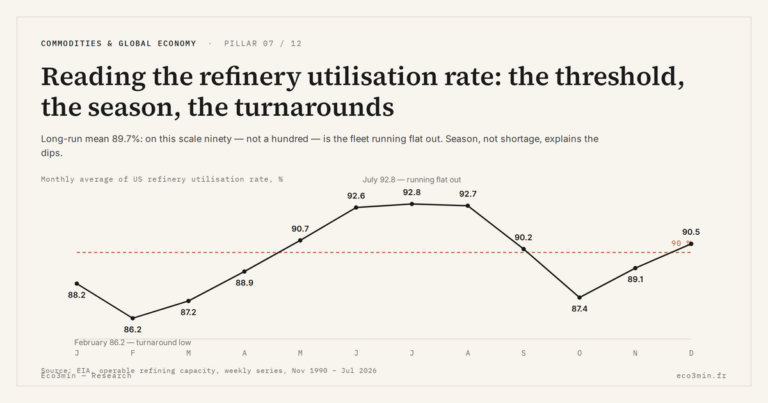

Full pillar →Reading the refinery utilisation rate: the threshold, the season, the turnarounds

A refinery runs full near ninety percent, not a hundred: the last slice of nameplate capacity is a…

IMO 2020: the regulatory shock that rewrote product spreads

An environmental rule on marine sulfur can move a refining spread more than a swing in crude. IMO…

The 2022–2023 refining golden age: anatomy of an episode

In 2022, refined fuel prices climbed faster than crude. That gap, measured by the 3-2-1 crack spread, reached…