Negative Term Premium 2016-2024: Anatomy of an Eight-Year Monetary Anomaly

For eight consecutive years — from June 2016 to August 2024 — the 10-year Treasury term premium remained in negative territory, a configuration modern finance had theoretically ruled out and that the New York Fed nonetheless measured month after month on its ACM dashboard.

TL;DR

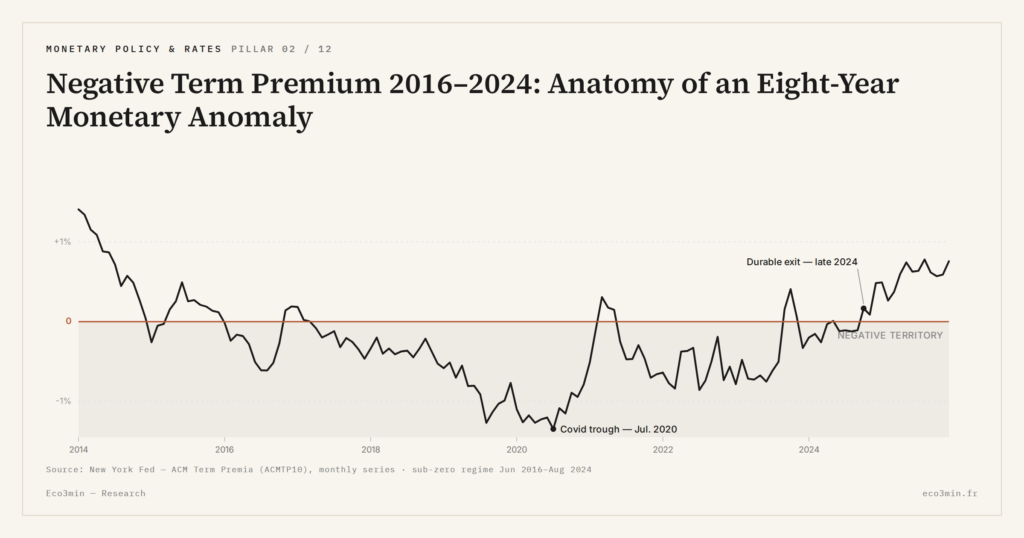

From June 2016 to August 2024 the 10-year Treasury term premium stayed negative for eight straight years, the longest such stretch in the ACM model's history back to 1961.

- Earlier negative-premium episodes (the late 1950s, 1993-1994, the 2004-2007 Greenspan phase) never ran beyond a twenty-month stretch, per Christensen and Rudebusch's ACM backcast.

- Three forces held the residual under zero: persistent QE3 reinvestment (Fed balance sheet near 4.5 trillion through 2017), prolonged ZIRP, and structural Treasury demand from Basel III collateral rules and pension liability-matching.

- The premium bottomed near minus 1.2% in March 2020, then stayed negative through the fastest hiking cycle in forty years (0-0.25% to 5.25-5.50%), crossing zero durably only in August 2024, eighteen months after the last hike.

Three sub-periods structure this anomaly: post-QE3 persistence through 2019, Covid shock and renewed ZIRP through 2021, hiking cycle with persistently negative premium through 2024. No spontaneous return to normal.

1. Characterizing the Historical Anomaly

The ACMTP10 term premium crossed into negative territory in June 2016 per the New York Fed estimates. The series then left a near-zero zone it had occupied since early 2014 — the exit from QE3 — to settle durably below the line. What makes the 2016-2024 phase exceptional is not the mere negativity of the residual, but its persistence: eight consecutive years without a durable crossing of zero, an unprecedented configuration in the modern history of the ACM model backcast to 1961. Related question: what a negative term premium signals.

Prior negative-premium episodes had not extended through time. Christensen and Rudebusch (2019), in an FRBSF Economic Letter publication, reconstructed the pre-2013 history by applying ACM retrospectively: a brief episode in the late 1950s is identifiable, another in 1993-1994, and a third during the Greenspan phase 2004-2007 — none exceeded a twenty-month consecutive stretch. Crump and Gospodinov (2022), in a methodological study published in the Journal of Econometrics, confirmed that these brief pre-modern episodes are not comparable in nature to the 2016-2024 phase: they corresponded to particular cycle configurations, while the post-2016 phase reflects a structural transformation of market conditions.

The historical floor is reached in March 2020 at the height of the Covid shock, near minus 1.2% per ACM backcasted estimates. This level implies that at that precise moment, an investor acquiring a 10-year Treasury was receiving, as compensation for carrying ten years of duration, roughly 120 basis points less than would have been received by rolling successive short positions — a configuration classical finance would have judged arbitrageable absent frictions. For the overall decomposition of this negative residual, the post-2008 monetary context is what must be invoked. A related question: whether negative rates actually work.

2. Sub-Period 1 — 2016-2019: QE3 Persistence and First Hiking Cycle

Between June 2016 and end-2018, the ACMTP10 term premium oscillated between minus 20 and minus 50 basis points. Three forces combined to explain this durable settling in negative territory. First force: the persistence of Fed QE programs. QE3, completed in October 2014, left a stock of duration removed from the market for years. The Fed continued reinvesting maturing coupons and amortizations through October 2017, which sustained purchase pressure on long Treasuries even after the program’s nominal end. The Fed balance sheet then remained around 4.5 trillion dollars per FRED WALCL — a historically high level that mechanically weighed on the demanded premium. Supporting data: The term-premium history series.

Second force: ultra-accommodative forward guidance. The FOMC dot plot, published quarterly, projected a gradual and limited policy-rate rise through 2017, accompanied by official communication anchoring expectations at low levels. The Fed initiated its first short-rate hiking cycle in December 2015, at a pace of one hike per year through 2017 — far less aggressive than prior historical cycles. The ACMY10 component (cumulative expectations) adjusted upward, but slowly, which left the term premium to absorb part of the gap between observed yield and expectations.

Third force: structural demand for Treasuries as a safe asset and regulatory collateral. Basel III rules progressively imposed between 2013 and 2019 raised bank demand for high-quality assets, with Treasuries as the reference. Defined-benefit pension funds also continued to buy long duration to match actuarial liabilities. This structural demand reduced the free float of available duration, mechanically compressing the compensation demanded by marginal holders. The mechanisms documented in the duration channel from the central balance sheet apply here in mirror: the QE3 stock persistence combined with regulatory demand produces a durable premium compression.

The first Fed QT episode between October 2017 and July 2019 — gradual balance-sheet reduction from 4.5 trillion toward 3.8 trillion — coincided with a slight term-premium recovery toward minus 10 to minus 20 basis points, but without a zero crossing. The January 2019 Powell pivot interrupted the move: the Fed announced a pause in QT, then a complete halt in July 2019. The term premium restabilized around minus 30 basis points.

3. Sub-Period 2 — 2019-2021: Powell Pivot, Covid Shock, Renewed ZIRP

Between January 2019 and early 2020, the term premium remained below zero but in a tightened range, around minus 20 to minus 30 basis points. The market gradually adjusted its expectations to a less restrictive monetary cycle than previously anticipated. The prospect of a durable return to zero was emerging without materializing.

March 2020 flipped the dynamic. The Covid shock triggered a massive flight-to-quality into Treasuries as a global safe asset. The 10-year yield collapsed below 0.55% intraday on March 9, 2020 — an unprecedented historical level. ACMTP10 plunged in the same move: NY Fed backcasted estimates place the floor near minus 1.2% mid-March. The Fed responded with a series of emergency measures: immediate return to unlimited QE purchases on Treasuries and MBS, lowering the policy rate to zero on March 15, deploying liquidity facilities (PDCF, MMLF, PMCCF, SMCCF) under the CARES Act adopted on March 27. The Fed balance sheet jumped from 4.2 trillion in early March 2020 to 7.2 trillion by end-June 2020 per WALCL — the fastest expansion in modern history. Related coverage: the 2020 Covid episode read by the indicators.

The term premium did not immediately close after shock stabilization. Several factors prolonged the negative phase. The FOMC forward guidance adopted in September 2020 (“FAIT” — Flexible Average Inflation Targeting) anchored short-rate expectations at zero “until inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.” The dot plot published through mid-2021 projected a 0.125% policy rate across the entire visible horizon, about three years. QE purchases continued at a pace of 80 billion per month on Treasuries plus 40 billion on Agency MBS, sustaining continuous purchase pressure on duration. The cumulative stock of Fed-held Treasuries grew from about 2.5 trillion in early 2020 to over 5.5 trillion by mid-2022. The wider context: what a positive term premium implies for valuations.

This configuration — zero policy rate, active purchases, dovish forward guidance — constituted the longest unconventional monetary policy phase in Federal Reserve history. The term premium remained durably negative, oscillating between minus 80 and minus 40 basis points between March 2020 and end-2021.

4. Sub-Period 3 — 2022-2024: Hiking Cycle with Premium Still Negative

The exit from the Covid emergency phase began in November 2021 with the tapering announcement, and accelerated sharply against the inflation surge of late 2021 – early 2022. The Fed initiated its hiking cycle on March 16, 2022 with a 25-basis-point hike, then strung eleven hikes through July 2023 — the fastest policy-rate climb in forty years, taking the fed funds target range from 0-0.25% to 5.25-5.50%. QT started in June 2022 at a capped pace of 60 billion Treasuries per month.

Despite this brutal monetary inflection, ACMTP10 remained negative across the entire 2022-2024 period. It rose progressively from the March 2020 floor, crossed back above minus 0.5% in early 2022, then oscillated between minus 0.3% and minus 0.1% between mid-2022 and mid-2024. The 10-year yield nonetheless reached elevated levels: 4.25% in October 2022, 5.00% at the October 23, 2023 intraday peak. But the ACM decomposition attributes these levels primarily to the ACMY10 expectations component — which reflects the ongoing hiking cycle — and not to the term premium.

This apparent divergence has an explanation. The rapid policy-rate climb pushed the ACMY10 component to levels comparable to prior cycles, sufficient to drive the nominal yield upward. But the term premium — residual — responds to different forces: still-high cumulative Fed balance-sheet size (around 8 trillion mid-2022, in slow decline), persistent structural duration demand, foreign holder base in recomposition but not yet fully disengaged. These structural forces, identified by the literature as principal residual determinants, do not invert instantaneously with the policy rate. The empirical detail is laid out in the mechanics of rate decisions.

The durable crossing of zero by the term premium finally occurred in August 2024 — 18 months after the cycle’s last hike of July 2023 and more than two years after QT started. Monetary cycle deceleration, QT persistence, and gradual upward revision of r-star then converged to produce the durable crossing.

5. Exiting the Anomaly in August 2024

The exit from the negative phase was not abrupt but gradual. The six-month moving average of ACMTP10 crossed zero in August 2024 and then settled in positive territory through year-end 2025. The fine trajectory shows oscillations in July-September 2024 around the zero line, then stabilization above from October 2024.

Several FOMC members commented on this exit retrospectively. At the December 13, 2023 FOMC press conference, Jerome Powell first mentioned explicitly that “term premiums have been low for some time and we have seen some adjustment.” The formulation was repeated and refined at the January and March 2024 conferences. John Williams, at a NABE intervention in October 2024, indicated that an upward r-star revision is now consistent with observed data. For the symmetric return to positive, these statements and their implications take over the analytical baton.

Conclusion

Eight consecutive years of negative term premium do not boil down to a simple statistical anomaly. It is a configuration produced by the accumulation of forces — persistent QE3, prolonged ZIRP, amplifying Covid shock, structural demand for Treasuries — that combined over 2016-2024 to durably compress the residual below zero. The exit only came with a combination of inflections: gradual monetary cycle exit, QT persistence, and macroeconomic r-star revision. The term premium is never a mechanical measure of a single driver, which the 2016-2024 phase illustrates retrospectively with clarity. For the corresponding cross-read, see gold demand placed within the U.S. fiscal frame.

Reading a negative term premium as a passing anomaly that naturally corrects within a few months would misunderstand the 2016-2024 phase: the configuration lasted eight years, weathered two major shocks (Covid 2020, inflation 2022-2023), and survived a historic hiking cycle. Normalization is not an automatic mean reversion.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…