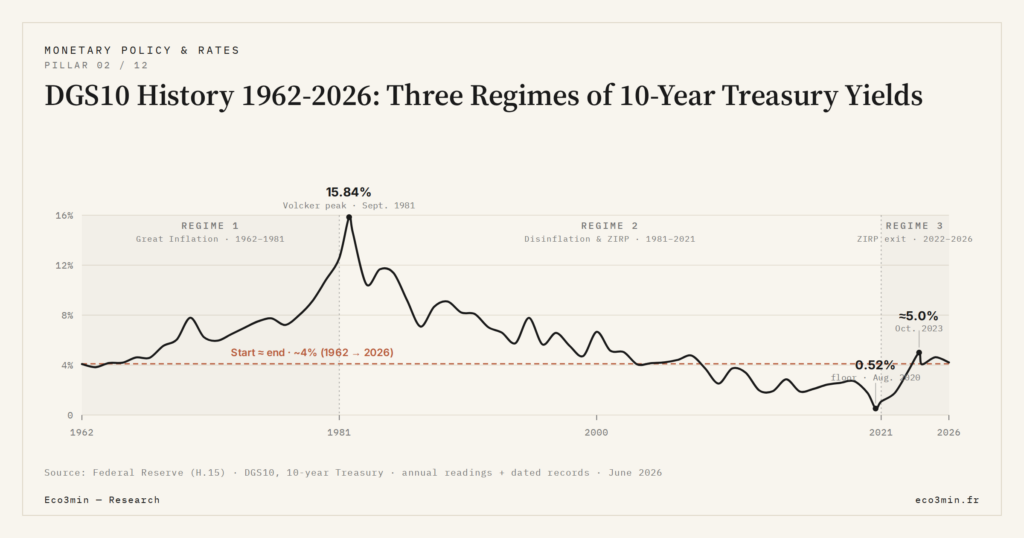

DGS10 History 1962-2026: Three Regimes of 10-Year Treasury Yields

The FRED DGS10 series starts in January 1962 at 4.11% and stands in May 2026 around 4.2%. This near-perfect return masks three successive monetary regimes with radically different drivers and amplitudes.

TL;DR

The 10-year's 6% average since 1962 is a statistical mirage: it blends an 8.5% Great Inflation, a 5.8% disinflation era, and a 4.1% post-2022 regime that share no common driver.

- Regime 1, the Great Inflation (1962-1981): DGS10 climbs from 4% to a 15.84% peak in September 1981, when Volcker pushed the Fed Funds Rate above 19%; over 1973-1980 the average ex-post real yield was about -1.8%.

- Regime 2, disinflation and ZIRP (1981-2021): a 40-year bond bull market drives the yield to a 0.51% COVID floor in August 2020, with QE pushing the ACM term premium to -100 bps in March 2020.

- Regime 3, ZIRP exit (since 2022): +350 bps in under two years (1.51% end-2021 to 5.0% in October 2023), alongside an r-star the NY Fed revised to 0.9-1.1% in June 2024, up from 0.4% in 2019.

- Foreign official holdings rose from roughly 5% of marketable Treasury debt in 1980 to nearly 40% in 2014, compressing yields below domestic-only levels and helping explain the Greenspan conundrum; that captive bid has since faded.

Identifying the regime in force is not a historian’s affectation: it is the precondition for applying the right reading grid to a 10-year yield whose determinants shift over time.

1. Three regimes across 64 years of series

Over the 1962-2026 horizon, DGS10 traces three qualitatively distinct trajectories. The Great Inflation 1962-1981 sees a structural rise from 4.1% to 15.84% in September 1981, the absolute peak of the series during the Volcker tightening. The disinflation and ZIRP 1981-2021 describe a long bond bull market that brings the yield down to 0.51% in August 2020, the COVID floor. The post-2022 ZIRP exit produces a brutal repricing toward 5.0% in October 2023, then a stabilization around 4.2% in 2025-2026. A related perspective: the anatomy of the disinflationary regime.

Each regime corresponds to different macroeconomic drivers. The first is dominated by inflation expectation drift and the Fed’s initial inability to anchor them. The second is carried by Volcker-Greenspan disinflation, globalization, then post-2008 monetary repression. The third combines a re-estimation of the natural interest rate, fiscal risk reintroduction, and a positive term premium. This regime identification structures DGS10 as a structural macro variable in contemporary fixed income analysis.

2. Regime 1 — The Great Inflation, 1962-1981

Regime 1 opens in an economy where CPI inflation is still near 1% and DGS10 oscillates between 4 and 4.5%. The rupture comes in the late 1960s with the Vietnam military escalation, widening federal deficits, and the end of the Bretton Woods system in 1971 that officially detached the dollar from gold. The oil shocks of 1973 and 1979 accelerate the inflationary drift: annual CPI climbs to 11% in 1974, falls briefly, then rises again toward 13-14% in 1979-1980.

DGS10 follows the inflation dynamic with variable delay and amplitude. From 4% in 1965, it reaches 8% in 1973, 10% in 1979, and explodes to 15.84% in September 1981 when Paul Volcker, Fed chairman, takes the Fed Funds Rate above 19% to break inflation expectations. Across this entire regime, the DGS10 beta to CPI surprises was particularly elevated: one point of inflation surprise translated into 30 to 50 bps of DGS10 rise within weeks.

The DGS10/DGS2 slope was predominantly flat or inverted over 1979-1981, the classic signal of an active monetary fight against inflation. The exit from this regime occurred gradually between 1982 and 1984, as Volcker’s anti-inflation credibility was established and 10-year inflation expectations, though not directly measurable at the time, began to re-anchor.

A specific feature of regime 1 is the growing gap between DGS10 and realized inflation: while in a stable regime holders demand positive compensation for expected inflation, Treasury holders in 1973-1980 regularly accepted negative ex-post real yields. The average ex-post real yield over 1973-1980 was about -1.8%, a configuration explained by the combination of captive institutions (banks, regulated pension funds) required to hold Treasuries and degraded Fed credibility. It is this involuntary repression that implicitly transferred wealth from creditors to the U.S. Treasury during regime 1. This is treated at length in the reach of the 10-year benchmark rate. More context: The copper/gold ratio set against the recession signal.

3. Regime 2 — Disinflation and ZIRP, 1981-2021

Regime 2 is the textbook long bond bull market. DGS10 falls from 15.84% in September 1981 to 5.3% in 2007, then to 0.51% in August 2020. Forty years of secular decline, punctuated by a few cyclical rebounds (1994, 2000, 2007, 2013, 2018) that never reversed the underlying trend. The underlying drivers are Volcker-Greenspan disinflation, the globalization of value chains compressing unit costs, favorable demographics (massive baby-boomer entry into retirement savings), and the post-1995 technological revolution that boosted productivity.

Within regime 2, two sub-periods deserve distinction. The 1981-2008 period is marked by a moderate DGS10/Fed Funds beta (around 0.5) and a positive term premium (around 100-200 bps). The 2008-2021 period is dominated by the successive QE programs (QE1, QE2, QE3, then COVID QE in 2020) that push the term premium into negative territory (-100 bps in March 2020 on the ACM decomposition). This monetary repression is the distinctive feature of the 2008-2021 sub-regime and explains the abnormally low DGS10 floor.

Four structuring episodes punctuate regime 2. The Greenspan “conundrum” 2004-2006 sees the Fed raise Fed Funds from 1.0% to 5.25% without DGS10 following proportionally — it rises only from 4.1% to 5.2%, an apparent beta around 0.3. The 2013 taper tantrum sees DGS10 jump from 1.66% to 2.98% in four months after Bernanke mentioned a forthcoming normalization. The 2015-2018 mini-cycle brings DGS10 from 1.7% to 3.2% before the late-2018 pivot. The 2020 COVID shock plunges DGS10 to its historical floor of 0.51% in August. All these dynamics are analyzed in the DGS10/Fed Funds configurations by regime that detail the transmission mechanics.

4. Regime 3 — ZIRP exit, 2022-2026

Regime 3 opens brutally in 2022 with the fastest DGS10 rise since the late 1970s. From 1.51% in December 2021, the yield reaches 4.25% in October 2022, then 5.0% in October 2023, a +350 bps move in less than two years. The stabilization around 4.2% in 2025-2026 does not bring DGS10 back to 2010-2021 levels: the regime is durably different.

Three factors identify regime 3 as qualitatively distinct from previous tightening cycles. First factor: the re-estimation of the natural interest rate (r-star). The Holston-Laubach-Williams model revised in June 2024 by the NY Fed places r-star around 0.9-1.1% in Q4 2024, against 0.4% in 2019. This 60 bps revision modifies the DGS10 theoretical equilibrium permanently. Second factor: the reintroduction of fiscal risk, with a U.S. deficit around 6.5% of GDP and debt-to-GDP at 120%, configurations that impose a higher term premium. Third factor: the return of the ACM term premium to positive territory (+60 bps end-2023), which makes Fed Funds to DGS10 transmission more unstable. A broader view: an unpacking of the public-debt-and-gold pair.

The September-October 2023 episode is the emblematic marker of regime 3. DGS10 moves from 3.8% to 5.0% in six weeks even as Fed Funds futures were already pricing cuts for 2024. The repricing is 80% driven by the real leg (DFII10 +100 bps) and 20% by the breakeven (+20 bps), with a substantial contribution from the term premium that rebuilds by about +50 bps. This configuration — long yield rising independently of expected Fed Funds — had not been observed since regime 1.

The May 2026 configuration, with a DGS10 stable around 4.2%, masks a more complex underlying dynamic. The inflation breakeven T10YIE stands around 2.25-2.30%, close to the Fed target after CPI/PCE translation. DFII10 oscillates around 1.95-2.00%, the highest level since 2009 outside the 2023 episode. The ACM term premium remains positive around +30 to +40 bps. This combination — normalized real rate, anchored breakeven, positive term premium — describes a coherent equilibrium but one structurally different from what prevailed before 2022. Holders of long bond portfolios built on 2010-2021 assumptions saw their duration risk materialize in proportions unprecedented for forty years.

The DGS10 measurement method remains identical across the three regimes — it is the Constant Maturity method explained that guarantees comparability of a continuous 64-year series. What changes are the underlying macroeconomic drivers and therefore the DGS10 elasticity to the usual explanatory variables.

A worthwhile observation across regimes is the role of foreign Treasury demand in shaping each era’s DGS10 dynamics. Regime 2 saw the structural rise of foreign official holdings, from roughly 5% of marketable Treasury debt in 1980 to nearly 40% in 2014 at the peak of Asian central bank accumulation. This foreign bid compressed yields well below domestic-only equilibrium levels and helps explain the Greenspan conundrum mechanically. Regime 3, by contrast, has seen foreign official holdings stagnate or decline as a percentage share, while private foreign holdings (notably Japanese life insurers and European pension funds) have become more rate-sensitive. The composition of marginal Treasury demand is now closer to private domestic and price-elastic foreign than to captive foreign accumulation — a structural shift that contributes to higher equilibrium term premia.

5. Differentiation versus extreme duration cycles

Identifying DGS10 regimes does not dispense with examining other Treasury curve segments. The 30-year (DGS30) follows a related historical trajectory but with different amplitudes, notably on total returns for very-long-duration holders. The 2020-2024 repricing produced nominal price losses on some 30-year zero-coupons exceeding 60%, a phenomenon analyzed in the 30Y duration crash. This 30-year dynamic amplifies what was observed on DGS10 but fits within the same regime sequence.

The DGS10/DGS3M slope, measured by the T10Y3M spread, provides another angle of historical reading. The historical curve inversions (1973, 1980, 1989, 2000, 2007, 2019-2020, 2022-2024) typically precede NBER recessions, but their signal robustness shifts by regime: highly reliable in regime 2, more ambiguous on the 1979-1981 and 2022-2024 transitions.

The regime-based DGS10 analysis also illuminates the regimes of monetary transmission to corporate balance sheets. Regime 1 transmitted inflation to nominal yields via rapid expectation revisions. Regime 2 transmitted Fed Funds via a relatively stable curve and a reduced term premium. Regime 3 transmits a combination of real factors, expectations and term premium, which makes yield forecasting models calibrated on 2010-2021 systematically biased since 2022.

Comparing the current DGS10 to its long-term historical mean (about 6% over 1962-2026) to conclude it is “still low.” This mean aggregates three incommensurable regimes. The Great Inflation 1962-1981 averages 8.5%, the disinflation and ZIRP 1981-2021 averages 5.8%, and the ZIRP exit 2022-2026 averages 4.1%. Comparing today’s DGS10 to the global mean is comparing a 2026 economy to a mean dominated by macroeconomic configurations that no longer exist.

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Rates: The True Cost of Capital Is Repricing

Why real rates are reasserting themselves as markets' anchor and how to recalibrate investment and financing decisions facing…

Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…