CAPE 35-40 in 2024-2026: why the current level joins the third extreme cluster in the history of equity valuation

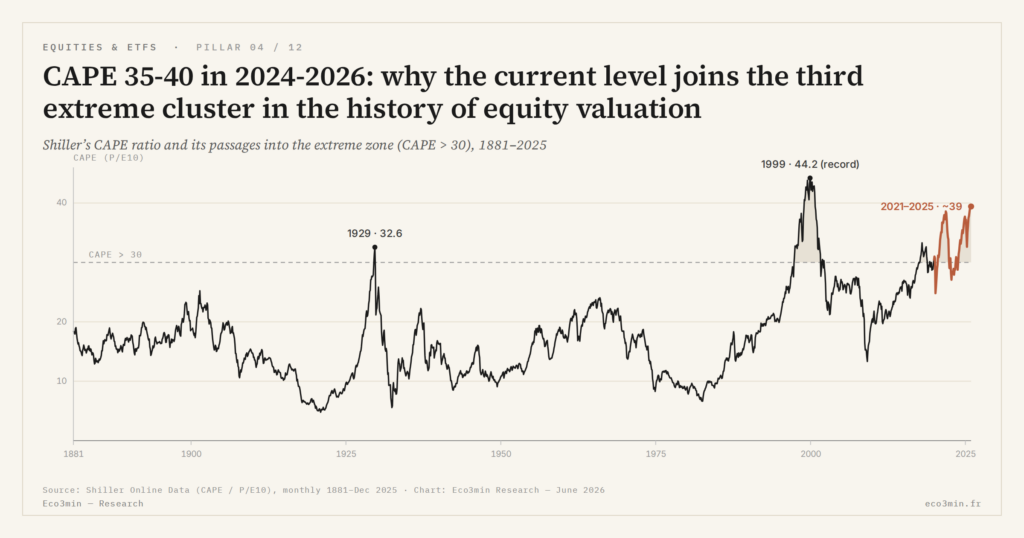

In May 2026, the S&P 500 CAPE oscillates around 35-40 per Shiller Online Data — the ratio’s third durable passage above the 30 threshold in 145 years after 1929 and 1999, in a configuration combining extreme equity valuation and positive real rates.

TL;DR

At CAPE 35-40 in mid-2026, the S&P 500 enters its third extreme-valuation cluster since 1881, splitting analysts between an AI-capex justification and a thin-risk-premium warning of a weak decade.

- Positive real rates near 2.1% place the current peak closer to 1929 (CAPE 32.56) than to 1999 (44.19, real rates near 4%), even as Big Tech concentration now exceeds the 1999 dot-com peak.

- The bull case sees AI productivity lifting forward returns toward the 6-7% post-war norm, while the Shiller and ECY regressions both land near 3-4% real, with neither resolvable before realized 2026-2036 returns.

- Both prior extreme clusters carried the same fundamental-justification narrative (electrification in 1929, internet in 1999), yet sectoral leaders such as RCA and Cisco still corrected sharply after the capex peak.

Two competing theses structure the analysis of this phase by mid-2026 — fundamental justification through Big Tech AI capex versus structural warning on 10-year forward returns — with neither empirically settled.

1. The 2020-2026 CAPE Trajectory

At the March 2020 COVID-shock trough, the S&P 500 CAPE briefly fell to around 24 per Shiller Online Data — an elevated level but outside the extreme zone, due to the rapid price drop combined with decadal real earnings barely affected by the point shock. This anomaly lasted only a few months. By fall 2020, the CAPE was climbing back above 30 under the combined effect of the S&P 500 price rebound (supported by COVID transfers, Fed liquidity and the work-from-home acceleration benefiting Big Tech) and slow erosion of the decadal earnings base, which progressively incorporated the low-earnings 2008-2010 GFC years.

The peak was reached in November 2021 around 38-40 per Shiller Online Data, in a context of maximum Fed liquidity (WALCL balance sheet around $8.7 trillion per FRED) and Big Tech capex already accelerating on cloud infrastructure. The 25% S&P 500 correction in 2022 — combined with the Fed Funds rise from 0-0.25% to 5.25-5.5% per FOMC minutes — briefly brought the CAPE back around 28-30 in late 2022, but the 2023-2024 rebound reinstalled it above 35.

By mid-2026, the CAPE oscillates between 35 and 40 depending on the week, in a range that has not been durably broken downward since summer 2020. The cumulative duration of the extreme-zone passage — now four consecutive years above 30 — is unprecedented in the ratio’s modern history. The 1996-1999 episode had lasted about three years before the terminal peak of December 1999 at 44.19, and all other historical peaks (1929, 1966) had been briefer in the extreme zone. Each of these valuation peaks can be lined up against the present one in the tool that lines up macro regimes moment by moment, which records the conditions that prevailed at each.

This persistence is not an anecdotal statistical curiosity. It qualitatively modifies the analytical debate: while prior extreme peaks were read as temporary anomalies destined to dissolve through correction, the 2021-2026 peak resists this reading. The CAPE reading as regime thermometer must therefore integrate this persistence as new empirical data rather than as an anomaly to be explained away.

2. Comparison with 1929 and 1999

The current peak is statistically comparable to the two historical extreme-zone precedents, but with macroeconomic specificities that modify its interpretation. September 1929: CAPE at 32.56 in a context of sustained economic growth, massive technological emergence (automobiles, electrification, radio, nascent commercial aviation) and broad-based public equity speculation facilitated by margin credit expansion. The real S&P 500 return over 1929-1939 was about −0.5% annual per Shiller-data calculations.

December 1999: CAPE at 44.19, absolute series record. The context combined the emergence of internet as transformative infrastructure, record valuations for companies without earnings (dot-com bubble), a relatively accommodative Greenspan monetary policy after the 1998 LTCM crisis, and massive sectoral concentration of the equity market in technology. The real S&P 500 return over 1999-2009 was about −2.7% annual.

May 2026: CAPE 35-40, in the intermediate zone between 1929 and 1999. The context differs from both precedents on several important dimensions. First, real rates are clearly positive (real DGS10 around 2.1%) — a configuration that resembles 1929 more than 1999 (where real rates ran around 4%). Second, sectoral concentration is extreme — the seven U.S. Big Tech firms represent a historically high share of S&P 500 capitalization per S&P Dow Jones Indices, exceeding the tech concentration at the 1999 dot-com peak. Third, capex invested in AI infrastructure — data centers and dedicated chips — reaches levels comparable to historical transformative investment cycles. A closer look: how the record reframes the timing worry.

These contextual differences produce two competing readings of the present. The historical grid of 145 years of Shiller series documents that both extreme precedents were followed by a decade of weak or negative returns — an empirical observation that constrains but does not determine the 2024-2026 reading.

3. First Thesis — AI Capex Justifies the Multiples

The dominant thesis, defended by a significant share of the sell-side industry, several large asset managers and some academic commentary in 2024-2025, makes Big Tech AI capex the fundamental justification for current multiples. The central argument: cumulative investments by U.S. hyperscalers — Microsoft, Alphabet, Amazon, Meta — in AI-dedicated data centers and chips have reached levels historically comparable to major transformative investment cycles.

The figures are massive. Per the hyperscalers’ quarterly financial communications, aggregate AI capex rose from roughly $150 billion in 2022 to over $350 billion in 2025 estimated, with projections continuing to exceed $400 billion in 2026. This acceleration has limited historical precedent: comparable mega-investment phases — railroads in the 1880s, electrification in the 1920s, telecommunications in the 1990s — produced durable productive transformations that ex post justified the elevated valuations of related assets.

In this reading, the current CAPE 35-40 would be justified by anticipated acceleration of economic productivity and therefore future earnings. If AI effectively produces productivity gains comparable to electricity or internet, forward 10-year earnings of Big Tech (and by extension of an S&P 500 dominated by them) would significantly exceed the Shiller projections based on pre-AI history. The Shiller regression would not be violated — it would simply be applied to a wrong normalized-earnings reference. The chronology of the S&P 500 denominated in gold sets this observation on a secular scale. The comparison of AI capex to historical transformative investments documents the bull case in detail.

This thesis is not absurd but carries several strong hypotheses that must be made explicit. First hypothesis: AI productivity gains will be monetizable to shareholders, not dissipated into consumer benefits or captured by upstream suppliers (Nvidia, TSMC). Second hypothesis: the AI capex return will be achieved over the decadal horizon relevant to the Shiller regression, not over a five- or twenty-year horizon that would refute the projection. Third hypothesis: extreme sectoral concentration will not produce macroeconomic fragility that would degrade consolidated S&P 500 earnings. None of these three hypotheses is demonstrated by mid-2026.

4. Second Thesis — ECY 0.5-0.8% as Structural Warning

The alternative thesis, defended notably by AQR, Vanguard and several academic works published in 2024-2025, treats the current ECY at 0.5-0.8% as a structural warning on 10-year forward returns. The Shiller regression applied to the current CAPE projects a forward 10-year real S&P 500 return of roughly 3 to 4% annual, well below the post-WWII historical average of 6-7% real. This projection is consistent with the ECY regression which produces, through a different analytical construction, a convergent projection.

The central analytical argument: the fundamental justification through AI capex reproduces a pattern already observed in 1929 (justifications via electrification) and 1999 (justifications via internet) — patterns that did not prevent the subsequent decades of weak returns. The argument is not that AI capex lacks value — it manifestly has some — but that its monetization to shareholders over ten years is not mechanically guaranteed by current valuation. The market is “already paying” for this monetization, which reduces the expected return if monetization effectively materializes, and produces negative return if it proves slower or more diluted than expected.

This thesis draws on three historical precedents. First, the 1920s electrification capex effectively transformed U.S. productivity but with an absorption delay stretching over two to three decades after the investment peak — the effect on consolidated S&P 500 earnings became significant only post-WWII. Second, the 1990s internet capex produced durable transformations but a large share of the created value was dissipated into consumer benefits (free search, low-cost communication) rather than captured by shareholders. Third, in both cases, sectoral concentration of the capex peak phases produced severe corrections on sectoral leaders (RCA and other electrification stocks in the 1930s, Cisco and other internet stocks in the 2000s). More on this: our study on how real rates, multiples and earnings shape equity valuation.

For this thesis, the ECY 0.5-0.8% is analytically more informative than the pure CAPE because it integrates real rates — it indicates that the equity risk premium cushion is historically thin, a configuration observed only in the late 1920s and the late 1990s. The construction and use of the Excess CAPE Yield provides the operational framework for this reading, and the empirical real-rates-vs-CAPE relationship furnishes the complete historical audit of the metric.

What ultimately distinguishes the two theses is not the description of the present — both agree that the CAPE sits at extreme levels and that AI capex is unprecedented in magnitude — but the joint prediction they make on the next ten years. The bull case predicts S&P 500 real returns near or above the historical 6-7% average through productivity acceleration. The analysis is carried further in the current macro regime. The warning thesis predicts returns near the Shiller projection of 3-4% real, with explicit residual variance allowing both better and worse outcomes. Resolution will come mechanically from realized returns over 2026-2036, validated against both projections. In the meantime, a rigorous reading of the current phase implies holding both theses simultaneously without privileging one — analytically costly but empirically honest given the available evidence.

Concluding that the CAPE’s “persistence” in the extreme zone since 2020 demonstrates that this time is different is premature. Both historical extreme-zone precedents (1929 and 1999) also experienced multi-year phases in the elevated zone before the turn — 1996-1999 held the CAPE above 30 for three years before the December 1999 terminal peak. Eco3min’s analysis of the Great Depression traces this episode. The current four-year persistence is statistically notable but does not disqualify the Shiller framework or the empirical regression over 1881-2025. Distinguishing a temporary persistence from a structural model break requires a longer observation window than that available by mid-2026 — resolution expected mechanically from realized returns over 2026-2036.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Reading Earnings Surprises: Cash Flow, Margins, Guidance

How to analyze an earnings surprise beyond the simple beat or miss: cash flow, margins, guidance, and weak…

Equal-Weight ETFs: The Quiet Signal Behind Rising Indices

Equal-weight ETFs reveal the true health of the equity market behind mega-cap-driven indices. Their gap with cap-weighted ETFs…

Smart Beta ETFs: The Hidden Risk Behind Factor Performance

Smart beta ETFs now hold ~15-20% of global equity ETF assets. Stacking factor exposures often rebuilds hidden concentration…