DGS10: 10-Year Treasury Yield as a Macro Signal and Financing Benchmark

DGS10, the Fed’s daily Constant Maturity series, is the nominal 10-year Treasury yield that anchors all long-term pricing in the U.S. economy: mortgages, corporate bonds, equity discount rates, fiscal sustainability.

TL;DR

DGS10, the Fed's daily 10-year Constant Maturity yield, anchors US mortgages, corporate spreads and equity discount rates; its post-2022 climb to 4-5% repriced the natural rate, fiscal risk and transmission.

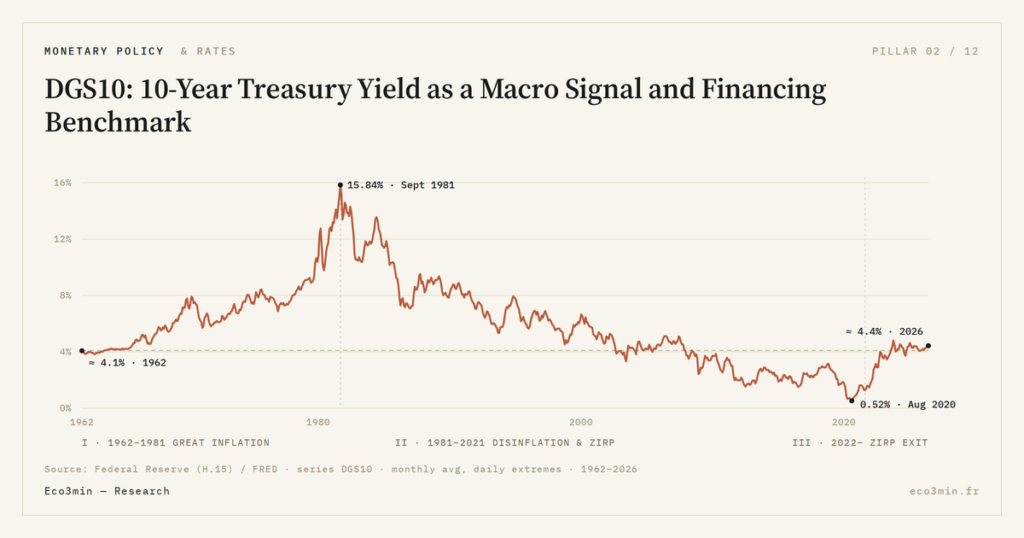

- Built from an interpolated Treasury curve since January 1962, the 64-year series ran from 4.11% to a 15.84% Volcker peak in September 1981, a 0.51% trough in August 2020 and 5.0% in October 2023, returning near 4.2% in May 2026 across three distinct regimes.

- As the standard discount-rate proxy, a 270 bps rise (1.55% to 4.25%) from November 2021 to October 2022 accounts, via a 12-15 year-duration DCF, for nearly all the Nasdaq 100's 30%-plus derating while basket earnings fell only 5-8%.

- The 30-year mortgage tracks DGS10 plus 150-200 bps and hit 7.79% (Freddie Mac PMMS) at the October 2023 peak of 5.0%; existing-home sales later fell to a 3.8 million annualized rate, the lowest since 1995.

- Higher equilibrium underpins the move: Holston-Laubach-Williams estimates lift r-star from 0.4% in 2019 to roughly 0.9-1.1% by Q4 2024, while the ACM term premium turned positive at +60 bps by end-2023.

After a decade of ZIRP, the post-2022 exit returned DGS10 to a 4-5% range that simultaneously repriced the natural rate of interest, the U.S. fiscal risk premium, and the mechanics of monetary transmission.

1. DGS10: what the FRED series actually measures

When FRED displays DGS10 = 4.32% on a Tuesday morning, this number is not the yield of a specific Treasury bond with an identifiable CUSIP. It is the yield of a hypothetical bond with exactly 10 years of residual maturity, reconstructed each business day by the Federal Reserve from an interpolated curve of outstanding Treasuries. The method, known as Constant Maturity Treasury (CMT), has been published in the H.15 Selected Interest Rates release since 1962, giving 64 years of continuous daily history. This construction matters for macroeconomic analysis because no actual bond has a constant residual maturity over time: its remaining life shrinks each day, which would make raw yield series non-comparable from one year to the next. On the same question: what the 10-year Treasury yield drives.

The Treasury Department’s algorithm uses a quasi-cubic spline calibrated on on-the-run Treasuries at the main pillar maturities (1M, 3M, 6M, 1Y, 2Y, 3Y, 5Y, 7Y, 10Y, 20Y, 30Y). The Fed smooths on-the-run versus off-the-run spreads, so the CMT yield is effectively a weighted average of points on the interpolated curve at the exact 10-year tenor. The current methodology dates from a 1980 revision that replaced the older linear regression approach with cubic splining. A second revision in 2005 refined the treatment of pivot points around the 1Y, 5Y and 30Y tenors. For the full methodological detail, see the Constant Maturity calculation method.

This technical plumbing has direct consequences for macro analysts: DGS10 smooths certain market tensions. The Treasury illiquidity episodes of March 2020 and October 2023, when the on-the-run 10Y diverged materially from the off-the-run, only partially appeared in DGS10. In March 2020, the on-the-run versus off-the-run 10Y spread reached almost 25 bps before the Fed intervention of 15 March 2020, but the published DGS10 reflected only 8 to 10 bps of that stress. Capturing these tensions requires cross-referencing DGS10 with other indicators: Bloomberg US Government Securities Liquidity Index, MOVE Index, auction tail spreads, and dealer take-up as a share of primary allocations.

The series begins in January 1962 at 4.11%. Sixty-four years later, in May 2026, it stands near 4.2%. This near-perfect return to the starting point conceals three radically different macroeconomic regimes that three yield regimes since 1962 detail: the Great Inflation of 1962-1981 (a structural rise to 15.84% in September 1981, the absolute peak of the series during the Volcker tightening), disinflation and ZIRP from 1981 to 2021 (a long bond bull market down to the 0.51% trough of August 2020), and the post-2022 ZIRP exit (the brutal repricing to 5.0% in October 2023).

Several adjacent Treasury series deserve clear distinction from DGS10. DGS10 denotes the nominal 10-year. DFII10 (Daily Treasury Inflation-Indexed 10-Year) is the ex-ante real yield on the 10-year TIPS, available since January 2003. T10YIE (Treasury 10-Year Inflation Expectations) is the breakeven inflation computed as DGS10 minus DFII10, measuring average expected annualized inflation over the coming decade. DGS3M is the 3-month CMT yield, the standard short-rate reference; DGS2 and DGS30 denote the 2-year and 30-year respectively. All these yields follow the same CMT methodology and are published simultaneously in the H.15 release. The full DGS10 daily series is available in the FRED DGS10 daily dataset with download and methodology notes. For context: the relationship between copper-gold and the term premium.

The DGS10 series interacts with the broader Treasury issuance calendar in ways the daily series does not fully capture. Refunding announcements published quarterly by the Treasury, which detail upcoming coupon and bill issuance volumes, regularly produce DGS10 moves of 5 to 15 bps on the publication day alone. The October 2023 refunding announcement, which increased long-end issuance more than expected, contributed an estimated 10-15 bps to the cumulative DGS10 rise that month. Reading DGS10 in isolation from the Treasury issuance calendar therefore misses an important driver, particularly in periods of large supply uncertainty. Worth reading alongside: Gold and the fiscal dimension of the U.S. monetary regime.

2. The four functions of DGS10 in the real economy

DGS10 is not tracked for its own sake: its centrality comes from its transmission into real variables. Four channels dominate and structure U.S. macroeconomic analysis.

2.1 Reference discount rate for long-term valuations

Every valuation built from discounted future cash flows — corporate DCF models, real estate pricing, infrastructure project appraisal, pension sustainability analysis, long-dated derivative pricing — uses a discount rate. DGS10 serves as the standard proxy for the 10-year risk-free rate in nearly every U.S. financial model. When DGS10 moved from 1.5% in August 2020 to 5.0% in October 2023, the terminal value of a growth company projecting 4% perpetual growth saw its Gordon-Shapiro multiplier fall by more than a factor of four, mechanically compressing the present value of far-dated cash flows. A related read: Eco3min’s mapping of the policy-to-profits channel.

That move accounts mechanically for a substantial share of the growth sector derating observed in 2022-2023, independent of operating fundamentals. The Nasdaq 100 corrected by more than 30% between November 2021 and October 2022, while aggregate earnings of the basket contracted only 5 to 8%. Over the same window, DGS10 rose from 1.55% to 4.25%, a 270 bps move. A straightforward DCF application, using a 12 to 15-year average cash-flow duration for the tech basket, accounts for essentially all of the observed derating.

The valuation-DGS10 elasticity is not uniform: long-duration sectors (unprofitable tech, early-stage biotech, growth REITs) are far more sensitive than short cash-flow sectors (consumer staples, banks, cyclical energy). The CAPE ratio relative to DGS10, sometimes called the yield gap or excess CAPE yield, historically follows a negative correlation: as DGS10 rises, the sustainable CAPE compresses. Our Q&A on duration and rate sensitivity sets out how this works. This mechanism is documented in Robert Shiller’s work since the 1980s (Yale ICF working papers, annual CAPE and yields dataset). The 1962-2024 correlation between DGS10 and the inverse CAPE (earnings yield) is roughly 0.55 on rolling decade averages.

The discount rate channel extends beyond listed equities. It also structures private equity, venture capital, and commercial real estate pricing. U.S. PE funds typically value portfolio companies on cash-flow or EBITDA multiples whose equilibrium level tracks the inverse of DGS10. The 2022-2024 repricing contributed to a durable compression of acquisition multiples by roughly 1.5 to 2.5 EBITDA turns in the U.S. mid-market, according to Bain Capital Private Equity reports from 2024.

2.2 Anchor for mortgage rates and corporate bond yields

In the United States, the 30-year fixed mortgage rate is indexed on DGS10 through Fannie Mae and Freddie Mac MBS. The empirical rule observed by Freddie Mac since 1990 is straightforward: 30Y mortgage rate ~ DGS10 + 150 to 200 bps of spread, with the spread varying according to servicer financing conditions and MBS liquidity. In October 2023, when DGS10 peaked at 5.0%, the 30Y mortgage rate reached 7.79% (Freddie Mac PMMS, week of 26 October 2023), a 279 bps spread — historically elevated, reflecting MBS market stress following the regional bank failures and the Fed’s exit as a structural MBS buyer.

The mortgage-DGS10 elasticity has direct consequences for the U.S. housing market. Over the 24 months following the October 2023 DGS10 peak, existing home sales (NAR) dropped to an annualized 3.8 million, the lowest level since 1995. The share of homeowners locked in by mortgage rates below 4% reached 60% of the stock by end-2024, creating a structural blockage in housing turnover (Federal Housing Finance Agency, 2024). Monetary transmission to corporate earnings deconstructs the upstream channel.

In the corporate bond market, DGS10 functions as a benchmark on top of which credit spreads are added, calibrated to issuer ratings. An A-rated investment grade 10-year typically trades at DGS10 + 80 to 150 bps. A BB single-B high yield trades at DGS10 + 300 to 700 bps. The DGS10 rise between 2022 and 2023 mechanically lifted corporate yields by more than 250 bps on IG and 350 bps on HY, with no underlying deterioration of issuer fundamentals.

This repricing had a direct impact on average corporate issuance maturities. Over 2022-2024, U.S. corporates shortened their average issuance maturity from 12 years (2015-2021 average) to 7-8 years, preferring to wait for long-end normalization rather than locking high coupons on long maturities. This strategy reduces stock duration but exposes corporates to a refinancing wall concentrated in 2026-2029, particularly acute in the BBB and BB tiers.

The corporate refinancing wall is concentrated in specific industry segments. Real estate investment trusts (REITs), particularly office and retail subsectors, carry mortgage debt structures highly sensitive to DGS10 levels. Leveraged buyout debt from the 2019-2021 vintage, typically priced at floating rates with caps, is rolling into a higher rate environment with limited natural hedging capacity. Telecom and media issuers, which used 10+ year tenors heavily during the ZIRP era, face refinancing decisions at substantially higher coupons. The aggregate maturity wall for U.S. corporates over 2026-2029 is estimated at $2.5 to $3 trillion, with roughly 20% rated BB or below.

2.3 Primary input of financial conditions indices

The three most-followed financial conditions indices (FCIs) incorporate DGS10 as a key variable: the Goldman Sachs FCI assigns it a weight of roughly 20-25% depending on internal calibration, the Chicago Fed NFCI weights it through the risk sub-component, and the Bloomberg US FCI includes it in the rates bloc. When DGS10 rises by 100 bps holding other variables constant, FCIs typically tighten by 0.3 to 0.5 standard deviations, empirically translating into a 30 to 60 bps annualized reduction in U.S. quarterly growth over 2 to 4 quarters, according to estimates from the San Francisco Fed (Economic Letter, 2019).

DGS10 enters FCIs both as a price (yield level) and as a volatility (via the MOVE Index, which measures implied volatility on Treasury options). A DGS10 rise paired with a MOVE spike — the configuration observed in October 2023 and April 2025 — tightens financial conditions doubly. MOVE touched 199 on 21 March 2023 (post-SVB), close to its 217 peak reached in October 2008, signaling major pricing stress along the Treasury curve.

The incorporation of DGS10 in FCIs has direct implications for Fed reaction. When long yields tighten autonomously, the FOMC can slow the pace of Fed Funds hikes because the market is already doing part of the work. The long-end tightening of September-October 2023 was explicitly cited by Jerome Powell as contributing to the Fed Funds pause decided at the 1 November 2023 FOMC. This substitution logic between Fed Funds and long yields is a transmission mechanism in its own right, distinct from the direct policy-rate-to-short-rate channel.

2.4 Signal of long-term expectations

DGS10 embeds forward-looking information on a 10-year horizon in two additive components: the expected path of the Fed Funds Rate over the coming decade, and a term premium that compensates holders for uncertainty around that path. The Fed publishes the Adrian-Crump-Moench (ACM) term premium decomposition daily, accessible from the Federal Reserve Bank of New York website. See our term-premium data series for the underlying data. Over 2010-2021, the 10-year ACM term premium fluctuated between -100 bps and +50 bps, reflecting the negative premium imposed by Treasury demand during QE programs. Since 2022, the term premium component has returned to positive territory, reaching +60 bps by end-2023.

DGS10 also contains a decomposition between real yield (captured by DFII10, the 10-year TIPS yield) and inflation expectations (captured by the T10YIE breakeven, defined as DGS10 minus DFII10). This identity makes it possible to empirically settle between two opposing readings of the same DGS10 move. The method is detailed in how to decompose nominal into real and expectations.

The forward-looking information embedded in DGS10 exceeds the information contained in current Fed Funds. For that reason, the market closely monitors long-yield surprises: a +20 bps move on DGS10 following an FOMC suggests a repricing of the entire Fed path well beyond the immediate decision. Conversely, a stable DGS10 in response to an unexpected Fed Funds decision indicates that markets view the surprise as transient, reducing the expected macroeconomic impact.

3. Reading the current phase: why 2022-2026 is not a classical cycle

Over 64 years of history, DGS10 has gone through many rising phases. The post-2022 repricing (0.51% in August 2020, 5.00% in October 2023, 4.2% in May 2026) at first glance resembles a classical hiking cycle. Three quantitative elements nonetheless make it qualitatively different from the 1994, 1999-2000, 2003-2007 and 2015-2018 cycles.

3.1 The repricing of the natural rate of interest (r-star)

The natural rate of interest, or r-star (r*), is the real equilibrium rate that maintains the economy at full employment with stable inflation. Laubach-Williams model estimates, maintained by the Federal Reserve Bank of New York, put r-star at 0.4% in 2019, pre-COVID. Recent estimates from the revised Holston-Laubach-Williams model (published June 2024 by the NY Fed) place it around 0.9% to 1.1% in Q4 2024, about 60 bps higher than pre-pandemic.

This revision affects DGS10 directly. If r-star = 1% and inflation target = 2%, the theoretical DGS10 equilibrium is around 3% + term premium. With a term premium near 50 bps, the theoretical equilibrium is 3.5%. A DGS10 at 4.2% in May 2026 implies either a higher term premium, a still-underestimated r-star, or inflation expectations above 2% — three readings the TIPS/breakeven decomposition allows to discriminate.

Several factors have pushed r-star estimates higher. U.S. demographics show a slowdown in aging expected after 2030, reducing downward pressure on net savings. Investments in artificial intelligence, semiconductors and decarbonized energy create structurally stronger demand for savings than in the 2010s. Post-COVID reshoring and U.S. industrial policies (CHIPS Act, IRA) raise the marginal cost of capital. The combination of these factors justifies a higher r-star than the 2010s decade, which transmits mechanically to the DGS10 equilibrium.

The empirical identification of r-star carries substantial uncertainty bands. The 95% confidence interval around the Holston-Laubach-Williams point estimate is typically +/- 100 bps, meaning a published estimate of 1.0% could be consistent with true values ranging from 0% to 2%. This statistical uncertainty propagates to any DGS10 equilibrium calculation built on r-star. The practical implication is that no single point estimate of equilibrium DGS10 should be treated as a precise benchmark — a fan of plausible equilibrium values is more honest, and the question becomes whether observed DGS10 sits inside or outside this fan.

3.2 The renewed weight of fiscal risk

The U.S. federal deficit stands around 6.5% of GDP for fiscal year 2024 (Congressional Budget Office, August 2024), against a 3.5% average over 2010-2019. Public federal debt to GDP reaches roughly 120% in Q1 2026, up from 90% in 2019. This configuration forces the Treasury Department to refinance a meaningful share of the stock each year (roughly 30% on a rolling annual basis per the Treasury Borrowing Advisory Committee, November 2025), on top of the primary deficit.

The marginal buyers of Treasuries have changed. Foreign central banks, which held 30% of U.S. federal debt in 2014, now hold only 22% as of end-2025 (TIC data, Treasury). The Fed, which expanded its balance sheet to $9 trillion in 2022, has begun a quantitative tightening that structurally removes demand. Regional banks pulled back from the Treasury market after the SVB crisis of March 2023. The market had to find new marginal buyers — money market funds, basis-trading hedge funds, retail investors — who demand a higher term premium. The supply pressure of Treasury issuance on yields documents this mechanism.

This reintroduction of fiscal risk into DGS10 pricing has a historical precedent: the 1976-1981 period and, to a lesser extent, 1992-1994 saw a visible fiscal premium develop in the long U.S. curve. The 2022-2026 phase, situated within the broader context of monetary regimes and interest rates, shares three characteristics with these precedents: a structural deficit above 5% of GDP, political difficulty in passing bipartisan fiscal compressions, and increased media attention to long-term CBO trajectories. It differs by the magnitude of debt-to-GDP (a historical peacetime level) and by the absence of an inflationary relay to erode the real value of the stock — 2026 inflation hovering near 2.5% versus 8-9% in 1978-1980.

3.3 The rare configuration of DGS10 < Fed Funds

In May 2026, DGS10 stands around 4.2% while the Fed Funds Rate target remains at 4.25-4.50%. This configuration, where the 10-year yield sits below the policy rate, is statistically rare: across 64 years of series, it has been observed in only five episodes (1979-1980, 1989, 2000, 2006-2007, 2022-2024, and again since end-2024). Four of the five precedents were followed by a recession within 12 to 24 months.

The current episode nonetheless stands out by its duration and dis-inversion context: the T10Y3M spread flipped into positive territory in August 2024 after 26 months of inversion, but the DGS10/DFF spread remains slightly negative. This mixed configuration is also legible against why the 4% threshold reset the regime. It — short-end slope normalized, long-end residually flat — challenges recession-signal models and is analyzed in the 10y / 3m spread as recession signal.

The strictest reading of the five historical DGS10 < Fed Funds episodes gives a median 17-month delay between the crossing and the official NBER recession start. But this statistic rests on five observations only and remains statistically fragile. More importantly, contexts differ sharply: 1979 was dominated by Volcker’s fight against inflation, 2000 by the dot-com bubble unwind, 2006-2007 by the pre-subprime crisis. The 2024-2026 configuration does not replicate any of these contexts identically, calling for caution in mechanically extrapolating the signal.

3.4 Comparison with previous DGS10 hiking cycles

Comparing the 2022-2026 repricing with three documented hiking cycles helps isolate what makes it distinct. The 1994 cycle, when DGS10 moved from 5.8% to 8.0% within 12 months after the surprise tightening under Greenspan, was dominated by the repricing of Fed Funds expectations. Term premium remained stable around 100 bps, and the real component (measured ex post via TIPS, which did not yet exist) explained only a modest fraction of the move. Consequence: normalization was rapid, DGS10 falling back below 6% by 1996.

The 2003-2007 cycle, which saw DGS10 move from 3.1% to 5.3%, accompanied a Fed Funds cycle (1.0% to 5.25%) without notable term premium repricing, which remained between 0 and 100 bps. This is what Greenspan called the conundrum in his February 2005 Congressional testimony: the long end was not rising in proportion to the Fed tightening. The ex-post explanation — structural demand from Asian central banks recycling trade surpluses into Treasuries — was only fully understood after 2008.

The more recent 2015-2018 cycle saw DGS10 move from 1.7% to 3.2%. Term premium remained in negative territory through most of the cycle. The move was almost entirely driven by the Fed Funds expectations leg (DFII10 contributed 70%, T10YIE 30%). Normalization was abruptly interrupted at end-2018 by the risk-asset selloff, forcing the Fed to pivot.

The 2022-2026 cycle stands apart from these three precedents on three markers: the contribution of term premium to the total move (estimated at 40-50% by NY Fed researchers over the 2022-2024 window), the persistence of elevated yields despite a Fed Funds pause, and the transient positive correlation between equities and bonds in stress episodes. These three markers converge on a diagnosis of monetary regime change rather than a simple hiking cycle.

4. Three misreadings to correct

DGS10 fuels contradictory interpretations across financial media. Three frequent readings deserve correction because they generate repeated analytical errors.

4.1 DGS10 as discounted sum of expected Fed Funds

The theoretical term structure formulation says the 10-year yield is the integral of expected Fed Funds over 10 years plus a term premium. This formulation is mathematically correct but operationally misleading if the second term is neglected. Between 2010 and 2021, the ACM 10-year term premium spent most of the time in negative territory (down to -100 bps in March 2020), meaning Treasury holders were paying a premium to hold them rather than the reverse — a phenomenon tied to QE programs, post-2008 safe-asset demand, and prudential regulation (Basel III required banks to hold HQLA stock, mostly Treasuries).

Since 2022, term premium has returned to positive territory, contributing directly to DGS10 levels independent of Fed Funds expectations. Conflating the two readings leads to underestimating the persistence of elevated yields even if the Fed eases. October 2023 illustrates the point: while Fed Funds futures were already pricing aggressive cuts for 2024, DGS10 rose to 5.0% because the term premium was rebuilding. The transmission mechanism through policy rates details this decomposition.

4.2 DGS10 as expected inflation

This formulation conflates the nominal yield with breakeven inflation. DGS10 is nominal, T10YIE is the inflation expectation, and the difference between them (DGS10 minus T10YIE = DFII10, the 10-year TIPS yield) is the real yield. The same middle term is broken down in the breakeven inflation component. In October 2023, the DGS10 move from 3.8% to 5.0% was driven roughly 80% by the real leg (DFII10 from 1.5% to 2.5%), and only about 20% by the inflation leg (T10YIE from 2.3% to 2.5%). Reading this move as a reawakening of inflation expectations is empirically wrong: it was first and foremost a rise in real yields.

The error has operational consequences: a move driven by real yields has different implications for asset classes than a move driven by inflation. Real assets (gold, TIPS, infrastructure) benefit from rising inflation expectations but suffer from rising real yields. Nominal assets (long Treasuries, fixed-coupon corporate bonds) suffer doubly. The DGS10 move from 3.8% to 5.0% in October 2023 translated into a positive observed correlation between equities and bonds over the 6-week window, breaking the decade-long negative correlation pattern that had supported 60/40 strategies.

4.3 Rising DGS10 as imminent recession

This reading inverts the documented causality. Historically, it is yield curve inversion (DGS10 below short rates like DGS3M or DGS2) that precedes recessions, not DGS10 rising in absolute level. A standalone rise in DGS10 is not a recession signal: it can on the contrary accompany robust growth if driven by rising real yields and a normalized term premium. The U.S. growth phases of 1962-1969, 1983-1989 and 2003-2007 were all associated with historically elevated DGS10 levels, without signaling imminent recession.

What predicts recession is the slope — not the level. The most documented signal is T10Y3M, the difference between DGS10 and DGS3M: when it flips into negative territory, a recession typically follows within 6 to 18 months as seen in the 1973, 1980, 1981, 1990, 2001, 2008 and 2020 episodes. This distinction is essential and connects directly to the broader yield-curve literature.

The level-versus-slope distinction has more than analytical importance: it is the foundation of nearly every operational recession model used by U.S. macro practitioners. The Cleveland Fed model, the NY Fed model, the Conference Board Leading Economic Index — all use yield curve slope inputs, not yield levels. Practitioners who track standalone DGS10 as a recession signal therefore work outside the documented framework, with a track record that does not stand empirical scrutiny across multiple cycles.

DGS10 is rising because markets expect more inflation. This reading is correct in roughly 30% of historical cases but wrong in the other 70%. The empirical DGS10 = DFII10 + T10YIE decomposition makes it possible to settle each episode case by case, without projecting a narrative onto the nominal yield. The October 2023 and April 2025 episodes were both dominated by the real component, not by the inflation component.

5. International transmission of DGS10

DGS10 is not only the U.S. cost-of-capital reference: it is the world’s most followed sovereign yield and indirectly structures global fixed income pricing. Three channels dominate this international transmission.

5.1 Correlations with AAA sovereign yields

The 2000-2024 correlations between DGS10 and European 10-year sovereign yields (German Bund 10Y, French OAT 10Y) are systematically positive but vary across periods: around 0.75 over the 2010-2019 decade, but reduced to 0.55-0.65 over 2020-2024 under the impact of divergent Fed/ECB monetary cycles. The Bund-Treasury spread, which was negative (Treasuries above Bund) over most of 2009-2015, fluctuated around 150-200 bps over 2022-2024 before stabilizing around 170 bps in 2025.

This transmission has one main mechanism: global bond arbitrageurs, primarily European and Japanese pension funds, smooth divergences through their cross-border allocations. When DGS10 rises faster than Bund 10Y, these investors rotate part of their allocations toward Treasuries, contributing to spread compression and pulling the Bund higher with a lag. The channel is partially neutralized by FX hedging costs, which can erode or even invert the apparent yield pickup.

5.2 Impact on emerging market yields

Investment-grade emerging market sovereign yields (Mexico, Indonesia, Poland, South Africa) follow DGS10 with a beta around 0.8-1.2. A 100 bps DGS10 rise empirically translates into an 80 to 120 bps rise in EM IG sovereign yields, depending on the episode and risk class. This transmission rests on both the demand channel (global investors require a minimum spread over Treasuries) and the FX channel (a higher DGS10 typically strengthens the dollar against EM currencies, weighing on issuer solvency for local-currency debt).

The 2022-2024 episode illustrated this mechanism: the 350 bps DGS10 rise was accompanied by an average 280 bps rise on the EMBI Global IG index, and 420 bps on the EMBI Global HY index. Several sub-investment-grade issuers were forced into restructuring (Ghana, Sri Lanka, Zambia) for which DGS10 is not the main cause but the accelerator.

5.3 Influence on savings rates and the carry trade

The DGS10 versus JGB 10Y differential (the Japanese sovereign yield long maintained under yield-curve control by the BoJ) structured the global carry trade for two decades: borrow in low-cost yen to buy higher-yielding Treasuries. The progressive normalization of Japanese YCC policy since 2022 and the JGB 10Y rise toward 1.5% in 2025 compressed this differential and triggered carry trade unwinds, most visibly in August 2024 (a brutal USD/JPY drop accompanied by global equity volatility).

The DGS10 versus Bund 10Y differential plays a similar role for euro-U.S. capital flows. When the spread widens (DGS10 higher), net flows historically rotate toward dollar assets. This mechanism accompanied the EUR/USD move from 1.18 in 2021 to 1.05 in 2022, and partially explains the dollar’s resilience despite apparent cyclical divergence.

6. Reading DGS10 over the coming quarters

DGS10 remains a central state variable of the monetary regime. Three reading angles allow characterization of each move without projecting a narrative, staying in the register of empirical observation.

6.1 Decompose every move into real and breakeven

The minimal discipline is to publish, alongside every DGS10 commentary, the DFII10 (TIPS) and T10YIE (breakeven) decomposition for the same date. A +30 bps DGS10 move over 5 days can be (i) +30 bps real / 0 breakeven (real tightening), (ii) +5 bps real / +25 bps breakeven (inflation reawakening), (iii) +15 bps real / +15 bps breakeven (mixed move). The three have very different economic implications and call for potentially opposite monetary policy responses. In depth: the delayed pass-through from rates to earnings.

The Fed publishes the three series daily (DGS10, DFII10, T10YIE) on the H.15. This decomposition is the most powerful tool for decoding a yield move without falling into the narrative trap. It has one limit worth flagging: T10YIE is not a pure measure of inflation expectations. It includes an inflation risk premium and is biased by a TIPS liquidity premium that can turn negative in stress periods (TIPS are less liquid than nominal Treasuries). The Fed also publishes the adjusted breakeven (TIPS-implied expected inflation) which removes this premium, but with a multi-week delay.

6.2 Monitor the DGS10 / Fed Funds Rate spread

The DGS10 minus Fed Funds relationship (the fix-short spread) captures the long curve slope and indirectly the term premium. A persistently negative spread signals either an anticipation of marked Fed Funds cuts ahead, or a very low term premium. The May 2026 configuration (DGS10 4.2% versus DFF 4.25-4.50%) calls for close monitoring. Across the five historical episodes where DGS10 fell below DFF, four were followed by a recession within 12 to 24 months.

Tracking the DGS10/DFF spread should be combined with tracking the T10Y3M spread. When both are negative simultaneously, the recession signal is most robust (1979, 1989, 2000, 2007, 2022-2024 episodes). When only DGS10/DFF is negative but T10Y3M is positive, the signal is ambiguous — this is the May 2026 configuration. The most prudent reading is that the signal is partially active, to be confirmed by other indicators (Sahm rule on unemployment, ISM manufacturing, credit conditions via the Senior Loan Officer Survey).

The ACM term premium published by the NY Fed is the best available proxy for the premium demanded by marginal holders. A sustained term premium rise above +75 bps would signal a structural loss of Treasury attractiveness as a safe asset, and a repricing of U.S. fiscal risk. Conversely, a term premium compression into negative territory would signal either a return of foreign demand or a new QE cycle.

Qualitative tracking goes through the quarterly Treasury Borrowing Advisory Committee reports, which publish bid-to-cover ratios on Treasury auctions, allocations to dealers, primary investors and indirect bidders. A persistent drop in bid-to-cover on 10-year auctions, paired with a rise in dealer take-up, is a leading signal of long-end demand stress that transmits to DGS10 within a few weeks.

6.4 Articulate with the full curve

DGS10 in isolation is not enough. A coherent reading integrates DGS3M, DGS2, DGS5, DGS30 to capture the full curve shape. A DGS10 stable around 4% can mask a 2s10s steepening or a 10s30s flattening that radically change the macroeconomic interpretation. Cycle-signal models (CFR Recession Probability Model, NY Fed Term Spread Model) typically use T10Y3M rather than standalone DGS10 for that reason. Data reference: The yield-curve inversion series.

Reading by curve segments also allows identification of specific messages. A 2s10s steepening at the start of a Fed Funds cutting cycle typically signals an expected recession with a substantial fiscal and monetary response. A 10s30s flattening, conversely, signals deterioration of long-term expectations on growth or fiscal stability. These messages are distinct and complementary, each calling for a different macro reading grid. Our guide to steepeners and flatteners walks through each case.

Full-curve monitoring also integrates stress indicators: MOVE Index (Treasury option implied volatility), bid-ask spreads on on-the-run Treasuries, primary dealer take-up as a percentage of auction allocations. When these indicators deteriorate simultaneously, the published DGS10 becomes an increasingly noisy proxy of the true macroeconomic pricing. The March 2020, March 2023 (post-SVB) and October 2023 stress episodes all combined simultaneous deterioration of these indicators with a marked DGS10 move, justifying never reading the 10-year yield in isolation from the market conditions producing it.

The relationship between DGS10 and the 5-year U.S. sovereign CDS, long anecdotal, has become more significant since the May 2023 debt ceiling episode. The 5Y U.S. CDS, which traded below 30 bps over 2014-2021, rose to 165 bps in May 2023 before falling back toward 40-50 bps after the political agreement. This CDS volatility introduces a new sovereign risk premium component into DGS10 that did not exist in earlier regimes.

One under-appreciated property of DGS10 is its function as a coordination device across heterogeneous market participants. Hedge funds running basis trades, pension funds matching long liabilities, bank treasuries managing HQLA stocks, foreign reserve managers, retail BondLadder investors — all consult DGS10 as their common reference point, even when their actual transactions occur in different segments of the curve. This convergence makes DGS10 the most resilient public macro signal available, in the sense that no single category of participants can durably distort its level without provoking opposing flows from another category.

DGS10 is not a passive thermometer of U.S. macro: it is the active channel through which all monetary policy and all fiscal trajectories translate into the cost of capital.

7. DGS10 as a state variable of the monetary regime

The 1962-2026 DGS10 sequence tells the story of three successive monetary regimes, readable in the real/breakeven decomposition and in the relationship to Fed Funds. The 1962-1981 regime was dominated by drifting inflation expectations until the Volcker shock. The 1981-2021 regime was that of disinflation, then post-2008 monetary repression that pushed the term premium into negative territory. The regime opened in 2022 combines natural rate repricing, fiscal risk reintroduction, and positive term premium.

Each regime corresponds to a different DGS10 elasticity to underlying variables. In the 1962-1981 regime, DGS10 reacted strongly to CPI surprises: one point of inflation surprise translated into 30-50 bps of DGS10 rise within weeks. In the 1981-2021 regime, it reacted more to Fed Funds decisions and QE announcements, with a Fed Funds to DGS10 elasticity of roughly 0.3-0.5 over the 1994, 1999, 2004 and 2015 cycles. In the post-2022 regime, it incorporates a fiscal component absent from the two previous ones, and the Fed Funds to DGS10 elasticity falls to 0.5-0.7 on the upleg of the 2022-2023 cycle but becomes nearly zero or even negative in the anticipated easing phases.

Reading DGS10 is therefore not about comparing its level to a long-term historical average: it is about identifying the regime one is in and applying the appropriate reading grid. This regime identification, more than any level forecast, is the central challenge of fixed income analysis in 2026. The tools remain the same — real/breakeven decomposition, term premium monitoring, full-curve articulation — but their interpretation shifts with the identified regime.

The likely persistence of a post-2022 monetary regime distinct from previous decades implies that mental anchors built on 2010-2021 (DGS10 capped around 3%, negative term premium, mortgage rates below 4%) must be revised. The ongoing repricing is not a cyclical anomaly to correct: it is a normalization toward an equilibrium level consistent with the new r-star, fiscal and demographic configuration. The implications extend well beyond the Treasury market alone and touch the entire U.S. macroeconomic pricing complex.

For 2026 macro analysis and beyond, three open questions will structure the reading of DGS10. First, how far can the upward revision of r-star continue, and what macroeconomic conditions (productivity, demographics, deficits) would stabilize it? Second, how does the term premium evolve as a function of the U.S. fiscal trajectory and the composition of Treasury demand by investor cohort? Third, under what conditions would the equity/bond correlation flip durably from positive (inflationary regime) to negative (disinflationary regime), with implications for diversified portfolios?

Each of these questions extends beyond DGS10 alone but is directly observable in its decomposition and dynamics. The 10-year yield is therefore not the solution to a macro problem but the most consolidated dashboard for tracking the progressive resolution of these structural uncertainties. It is this synthetic function, more than any standalone figure, that justifies the singular status of DGS10 in U.S. and global macro-finance.

This regime-identification approach has practical implications for portfolio construction and macro communication. For portfolio construction, it means that duration risk in 2026 cannot be assessed by reference to 2010-2019 volatility regimes — current DGS10 volatility, conditional on the fiscal and term premium configuration, is structurally higher. For macro communication, it means that headline DGS10 movements should always be reported with their TIPS/breakeven decomposition; reporting DGS10 alone, as is still common in financial media, leaves the reader without the information needed to assess whether the move is real-rate driven or inflation-driven, with very different policy implications.

The post-2022 regime also reopens questions that were considered settled during the QE era. The relationship between DGS10 and the U.S. dollar’s reserve currency status, treated as exogenous over 2010-2021, has become a live empirical question as fiscal trajectories deteriorate and as alternative reserve assets gain marginal share. The transmission channels from DGS10 to mortgage rates, corporate bond yields and emerging market sovereign yields, treated as stable empirical relationships, have shown structural breaks since 2022 that warrant ongoing monitoring rather than assumed constants. Also relevant: Monetary Transmission to Corporate Earnings: Time Lags, Margins, and Rate-Cycle Effects.

- DGS10 is a daily Constant Maturity construction published by the Fed in the H.15 release, not the yield of an identifiable Treasury bond, which implies a smoothing of on-the-run versus off-the-run tensions.

- Four economic functions: discount rate for long-term valuations, anchor for mortgages and corporate bonds, primary input of financial conditions indices, signal of long-term expectations through the TIPS + breakeven decomposition.

- The 2022-2026 repricing combines r-star revision (from ~0.4% to ~1%), fiscal risk reintroduction (deficit ~6.5% of GDP, debt/GDP ~120%), and positive term premium (+60 bps end-2023) — three factors absent from earlier cycles.

- Three misreadings to avoid: DGS10 as pure sum of expected Fed Funds (ignores term premium), DGS10 as proxy for expected inflation (conflates nominal and real), rising DGS10 as recession signal (it is the slope that predicts, not the level).

- The operational reading grid decomposes every move into TIPS + breakeven, monitors the DGS10 minus Fed Funds spread and the ACM term premium, and articulates DGS10 with the rest of the curve (DGS3M, DGS2, DGS30).

Last updated — 12 July 2026

Disclaimer – Financial Information: The analyses, commentary, and content published on eco3min.fr are provided for informational and educational purposes only. They do not constitute investment advice or a solicitation to buy or sell financial instruments. Past performance is not indicative of future results. All investment decisions involve risk and are the sole responsibility of the reader.

Read next

Full pillar →Real Interest Rates: The Quiet Signal Reshaping Markets

Real interest rates: why their persistence in positive territory in 2026 is reshaping the rules for bonds, equities,…

OAT-Bund Spread: A Quiet Gauge of French Sovereign Risk

OAT-Bund spread: how this yield gap has become a key signal on French sovereign risk, fiscal policy and…

Inverted Yield Curve: Reading a Regime Signal Without Immediate Effect

The inverted yield curve operates as a regime signal, not a timing tool. Its lagged effects are constitutive…