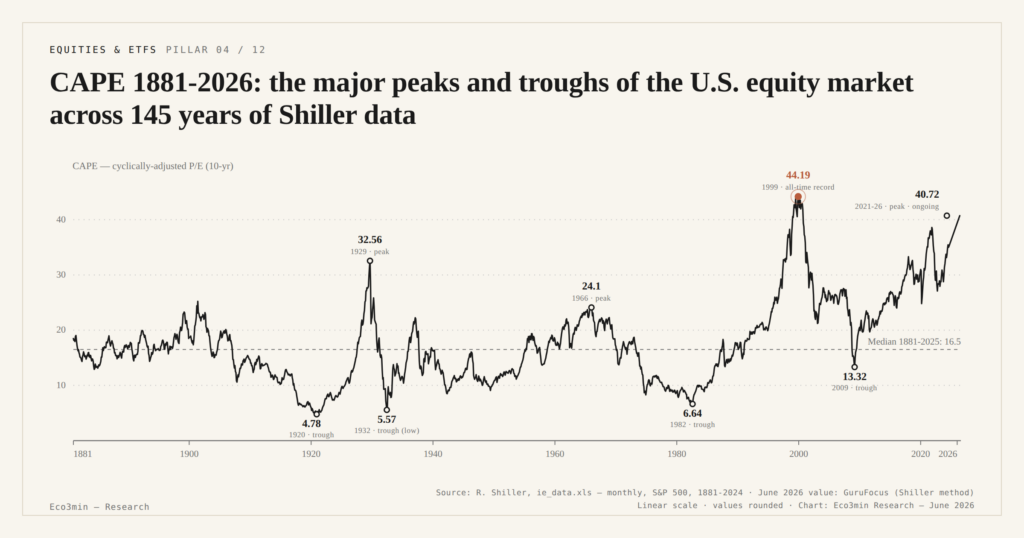

CAPE 1881-2026: the major peaks and troughs of the U.S. equity market across 145 years of Shiller data

Seven inflection points structure the Shiller series since 1881: 1920 trough at 4.78, 1929 peak at 32.56, 1932 Depression trough at 5.57, 1966 peak at 24.1, 1982 Volcker trough at 6.64, 1999 dot-com peak at 44.19 (absolute record), 2009 GFC trough at 13.32 — to which the post-pandemic peak of November 2021 around 38-40, still ongoing in 2026, must be added.

TL;DR

Seven inflection points anchor 145 years of Shiller data, and the pattern is consistent: deep-value troughs preceded strong decades, extreme peaks weak ones. Reading each inflection as a starting level rather than a timing signal has consequences downstream — see holding-period lock-in and sequencing risk.

- The series runs from a 1932 Depression low of 5.57 to the 1999 dot-com record of 44.19, with the 1881-2025 median near 16-17.

- Four deep-value troughs (1920, 1932, 1982, 2009) were each followed by real S&P 500 returns of roughly 8 to 14% annual over the next decade.

- The three extreme peaks (1929, 1966, 1999) preceded decades of −0.5% to −2.7% real annual returns; CAPE 24.1 in 1966 signalled fifteen weak years without an immediate crash.

- Since July 2001, FASB 142's goodwill rule has lifted reported CAPE by an estimated 2 to 4 points (Siegel), putting a corrected current reading near 33-34.

Reconstructing each episode, identifying the macro conditions that produced them, and examining the forward 10-year returns that followed is the empirical reference exercise of the CAPE cluster. The counterpart of this page lives in CAPE explained: methodology and 10-year real earnings average.

1. Historical Troughs — Four Passages in the Deep Value Zone

The Shiller series since 1881 has documented four durable passages through the deep value zone (CAPE below 10), each produced by a major macroeconomic shock. The first is the post-WWI trough of December 1920 at 4.78 per Shiller Online Data. This zone of extremely low valuation is the combined legacy of the 1920-1921 depression — which was not recognized at the time as a major recession and lasted less than two years — and post-war monetary uncertainty. The real S&P 500 return over 1920-1930 was remarkable: around 14% annual per Shiller-data calculations, one of the highest real-return decades in the ratio’s history. A related answer: reading CAPE alongside the forward multiple.

The second trough is that of the Great Depression — June 1932 at 5.57, the absolute series low. This value was reached at the trough of the most severe economic contraction of the 20th century: U.S. GDP down cumulatively about 25% between 1929 and 1933 per back-calculated BEA estimates, unemployment at 25% in 1933. The real S&P 500 return over 1932-1942 was about 8% annual — solid but below the post-WWII expansion decades, due to the double destabilization of the depression then the war.

The third trough is the start of stagflation, August 1982 at 6.64. The context combines the Volcker Fed Funds peak at 19-20% in July 1981 per FOMC minutes, and the economic deterioration produced by forced disinflation — UNRATE at 10.8% in November 1982 per BLS series. The real S&P 500 return over 1982-1992 was about 11% annual, marking the start of the 1982-2000 secular bull market. See our note on stagflation for a fuller treatment.

A fourth deep value passage deserves mention without reaching the strict 10 threshold: March 2009 at 13.32. This GFC trough is less low than the previous three but constitutes the lowest level reached in the post-Bretton Woods era. The real S&P 500 return over 2009-2019 was about 11% annual, comparable to the post-1982 and post-1932 decades. These four empirical troughs produce a statistical regularity: the deep value zone has systematically preceded a decade of solid real returns, which is precisely the CAPE predictive property as documented through the Shiller regression.

2. Historical Peaks — Three Passages in the Extreme Zone

The first peak in the extreme regime is September 1929 at 32.56. This level was reached at the end of the Roaring Twenties decade, in a context of sustained economic growth, massive technological progress (automobiles, electrification, radio) and broad-based public speculation in equities. The Black Tuesday crash of October 29, 1929 and the subsequent collapse produced a negative real S&P 500 return over 1929-1939 — around −0.5% annual per Shiller-data calculations — an empirical ex post validation of the CAPE’s predictive power.

The second peak is the Nifty Fifty peak of January 1966 at 24.1. This peak is lower than the other two but constitutes an interesting case: it preceded not an immediate crash but fifteen years of stagflation and weak real returns. The real S&P 500 return over 1966-1976 was about −0.5% annual, and over 1966-1982 (from peak to Volcker trough) about −1% annual. CAPE 24.1 was not an immediate crash signal; it was a signal of weak decadal forward returns, which validated empirically even without a single sharp correction.

The third peak is the absolute historical record: December 1999 at 44.19. This level, never reached before or after in the series, was produced by the dot-com bubble — record capitalizations for internet companies without earnings, broad optimism on “new economy” productivity. The Nasdaq Composite lost 78% of its value between March 2000 and October 2002 per FRED. The real S&P 500 return over 1999-2009 was about −2.7% annual, worse than the post-1929 decade, marking the “lost decade” for U.S. equities. Eco3min’s catalogue of historical market crises places them on a common timeline.

The fourth ongoing peak is the one that started in November 2021 around 38-40 and remained sustained through May 2026. This persistence is unprecedented in the modern series: no prior peak has held the CAPE in the extreme zone for four consecutive years — the 1996-1999 episode lasted about three years before the terminal peak. The reading of the 2024-2026 regime at CAPE 35-40 covers the competing theses that structure the debate on this persistence.

3. Intermediate Phases — Normal and Elevated Regimes

Between deep value troughs and extreme peaks, the CAPE has spent most of its history in the “normal” (13-20) and “elevated” (20-30) zones. The historical CAPE median over 1881-2025 sits around 16-17 per Shiller-data calculations, placing this normal zone as the statistical dominant of the ratio.

Normal regime phases cover notably the 1950s-1960s decades (sustained post-WWII economic growth, moderate inflation, CAPE oscillating between 11 and 22), the 1980s-1990s before the final dot-com phase (CAPE between 11 and 25 over 1982-1995), and certain post-crisis windows. The real S&P 500 returns over the decades following a CAPE in the normal zone have run around 6 to 8% annual — the standard return zone of U.S. equities, neither the outperformance derived from deep value troughs nor the underperformance derived from extreme peaks.

Elevated regime phases (CAPE 20-30) are historically rarer but documented over extended periods. The mid-to-late 1960s show a CAPE between 20 and 24 — a stable elevated zone before the 1970s degradation. The 2010s post-GFC kept the CAPE between 22 and 30 for almost the entire decade, a historically unprecedented configuration by its duration. The real S&P 500 return over 2010-2020 was about 11% annual — above the historical median, suggesting that the stable elevated zone can produce solid returns provided valuation does not tip into the extreme.

This four-regime typology — deep value, normal, elevated, extreme — is not a theoretical convention but a statistical reading of the historical distribution. It structures the reading of peaks and troughs as well as that of intermediate phases, giving each ratio level an empirical comparative reference rather than a mechanical threshold to respect or cross. The distinction with other valuation measures structures the CAPE’s uniqueness as a regime thermometer.

4. The FASB 142 Break and Pre-Post 2001 Comparability

Any historical reading of the Shiller series must integrate a structural accounting break that occurred in July 2001: the adoption of FASB Statement 142 by the Financial Accounting Standards Board, which modified the accounting treatment of goodwill (acquisition premium) in U.S. listed companies’ accounts. Before 2001, goodwill was amortized over a maximum of forty years, spreading its accounting impact over very long periods. From July 2001, goodwill ceases to be amortized and is subject to annual impairment tests — any depreciation is immediately and fully booked as a charge.

The practical effect on S&P 500 GAAP earnings has been significant: recession phases now produce massive concentrated depreciations, against smoothed amortizations before. Post-2001 GAAP earnings are therefore structurally more volatile, and tend to be depressed relative to pre-break earnings. For the CAPE, which uses GAAP earnings in the denominator, this means post-2001 values are mechanically higher than they would have been under the pre-FASB 142 methodology. Jeremy Siegel and several other critics estimate this effect at 2-4 CAPE points on average over 2001-2025. Related analysis: the Eco3min frame for valuing equities.

This break is a central argument of the CAPE critique, developed notably by Siegel in his 2016 paper “The Shiller CAPE Ratio: A New Look.” The argument: comparing a 2025 CAPE of 36 to a 1929 CAPE of 32.56 overvalues the present relative to the past, because 2025 earnings are depressed by FASB 142 while 1929 earnings were not. A corrected CAPE reading would remove the FASB 142 effect and bring the current CAPE to roughly 33-34 — still in the historical extreme zone but less extreme than the raw value. Where the current reading falls relative to the 1929 and 1999 extremes is laid out in the macro-regime comparator, which juxtaposes two historical states and the data each carried. A related angle on real equity valuation is available in real equity valuation stripped of fiat money.

Shiller responded to this critique without fully conceding. His argument: the FASB 142 effect is real but marginal, and the empirical predictive property of the CAPE over 1881-2025 remains statistically robust including over the post-2001 sub-period. Shiller regressions over 2001-2015 vs 1881-2000 produce similar coefficients, suggesting the accounting break has not significantly modified the ratio’s predictive power. The complete methodological critique of the CAPE by Siegel and the Shiller response cover this debate in detail.

- Seven inflection points structure the Shiller series: 1920 trough (4.78), 1929 peak (32.56), 1932 trough (5.57 — absolute low), 1966 peak (24.1), 1982 trough (6.64), 1999 peak (44.19 — absolute record), 2009 trough (13.32), plus the ongoing 2021 post-pandemic peak.

- The four deep value troughs have systematically preceded decades of solid real returns (8-14% annual over 10 years); the three extreme peaks have preceded decades of weak or negative real returns (−0.5% to −2.7% annual).

- The historical CAPE median over 1881-2025 sits around 16-17 — the normal regime (13-20) is the statistical dominant of the ratio, covering the 1950s-1960s and 1980s-1990s decades.

- The July 2001 FASB 142 break on goodwill treatment structurally modifies post-2001 GAAP earnings and constitutes the central debate on pre-post comparability in the historical series — a documented controversy between Jeremy Siegel and Shiller.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Reading Earnings Surprises: Cash Flow, Margins, Guidance

How to analyze an earnings surprise beyond the simple beat or miss: cash flow, margins, guidance, and weak…

Equal-Weight ETFs: The Quiet Signal Behind Rising Indices

Equal-weight ETFs reveal the true health of the equity market behind mega-cap-driven indices. Their gap with cap-weighted ETFs…

Smart Beta ETFs: The Hidden Risk Behind Factor Performance

Smart beta ETFs now hold ~15-20% of global equity ETF assets. Stacking factor exposures often rebuilds hidden concentration…